Confidential Computing Market Size, Share & Industry Analysis, By Component (Hardware, Software (Confidential Computing Software Developers and Security & AI/ML Software Vendors), and Services (Cloud Service Providers (CSPs) and System Integrators & Managed Service Providers (MSPs))), By Deployment (On-premise and Cloud), By Enterprise Type (Large Enterprises and Small and Mid-sized Enterprises (SMEs)), By Application (Privacy & Security, Blockchain, Multi-party Computing, and Others), By Industry (BFSI, Manufacturing, Retail & Consumer Goods, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

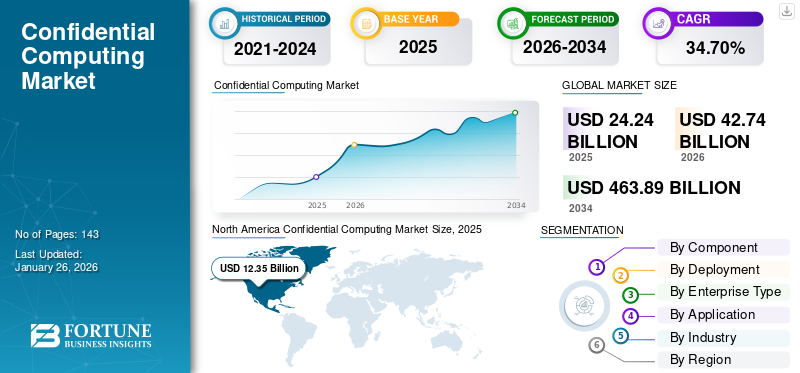

The global confidential computing market size was valued at USD 24.24 billion in 2025 and is projected to grow from USD 42.74 billion in 2026 to USD 463.89 billion by 2034, exhibiting a CAGR of 34.70% during the forecast period. North America dominated the global market, accounting for a 51.00% share in 2025.

The process of confidential computing entails the segregation of data within a secure Central Processing Unit (CPU) while it is being processed, in order to protect it against internal threats, network vulnerabilities, and other technological risks. It includes both software and hardware-based security measures for businesses that utilize cloud-based computing infrastructure.

The use of computing technology involves a new security approach that involves encrypting workloads while processing files, restricting access, and ensuring comprehensive data protection. The importance of this technology is growing with the emergence of cloud computing. Major players in the industry are introducing new offerings in their product portfolios.

- In April 2024, at Google Cloud Next, the company reported enhancements to its confidential computing solutions. These include expanded hardware instances, adding support for data migrations, and further extension of partnerships that have helped establish Confidential Computing as a vital solution for data confidentiality and security.

The market is dominated by established key players, such as Intel Corporation, IBM Corporation, Alphabet Inc., Alibaba Group, and NVIDIA Corporation. These players focus on entering into partnerships and collaborations with small and regional players to enhance their offerings and expand their geographic presence. For instance,

- In October 2024, Intel Corporation and Cohesity entered into collaboration to enhance hardware security in cloud environment.

Security and privacy were a top priority during the COVID-19 pandemic as many businesses implemented remote work policies and transitioned rapidly to cloud services. The rising usage of cloud services sparked worries about data security during processing. However, cloud providers embraced this technology to adhere to regulatory standards.

Download Free sample to learn more about this report.

Impact of Generative AI

Usage of Confidential Computing Capabilities Across Generative AI to Upsurge its Adoption

Generative AI enterprises are significantly accelerating the adoption of the product, as enterprises increasingly require secure environments to process and train on sensitive datasets, including proprietary documents, personal data, financial records, and healthcare information.

Generative AI models such as large language models (LLMs), image generators, and multimodal systems often involve high-value intellectual property and are trained using massive volumes of regulated or private data, increasing concerns around data leakage, model theft, and unauthorized access. Confidential computing addresses these concerns by enabling the training and inference of AI models in isolated, hardware-based environments, such as Intel SGX, AMD SEV, or ARM CCA, where data and algorithms remain protected even during runtime.

