Convenience Food Market Size, Share & Industry Analysis, By Product Form (Ready-to-Eat (RTE), Ready-to-Heat (RTH), Ready-to-Cook (RTC) and Instant Shelf-Stable Foods), By Storage Condition (Frozen, Ambient/Shelf-Stable and Chilled/Refrigerated), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail & Quick Commerce, and Others) and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

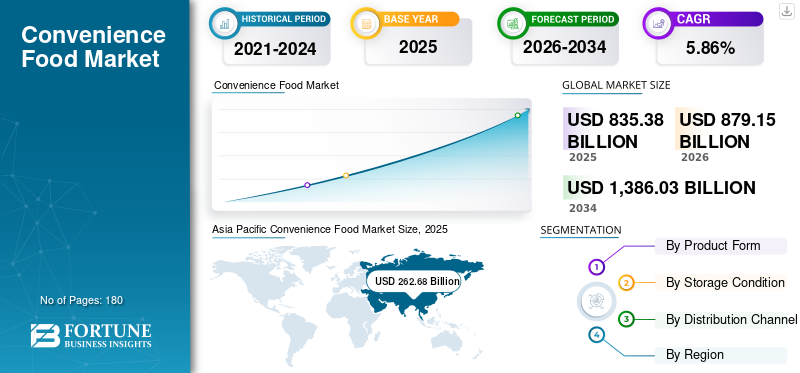

Convenience Food Market Size and Future Outlook

The global convenience foods market size was valued at USD 835.38 billion in 2025. The market is projected to grow from USD 879.15 billion in 2026 to USD 1,386.03 billion by 2034, exhibiting a CAGR of 5.86% during the forecast period. Asia Pacifc dominated the global convenience foods market with a market share of 31.44% in 2025.

Convenience foods are food products that are partially or fully prepared and designed to minimize the time, effort, and skill required for cooking or meal preparation. From ready-to-eat meals to instant shelf-stable snacks, convenience foods fill store shelves with options that are easy to store, quick to prepare, and reliably tasty. Their popularity is growing as city life speeds up, consumers lead busier lives, and the number of dual-income and single-person households increases.

Companies such as Nestlé S.A., Unilever plc, and Conagra Brands, Inc. are key players operating in this market. New product launch and production capacity expansion are the key strategies adopted to boost product sales and support the growth of the convenience food market.

Download Free sample to learn more about this report.

CONVENIENCE FOODS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 835.38 Billion

- 2026 Market Size: USD 879.15 Billion

- 2034 Forecast Market Size: USD 1,386.03 Billion

- CAGR: 5.86% from 2026–2034

- Asia Pacific dominated the convenience foods market with a 31.44% share in 2025.

- Ready-to-Eat (RTE) foods accounted for the largest product form segment in 2025.

- Supermarkets & hypermarkets held the largest distribution channel share in 2025.

Asia Pacific

Asia Pacific generated USD 262.68 billion in 2025 and remained the largest regional market.

North America

North America reached USD 235.47 billion in 2025, driven by strong demand for premium and innovative convenience foods.

Europe

Europe recorded USD 196.01 billion in 2025, supported by demand for ready-to-heat and health-focused food products.

U.S.

The convenience foods market reached USD 186.40 billion in 2025.

Japan

The convenience foods market reached USD 47.54 billion in 2025, accounting for 5.69% of global revenue.

Read More

CONVENIENCE FOOD MARKET TRENDS

Growth of E-commerce to Boost Market Growth

Current trends in convenience foods reflect a shift toward healthier, plant-based, and sustainably packaged products. Increasing incorporation of fruits and vegetables into convenience foods is enhancing nutritional value and broadening consumer appeal across everyday meal categories. Such products appeal to busy, health-conscious consumers, with a pronounced focus on clean labels and functional ingredients. Rapid expansion, particularly in response to rapid urbanization and increased demand for convenient nutrition, also supports convenience food market growth. Environmental concerns are also shaping the trend, as the rapid adoption of eco-friendly packaging solutions for ready-meal options, including recyclable and biodegradable materials. Moreover, the growth of e-commerce, online food delivery, and the integration of smart, AI-driven, or personalized nutrition options transformed consumer access. Together, these trends indicate a market evolving toward higher differentiation, omnichannel distribution, and more informed consumer choice.

