Computational Biology Market Size, Share & Industry Analysis, By Component (Software/Platforms and Services), By Technology (Bioinformatics & Sequence Analytics, Molecular Modelling & Simulation, Machine Learning/AI in Biology, Network Modelling, and Others) By Application (Omics Data Analysis, Structural Biology & Molecular Modelling, Drug Discovery, Biomarker & Patient Stratification, Clinical & Translational Informatics, Disease Modelling, and Others), By End User (Pharma Companies, Institutes, CROs & CDMOs, Hospitals & Diagnostic Laboratories, and Others), & Regional Forecast, 2026-2034

Computational Biology Market Size and Future Outlook

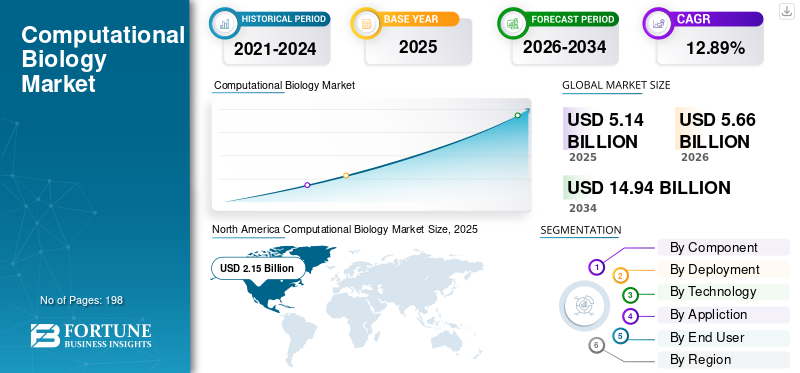

The global computational biology market size was valued at USD 5.14 billion in 2025. The market is projected to grow from USD 5.66 billion in 2026 to USD 14.94 billion by 2034, exhibiting a CAGR of 12.89% during the forecast period. North America dominated the computational biology market with a market share of 41.83% in 2025.

Computational biology methods are applied to examine biological information, simulate molecular and cellular systems, and aid in decision-making in genomics, proteomics, drug development, biomarker discovery, and translational research. The market is growing due to the increasing production of multi-omics and genomic data, greater adoption of cloud-based and AI-driven research platforms, and heightened demand for computational tools that can expedite target discovery, molecular modeling, and precision medicine processes. Market demand is rising as research institutions, biopharmaceutical firms, and healthcare entities enhance data driven R&D abilities through extensive genomic datasets, scalable analytical frameworks, and unified bioinformatics systems to boost discovery productivity, generate clinical insights, and improve development effectiveness.

Key players operating in the global market include Schrödinger, Inc., Illumina Inc., Danaher Corporation (Genedata AG), Thermo Fisher Scientific Inc., and DNAnexus, Inc. These firms are focusing on bioinformatics and sequence analytics, cloud-native scientific data platforms, molecular modelling and simulation, AI in biology, and translational data applications that support drug discovery and precision medicine.

Download Free sample to learn more about this report.

Computational Biology Market Key Takeaways

- 2025 Market Size: USD 5.14 billion

- 2026 Market Size: USD 5.66 billion

- 2034 Forecast Market Size: USD 14.94 billion

- CAGR: 12.89% from 2026–2034

- North America dominated the computational biology market with a 41.83% share in 2025.

- The Cloud-Based segment is projected to hold a 56.5% share in 2026.

- The Bioinformatics & Sequence Analytics segment is projected to account for 38.2% share in 2026.

North America

North America held 41.83% share in 2025, valued at USD 2.15 billion.

Asia Pacific

Asia Pacific market is projected to reach USD 1.29 billion by 2026.

Europe

Europe market is projected to grow at a CAGR of 11.49% during the forecast period.

U.S.

Market is projected to reach USD 2.04 billion by 2026.

Japan

Market is projected to reach USD 0.35 billion by 2026.

Read More

COMPUTATIONAL BIOLOGY MARKET TRENDS

Growing Role of AI and Machine Learning In Biological Data Analysis is a Significant Trend Observed in Market

The increasing importance of AI and machine learning in biological data analysis is emerging as a significant market trend since life science entities are managing extensive and intricate genomic, proteomic, and multimodal datasets that traditional tools alone struggle to analyze. AI and ML assist researchers in swiftly identifying patterns, enhancing data interpretation, prioritizing targets, and automating segments of discovery and translational processes. This enhances the pace of research, minimizes manual work, and facilitates improved decision-making in biomarker identification, drug development, and precision medicine initiatives. The trend is also gaining momentum as companies increasingly seek to integrate AI features directly into their scientific software platforms rather than relying on separate, unrelated tools. With a growing number of laboratories adopting cloud-based and data-centric research and development, the integration of AI into daily scientific processes is anticipated to rise even more. These factors are supporting the overall global computational biology market growth.