- According to industry estimates, over 70% of enterprise AI workloads will involve sensitive data by 2026, driving demand for secure AI infrastructure. As per Fortanix, product adoption in AI/ML operations has grown by over 45% year-over-year since 2022, especially in sectors such as banking, healthcare, and government.

It plays a critical role in creating a secure foundation that enables companies to scale their AI initiatives confidentially.

Impact of Reciprocal Tariffs

Implementation of Reciprocal Tariffs can Affect Market Progress Negatively

Higher tariffs on the global semiconductor industry by the U.S. will influence costs, supply chains, innovation, and geopolitical dynamics, adversely affecting the semiconductor industry.

The cost of U.S. semiconductor imports, particularly from China, Taiwan, and South Korea, is set to rise considerably. Businesses dependent on these imports will suffer increased production costs, which may result in decreased profit margins or higher consumer prices.

The technology relies on particular hardware such as memory encryption modules, secure processors, and trusted chipsets. However, reciprocal tariffs on electronics and semiconductors, particularly among regions such as the U.S. and China or the EU and the U.S., can surge import/export costs by 5% to 15%.

This directly raises the Bill of Materials (BOM) for devices and servers that provision trusted execution environments (TEEs), thereby increasing the Total Cost of Ownership (TCO) for both cloud providers and on-premise users. The impact is specifically noticeable for SMEs and cost-effective markets, where higher infrastructure costs can delay adoption of secure computing technologies.

CONFIDENTIAL COMPUTING MARKET TRENDS

Expansion of Multi-Cloud and Hybrid Environments to Propel Product Demand

The shift toward multi-cloud and hybrid architectures has led organizations to prioritize secure computing environments across different cloud providers. Confidential computing solutions are essential for businesses that must maintain control over sensitive information while leveraging the benefits of cloud infrastructure.

- As per Flexera and Spacelift Insights, 92–93% of enterprises adopted a multi-cloud approach, using an average of 4.8 various clouds.

- As per Industry Experts, hybrid cloud implementation is anticipated to reach 90% by 2027, as enterprises seek redundancy and flexibility.

Multi-cloud and hybrid cloud environments increase the requirement for secure, isolated execution environments (AMD SEV-SNP, Intel SGX, and NVIDIA's confidential computing solutions to safeguard data from revelation to cloud providers.

This rising inclination of end-users toward adopting multi-cloud and hybrid-cloud strategies is driving the need for consistent and secure data processing across several environments. These solutions provide secure data processing regardless of the environment.

Thus, the increasing inclination of end users to adopt hybrid and multi-cloud strategies is driving the demand for these computing solutions.

MARKET DYNAMICS

Market Drivers

Advancements in Secure Hardware Enclaves and Software Propel Market Growth

Several advancements in secure hardware enclaves by Intel, Arm, Microsoft, and AMD have made it easier for businesses to implement confidential computing.

- In November 2023, Microsoft announced the general accessibility of the new DC-series databases capable of 40 vCores, which support Always Encrypted with secure enclaves. These use initial Intel SGX (Intel Software Guard Extensions) hardware-based technology that allows computations on delicate encrypted data within server-side secure enclaves that safeguard data confidentiality from malware.

- Description: Intel's Software Guard Extensions help end users secure data in use through unique application isolation technology.

In addition, many confidential computing services are at their early proof-of-concept stage; however, their adoption is expected to rise in the coming years, thereby significantly impacting the market. This software segmental demand is accelerated due to factors such as an appetite for new revenue generators, expanding regulations, and demand for comprehensive security postures.

- As per insights from the Confidential Computing Summit 2024, three reasons that could amplify the technology awareness are enhancing the user experience of existing solutions, accentuating the business value of the market, and enabling developers to develop applications that leverage such solutions.

Thus, growing enterprise awareness, increased data security concerns, expanding partner ecosystems, and advancements in secure hardware enclaves are driving the market expansion in recent years.

Market Restraints

High Implementation Costs Associated with the Product to Hinder Market Growth

A key restraining factor in the market is the high implementation costs associated with deploying confidential computing solutions.

One of the primary barriers to the widespread adoption of such a solution is the high cost associated with the technology implementation. Setting up secure hardware enclaves and maintaining a secure processing environment requires a significant investment in dedicated hardware, specialized software, and related services.

