Commercial Aircraft Fire, Ice & Rain Protection Aftermarket Size, Share & Industry Analysis, By Component (Fire Protection (Fire Detectors, Extinguishing Bottles, Fire Control Units, and Predictive & Smart Tech) and Ice & Rain Protection (Heating & De-Icing Systems, Ice Detection & Sensing Systems, Windshield & Radome Technologies, and Water Line), By Offering (MRO Services and Refurbished Parts), By Aircraft Family (Airbus A220, Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, & Others), and Regional Forecast, 2025-2045

Commercial Aircraft Fire, Ice & Rain Protection Aftermarket Size and Future Outlook

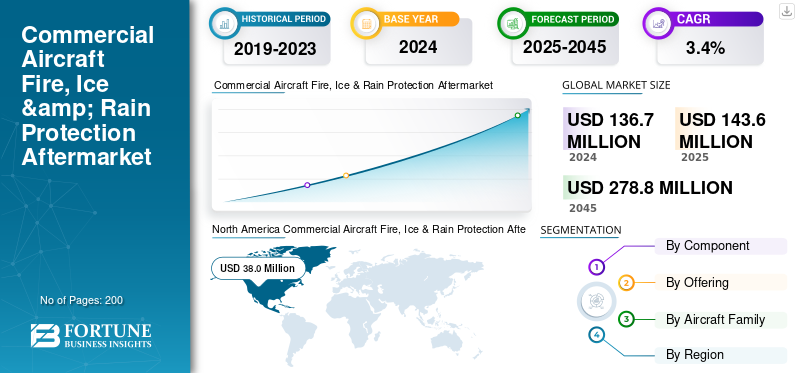

The global commercial aircraft fire, ice & rain protection aftermarket size was valued at USD 136.7 million in 2024. The market is projected to grow from USD 143.6 million in 2025 to USD 278.8 million by 2045, exhibiting a CAGR of 3.4% during the forecast period. North America dominated the global commercial aircraft fire, ice & rain protection aftermarket with a market share of 27.80% in 2024.

The commercial aircraft fire, ice & rain protection aftermarket covers the maintenance, repair, overhaul, and certified refurbishment of anti-ice systems, safeguarding aircraft against in-flight hazards. This includes fire protection (detection loops, extinguishers, cylinders), ice protection (pneumatic boots, TKS fluid systems, electro-thermal heaters), and rain protection (windshield wipers, hydrophobic coatings, heating elements). The market is shaped by rising fleet utilization, regulatory mandates, and the shift toward refurbishment as a cost-effective alternative to OEM replacements. With airlines facing cost pressures and sustainability mandates, demand for eco-friendly de-icing fluids and predictive maintenance-enabled servicing is steadily accelerating.

Furthermore, the market encompasses several major players with Collins Aerospace, Honeywell Aerospace, Thales Group, and Safran Electronics & Defense at the forefront. A broad portfolio of innovative products, along with strong geographic presence expansion, has supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Commercial Aircraft Fire, Ice & Rain Protection Aftermarket Key Takeaways

- 2024 Market Size: USD 136.7 million

- 2025 Market Size: USD 143.6 million

- 2045 Forecast Market Size: USD 278.8 million

- CAGR: 3.4% from 2025–2045

- North America dominated the market with a 27.80% share in 2024.

- Ice & Rain Protection dominated the market, valued at USD 73.7 million in 2024.

- MRO Services dominated the market with over 95% share in 2025.

North America

Valued at USD 38.0 million in 2024, projected to grow steadily with strong MRO demand.

Asia Pacific

Fastest-growing region, supported by rapid fleet expansion and increasing A320neo deliveries.

Europe

Mature MRO hub driven by stringent EASA regulations and eco-friendly de-icing adoption.

U.S.

Growth driven by fleet modernization, smart diagnostics, and electrothermal ice protection systems.

Japan

The Japan market is driven by technological advancements and innovation.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Fleet Growth and Harsh Weather Leading to Higher MRO Demand, Fueling Market Expansion

Airlines are increasingly prioritizing predictive maintenance solutions to reduce aircraft downtime and prevent costly AOG (Aircraft on Ground) events. Advanced diagnostic systems integrated with AI and IoT enable real-time monitoring of avionics, engines, and control systems, driving efficiency and safety. This trend is particularly strong in large fleets where aircraft operational reliability is critical. For example, in March 2025, Emirates partnered with Honeywell to deploy predictive health monitoring systems across its Boeing 777 fleet, enabling data-driven diagnostics to reduce unplanned maintenance events. Such investments highlight how predictive capabilities are fueling MRO demand and the adoption of refurbished diagnostic components.