- For instance, in October 2025, Benchling launched Benchling AI, a scientific AI command center designed to bring agents and predictive models directly into the platform used by scientists.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Use in Genomics and Precision Medicine is Driving Market Growth

Rising adoption in genomics and precision medicine is a key market driver as computational biology tools are essential for analyzing vast genomic, transcriptomic, and multimodal datasets and transforming them into valuable clinical insights. With the increasing adoption of precision medicine by healthcare systems and life science firms, there is growing demand for software and platforms that assist in variant interpretation, biomarker discovery, patient stratification, and therapy selection. This is also leading to increased utilization of cloud-based bioinformatics, AI-driven analytics, and unified genomic data systems. The trend is solidifying as genomic profiling advances from research environments into wider clinical and translational processes. Consequently, organizations are allocating increased resources to computational solutions that enhance speed, scalability, and precision in data analysis. All these factors cumulatively drive the overall market growth.

- For instance, in April 2025, Illumina Inc. announced collaboration with Tempus aimed at accelerating the clinical adoption of next-generation sequencing tests through genomic AI innovation.

MARKET RESTRAINTS

Data Fragmentation and Poor Interoperability to Limit Market Growth

Data fragmentation and inadequate interoperability serve as significant market constraints since computational biology relies on integrating genomic, clinical, proteomic, and other omics datasets from various systems into a single functional workflow. In numerous organizations, these datasets remain on distinct platforms, utilize various formats, and adhere to inconsistent metadata standards, resulting in integration that is slow, costly, and technically challenging. This slows down analysis, constrains scalability, and postpones the creation of clinically or commercially valuable insights. It additionally introduces extra complexity for discovering biomarkers, interpreting variants, conducting translational research, and collaborating across institutions. Consequently, numerous end users require additional time, resources, and services merely to synchronize data prior to commencing actual analysis, which may hinder market adoption.

MARKET OPPORTUNITIES

Rising Adoption in Clinical Trials and Disease Modeling to Offer Market Growth Opportunities

Increasing use in clinical trials and disease modeling is generating a significant market opportunity, as sponsors and research teams increasingly require computational tools to enhance trial design, expedite patient eligibility identification, and accurately model disease behavior. These platforms assist in minimizing recruitment delays, facilitate biomarker-driven stratification, and enhance decision-making in intricate studies. They are also gaining more significance as trials advance toward precision medicine, which requires more data for patient selection and disease progression analysis. Simultaneously, disease modeling tools assist researchers in simulating biological pathways and patient reactions earlier in development, enhancing target prioritization and lowering trial risk. This generates fresh business prospects for suppliers providing bioinformatics, AI, translational informatics, and modeling platforms. All these factors would drive the market growth in the coming years.

- For instance, in March 2025, Tempus AI acquired Deep 6 AI to strengthen its clinical trial matching capabilities. The company said Deep 6 AI’s platform had access to more than 750 provider sites and over 30 million patients.

MARKET CHALLENGES

Shortage of Skilled Bioinformatics and Computational Talent Pose a Prominent Challenge to Market Growth

Shortage of skilled bioinformatics and computational talent is a major market challenge as computational biology solutions require professionals who can work across biology, statistics, software engineering, AI, and data interpretation. Many end users can invest in platforms, but still struggle to scale adoption as they lack teams that can build pipelines, validate outputs, integrate datasets, and convert results into research or clinical decisions. This slows implementation, increases dependence on external services, and raises the overall cost of deployment. The challenge is becoming more visible as AI, automation, and multi-omics workflows make technical requirements even more specialized. All the factors cumulatively affect the market growth.

- For instance, the 2025 National Life Sciences Workforce Trends Report was released by the Life Sciences Workforce Collaborative in July 2025. It found that the industry is dealing with rapid technological change, broader AI integration, and increasing investment in upskilling workers to address workforce gaps.

Segmentation Analysis

By Component

Software/Platforms Widely Adopted Due to Central Role in Data Analysis, Modeling, and Recurring Platform-Based Scientific Workflows

In terms of component, the market is divided into software/platforms and services.

The software/platforms segment led the global computational biology market share in 2025. This results from the key function of bioinformatics platforms, molecular modeling tools, omics analysis software, and translational data systems in standard computational biological processes. These platforms maintain the largest market share as most end users depend on licensed or subscription software to handle biological data, conduct analyses, model molecular interactions, and aid discovery and precision medicine initiatives. The extensive application in pharmaceutical and biotechnology firms, academic institutions, CROs/CDMOs, and hospitals and diagnostic labs bolsters segment leadership. The segment is further reinforced by their scalable characteristics and recurring revenue model, as customers frequently enhance their utilization via cloud deployment, hosted environments, and added analytics modules over time.