Such investments can be particularly challenging for small and medium-sized enterprises that may lack the resources to invest in such advanced security measures. Moreover, as the market is still evolving, there is a lack of standardized frameworks and protocols. Several vendors provide their own versions of secure enclave technologies, further leading to potential compatibility concerns. This approach also raises a lack of interoperability between solutions.

Market Opportunities

Rising Adoption of Computing Solutions across Emerging Markets Creates Lucrative Opportunities for Market Players

As digitalization is spreading across several emerging markets, the need for secure computing solutions is becoming more prevalent. In particular, for markets and industries such as manufacturing, government, and public sector, it is expected that the adoption of the product will grow significantly.

- In the manufacturing industry, the technology can be used for securing trade secrets in collaborative projects. Manufacturers often collaborate with partners, suppliers, and even competitors on R&D projects. These collaborations involve sharing sensitive data, which requires a high level of trust. Any data leakage can result in significant financial loss, making secure processing a strategic imperative.

- In the government and public sector, there is a constant demand for the sharing of sensitive and mission-critical data, which needs to be secured at all costs. To gain secure data processing between the government and other agencies, government firms are expected to adopt these solutions on a larger scale.

- For instance, in March 2025, Acompany established the Confidential Computing Lab (CC Lab), a research institute committed to research and development in hardware-driven confidential computing in Japan. With CC Lab, Acompany aims to lead product development by progressing research in confidential computing and reinforcing collaboration with academic institutions.

Thus, it is expected that market players can leverage these requirements from these sectors and develop tailored solutions to enhance customer experience.

SEGMENTATION ANALYSIS

By Component

Services Segment Led due to Rising Demand for Confidential Computing Services

By component, the market is divided into hardware, software (Confidential Computing Software Developers and Security & AI/ML Software Vendors), and services (Cloud Service Providers (CSPs) and System Integrators & Managed Service Providers (MSPs)).

The services segment held the highest market share in 2024. The requirement for confidential computing services is growing worldwide owing to the increasing need for protected data processing in insecure environments. The demand is more pronounced as enterprises fast-track digital transformation and cloud implementation. Cloud service vendors such as AWS, Google Cloud, and Azure are growing these offerings to comprise turnkey services, empowering businesses to deploy protected environments without requiring in-house cryptographic expertise.

The software segment, comprising solutions from confidential computing software developers and security & AI/ML software vendors, is projected to lead the market with the highest CAGR during the forecast period with a share of 38.35% in 2026. Such software acts as a bridge between secure hardware (such as AMD SEV, ARM CCA, and Intel SGX) and enterprise implementations, empowering developers to process and manage secure work operations without deeply altering their codebases.

By Deployment

Rise in Usage of Multi-Cloud Solutions to Aid the Cloud Segment Growth

By deployment, the market is divided into on-premise and cloud.

The cloud segment is anticipated to demonstrate the highest CAGR in the forecast period, as organizations are transitioning their data workloads to the cloud with a share of 20.46% in 2026. As a result of the pandemic, organizations implemented work-from-home policies, prompting them to move their data to the cloud. The increasing demand for multi-cloud solutions is also fueling segment growth. For instance,

- As per Industry Experts, over 90% of newly developed applications will be multicloud-empowered, designed to use platform-delivered competencies and offer more inventive solutions.

Enterprises continue to depend on on-premises deployment due to concerns about data sensitivity and security risks. Enterprises choose to maintain control of key management systems (KMS) within their on-premise data centers.

By Enterprise Type

Large Enterprises Segment Led Owing to the Increasing Adoption of Computing Solutions

By enterprise type, the market is segmented into large enterprises and Small and Mid-sized Enterprises (SMEs).

Large enterprises held the highest confidential computing market share 70.29% in 2026 and are estimated to grow with the highest CAGR over the forecast period. Large corporations depend on computing solutions as they offer enhanced assurance that their data remains secure and private when stored on the cloud. This also safeguards data, extends the advantages of the cloud to sensitive workloads, secures intellectual property, and facilitates secure collaboration with partners on innovative cloud solutions. Additionally, it alleviates worries about selecting a cloud provider and safeguards data processes at the edge.

