Commercial Lending Market Size, Share & Industry Analysis, By Loan Type (Term Loans, Commercial Loans, Equipment Finance, Invoice Financing, and Others), By Borrowers Type (Micro Businesses, SMEs, Large Enterprises, and Commercial & Institutional Borrowers), By End User (Manufacturing, Construction & Real Estate, Wholesale & Distribution, Retail & E-commerce, IT & Telecom, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

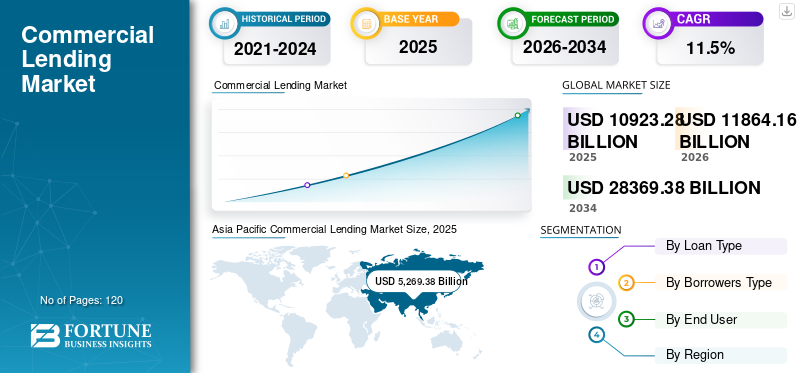

The global commercial lending market size was valued at USD 10,923.28 billion in 2025. The market is projected to grow from USD 11,864.16 billion in 2026 to USD 28,369.38 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period. Asia Pacific dominated the global commercial lending market with a market share of 48.23% in 2025.

The market is seeing steady expansion, supported by corporate capex cycles, working-capital needs (inventory and receivables), and infrastructure and real estate financing requirements. Borrowers are increasingly prioritizing speed, certainty of funding, and flexible structures (revolvers, asset-based lending, syndicated facilities), while lenders are responding with digitized origination, automated credit decisions for smaller tickets, and stronger risk-based pricing and covenanting. Parallely, tighter supervisory focus on credit risk, concentration limits (especially in CRE), and climate risk governance is pushing lenders to upgrade underwriting models and portfolio monitoring.

- For instance, In January 2025 the U.S. Federal Reserve’s Senior Loan Officer Opinion Survey reports stronger demand for commercial and industrial (C&I) loans to large and middle-market firms, showing improving appetite for core business credit even as standards remained cautious.

Furthermore, leading lenders such as JPMorgan Chase, Bank of America, Wells Fargo, Citigroup, RBC, HSBC, BNP Paribas, and MUFG are prioritizing digital distribution for business borrowers, improving early-warning systems and portfolio analytics, and expanding specialized lending desks (asset-based lending, equipment finance, supply chain finance, and syndicated lending) to better match evolving borrower requirements and risk-return targets.

Download Free sample to learn more about this report.

COMMERCIAL LENDING MARKET TRENDS

Rising Demand for Private Credit is a Prominent Trend Observed in Market

Rising demand for private credit is becoming a prominent trend in the commercial lending market as corporates and sponsor-backed businesses are looking for funding options beyond traditional banks. Private credit funds and direct lenders often provide faster execution, larger ticket sizes, and more flexible deal structures than bank loans, which is an attractive option during tighter bank underwriting. This channel has expanded rapidly as investors allocate more capital to private debt in search of stable yields, enabling funds to scale origination and compete directly with banks.

In parallel, many borrowers prefer private credit because it can offer customized covenants and tailored repayment profiles, especially for complex or time-sensitive transactions. The growth of private credit is also influencing pricing dynamics, pushing banks to focus on relationship-led lending and specialized products. Overall, private credit is reshaping the competitive landscape by widening access to capital and diversifying sources of corporate funding.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Working-Capital Requirements is Propelling the Adoption for Commercial Lending

Rising working-capital requirements are propelling the adoption of commercial lending as businesses increasingly need reliable liquidity to manage day-to-day operations. Companies often face longer receivables cycles, seasonal sales fluctuations, and the need to maintain higher inventory levels, which can strain cash flows even when revenues are stable.

