Continuous Variable Transmission Market Size, Share & Industry Analysis, By Type (Belt-driven CVT, Chain-driven CVT, Toroidal CVT, Hydrostatic CVT, and Others), By Component (Pulleys, Belts/Chains, and Control Units), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By propulsion Type (ICE, HEV, and BEV) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

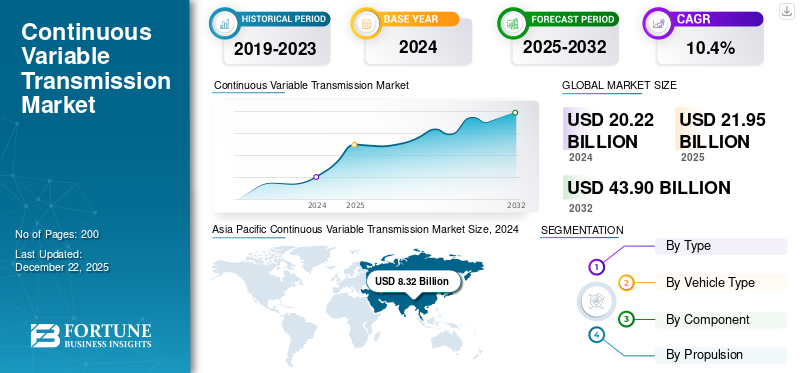

The global Continuous Variable Transmission market size was valued at USD 21.95 billion in 2025. The market is projected to grow from USD 24.04 billion in 2026 to USD 50.89 billion by 2034, exhibiting a CAGR of 9.83% during the forecast period. Asia Pacific dominated the Continuous Variable Transmission market with a market share of 44.46% in 2025.

A Continuous Variable Transmission (CVT) is an automatic transmission system that seamlessly changes through a continuous range of gear ratios, contrasting traditional transmissions that use fixed gears. It uses a belt and pulley mechanism for optimal engine performance, improving fuel efficiency and ensuring smoother acceleration. CVTs are commonly found in modern cars, especially hybrid and compact vehicles, due to their ability to maintain the engine at its most efficient Revolutions per minute (RPM). They reduce mechanical complexity, enhance driving comfort, and support better mileage, making them a popular choice for manufacturers focused on performance and economy.

The global market is experiencing steady growth due to rising demand for fuel efficient vehicles and advancements in transmission technology. Growing focus on reducing carbon emissions and improving vehicle performance has made CVT systems highly desirable in passenger cars and hybrid vehicles. Asia Pacific region dominates the market, led by strong automotive production in China and Japan.

Key players in the CVT market include Toyota Motor Corporation, Honda Motor Co. Ltd., JATCO Ltd., Aisin Corporation, and Punch Powertrain. These companies invest heavily in R&D to develop advanced, lightweight, and effective CVT systems.

The COVID-19 pandemic significantly disrupted the CVT market due to production halts, supply chain interruptions, and reduced consumer demand for automobiles. Lockdowns and restrictions in major automotive manufacturing regions, particularly Asia Pacific and Europe, led to decreased vehicle output and delayed product launches. However, as economies began recovering post-2021, there was a gradual rebound in vehicle sales, supported by pent-up demand and easing supply issues. Additionally, the shift in consumer preference toward personal mobility and fuel-efficient vehicles bolstered the CVT market. Though the pandemic caused short-term challenges, it also accelerated technological investments and digitalization efforts within the automotive sector.

Download Free sample to learn more about this report.

Continuous Variable Transmission Market Trends

Shift Toward Advanced, Lightweight CVT Designs is an Emerging Market Trend

One of the most significant ongoing trends in the CVT market is the shift toward advanced, lightweight CVT designs, exemplified by the launch of JATCO’s new CVT‑XS unit for small and medium front-wheel-drive vehicles. In October 2023, JATCO began mass production at its Mexican plant, marking a breakthrough in transmission efficiency and performance. The CVT‑XS is built on the proven CVT‑X platform which boasts a competitive edge of 90% transmission efficiency and enhances through refinements that improve drivability, responsiveness, and packaging. Key upgrades include a downsized mechanical oil pump (cutting mechanical losses), a multi-plate clutch combined with a tri‑way linear solenoid (for smoother acceleration and reduced engine revs), and a twin oil-pump setup to suppress engine revving during throttle transitions.