The adoption of this technology poses a challenge for SMEs due to the substantial investment required. The specialized hardware needed includes dedicated processors and secure enclaves to ensure the security and privacy of data and computations.

By Application

Multi-party Computing Segment to Lead, Driven by their Benefits of Online Accessibility of Assets

On the basis of application, the market is segmented into privacy & security, blockchain, multi-party computing, IoT & edge, and personal computing devices.

The multi-party computing segment is expected to witness the highest growth in the next few years, due to its ability to assist businesses in minimizing the risk of single points of compromise and facilitate compliant, instant digital asset transactions. Multi-party computing offers the benefit of keeping assets accessible online for real-time transactions, enabling multiple parties to engage in transactions while fulfilling privacy and policy mandates.

The privacy & security segment held the largest market share in 2024. The increasing awareness about data privacy is expected to have a significant impact on the formulation of new government regulations, thereby driving the uptake of confidential computing solutions. Stringent measures on data privacy initiated by several governments worldwide boost the segment’s growth.

By Industry

To know how our report can help streamline your business, Speak to Analyst

Manufacturing Segment to Display Highest CAGR due to Growing Focus on Enhancing Supply Chain

By industry, the market is classified into BFSI, manufacturing, retail & consumer goods, healthcare & life science, IT & telecom, government & public sector, and others.

The manufacturing segment is projected to witness the highest CAGR during the forecast period. Confidential computing in manufacturing is expected to enhance the supply chain visibility and improve collaboration among stakeholders across the value chain. Manufacturing enterprises are expected to adopt this type of computing to supplement collaborative use cases such as Multi-Party Computing (MPC) and real-time supply chain tracking/provenance.

The BFSI segment accounted for the largest market share in 2024. By using the technology, financial institutions gain the ability to work together and share their insights on money laundering and digital fraud patterns, leading to the creation of advanced algorithms for fraud detection. Banks and other financial institutions rely on the trust of their clients, which is crucial for attracting and retaining business.

- In September 2024, NTT DATA and IBM announced an enhancement of their collaboration with the introduction of SimpliZCloud, a novel hybrid cloud service designed to cater to the computational requirements of financial services firms in India. The service incorporates confidential computing capabilities to safeguard data during its usage, and encryption features to ensure the security of data both at rest and in transit.

CONFIDENTIAL COMPUTING MARKET REGIONAL OUTLOOK

The market is geographically studied across North America, South America, Europe, the Middle East & Africa, and Asia Pacific, and each region is further studied across various countries.

North America

North America Confidential Computing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 12.35 billion in 2025, representing 51.00% of the global market share, and is projected to reach USD 21.98 billion in 2026. According to our analysis, North America generates a maximum revenue share and is estimated to showcase strong growth during the forecast period. This growth is due to the significant presence of local cloud hyperscale providers in the U.S. One of the key drivers for confidential computing market growth in the region is the increasing demand for security and efforts to address cyber threats among the countries in North America. Governments in the region are prioritizing the development and adoption of innovative cybersecurity approaches, leading to a surge in the demand for security solutions.

- According to Palo Alto Networks (2024), over 60% of North American firms stated cloud misconfigurations and insider dangers as leading causes of data breaches. Common threats comprise insider breaches, ransomware, supply chain attacks, and advanced persistent threats (APTs), which often exploit hybrid and cloud environments where data is most susceptible during processing.

Download Free sample to learn more about this report.

The market in the U.S. is experiencing a strong upward trajectory due to increased awareness of data privacy threats and the enforcement of strict regulatory standards. Businesses are progressively integrating these technologies to protect sensitive data at every stage, from processing to storage. This movement is stimulating the development of secure computing solutions and encouraging partnerships between major tech companies and cybersecurity firms to address the rising need for strong data protection measures.The U.S. market is projected to reach USD 15.7 billion by 2026.

- In 2024, the U.S. Department of Defense (DoD) sanctioned the deployment of confidential computing-powered cloud infrastructure for protected mission-critical operations across several federal departments.