MARKET RESTRAINTS

Regulatory Complexity Raising Cost and Downtime, Hinders Market Growth

Strict FAA and EASA mandates for fire suppression bottles, thermal blankets, and de-icing fluids, while ensuring safety, significantly raise MRO costs. Certified refurbished parts face long approval timelines, and operators often depend on OEM-approved centers, creating supply bottlenecks. Environmental restrictions on glycol-based fluids in Europe and North America add compliance burdens, increasing airlines' operational costs. Limited global capacity of specialized MRO providers leads to longer turnaround times and aircraft-on-ground risks. Thus, while regulation ensures airworthiness, it inadvertently restricts market flexibility, slows the adoption of refurbishment, and increases operator reliance on costly OEM-supplied parts.

MARKET OPPORTUNITIES

Eco-Friendly Fluids and Digital MRO Driving Growth

The market presents major opportunities in eco-friendly de-icing fluids and digitally enabled MRO solutions. As airports tighten environmental regulations, demand is rising for biodegradable or non-glycol-based alternatives, opening space for new fluid suppliers and refurbishment centers specializing in sustainable solutions. Digitalization further enhances opportunity, with predictive maintenance, IoT-enabled sensors, and deicing condition-monitoring tools reducing downtime and optimizing part lifecycles. Emerging markets in Asia Pacific are expanding their MRO hubs, creating opportunities for OEMs and third-party service providers to establish localized facilities. Together, sustainability mandates and digital tools create profitable avenues for growth in both components and refurbishment services.

MARKET CHALLENGES

Supply Chain Gaps and Seasonal Spikes Hinder Market Growth

A major challenge in the commercial aircraft fire, ice & rain protection aftermarket growth is supply-chain vulnerability and seasonal demand surges. Limited global capacity to refurbish de-ice boots, fire bottles, and windshield systems results in long turnaround times, especially during peak winter operations. Airlines often face Aircraft-on-Ground (AOG) delays due to parts shortages, leading them to rely on refurbished components. Environmental rules restricting the use of glycol-based fluids in Europe further complicate logistics and raise compliance costs.

In July 2024, AAR extended its agreement with Collins Aerospace to distribute de-icing components globally, highlighting the aftermarket’s growing reliance on third-party distributors to mitigate supply-chain risk.

COMMERCIAL AIRCRAFT FIRE, ICE & RAIN PROTECTION AFTERMARKET TRENDS

Hybrid Systems Transforming Maintenance Needs

Technological advancements are reshaping the MRO landscape for fire, ice, and rain protection. Hybrid electro-thermal systems are gradually replacing pneumatic boots, reducing mechanical wear but requiring advanced diagnostics and digital maintenance platforms. Fire suppression is moving toward lighter, halon-free alternatives, requiring technicians to adapt to new materials and refill processes. Rain protection is evolving with electrically heated windshields and hydrophobic coatings that extend replacement cycles. Integration of AI-driven monitoring enables predictive maintenance, helping airlines minimize AOG events. These innovations shift MRO demand from routine replacements toward specialized digital maintenance, creating a new wave of aftermarket services.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

High Demand for Safety Roles Contributed to Ice & Rain Protection Segment Growth

On the basis of component, the market is classified into fire protection and ice & rain protection.

The ice & rain protection segment leads the segment, accounting for a dominant market share and reaching USD 73.7 million in 2024, driven by its high operational frequency and critical safety role across regional, narrowbody, and turboprop fleets. Pneumatic boots, TKS systems, and windshield heating require recurring inspections, replacements, and servicing, especially in icing-prone geographies. Seasonal surges in North America and Europe amplify MRO demand, while Asia Pacific’s growing fleets add further pressure. Unlike fire systems with longer service cycles, de-icing and rain systems face continuous wear, driving higher spend.

- In July 2024, AAR expanded its Collins Aerospace agreement to include the distribution of de-icing components, addressing surging aftermarket demand.

By Offering

Increasing Focus on Preventive Maintenance and Inspection Fueled MRO Services Segment Growth

In terms of offering, the market is categorized into MRO services and refurbished parts.

The MRO services segment captured the largest commercial aircraft fire, ice & rain protection aftermarket share in 2024. In 2025, the segment accounted for over 95% of the market. MRO services dominate over refurbished parts, as fire suppression bottles, de-icing boots, and windshield heating elements have fixed maintenance intervals under FAA/EASA regulations. Airlines prioritize scheduled MRO to minimize AOG risks, with many opting for OEM-authorized centers despite higher costs. Seasonal checks, mandatory inspections, and repetitive part servicing make MRO revenue larger and more predictable than refurbished spares. The trend is reinforced by digital diagnostic systems enabling predictive maintenance, which increases recurring service activity.