Additionally, a reoriented control-valve layout has reduced overall unit height, improving pedestrian safety and vehicle crashworthiness. This trend is driven by tightening regulatory emissions standards, such as the U.S. GHG/CAFE targets, prompting OEMs to pursue lighter, more efficient drivetrains without compromising safety or space. The CVT‑XS demonstrates how OEMs and suppliers innovate to reconcile fuel economy, vehicle dynamics, and regulatory compliance, making lightweight CVTs a key strategic support in future passenger vehicle design.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increasing Consumer and Regulatory Demand for Fuel-Efficient and Emission Standardization Enhances the CVT Demand

The market is the accelerating due to implementation of stricter CO₂ emissions and increase in the demand for fuel efficiency standards enforced by governments, especially in the European Union, North America, and key Asia Pacific markets. In Europe, as part of the “Fit for 55” package, EU regulators have mandated that average CO₂ emissions for new passenger cars must lower by 55% by 2030, with a full ban on combustion engine sales by 2035. To ease the transition, the EU Council recently approved a flexible compliance mechanism spanning 2025–2027, allowing manufacturers to average emissions over this period. However, to avoid heavy non-compliance penalties—potentially in billions—OEMs must harness advanced powertrains, with CVTs being key aspect for lightweight, combustion-efficient vehicles.

In the U.S., the EPA finalized rules in March 2024 demanding nearly a 50% reduction in fleet-average greenhouse gas emissions by 2032, aligning with Corporate Average Fuel Economy (CAFE) requirements driving automakers toward higher-efficiency CVT solutions in non-electric vehicles. Meanwhile, Canada confirms that CVTs typically boost fuel economy by around 4%, directly supporting emissions reduction goals. On the OEM side, manufacturers including Nissan link CVT enhancements directly to corporate sustainability targets. Their “Improving Efficiency” initiative highlights CVT as a critical tool to optimize engine RPM and minimize fuel consumption across vehicle lines. Nissan’s broader environmental goals such as reducing lifecycle CO₂ output by 30% and manufacturing emissions by 52% by 2030 compared to 2018, depend substantially on softer load powertrains, where CVT plays an significant role.

Additionally, OEMs invest in electrification by integrating CVTs into hybrid solutions. For instance, Nissan and JATCO have announced a USD 50 million for U.K. facility to manufacture 3-in-1 EV powertrains, combining CVTs and electric components, starting in 2026 with an annual capacity of 340,000 units. This strategic pairing amplifies the role of CVTs in achieving cleaner propulsion during the energy transition while supporting compliance with evolving emission standards.

Market Restraints

Limited Compatibility with High-Performance and Large Vehicle Applications is Restraining the Market Growth

Significant challenges faced by the global Continuous Variable Transmission (CVT) market include its inherent limitation in handling high-torque applications, which restricts adoption of performance-oriented vehicles, large SUVs, and heavy-duty commercial vehicles. While CVTs excel in fuel efficiency and smooth power delivery for mainstream passenger cars, their belt or chain-driven designs struggle to reliably manage the extreme torque outputs characteristic of high-performance engines, towing vehicles, or off-road applications without negotiating on durability or driving dynamics. This technical constraint has consigned CVTs primarily to economy and mid-range vehicle segments, creating a barrier to broader market penetration.

CVTs rely on frictional contact between belts/chains and pulleys to transfer power, a design that becomes problematic under high torque loads. Under sustained high torque (e.g., uphill towing or rapid acceleration), the belt-pulley interface generates excessive heat, leading to premature wear and potential slippage. For example, Subaru’s 2024 technical bulletin acknowledged limitations of its Lineartronic CVT in the Ascent SUV when towing near its 5,000-lb capacity, stimulating the brand to offer enhanced cooling systems as a retrofit.

High-torque applications demand instantaneous response, which conflicts with the CVT’s tendency to "hold" RPMs for efficiency. Nissan’s decision to abandon CVTs in its 2024 Z Nismo performance coupe (reverting to a 9-speed automatic) underscores this issue, with engineers citing driver dissatisfaction with acceleration feel. JATCO’s 2023 reliability report revealed that chain-driven CVTs in 3.5L+ engine applications (e.g., Infiniti QX60) required 30% more common chain inspections than lower-torque models.

The torque-handling limitation restricts CVTs to light-duty, efficiency-focused applications, capping their market potential. Until breakthroughs in materials science (e.g., graphene-coated belts) or hybridized designs can reliably address high-torque demands, CVTs will lack from performance and heavy-duty segments, leaving a significant portion of the transmission market to DCTs, automatics, and e-axles.