South America

South America’s market is estimated to witness progressive growth from 2025 to 2032. Countries in South America have recorded some achievements over the past few years. There is also growing acceptance of digital technologies in both government and corporate sectors, such as healthcare, retail, and automotive. Government organizations and agencies have been at the forefront in adopting these solutions. One of the most serious threats government agencies are facing today is state-sponsored cyber warfare, which is occurring against the backdrop of rising geopolitical and geo-economic tensions.

- The Brazilian Association of Software Companies (ABES) reported that in 2023, Brazil’s expenditure on security solutions amounted to approximately USD 1.3 billion, marking a 13% increase from 2022. IT and data security are expected to remain key focal points in Brazil.

Europe

The Europe market was valued at USD 8.22 billion in 2025, capturing 33.90% of global revenue, and is estimated to reach USD 14.94 billion in 2026. The adoption of product in the region is expected to be driven by European markets such as Germany, the U.K., France, Spain, and Benelux. Growth in the region will be driven by factors such as the push for regulatory compliance, including GDPR, increasing privacy concerns, and the use cases for AI/ML adoption. For instance,The UK market is projected to reach USD 2.59 billion by 2026, while the Germany market is projected to reach USD 2.8 billion by 2026.

- Europe is at the forefront of federated data-sharing and AI collaboration initiatives, such as the European Health Data Space and GAIA-X, and Horizon Europe. These initiatives depend heavily on the ability to share and analyze data without compromising privacy or regulatory compliance.

Middle East & Africa

Middle East & Africa contributed approximately USD 0.4 billion to the global market in 2025, accounting for 1.60% share, and is expected to reach USD 0.64 billion in 2026. Digital adoption is gaining momentum as the Middle East countries' governments are executing multiple national initiatives. The governments are conducting digital technology adoption programs supported by technologies such as the Internet of Things, cloud computing, artificial intelligence, and machine learning. The UAE is focused on long-term investment in the digital economy by developing in the areas of advanced technologies such as artificial intelligence and cloud computing post-pandemic.

Asia Pacific

In 2025, Asia Pacific held 11.20% of the global market, reaching a valuation of USD 2.73 billion, and is projected to grow to USD 4.37 billion in 2026. Numerous companies in Asia Pacific are focused on developing and launching cutting-edge cybersecurity solutions to address the growing demand for security services and solutions.The Japan market is projected to reach USD 1.12 billion by 2026, the China market is projected to reach USD 1.31 billion by 2026, and the India market is projected to reach USD 0.41 billion by 2026.

- In June 2024, there was an announcement from Amazon Web Services (AWS) about a plan to invest USD 9 billion in Singapore over the next five years. The investment aims to improve its cloud services and infrastructure and is a part of AWS's continuous expansion in Southeast Asia. In October 2022, AWS revealed a 15-year plan to invest USD 5 billion in a cloud facility in Thailand.

Thus, above mentioned scenarios are likely to further propel the demand for these solutions in the years to come.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Developing Innovative Solutions to Provide Improved Solutions

The market position of key participants is being reinforced through the introduction of new products. Furthermore, companies are expanding their product portfolio and accomplishing organizational objectives through partnerships and collaboration strategies. Advanced technology solutions such as AI, Machine Learning (ML), and cloud are now being utilized by top companies to enhance their products and provide improved solutions.

Major Players in the Confidential Computing Market

To know how our report can help streamline your business, Speak to Analyst

The global market is consolidated, within hardware, the top players accounting for around 53% - 55% of the market share. These players sell products through their offices in these regions, while some use a multichannel distribution approach to sell their products to numerous end-user businesses.

Long List of Key Confidential Computing Players Studied

- Intel Corporation (U.S.)

- Microsoft Corporation (U.S.)

- IBM Corporation (U.S.)

- Alphabet Inc. (U.S.)

- Alibaba Group (China)

- Advanced Micro Devices, Inc. (U.S.)

- Arm Limited (U.K.)

- Edgeless Systems (Germany)

- Fortanix (U.S.)

- Anjuna Security, Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- AMAZON.COM, INC. (U.S.)

- DECENTRIQ (Switzerland)

- Profian (U.S.)