- For instance, in February 2025, As per industry analysis, banks reported a net increase in demand for business loans in 2024, including demand for C&I loans across firm sizes, showing that companies were actively seeking liquidity to support operational requirements.

Commercial lending products such as revolving credit facilities, short-term working-capital loans, and asset-based lending help firms bridge these gaps and continue operating without disruption. This demand is especially strong in wholesale, distribution, manufacturing, and retail segments where inventory and payment cycles are critical. As supply chains remain complex, many firms also require additional financing to secure raw materials, manage shipping timelines, and avoid stock-outs.

MARKET RESTRAINTS

High Interest Rates and Elevated Borrowing Costs Restrict the Market Growth

High interest rates and elevated borrowing costs are restricting the commercial lending market growth by reducing the willingness of businesses to take on new debt. As lending rates rise, debt servicing becomes more expensive, prompting companies to delay capital expenditure, expansion plans, and large asset purchases. Higher rates also increase repayment risk, leading borrowers to prefer shorter tenors or rely more on internal cash flows.

From the lender side, elevated rates raise default risk expectations, encouraging more conservative credit assessments and tighter loan terms. Small and mid-sized enterprises are particularly affected, as higher pricing and collateral requirements limit their access to affordable financing. Overall, sustained high borrowing costs dampen loan demand and slow credit growth across multiple commercial segments.

MARKET OPPORTUNITIES

Rising Digitalization of Lending and Faster Underwriting to Offer Market Growth Opportunities

Rising digitalization of lending and faster underwriting are creating strong growth opportunities in the market by improving efficiency and accessibility. Digital platforms enable lenders to automate credit assessments, document verification, and risk scoring, significantly reducing loan approval timelines. Advanced data analytics and AI-driven models allow lenders to evaluate borrower risk more accurately using real-time cash flow and transaction data. This is particularly beneficial for small and mid-sized businesses that require quick access to working capital. As a result, lenders can offer more competitive and customized financing structures while maintaining credit discipline. Digital channels also lower operational costs and expand geographic reach without relying on branch-based networks. In addition, improved transparency and monitoring tools enhance portfolio management and early risk detection.

Segmentation Analysis

By Loan Type

Rising Need for Commercial Loans for Broad Applicability Across Business Needs Propelled Segmental Growth of Commercial Loans

Based on the loan type, the market is divided into term loans, commercial loans, equipment finance, invoice financing, and others.

Commercial loans accounted for the largest market share due to their broad applicability across business needs such as working capital, expansion funding, refinancing, and day-to-day liquidity management. These loans are widely adopted by large enterprises and mid-market firms because they can be structured as revolving facilities or term-based borrowing, offering flexibility based on cash-flow cycles.

- For instance, in January 2025, the U.S. Federal Reserve’s Senior Loan Officer survey reported a stronger demand for C&I loans from large and middle-market firms, reflecting higher reliance on core commercial borrowing.

Invoice financing is anticipated to rise with a CAGR of 16.2% over the forecast period due to faster SME credit adoption, increasing use of receivables-backed funding, and rising preference for short-cycle liquidity tools that reduce cash conversion stress.

By Borrowers Type

Rising Need by Large Enterprises Due to Diverse Cash Flows to Propel Segmental Growth

Based on the borrowers type, the market is divided into micro businesses, SMEs, large enterprises, commercial & institutional borrowers.

Large enterprises accounted for the largest commercial lending market share mainly due to their borrowing being in higher ticket sizes and use multiple facilities such as revolving credit, term loans, syndicated loans, and trade finance across geographies. Their stronger audited financials, diversified cash flows, and established banking relationships improve credit eligibility and enable lenders to deploy larger limits with better risk visibility. Large corporates also refinance and restructure debt more frequently, which sustains lending volumes even during slower capex cycles.

SMEs is anticipated to rise with a CAGR of 15.3% over the forecast period driven by expanding formalization of small businesses, increasing need for working-capital finance, and improved access to credit through digital onboarding and faster underwriting.

By End User

To know how our report can help streamline your business, Speak to Analyst

Rising Large Ticket and Long Tenor Financing by Construction and Real Estate to Boost Segment Growth

Based on end user, the market is segmented into manufacturing, construction & real estate, wholesale & distribution, retail & e-commerce, IT & telecom, and others.