Market Opportunities

Advanced CVT Systems for High-Performance and Luxury Vehicles is a Crucial Opportunity for the Market

A significant yet underexplored opportunity for the growth of the Continuous Variable Transmission market share lies in developing high-torque, durable CVT systems for performance-oriented and luxury vehicles. Traditionally, CVTs have been associated with fuel-efficient compact cars due to their smooth acceleration and efficiency benefits. However, recent technological breakthroughs enable CVTs to handle higher power outputs and dynamic driving conditions, making them feasible for sports cars, premium sedans, and performance SUVs.

Leading transmission manufacturers are overcoming historical limitations of CVTs—such as torque capacity, belt slippage, and driver disengagement through high-strength chain and belt designs. For instance, Bosch’s CVT4EV project (2023) introduced a reinforced steel belt capable of handling 400+ Nm of torque, making it suitable for high-performance applications. Advanced control systems for sporty driving dynamics - ZF Friedrichshafen’s "CVT-Sport" software (2024) mimics stepped gear shifts in performance modes, providing the controlled response of a DCT while retaining CVT efficiency.

The high-performance CVT revolution represents a paradigm shift, transforming CVTs from economy-focused components to premium, driver-centric technologies. Manufacturers investing in torque capacity, dynamic response, and material science will capture this lucrative opportunity, reshaping the transmission landscape. Regulatory pushes for hybridization as transitional technology are accelerating e-CVT adoption. The European Union’s Euro 7 norms (2025) incentivize mild and full hybrids, where e-CVTs play a critical role. ACEA (European Automobile Manufacturers’ Association) notes that 43% of new hybrids in Europe will use CVT-based systems by 2027. Japan’s Green Vehicle Promotion Council has recognized e-CVTs as a "key transitional technology" to achieve its 2030 CO₂ targets, with subsidies for domestic OEMs developing these systems.

The e-CVT’s ability to enhance hybrid efficiency while leveraging existing manufacturing infrastructure makes it a strategic solution for automakers navigating the ICE-to-EV transition. As hybridization grows in emerging markets (e.g., India’s FAME-III subsidies) and commercial segments, the e-CVT market is poised for long-term relevance, with innovations focused on modularity and electrification inclination.

Segmentation Analysis

By Vehicle Type

Popularity and Adaptability Drive the Dominance of SUVs in the Automotive Market

Based on the vehicle type, the market is segmented into passenger vehicles, light commercial vehicles and heavy commercial vehicles. Furthermore, the passenger vehicles segment is classified into Class A, Class B, Class C, Class D, Class E, Class M, & SUV.

The SUV segment is rapidly expanding and gaining dominance in the automotive market, driven by a shift in consumer preferences toward larger vehicles, particularly for family use, along with the growing popularity of crossovers. The SUV segment is expected to lead the market, contributing 47.62% globally in 2026. This shift is reflected in the introduction of models like the Ford Bronco and Toyota RAV4, which feature dual-clutch systems to enhance performance and fuel efficiency. At the same time, the hatchback and sedan segments remain significant, with automakers such as Volkswagen, Renault, and Hyundai emphasizing fuel economy and driving dynamics, often incorporating dual-clutch transmissions in their compact and mid-size models.

Light commercial vehicles including delivery vans and pickups are transitioning from manual to automated/manual transmissions (AMT) and CVTs to meet stringent fuel & emissions norms. China’s mandate for 40% NEV penetration in LCV fleets by 2030 and tightened CAFE standards in North America drive CVT adoption. Heavy commercial vehicles such as trucks, buses, and heavy-duty machinery are increasingly leverage hydrostatic and chain CVTs for high torque, precision control, and fuel performance. Hydrostatic CVTs alone generated around USD 3 billion in 2024, projected at ~5.9% CAGR to 2034. These systems support infrastructure and logistics expansion, especially in Asia Pacific, North America, and Europe.

By Type

Belt‑Driven Segment Led the Market Due to Cost-Effective, Smooth Operation in Passenger Cars

By type, the market is classified as belt-driven, chain-driven, toroidal CVT, hydrostatic CVT, and others.

In 2026, the Belt-driven CVTs segment is projected to lead the market with a 51.24% share due to their cost-effectiveness and smooth operation, which makes them ideal for compacts and hybrids. Steel-belt innovations offer around 90% drivetrain efficiency and 5% better fuel economy as compared to traditional automatics, as highlighted by JATCO’s CVT‑XS with twin-pump lubrication. Technology focus by OEMs such as Nissan, Toyota, and Honda reinforces its global adoption in Asia Pacific, North America, and Europe.

