Compound Chocolate Market Size, Share & Industry Analysis, By Type (Milk, Dark, and White), By Product Type (Chips, Slab, Coatings, and Other Types), By Application (Confectionery, Bakery, Dairy and Frozen Desserts, Beverages, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

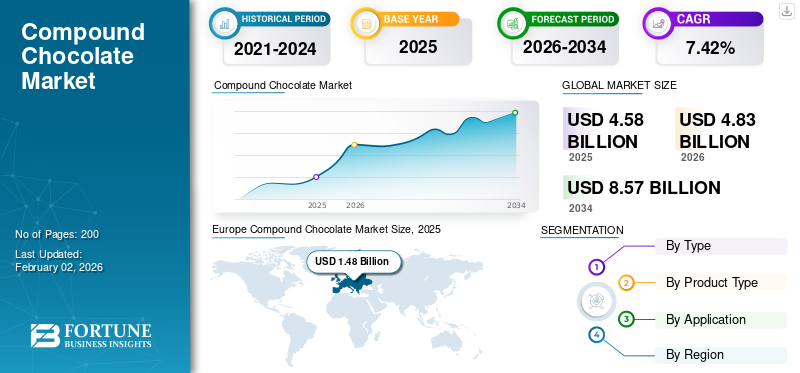

The global compound chocolate market size was valued at USD 4.58 billion in 2025. The market is projected to grow from USD 4.83 billion in 2026 to USD 8.57 billion by 2034, exhibiting a CAGR of 7.42% during the forecast period. Europe dominated the compound chocolate market with a market share of 32.18% in 2025.

Chocolate compound or compound chocolate is a cocoa-flavored fat-based coating and filling made of cocoa butter, powder, sugar, and vegetable fats. The compound is used as fillings in biscuits or cereals, as a coating on candy bars, or inside ice cream cones. The increased utilization of this chocolate form has been closely linked to the growth of the chocolate confectionery industry. Regionally, the per capita chocolate consumption in Western Europe and Asia is expected to rise considerably in the upcoming years, thereby driving the market.

Barry Callebaut, Cargill, Inc., Fuji Oil Group, Puratos Group, and Cemoi Group are prominent players operating in the market.

Download Free sample to learn more about this report.

Compound Chocolate Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 4.58 billion

- 2026 Market Size: USD 4.83 billion

- 2034 Forecast Market Size: USD 8.57 billion

- CAGR: 7.42% from 2026–2034

Market Share:

- By Region: Europe dominated the compound chocolate market with a 32.18% share in 2025, serving as a major hub for industrial chocolate production and cocoa importation.

- By Type: The milk chocolate segment is expected to hold the largest market share, favored for its sweet, creamy texture and wide appeal in various applications.

- By Application: The confectionery segment commands the largest market share, as compound chocolate's stability, versatility, and cost-effectiveness make it ideal for producing a wide range of sweets.

Key Regional Highlights:

- Europe: Market leadership is reinforced by a strong manufacturing base and a growing emphasis on sustainable and traceable cocoa sourcing, influenced by regulations like the EUDR.

- Asia Pacific: As the second-largest market, growth is rapidly accelerating due to rising middle-class discretionary spending, urbanization, and Western consumption trends in China and India.

- North America: High consumption rates and a growing consumer preference for artisanal, high-quality, and ethically sourced chocolates continue to drive significant market growth, especially in the U.S.

- Global Confectionery Demand: The overall market is fueled by the rising global demand for chocolate confectionery, particularly in emerging economies where consumer spending on indulgent treats is increasing.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Confectionery to Drive Market Growth

The demand for chocolate confectionery in emerging economies such as China, India, and others has witnessed a positive trend in recent years, attributed to rising consumer expenditure on indulgent confectionery products, especially chocolate confectionery. According to the Government of Canada, the retail sales of confectionery products in India grew from USD 2.6 billion in 2017 to USD 3.3 billion in 2021, wherein chocolate confectionery remained the largest subcategory, with retail sales of USD 1.8 billion. In the upcoming years, the confectionery sales in UAE are expected to grow tremendously, with the chocolate confectionery subsegment expected to hold the largest share, owing to the increasing popularity of fun-size, family-size, on-the-go, and other new and exotic chocolate confectionery packaging formats. Growing confectionery penetration in UAE will augment chocolate confectionery sales, further fueling the growth of the market.