In 2025, the construction & real estate dominated the global market as the sector typically has large ticket and long-tenor financing through construction loans, developer credit, commercial mortgage lending, and project-based funding. This dominance is also supported by the capital-intensive nature of real estate development, frequent refinancing cycles, and continued need for funding across residential, industrial, logistics, and mixed-use projects.

- For instance, in November 2025, the Mortgage Bankers Association reported that commercial and multifamily mortgage loan originations were 36% higher in Q3 2025 compared to previous year, highlighting a clear rebound in property linked financing activity.

IT & telecom is projected to grow at a CAGR of 16.7% over the forecast period due to rising investments in digital infrastructure such as cloud data centers, fiber rollout, 5G upgrades, enterprise connectivity, and AI-driven compute expansion.

Commercial Lending Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Commercial Lending Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valuing at USD 4,818.82 billion, and also maintained the leading share in 2025 with USD 5,269.38 billion. The Asia Pacific market growth is driven by a combination of structural and credit demand factors that are stronger than most other regions. The region has a large and expanding base of manufacturing, export-oriented industries, and domestic consumption, which consistently increases demand for working-capital finance such as revolving credit and short-term corporate loans.

China Commercial Lending Market

The China market in 2025 was estimated at around USD 1,329.50 billion, accounting for roughly 12.0% of global market revenues. This growth is attributed to large base of manufacturing and industrial enterprises that continuously require working-capital facilities to finance raw materials, inventory, and receivables. Additionally, ongoing investments in infrastructure, utilities, logistics networks, and industrial upgrading sustain demand for long-tenor project finance and term lending in China.

Japan Commercial Lending Market

Japan’s market is projected to be one of the largest globally, with 2025 revenues estimated at around USD 1,158.05 billion, representing roughly 11% of global market sales.

India Commercial Lending Market

The India market in 2025 was estimated at around USD 1,136.97 billion, accounting for roughly 10% of global market revenues.

North America

North America is projected to record a growth rate of 8.2% in the coming years, which is the second highest among all regions, and reach a valuation of USD 2,892.50 billion by 2025. North America’s commercial lending growth is driven by sustained demand for working-capital financing as businesses manage inventory cycles, receivables, and operating liquidity needs. It is also supported by ongoing investment in industrial modernization, logistics, and digital infrastructure, which increases demand for term loans and equipment finance.

U.S Commercial Lending Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2,399.44 billion in 2025, accounting for roughly 22.0% of global market sales.

Europe

Europe is projected to record a growth rate of 7.1% in the coming years and reach a valuation of USD 1,994.62 billion by 2025. Europe’s market is driven by continued demand for working-capital financing across manufacturing, trade, and services as companies navigate cost pressures and supply-chain adjustments. The market is also supported by investments in industrial modernization, energy transition projects, and infrastructure development, which increase the demand for long-term financing. In addition, SME financing remains a key focus across the region, supported by bank programs and alternative lenders.

U.K Commercial Lending Market

The U.K. market in 2025 was estimated at around USD 434.98 billion, representing roughly 4.0% of global market revenues.

Germany Commercial Lending Market

Germany’s market was projected to reach approximately USD 423.78 billion in 2025, equivalent to around 4.0% of global market sales.

South America and Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The South America market was set to reach a valuation of USD 279.33 billion in 2025. South America and the Middle East and Africa markets are driven by rising demand for working-capital financing as businesses manage cash flow volatility and longer payment cycles. Growth is also supported by infrastructure development, energy projects, and construction activities, which require project-based and long-tenor financing. In both regions, the expanding SME base and increasing formalization of enterprises are driving demand for short-term loans and revolving credit facilities. In the Middle East & Africa, the GCC is was set to reach a value of USD 221.98 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Shift Toward Alternative Data and Cash-Flow Based Underwriting by Lenders to Propel Market Progress

Commercial lenders are increasingly shifting from traditional collateral-heavy evaluation to cash-flow based underwriting supported by alternative data sources, which is improving credit access and speeding up approvals. Banks and non-bank lenders are using transaction data, invoice records, POS sales, payroll data, and bank statement analytics to assess real repayment capacity, especially for SMEs and micro businesses that lack long credit histories. This approach reduces dependency on physical collateral and improves lending penetration in services-led sectors where assets are limited.