The chain-driven CVT is the fastest-growing segment, driven by increasing demand for SUVs and performance-oriented vehicles that require robust transmission systems capable of handling higher torque without compromising efficiency. The chain-driven CVT is gaining traction in high-torque applications, such as SUVs, due to its durability and ability to handle greater power loads. The toroidal CVT, though efficient, is limited by high manufacturing costs and complexity, restricting its use to premium vehicles. The hydrostatic CVT is primarily used in agricultural and construction machinery rather than passenger vehicles.

To know how our report can help streamline your business, Speak to Analyst

By Component

Optical Performance Offered by the Pulleys Contributes to the Segmental Dominance

By component, classifies the market into pulleys, belts/chains, and control units.

The pulleys segment holds dominant market share as they are critical in adjusting gear ratios seamlessly, ensuring optimal performance. The belts/chains segment follows closely, with chains gaining prominence due to their higher durability in high-torque applications. Pulleys are a critical component in the operation of Continuous Variable Transmissions (CVTs), playing a vital role in adjusting the transmission ratio. The demand for high-performance pulleys is growing, driven by the need for smoother acceleration and better fuel efficiency in modern vehicles. Manufacturers are focusing on materials like aluminum and steel alloys for enhanced durability, performance, and weight reduction. As automakers strive to optimize CVT systems for both fuel economy and vehicle dynamics, the pulleys' design and functionality are continuously evolving, especially in the automotive sector, where efficiency is a key market driver.

The Belts/Chains segment will account for 41.06% market share in 2026. Belts and chains are integral to the operation of CVTs, serving as the medium through which power is transmitted between pulleys. The materials used for these components are continually evolving to offer improved durability, higher torque handling, and better resistance to wear. Rubber-based belts dominate the market, though steel and carbon-fiber-reinforced belts are gaining popularity for their enhanced strength and longevity. The significantly growing demand for more fuel-efficient and performance-oriented vehicles is pushing advancements in belt and chain technology, contributing to the steady expansion of this segment in the global CVT market.

Control units are central to the operation and optimization and fastest growing segment of CVT systems, as they regulate the interaction between the engine and transmission. These electronic systems ensure smooth shifting and adjust the transmission ratio based on real-time driving conditions. With advancements in automotive technology, the sophistication of control units has increased, incorporating features like adaptive learning algorithms and real-time diagnostics. As automakers move toward more intelligent and automated vehicles, the demand for advanced control units is rising, making them a crucial component in improving the efficiency and performance of CVTs across various vehicle types.

By Propulsion

Better Fuel Economy with Optimal Engine Performance Derived in ICE Vehicles Makes them Dominate the Market

By propulsion segregates the market into ICE, HEV, and BEV.

The Internal Combustion Engine (ICE) segment is projected to dominate the market with a share of 74.67% in 2026 and most established in the Continuous Variable Transmission (CVT) market. ICE vehicles, which continue to dominate global sales, benefit significantly from CVT systems due to their ability to provide smoother acceleration and improved fuel efficiency. By optimizing engine power delivery, CVTs reduce fuel consumption while maintaining performance levels, making them particularly popular in compact and mid-sized sedans, as well as in small SUVs. With rising fuel efficiency standards and increasing demand for eco-friendly solutions, automakers are investing in advanced CVT technology to meet regulatory requirements and enhance driving experience without compromising engine power.

Hybrid Electric Vehicles (HEVs) represent a rapidly growing sub-segment within the CVT market. HEVs combine an internal combustion engine with an electric motor, and the integration of CVTs in these vehicles provides several advantages. CVTs enable HEVs to seamlessly transition between electric and combustion power while optimizing fuel efficiency. Since HEVs are designed to maximize energy usage and minimize fuel consumption, the Continuous Variable Transmission’s ability to adapt to different driving conditions is crucial. As global demand for sustainable and fuel-efficient vehicles rises, HEVs equipped with CVTs are becoming increasingly popular, particularly in urban and suburban markets where fuel efficiency is a top priority.

Battery Electric Vehicles (BEVs) are beginning to incorporate CVTs, although this sub-segment remains smaller compared to ICE and HEV markets. Since BEVs rely entirely on electric power, they do not require traditional gear systems like conventional transmissions. However, some manufacturers are exploring the use of CVTs in electric drivetrains to optimize power delivery, improve efficiency, and reduce energy consumption in certain driving scenarios. BEVs with CVT technology can offer smoother acceleration and more responsive driving, which can be especially beneficial in urban environments. As BEV adoption continues to rise, the integration of CVTs may become more prevalent, especially in vehicles where efficiency and smooth performance are key selling points.