MARKET DYNAMICS

MARKET DRIVERS

Urban Lifestyles and Time Scarcity Are Accelerating Demand for Convenient Food

The global convenience food market is growing rapidly, driven by urbanization, time constraints, and changing household structures, with a growing proportion of dual-income families and single-person households. As consumers want products that can be prepared easily with minimal cooking effort, demand for ready-to-eat, ready-to-heat, and instant foods continues to rise. Moreover, advances in food processing, freezing, and packaging technologies have improved product quality, shelf life, and safety. In emerging economies, rising disposable incomes and the adoption of Western dietary patterns are key drivers of demand for packaged convenience foods. Ongoing innovation in flavors, portion sizes, and protein-enriched options is attracting younger consumers and supporting sustained growth across both developed and developing markets.

MARKET RESTRAINTS

Volatile Raw Material Prices Are Constraining the Pace of Market Expansion

Convenience foods are often associated with high sodium content, preservatives, and ultra-processed ingredients, which can lead to health complications such as obesity, diabetes, and others. This perception deters health-conscious consumers from purchasing such products. Moreover, volatile raw material prices can increase production costs, impacting product affordability, particularly in emerging markets, constraining premiumization. Moreover, uneven cold-chain infrastructure and limited penetration in emerging economies are limiting the penetration of frozen and chilled products in certain regions.

MARKET OPPORTUNITIES

Modern Retail Infrastructure Penetration In Emerging Economies is Unlocking New Growth Pathways for the Market

Frozen and ready-to-cook segments remain underpenetrated in these markets, primarily due to cold-chain and modern retail infrastructure penetration in emerging economies. However, E-commerce and quick-commerce platforms offer additional opportunities for manufacturers, as they enable direct consumer engagement, support the sale of personalized assortments, and raise awareness of premium product offerings from different brands. Companies are also launching tailored, localized product flavors in the market to meet the growing market demand. In addition, rising demand for clean-label, low-sodium, high-protein, plant-based, and functional convenience foods is creating significant opportunities for product innovation.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Form

Ready-to-Eat (RTE) foods Segment Held Majority Market Share Due to Rising Urbanization

By product form, the market is segmented into Ready-to-Eat (RTE), Ready-to-Heat (RTH), Ready-to-Cook (RTC), and instant shelf-stable foods.

The ready-to-Eat (RTE) foods segment accounted for the largest market share in 2025. The Ready-to-Eat (RTE) foods segment maintains a dominant position in the convenience food market, primarily as it eliminates the need for preparation time, appealing to consumers with limited time. There is a growing prevalence of on-the-go lifestyles due to urbanization and the rise of single-person households. Widespread availability of chilled and ambient ready-to-eat meals in supermarkets and convenience stores also supports product sales.

The instant shelf-stable foods segment is another fastest-growing food category that is expected to grow at a CAGR of 6.01% during the forecast period, driven by their affordability, long shelf life, and minimal preparation needs. These products are available through modern and traditional retail channels, especially in emerging markets. These products are also economical and hence favored by the price conscious consume segments.

By Storage Condition

Ambient/Shelf-Stable Segment Accounted For the Leading Market Share Due To its Extended Shelf Life

Based on storage condition, the market segment includes frozen, ambient/shelf-stable, and chilled/refrigerated.

The ambient and shelf-stable segment accounted for the largest convenience food market share, primarily due to its extended shelf life, minimal storage requirements, and widespread availability across various retail formats. Such products do not require refrigeration or freezing and are widely distributed through modern and traditional retail channels, particularly in emerging markets. Such products are economical and can be easily transported as they do not require any additional old storage infrastructure. Hence, such products are highly attractive to price-sensitive consumers. Moreover, expanding demand for products such as instant noodles, soups, and meal mixes among consumers continues to reinforce the dominance of this segment.