- In 2023, Lufthansa Technik reported record MRO demand in Europe for critical aircraft systems, including de-icing and windshield heating, highlighting MRO’s dominance.

To know how our report can help streamline your business, Speak to Analyst

By Aircraft Family

Airbus A320 Family (ceo/neo) Segment Led Market Due to Its Massive Global In-Service Fleet Exceeding 9,000 Aircraft

Based on aircraft family, the market is segmented into Airbus A220, Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, De Havilland Dash 8 (Q-Series), Embraer E-Jets (E1/E2), and Sukhoi Superjet 100.

The Airbus A320 Family (ceo/neo) segment held the dominating position in 2024. The Airbus A320 Family (ceo/neo) dominates demand for fire, ice, and rain protection MRO due to its massive global in-service fleet, which exceeds 9,000 aircraft. High daily utilization rates, short-haul frequency, and extensive operations across diverse climates accelerate wear on de-icing and rain protection systems. Airlines rely on frequent maintenance of windshields, wipers, and boot assemblies to ensure dispatch reliability. As A320neo deliveries ramp up, aftermarket demand will remain dominant for decades.

- In 2025, Airbus reported its A320 Family backlog surpassing 6,000 aircraft, solidifying the segment’s aftermarket dominance in protection systems.

Commercial Aircraft Fire, Ice & Rain Protection Aftermarket Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America & Africa, and the Middle East.

North America

North America Commercial Aircraft Fire, Ice & Rain Protection Aftermarket Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2023, valued at USD 37.5 million, and also led in 2024, with USD 38.0 million. North America dominates due to its large fleet size, harsh winter conditions, and strong regulatory oversight. Seasonal icing drives heavy demand for de-icing fluid services, boot refurbishment, and windshield heating system repairs. Airlines increasingly rely on established MRO hubs and distributors for quick turnarounds. The presence of key OEMs, such as Collins Aerospace, and leading aftermarket providers, such as AAR, ensures steady supply chain support. The U.S. market for fire, ice, and rain protection for commercial aircraft is growing steadily. This growth is driven by an aging fleet, more air travel, and the need to modernize for better safety and efficiency. The market is moving toward new technologies, including electrothermal ice protection, smart diagnostics, and eco-friendly, high-performance fire extinguishing agents.

- In July 2024, AAR expanded its global distribution agreement with Collins Aerospace to supply de-icing components, reinforcing North America’s leadership in aftermarket support.

Europe

Europe and Asia Pacific collectively represent high-growth regions. Europe remains a mature MRO hub, driven by stringent EASA safety mandates and early adoption of eco-friendly de-icing fluids. Seasonal operations in Scandinavia and Central Europe reinforce demand, while refurbishment gains traction as airlines cut costs.

Asia Pacific

Asia Pacific is the fastest-growing market, led by rapid fleet expansion in China and India and rising low-cost carrier penetration. Regional MRO capacity is expanding, though operators often depend on OEM-certified centers.

- In 2025, Airbus reported record A320neo deliveries in Asia Pacific, further boosting demand for MRO for ice and rain protection in growing fleets.

Latin America & Africa and Middle East

Over the forecast period, the Latin America & Africa and Middle East regions would witness moderate growth in this market space. The Latin America & Africa market in 2025 is set to reach USD 11.4 million in valuation. These regions represent smaller shares but exhibit niche growth. Latin America’s regional turboprops and short-haul fleets generate steady demand for de-icing boots and fire bottle servicing. Africa’s MRO activity remains limited but is rising as fleets modernize. The Middle East shows steady growth, largely driven by widebody-heavy fleets operated by Gulf carriers that require fire-suppression MRO. Hot weather reduces icing demand, but compliance-driven fire protection maintenance remains significant.

COMPETITIVE LANDSCAPE

Key Industry Players

A Wide Range of Product Offerings Coupled with Strong Distribution Network of Key Companies Supported Their Leading Positions

The aircraft fire, ice & rain protection aftermarket is moderately consolidated, with a mix of OEMs, Tier-1 suppliers, and aftermarket providers shaping competition. Collins Aerospace (Raytheon Technologies) and Safran dominate with comprehensive product portfolios spanning fire detection, suppression systems, and de-icing technologies. Liebherr-Aerospace provides advanced ice protection solutions, particularly for Airbus and regional aircraft.