CONTINUOUS VARIABLE TRANSMISSION MARKET REGIONAL OUTLOOK

Regionally, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Continuous Variable Transmission Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed approximately USD 9.42 billion to the global market in 2025, accounting for 44.46% share, and is expected to reach USD 10.69 billion in 2026. Asia Pacific dominates the global CVT market, led by countries including Japan, China, and India. Japan is the pioneer in CVT technology, with brands such as Toyota, Honda, and Nissan extensively using CVTs across their lineups. China’s rapidly growing automotive industry and strict emission regulations fuel CVT demand, especially in compact cars. India is witnessing increased CVT adoption due to rising disposable incomes and demand for automatic transmissions in urban areas. Southeast Asian markets such as Thailand and Indonesia are also contributing, driven by local production and affordability. The fastest-growing segment is entry-level CVT-equipped hatchbacks and sedans, particularly in emerging economies where consumers prioritize fuel efficiency and ease of driving. The Japan market is projected to reach USD 1.67 billion by 2026, the China market is projected to reach USD 6.24 billion by 2026, and the India market is projected to reach USD 0.93 billion by 2026.

North America

In 2025, North America held 36.82% of the global market share, reaching a valuation of USD 8.15 billion, and is projected to grow to USD 8.85 billion in 2026. North America holds a significant share in the CVT market, driven by high demand for fuel-efficient vehicles, particularly in the U.S. The U.S. Continuous Variable Transmission Market growth is mainly contributed by automakers such as Nissan, Honda, and Subaru, which widely adopt CVTs in sedans and SUVs to meet stringent fuel economy standards (CAFE regulations). However, consumer preference for traditional automatics and dual-clutch transmissions in performance vehicles slightly limits growth. Canada and Mexico are also adopting CVTs, though at a slower pace. The region is expected to grow steadily, supported by hybrid vehicle adoption and advancements in CVT durability for larger vehicles. The fastest-growing segment in North America is SUVs with CVTs, as automakers balance performance and efficiency. The U.S. market is projected to reach USD 4.73 billion by 2026.

Europe

The market in Europe reached USD 3.83 billion in 2025, representing 16.32% of total market revenue, and is projected to reach USD 3.92 billion in 2026. Europe is a mature yet growing CVT market, with demand primarily driven by stringent emission norms (Euro 6/7) and a strong focus on fuel efficiency. Western European countries such as Germany, France, and the U.K. lead in CVT adoption, particularly in compact and hybrid vehicles. However, the preference for manual and dual-clutch transmissions in premium and performance cars restrains full-scale CVT penetration. Eastern Europe shows slower adoption due to cost sensitivity and a used-car-dominated market. The fastest-growing segment is hybrid CVTs, as European automakers integrate them into mild and full hybrids to comply with CO₂ reduction targets. Increasing SUV sales with CVT options further support the region’s growth. The UK market is projected to reach USD 0.21 billion by 2026, while the Germany market is projected to reach USD 0.77 billion by 2026.

Rest of the World

The Rest of the World market accounted for USD 0.55 billion in 2025, representing 2.41% of the global industry, and is expected to reach USD 0.58 billion in 2026. The Rest of the World, including Latin America and the Middle East & Africa, represent a smaller but emerging CVT market. Latin America, particularly Brazil and Argentina, shows moderate CVT adoption due to economic fluctuations and a preference for low-cost manual transmissions. The Middle East has limited CVT penetration, as consumers favor rugged SUVs with conventional automatics. Africa’s market remains underdeveloped, constrained by low new-car sales and affordability issues. However, the fastest-growing segment in Rest of the World is budget-friendly CVT models in Latin America, where automakers are introducing cost-effective automatic options to cater to urban commuters. Government policies promoting fuel efficiency may drive gradual CVT adoption in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation, Diverse Product Portfolio, Quality, and Reliability make JATCO Ltd. a Leading Player

JATCO Ltd., a subsidiary of Nissan Motor Co., is widely recognized as the world’s largest manufacturer of CVTs. Established in 1999, JATCO’s leadership stems from its early and extensive focus on CVT technology, which it pioneered and refined through continuous R&D investment. JATCO’s global reach includes manufacturing plants in Japan, Mexico, China, and Thailand, enabling efficient supply chain management and close collaboration with automakers worldwide. The company’s innovative CVT designs, such as the CVT8 and CVT9 series, offer enhanced fuel efficiency, smoother acceleration, and improved durability, which align with stringent global emission standards. JATCO’s portfolio includes belt-driven CVTs, chain-driven CVTs, and advanced e-CVTs for hybrid vehicles, supporting a wide range of passenger cars, SUVs, and light commercial vehicles. Its technological leadership and partnerships with major OEMs such as Nissan, Mitsubishi, and Renault have coagulated its position globally as the dominant CVT supplier.