- NVIDIA Corporation (U.S.)

- phoenixNAP (U.S.)

- Evervault Inc. (U.S.)

- T-Systems International GmbH (Germany)

- Amazon Web Services, Inc. (U.S.)

- Duality Technologies (U.S.)

- Swisscom (Switzerland)

- Alpha3 Cloud (U.S.)

- OVHSAS (France)

- Many others

KEY INDUSTRY DEVELOPMENTS

- April 2025: NVIDIA announced the general availability of NVIDIA Secure AI to protect large AI models and data. NVIDIA Confidential Computing (CC) helps to safeguard large AI models and data. With NVIDIA CC, firms don't need to trade security and performance. It also includes the releases of Protected PCIe (PPCIE) mode, removal of Protected PCIe (PPCIE) mode, and Attestation changes.

- January 2025: IBM announced the expansion of its confidential computing portfolio to the Red Hat ecosystem. The declaration of Hyper Protect Container Runtime (HPCR) for Red Hat Virtualization Solutions (RHVS) and Hyper Protect Confidential Containers (HPCC) for Red Hat OpenShift Container Platform (OCP) aids the advancement of product technology.

- August 2024: Fortanix enhanced its Data Security Manager by adding file system encryption with the aim of accelerating full-stack data security. With this, the company expects to complement full disk encryption through the capabilities of securing separate file systems on particular hosts through encryption ruled by granular decryption policies.

- April 2024: Cohesity completed its strategic collaboration with Intel with the aim of leveraging the company’s confidential computing expertise in the Cohesity Data Cloud. Cohesity’s cyber vault service, built with Fort Knox, is an advanced and first-of-its-kind service in the data management ecosystem. Both companies are collaborating with the aim of reducing their end users’ risk of cyber threats. They are mainly targeting sectors such as healthcare, financial institutions, and government, where cybersecurity is very critical.

- September 2023: Intel introduced an attestation service to enhance its product portfolio. This service provides a comprehensive evaluation of Trusted Execution Environments (TEEs) in different deployment modes.

- April 2023: Microsoft extended its private VM family by launching the D and E Cesv5-series in preview. These VMs, which are equipped with Intel 4th generation Xeon Scalable processors, are supported by Intel Trust Domain Extensions (TDX), a hardware-based Trusted Execution Environment.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Several small-sized operating companies are securing funds in order to speed up and enhance their confidential computing ecosystem. These companies also use these funds to expand team size and focus on innovation in relation to the market. Companies that opt to support businesses in the financial community bolster their efforts in developing technologically advanced solutions and a global customer base.

- In August 2023, Anjuna secured funding of around USD 25 million in a Series B2 financing round with the aim of bolstering and expanding its confidential computing solutions for AI. AI Capital Partners, M Ventures, Darmstadt, SineWave Ventures, and others, headed the round. The round also witnessed equal participation from existing investors Insight Partners, Founder Collective, and others.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the factors above, it encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 34.70% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

By Deployment

By Enterprise Type

By Application

By Industry

By Region

|

|

Companies Profiled in the Report |

Intel Corporation (U.S.), Microsoft Corporation (U.S.), IBM Corporation (U.S.), Alphabet Inc. (U.S.), Alibaba Group (China), AMAZON.COM, INC. (U.S.), NVIDIA Corporation (U.S.), Huawei Technologies Co., Ltd. (China), Advanced Micro Devices, Inc. (U.S.), Arm Limited (U.K.), Edgeless Systems (Germany), Fortanix (U.S.), Anjuna Security, Inc. (U.S.), etc. |

Frequently Asked Questions

The market is projected to record a valuation of USD 350.04 billion by 2034.

In 2025, the market was valued at USD 24.24 billion.

The market is projected to grow at a CAGR of 34.70% during the forecast period (2026-2034).

The services segment is expected to lead the market.

Advancements in secure hardware enclaves and software segment drive market growth.

Intel Corporation, IBM Corporation, Microsoft Corporation, Alphabet Inc., and Advanced Micro Devices Inc. are the top players in the market.

North America holds the highest market share.

By application, the multi-party computing segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 143

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us