CAV Ice Protection specializes in TKS fluid-based systems for general aviation and regional turboprop aircraft. On the aftermarket side, AAR Corp. strengthens its position through global distribution agreements, such as its 2024 expansion with Collins Aerospace for de-icing components. Independent MROs and regional providers compete on cost-effective refurbished parts, especially in Europe and Asia Pacific, where airlines seek alternatives to high OEM pricing. The competitive focus is shifting toward eco-friendly fluids, halon-free fire suppression, and predictive digital diagnostics, with OEMs leveraging certification advantages. At the same time, independents target quick turnaround times and lower life-cycle costs.

LIST OF KEY COMMERCIAL AIRCRAFT FIRE, ICE & RAIN PROTECTION AFTERMARKET COMPANIES PROFILED

- Collins Aerospace (U.S.)

- Honeywell Aerospace (U.S.)

- Thales Group (France)

- Safran Electronics & Defense (France)

- Liebherr-Aerospace (Germany)

- Moog Inc. (U.S.)

- Parker Aerospace (U.S.)

- Spirit AeroSystems (U.S.)

- ST Engineering Aerospace (Singapore)

- Lufthansa Technik (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2024: Air Canada equipped A320 aircraft with a pilot-controlled induction tape de-icing system, eliminating the need for hot-fluid ground spraying and improving turnaround efficiency.

- September 2024: Vestergaard launched its OPTIM-ICE system, which uses LIDAR to detect surface ice and guide automated de-icing nozzles, improving the speed and accuracy of operations.

- February 2024: CTV News Edmonton reported that Alberta-based Pegasus developed MIDAS, or the Motion Icing Detection Alert System, for real-time detection of icing buildup. This work caught Boeing’s attention and involved collaboration with the company. MIDAS was already operational on Canada’s CH-147 Chinook fleet.

- December 2023: Air Canada became the first airline to trial a high-frequency electric de-icing solution on its Airbus A320 fleet, reducing winter departure delays and carbon emissions by replacing traditional glycol spraying with electric current.

- October 2023: CAV Systems published an update saying it had registered a trademark for TKS 406 BIO, a bio-derived, biodegradable de-icing fluid used with its TKS in-flight anti-ice and de-ice system. It will be delivered through laser-drilled titanium panels, with a launch planned for January 2024.

- September 2023: Vilnius Airport inaugurated the Baltic States’ first de-icing wastewater treatment plant, reflecting the industry’s shift toward eco-friendly de-icing infrastructure and regulatory compliance.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2045 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2045 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 3.4% from 2025-2045 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component, Offering, Aircraft Family, and Region |

|

By Component |

· Fire Protection o Fire Detectors o Extinguishing Bottles o Fire Control Units o Predictive & Smart Tech · Ice & Rain Protection o Heating & De-Icing Systems o Ice Detection & Sensing Systems o Windshield & Radome Technologies o Water Line |

|

By Offering |

· MRO Services · Refurbished Parts o PMA o USM |

|

By Aircraft Family |

· Airbus A220 · Airbus A320 Family (ceo/neo) · Airbus A330 (ceo/neo) · Airbus A350 · Airbus A380 · ATR 42/72 · Boeing 737 Family (Classic/NG/MAX) · Boeing 747 · Boeing 767 · Boeing 777 · Boeing 787 · Bombardier CRJ Series · COMAC C919 · De Havilland Dash 8 (Q-Series) · Embraer E-Jets (E1/E2) · Sukhoi Superjet 100 |

|

By Region |

· North America (By Component, Offering, Aircraft Family, and Country) o U.S. o Canada · Europe (By Component, Offering, Aircraft Family, and Country) o Germany o U.K. o Germany o France o Russia o Rest of Europe · Asia Pacific (By Component, Offering, Aircraft Family, and Country) o China o India o Japan o Australia o Rest of Asia Pacific · Latin America & Africa (By Component, Offering, Aircraft Family, and Country) o Brazil o Mexico o Rest of Latin America · Middle East (By Component, Offering, Aircraft Family, and Country) o UAE o Saudi Arabia o South Africa o Rest of Middle East |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 136.7 million in 2024 and is projected to reach USD 278.8 million by 2045.

In 2024, the market value in North America stood at USD 38.0 million.

The market is expected to exhibit a CAGR of 3.4% during the forecast period of 2025-2045.

The MRO services segment led the market by offering.

Fleet growth and harsh weather are leading to higher MRO demand.

Collins Aerospace (U.S.), Honeywell Aerospace (U.S.), and Thales Group (France) are some of the prominent players in the market.

North America dominated the market in 2024.

- 2019-2045

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us