MARKET RESTRAINTS

Raw Material Availability and Price Fluctuations to Limit Market Growth

The price of cocoa fluctuates highly as its production and demand vary greatly due to the dominance of a few key players in the cocoa trade, stock/grind ratios, weather patterns, labor requirements, political factors, diseases of crop yields, and others. According to the International Cocoa Organization (ICCO), the cocoa crop is affected by several pests and diseases, causing losses as high as 30% to 40% of global production. Lower stockpiles, delayed cocoa transport to ports (and hence different regions), unfavorable weather conditions such as drought or heavy rain, and political variability can contribute to increasing cocoa prices and cocoa ingredients. Suitable weather conditions, higher stockpiles, a decline in demand from processors, and the distribution of subsidized crop cultivation inputs to farmers may lead to decreased prices of cocoa and cocoa ingredients, hampering the expansion of the market.

MARKET OPPORTUNITIES

Increasing Focus on Sustainably Sourced Chocolate Products to Provide Growth Opportunities for Market Players

Major giants of cocoa and chocolate around the world, such as Olam International, Barry Callebaut, Cargill Inc., and others, have increased their efforts to improve sustainability in cocoa production and to achieve environmental goals such as reduction in deforestation, improvement in water management, and the adoption of good agricultural practices. Consumers' increased demand for certified and traceable cocoa products and chocolates is encouraging market players in the industry to opt for cocoa sustainability programs.

- UTZ Certification, Rainforest Alliance Certification, and Fair Trade USA certification are the most prominent certifications for cocoa, and in recent years, their adoption has increased incredibly.

- According to the Centre for the Promotion of Imports from developing countries (CBI), the global estimated production of Rainforest Alliance-certified cocoa beans amounted to 1.4 million tons in 2021.

COMPOUND CHOCOLATE MARKET TRENDS

Rising Trend of Plant-Based and Vegan Foods to Fuel Market Expansion

Consumers prefer dairy-free and vegan foods owing to rising ethical, environmental, and animal concerns, boosting the market growth. This trend has also been reflected in the compound chocolate industry, indicating a strong move toward vegan options. According to ProVeg International, a non-governmental organization, in 2020, 62% of consumers in Germany purchased plant-based chocolate and baked goods. Manufacturers are, therefore, increasingly focused on developing vegan-friendly options to appeal to ethical and health-conscious consumers, further broadening the market potential.

Segmentation Analysis

By Type

Sweet and Creamy Texture to Impel Milk Chocolate Segment Growth

Based on type, the market is classified into milk, dark, and white.

The milk segment is expected to dominate the global market. Milk chocolate is known to have a sweet and creamy texture, which is mostly preferred by people and kids who prefer comforting or conventional flavors. The mild taste makes it suitable for various applications such as bakery, confectionery, and ice cream.

The dark segment is expected to grow significantly over the forecast period, owing to its bold and intense flavor. Dark chocolate contains antioxidants and has zero or low sugar content, often preferred by health-conscious people. They are appealing to many consumers and are appreciated for their deep flavor and high-quality chocolate.

By Product Type

Coating Segment Dominates Market Owing to Ease of Use and Adaptability

Based on product type, the market is divided into chips, slabs, coatings, and others.

The coatings segment dominates the global market, owing to its ease of use and adaptability. Compound coatings do not require tempering, making them ideal for a wide temperature range. They also have the ability to incorporate diverse fats, allowing compound chocolate to achieve multiple textures, from creamy to crisp, and to be used in confectionery, bakery, and ice cream enrobing.

Chips will grow significantly in the coming years, as they have become a staple ingredient in various food products such as cookies, ice cream, muffins, pancakes, and others. These are mainly used as toppings and trail mixes, with the most popular chocolate chip varieties, including dark, white, and others. Players in the market are also coming up with innovative launches to meet the rising demand. For instance, in March 2023, Dr. Oetker, one of the U.K.’s leading food service baking brands, extended its baking collection with the launch of Dr. Oetker's Professional Chocolate Chips. The new product is specifically formulated for use in desserts and cakes.