- For instance, in February 2026, Schrödinger reported that its 2025 software revenue reached USD 200 million and highlighted continued growth in hosted and ratable software revenue. This indicates the strong commercial importance of software-led computational-biology solutions.

The services segment is anticipated to rise with a CAGR of 14.05% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Strong Acceptance and Broad Installed Base Supported the Dominance of Cloud-Based Segment

Based on deployment, the market is classified into on-premise, cloud-based, and hybrid.

The cloud-based segment captured the leading position in the global market in 2025. This is due to the fact that computational biology tasks frequently require extensive genomic, proteomic, and multi-omics datasets that demand significant computing power, adaptable storage, and rapid data sharing among teams. Cloud-based platforms remain the predominant choice as they assist users in executing analysis workflows more efficiently, eliminate substantial initial infrastructure expenses, and adjust usage according to project requirements. The increase in their adoption is due to the growing preference of pharmaceutical companies, research institutes, CROs, and diagnostic labs for connected platforms that enable collaboration, remote access, and quicker updates. Additionally, cloud deployment is particularly beneficial for AI-driven analytics and extensive bioinformatics workflows, as it provides users with speed, adaptability, and simpler system scalability. Furthermore, the segment is set to hold 56.5% share in 2026.

- For instance, in January 2025, Inotiv announced a partnership with VUGENE to integrate VUGENE’s cloud-based bioinformatics and computational platform into its Discovery & Translational Sciences Division.

The hybrid segment is anticipated to rise with a CAGR of 13.22% over the forecast period.

By Technology

Bioinformatics & Sequence Analytics Widely Preferred due to its Core Role in Various Workflows

Based on technology, the market is classified into bioinformatics & sequence analytics, molecular modelling & simulation, machine learning/AI in biology, systems biology & network modelling, and others.

The bioinformatics & sequence analytics segment dominated the market share in 2025. This is as most computational biology workflows begin with sequencing data generation, followed by read processing, alignment, variant interpretation, expression analysis, and multi-omics data handling. These tools continue to hold the largest share as they are widely used across pharmaceutical & biotechnology companies, academic institutes, CROs/CDMOs, and hospitals & diagnostic laboratories. Their dominance is also supported by the steady rise in whole-genome, transcriptome, and other omics datasets that require scalable and routine analysis pipelines. Furthermore, the segment is set to hold 38.2% share in 2026.

- For instance, in January 2025, Illumina announced a collaboration with NVIDIA to advance platforms for the analysis and interpretation of multiomic data in clinical research, genomics AI development, and drug discovery.

The machine learning/AI in biology segment is anticipated to rise with a CAGR of 16.27% over the forecast period.

By Application

High Usage in Various Data Analysis Led to Dominance of Omics Data Analysis Segment

On the basis of application, the market is divided into omics data analysis, structural biology & molecular modelling, drug discovery & preclinical optimization, biomarker & patient stratification, clinical & translational informatics, systems biology/pathway & disease modelling, and others.

In 2025, the market share was primarily led by the omics data analysis segment. This is owing to the fact that the majority of computational biology projects start with the examination of sequencing and various omics data prior to progressing into downstream applications such as biomarker identification, disease modeling, and clinical interpretation. These tools maintain the largest share as they are extensively utilized for managing large genomic, transcriptomic, epigenomic, and proteomic datasets in pharmaceutical companies, research institutions, CROs, and diagnostic labs. Their supremacy is further reinforced by the ongoing increase in multi-omics research, where users require scalable systems for data processing, integration, and visualization. Furthermore, the segment is set to hold 28.8% share in 2026.

- For instance, in February 2025, Illumina announced new technologies to expand its multiomics portfolio, including a new multimodal data analysis platform spanning genomics, spatial, single-cell, CRISPR, and methylation workflows.

The biomarker & patient stratification segment is anticipated to rise with a CAGR of 16.55% over the forecast period.

By End User

Pharmaceutical & Biotechnology Companies Led Demand due to High Spending on Data Analysis Tools

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, CROs & CDMOs, hospitals & diagnostic laboratories, and others.

The pharmaceutical & biotechnology Companies segment dominated the market share in 2025. This dominance is driven by regular investments by pharmaceutical & biotechnology companies in software platforms and related services to improve R&D productivity, shorten timelines, and support data-driven decision-making. Their leadership is also supported by the growing use of AI, cloud-based research platforms, and multi-omics workflows in drug development programs. Furthermore, the segment is set to hold 35.8% share in 2026.

- For instance, in May 2025, Benchling announced an expanded collaboration with Moderna to broaden the rollout of its R&D platform across Moderna’s research organization.

In addition, CROs/CDMOs are projected to witness 13.79% growth rate during the forecast period.