Aisin Seiki Co., Ltd., part of the Toyota Group, is the second-largest CVT manufacturer. Known for its precision engineering, advanced hydraulics, and electronics integration, Aisin’s CVT portfolio caters to traditional internal combustion engines and hybrid electric vehicles. Their CVT products include belt-driven systems, chain-driven transmissions, and e-CVTs, focusing on durability and compact design. Aisin’s collaborations with Toyota and other automakers have helped popularize their transmissions in global markets. Their recent innovations emphasize improving fuel economy and reducing noise, vibration, and harshness (NVH), supporting Toyota’s hybrid models such as the Prius and Corolla Hybrid. Aisin’s global manufacturing footprint and strong R&D investments ensure it remains a key competitor in the CVT landscape.

LIST OF KEY CONTINUOUS VARIABLE TRANSMISSION COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Aisin Corporation (Japan)

- JATCO Ltd (Japan)

- BorgWarner Inc. (U.S.)

- Getrag (Magnus Powertrain) (Germany)

- Eaton Corporation (U.S.)

- Schaeffler Group (Germany)

- Hyundai Transys (South Korea)

- Dana Incorporated (U.S.)

- GKN Automotive (Dowlais Group) (U.K.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Subaru launched its third-generation Crosstrek Hybrid, featuring a series-parallel hybrid powertrain with an eCVT. The vehicle is equipped with a Next-generation Subaru series-parallel hybrid system combining a newly developed 2.5-liter SUBARU BOXER engine with electric motors, a high-capacity lithium-ion battery, and CVT. Legendary Subaru Symmetrical All-Wheel Drive and Advanced EyeSight Driver Assist Technology are standard.

- February 2025: Zenvo partners with Ricardo for transmission development of the hypercar Aurora.

- July 2024: Nissan Motor India has reintroduced the 4th-generation X-Trail as a Completely Built Unit (CBU) in India, emphasizing its "Made in Japan" origin. The SUV has a 3rd-generation XTRONIC CVT (Continuous Variable Transmission) featuring D-Step Logic Control and paddle shifters. This launch marks the resumption of Nissan's CBU business in India, highlighting the X-Trail's focus on fuel efficiency and a refined driving experience

- August 2023: Nidec Power Train Systems Develops New Electric Oil Pump for CVT. This latest product is used to supply oil pressure to the CVT system of a vehicle in the idling-stop mode, and support a car’s engine-driven mechanical oil pump. In an active attempt to reduce their vehicles’ CO2 emissions, individual car manufacturers are shifting toward producing electric and hybrid vehicles and other eco-friendly cars equipped with an idling-stop function.

- December 2024: Italian company Alter Ego and kinematic studies undertaken at the Milan Technical University developed a beautifully complex new mechanism, the world's first geared CVT – 10% more efficient than a regular belted CVT.

REPORT COVERAGE

The global Continuous Variable Transmission market report provides detailed market analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.83% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Component

By Vehicle Type

By Propulsion Type

By Region North America (By Type, By Vehicle Type, By Component, By Propulsion Type, and by Country)

Europe ( By Type, By Vehicle Type, By Component, By Propulsion Type, and by Country )

Asia Pacific ( By Type, By Vehicle Type, By Component, By Propulsion Type, and by Country )

|

Frequently Asked Questions

Fortune Business Insights says the market will reach USD 50.89 billion by 2034.

The market is expected to grow at a CAGR of 9.83% during the forecast period.

Increasing consumer and regulatory demand for fuel-efficient and environmentally friendly vehicles enhances the demand for CVT.

Asia Pacific dominated the Continuous Variable Transmission market with a market share of 44.46% in 2025.

Asia Pacific market size share was USD 9.42 Billion in 2025.

ZF, Aisin, BorgWarner, Getrag, and JATCO are a few of the leading market players operating in the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us