In addition, lenders are embedding real-time monitoring tools that track revenue trends and liquidity patterns to adjust limits and detect early stress signals. The adoption of data-driven underwriting is also enabling more flexible products such as dynamic credit lines and receivables-linked facilities.

Overall, alternative data and cash-flow analytics are helping lenders expand the addressable borrower base while maintaining stronger risk control, supporting market growth.

LIST OF KEY COMMERCIAL LENDING COMPANIES PROFILED

- Citigroup (U.S.)

- JPMorgan (U.S.)

- HSBC (U.K.)

- Mitsubishi (Japan)

- Sumitomo Mitsui Financial Group (Japan)

- Wells Fargo (U.S.)

- Industrial and Commercial Bank of China (ICBC) (China)

- Agricultural Bank of China (ABC) (China)

- China Construction Bank (CCB) (China)

- Crédit Agricole Group (France)

- Barclays (U.K.)

- UBS Group (Switzerland)

- Deutsche Bank (Germany)

- Santander (Banco Santander) (Spain)

- Royal Bank of Canada (RBC) (Canada)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Mastercard and LoanPro announced a new strategic partnership to launch Loan on Card, a solution designed to enable lenders to deliver loans to approved consumer and small business borrowers through virtual and physical card-based experiences.

- September 2025: Infinity Commercial Lending (ICL) announced a strategic joint venture with Siguler Guff, a global private markets investment firm with extensive experience in credit markets, to launch a commercial real estate lending and securitization platform.

- June 2025: FIS announced that ATLAS SP Partners and institutional borrowers and institutional investors has chosen FI’ Commercial Loan Servicing solution to help power ATLAS’ loan lifecycle processing workflows.

- June 2025: Porch Group, Inc., homeowner’s insurance company announced a renewed partnership with Goosehead Insurance. The renewed partnership with Goosehead represents help in re-activate agency partnerships and further extend its distribution channels.

- June 2025: Citi Commercial Bank enhanced its lending capabilities for mid-sized corporates by offering a streamlined digital experience. This transformation of CCB’s existing credit processes will improve ease of use for global clients while accelerating turnaround times and enhancing the overall client experience.

- February 2025:P. Morgan announced expansion to its private credit commitment. The firm allocated USD 50 billion from its balance sheet, along with nearly USD 15 billion from multiple co-lenders. This strategic move is designed to extend the firm’s direct lending capabilities and provide tailored private credit solutions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Loan Type, By Borrowers Type, By End User, and Region |

|

By Loan Type |

· Term Loans · Commercial Loans · Equipment Finance · Invoice Financing · Others |

|

By Borrowers Type |

· Micro Businesses · SMEs · Large Enterprises · Commercial & Institutional Borrowers |

|

By End User |

· Manufacturing · Construction & Real Estate · Wholesale & Distribution · Retail & E-commerce · IT & Telecom · Others |

|

By End User |

· North America (By Loan Type, By Borrowers Type, By End User and Country) o U.S. o Canada o Mexico · Europe (By Loan Type, By Borrowers Type, By End User and Country) o Germany o U.K. o France o Spain o Italy o Russia o Benelux o Nordics o Rest of Europe · Asia Pacific (By Loan Type, By Borrowers Type, By End User and Country) o China o Japan o India o South Korea o ASEAN o Oceania o Rest of Asia Pacific · South America (By Loan Type, By Borrowers Type, By End User and Country) o Brazil o Argentina o Rest of Latin America · Middle East & Africa (By Loan Type, By Borrowers Type, By End User and Country) o Turkey o Israel o GCC o South Africa o North Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 10,923.28 billion in 2025 and is projected to reach USD 28,369.38 billion by 2034.

In 2025 the market value stood at USD 5,269.38 billion.

The market is expected to exhibit a CAGR of 11.5% during the forecast period.

By End user, the construction & real estate is expected to lead the market.

Rising working capital requirements propelling the adoption in the market.

Citigroup, JPMorgan, HSBC, Mitsubishi, and Sumitomo Mitsui Financial Group are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us