Computational Biology Market Regional Outlook

By region, the market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Computational Biology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest share of the global market and attained USD 1.96 billion in 2024 and maintained its dominance in 2025 with USD 2.15 billion. North America is expanding due to its robust foundation in biopharma research and development, high levels of cloud/software utilization, and extensive precision-medicine data collections. Moreover, the ongoing growth of real-world genomics and clinical research frameworks also support the market growth.

U.S. Computational Biology Market

The U.S. market led the North American region and is projected to be approximately USD 2.04 billion in 2026, representing about 36.0% of the worldwide market.

Europe

The Europe market is growing at a CAGR of 11.49% during the forecast period. Europe's expansion is fueled by cross-border genomic infrastructure, collaboration in public health data, and the progressive implementation of precision medicine. Another aspect is the region's effort to create federated access to genomic data among countries that supports market growth.

U.K. Computational Biology Market

The U.K. market in 2026 is estimated at around USD 0.20 billion, representing roughly 3.5% of global revenues.

Germany Computational Biology Market

Germany market size is projected to reach approximately USD 0.26 billion in 2026, equivalent to around 4.6% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach a valuation of USD 1.29 billion by 2026. Asia Pacific is expected to grow the fastest due to large scale genomics expansion, growing biotech investment, and rising adoption of AI and precision medicine.

Japan Computational Biology Market

The Japan market in 2026 is estimated at around USD 0.35 billion, accounting for roughly 6.2% of global revenues.

China Computational Biology Market

China’s market is projected to reach revenues of around USD 0.39 billion in 2026, representing roughly 6.8% of global sales.

India Computational Biology Market

The India market in 2026 is estimated at around USD 0.14 billion, accounting for roughly 2.5% of global revenues.

Latin America and Middle East & Africa

The growth in Latin America and the Middle East & Africa regions is anticipated to be slower over the forecast period. The growth of the market is driven by rising interest in precision health, expansion of genomics programs, and improving public-sector support for genomic medicine. The Latin America market in 2026 is estimated at around USD 0.28 billion.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.09 billion by 2026, representing about 1.6% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and Strategic Initiatives Strengthen Market Position of Key Players

The global market shows a moderate level of consolidation, with leading organizations such as Schrödinger, Inc., Illumina Inc., Danaher Corporation (Genedata AG), and Thermo Fisher Scientific Inc., accounting for a considerable share of total revenue. These players are working to enhance their market position through cloud-based scientific platforms, bioinformatics and sequence analytics, molecular modelling, AI based biology workflows, and translational data applications.

- In January 2026, Schrödinger announced a partnership with Lilly to make the TuneLab platform available within LiveDesign, expanding support for antibody discovery workflows.

Additional notable participants include Seven Bridges Genomics, SOPHiA GENETICS, TEMPUS, and Recursion, among others. These firms are anticipated to focus on product improvement, automation of workflows, and expanded support for genomics, biomarker identification, and computational drug research to elevate their market position over the study period.

LIST OF KEY COMPUTATIONAL BIOLOGY COMPANIES PROFILED

- Schrödinger, Inc. (U.S.)

- Illumina Inc. (U.S.)

- Danaher Corporation (Genedata AG) (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- DNAnexus, Inc. (U.S.)

- QIAGEN (Germany)

- Seven Bridges Genomics (U.S.)

- SOPHiA GENETICS (Switzerland)

- TEMPUS (U.S.)

- Recursion (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Benchling launched AI Connectors, built on MCP, to connect scientific data with AI tools used in R&D. The company said the new capability links scientific and enterprise systems such as SharePoint, Snowflake, and Notion so AI workflows can access full experimental and organizational context.

- April 2026: Illumina launched DRAGEN v4.5, a major software expansion aimed at improving insights across germline, oncology, and multiomic workflows.

- January 2026: Illumina introduced the Billion Cell Atlas, described as the world’s largest genome-wide genetic perturbation dataset, to accelerate AI and drug discovery.

- January 2026: Tempus launched Paige Predict, a new AI-powered biomarker prediction suite for digital pathology following its 2025 Paige acquisition.

- August 2025: SOPHiA GENETICS expanded its collaboration with AstraZeneca to use its multimodal AI Factories in breast cancer.

REPORT COVERAGE

The global computational biology market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.89% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 5.14 billion in 2025 and is projected to reach USD 14.94 billion by 2034.

In 2025, the market value stood at USD 2.15 billion.

The market is expected to exhibit a CAGR of 12.89% during the forecast period.

By component, the software/platforms segment is expected to lead the market.

Increasing use in genomics and precision medicine coupled with growing demand in drug discovery & development are primarily driving market expansion.

Schrödinger, Inc., Illumina Inc., Danaher Corporation (Genedata AG), and Thermo Fisher Scientific Inc. are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us