By Application

Low Cost and Economic Stability to Boost Confectionery Segment Expansion

Based on application, the market is subdivided into confectionery, bakery, dairy and frozen desserts, beverages, and others.

The confectionery segment holds the largest market share. Compound chocolate is one of the most commonly used types of chocolate used in the manufacturing of confectionery. These chocolates are also stable in warmer conditions and are more resilient, having a melting point around 35°C to 37°C, further making them an ideal option for making confectionery. Moreover, chocolates are a low-cost substitute for couverture chocolates, which further fuels their demand.

The bakery segment will grow at a significant rate over the coming years. Compound chocolate is mainly used in cooking and baking owing to its lower cost and ease of use. Moreover, the ability of the product to melt and harden quickly makes it ideal for creating a smooth, glossy coating. The lack of tempering further makes it more convenient for large-scale production.

Compound Chocolate Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Compound Chocolate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe maintained a strong presence in the global market, reaching USD 1.48 billion in 2025, accounting for 32.18% share, and is expected to reach USD 1.53 billion in 2026. Europe is considered a hub for industrial chocolate production as a number of major global industrial chocolate producers are based in Belgium, the Netherlands, Germany, and Switzerland. The region is also known to be the largest importer of cocoa paste, cocoa beans, and cocoa powder in the world. According to the Centre for the Promotion of Imports from Developing Countries, in 2023, Europe imported 1.8 million tonnes of cocoa beans from producing countries. In recent years, there has been an increased emphasis on the regulation, such as the European Regulation on Deforestation-free Products (EUDR), of the cocoa supply in the European Union. Many EU countries, which are also some of the major cocoa importers in the world, are coming together in the fight for sustainable cocoa and protesting against deforestation caused by cocoa production. This step is anticipated to bring positive changes to the regional industry.The UK market is projected to reach USD 0.21 billion by 2026, while the Germany market is projected to reach USD 0.18 billion by 2026.

Download Free sample to learn more about this report.

North America

The North America region captured 12.67% of the global market in 2025, generating USD 0.58 billion in revenue, and is projected to reach USD 0.61 billion in 2026. The market in North America is expected to grow significantly, owing to the existence of major manufacturers and high consumption rates. Consumers in the region are increasingly seeking artisanal, high-quality, and ethically sourced chocolates, driven by trends in sustainability and health-conscious product categories.

The U.S. is known to hold a significant share in the North America market owing to the growing demand for high-end chocolate and confectionery. Compound chocolate is the ideal option for manufacturers to use in a variety of industries such as confectionery, bakery, ice cream, and desserts, further boosting market growth.The U.S. market is projected to reach USD 0.24 billion by 2026.

Asia Pacific

In 2025, Asia Pacific generated USD 1.21 billion, contributing 26.50% to global market revenue, and is projected to grow to USD 1.3 billion in 2026. Asia Pacific is known to be the second-largest market and is emerging as a global hotspot for the chocolate confectionery industry, owing to the rapid rates of urbanization and the consequent increase in discretionary spending from the middle-class population. China and India are the two major growth engines responsible for the promising growth of the regional chocolate confectionery industry, owing to rising per capita income and growing westernization trends. The demand for compound chocolates is higher in the Asia Pacific region, and several reasons are driving the growth of the market in the region. The low price of the product, its suitability for a wide range of applications, and the presence of a huge number of producers in the region are some of the major factors contributing to market expansion in Asia Pacific.The Japan market is projected to reach USD 0.25 billion by 2026, the China market is projected to reach USD 0.4 billion by 2026, and the India market is projected to reach USD 0.15 billion by 2026.

South America

In most South American countries, the presence of all income classes of consumers is prevalent, which is a growth-boosting factor for real and compound chocolate products. Brazil is known to be the largest market in South America and is projected to hold a major share throughout the forecast period. According to the National Association of Cocoa Processing Industries (AIPC), in 2022, Brazil exported 33,521 tons of chocolate and 54,756 tons of cocoa products, generating a revenue of USD 226 million. Furthermore, the bakery industry in South America is lucrative, given the consumers’ preferences for sweet indulgent offerings – cocoa liquor and cocoa powder are extensively utilized in the manufacturing of baked commodities such as chocolate biscuits, cakes, and pastries. The artisanal bakery trend in the region is also set to provide huge traction to cocoa-based ingredients.

Middle East & Africa

Middle East & Africa recorded a market size of USD 0.83 billion in 2025, capturing 18.05% of the global market share, and is projected to reach USD 0.88 billion in 2026. The Middle East & Africa market is projected to show moderate growth. Côte d’Ivoire and Ghana have emerged as two regional hotspots contributing to the accelerated production of cocoa beans and the biggest surplus in the last six years; however, the downside of this is a steep price erosion. Although grinding-at-origin has gradually gained traction, the African marketplace is seeking robust manufacturing infrastructure for end products such as chocolate processing. This is expected to necessitate greater utilization of cocoa ingredients within the regional market, the economies of scale for which are rapidly attainable. Manufacturers and retailers are earning profits in the regional market, as in most of the developing economies of the region, the demand for low-priced cocoa and chocolate products is high and is only expanding. Increasing investment by key international chocolate processors and manufacturers in the Middle East & African market is further expected to boost the regional compound chocolate market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Players Emphasize Innovation and Sustainability Strategies to Increase Sales

The industry is moderately consolidated, with companies such as Barry Callebaut, Cargill, Inc., Fuji Oil Group, Puratos Group, and Cemoi Group accounting for a significant global compound chocolate market share. The prominent players in the market are extensively focusing on two strategies – new product development and concentrating their focus on sustainability, so as to procure organic, traceable, and Fairtrade cocoa. The global industry is concentrated with a few players and has witnessed robust growth in the past decade. The Barry Callebaut company emerged as a market leader in the global cocoa processing industry, followed by Cargill and Fuji Oil Group.

LIST OF KEY COMPOUND CHOCOLATE COMPANIES PROFILED

- Barry Callebaut (Switzerland)

- Cargill, Inc. (U.S.)

- Fuji Oil Group (Japan)

- Puratos Group (Belgium)

- Cemoi Group (France)

- Clasen Quality Chocolate (U.S.)

- Schokinag (Germany)

- IRCA Group Italia (Italy)

- Kerry Group (Ireland)

- Guittard Chocolate Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2024: Cargill, Incorporated, an American multinational food corporation, launched a range of block chocolates, cocoa powder, and chocolate chips products under its NatureFresh Professional brand at the 38th edition of AAHAR, India’s largest fair for international food and hospitality.

- April 2023: Barry Callebaut, one of the world’s leading manufacturers of high-quality chocolate and cocoa products, launched a new compound chocolate, Ruby Chocolate Chip. The new product has applications in bakery and snacks and falls under Barry Callebaut’s comprehensive Intense Indulgence solutions portfolio.

- November 2022: Barry Callebaut opened its third chocolate and compound manufacturing facility in India.

- October 2022: Puratos Group launched colored and flavored compound and compound filling in two variants, including fat-based filling Carat Supercrem and Hard Compound Chocolate - Carat Cover Classic.

- June 2021: Barry signed an agreement for the acquisition of a leading Belgian privately-owned B2B chocolate specialties and decorations producer - Europe Chocolate Company (ECC). The step was taken by the company to strengthen its manufacturing capabilities in the rapidly proliferating market of customized industrial chocolate.

REPORT COVERAGE

The global market report provides market size and forecast for all the segments. It includes details on the market dynamics and trends expected to drive the global market over the forecast period. It offers information about the key regions/countries, key industry developments, new product launches, and details on key countries' partnerships, mergers, and acquisitions. The global market analysis also covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.42% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Product Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

The global compound chocolate market size was valued at USD 4.58 billion in 2025. The market is projected to grow from USD 4.83 billion in 2026 to USD 8.57 billion by 2034, exhibiting a CAGR of 7.42% during the forecast period.

The market is expected to exhibit a CAGR of 7.42% during the forecast period of 2026-2034.

By type, the milk segment is anticipated to dominate the global market.

The increasing demand for chocolate confectionery is a key factor driving market growth.

Barry Callebaut, Cargill, Inc., Fuji Oil Group, Puratos Group, and Cemoi Group are the top players in the market.

Europe dominated the market in 2025.

The rising trend of plant-based and vegan foods revolt trend to fuel market Expansion

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us