Frozen is another major segment, amounting to 5.71% CAGR during the forecast period. Frozen convenience foods account for the fastest-growing segment owing to longer preservation of taste and nutrition, and growing household freezer penetration. With the expansion of cold-chain infrastructure, consumer acceptance of such products has increased significantly, especially in developed markets.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Supermarkets and Hypermarkets Accounted For the Majority Market Share Due to their Broad Product Assortments

By distribution channel, the market is segmented into supermarkets & hypermarkets, convenience stores, online retail & quick commerce, and others.

The supermarkets & hypermarkets segment held the largest market share in 2025, dominating the convenience food market. The dominance is attributed to their broad product assortments, competitive pricing, and one-stop shopping experience. These channels offer extensive shelf space for frozen, chilled, ambient, and private-label products, enabling consumers to compare brands and prices before making a purchase. Supermarkets benefit from high levels of consumer trust and established shopping routines, which position them as the preferred channel for bulk and family-size convenience food purchases.

The online and quick-commerce channels segment is the fastest-growing distribution channel with an estimated CAGR of 7.01% from 2026 to 2032. The growth of this channel is primarily driven by the increased adoption of digital platforms by consumers. These platforms offer unmatched convenience, rapid delivery, and personalized recommendations, encouraging higher-value basket sizes.

Convenience Food Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Convenience Food Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market is valued at USD 262.68 billion in 2025 and is one of the fastest-growing regions and the leading region in the world. This market includes instant shelf-stable foods and chilled products, which are popular among consumers due to their affordability and availability, particularly in China, India, and Southeast Asia. With the rise in disposable income and the growing number of people joining the workforce, time-saving meals are growing in popularity in India, China, Japan, Southeast Asia, South Korea, and other countries. Although ambient meal and chilled products are popular, frozen and RTC segments remain under-penetrated but rapidly emerging in urban populations.

India Convenience Food Market

The India market in 2025 was around USD 42.86 billion, accounting for roughly 5.13% of global market revenues.

China Convenience Food Market

China’s market in 2025 was around USD 88.37 billion, representing roughly 10.58% of global market sales.

Japan Convenience Food Market

The Japan market in 2025 reached around USD 47.54 billion, accounting for roughly 5.69% of global market revenues.

North America

The market in North America reached around USD 235.47 billion in 2025. The market is primarily driven by high popularity, the premiumization of these products, and strong product innovation by key market players. There is strong demand for ready-to-heat and ready-to-cook products among consumers, as they are suitable for those with time scarcity, leading to high acceptance. Manufacturers are developing health-oriented product reformulations, including high-protein, low-sodium, and clean-label claims to attract health-conscious consumers. The market is expected to grow further as online and quick-commerce channels expand, favoring bundled, premium offerings in product sales in this region.

U.S. Convenience Food Market

In 2025, the U.S. market reached USD 186.40 billion. The U.S. market is the largest and most innovative convenience food market, and its growth is supported by high product turnover and strong consumer demand for these products. Some of the key products popular in the market include Frozen ready meals, snacks, and protein-centric RTC products. The country has an advanced cold-chain infrastructure and broad retail coverage, which further supports market growth. Moreover, premium frozen meals, ethnic cuisines, and functional convenience foods are gaining traction, allowing manufacturers to innovate and launch new products further.

Europe

The European market reached USD 196.01 billion in 2025. The market is growing relatively slowly and steadily compared to the North American market. Products such as ready-to-heat and ready-to-cook foods are more popular in Northern and Western Europe than in Southern Europe, where home-cooked food is preferred. Despite limited popularity, companies have the opportunity to expand their chilled ready meals and health-positioned products targeted at health-conscious consumers. Innovation in product offerings for consumers following vegan or flexitarian diets also creates opportunities for innovation and market expansion.

Germany Convenience Food Market

The market in Germany in 2025 reached around USD 35.91 billion, representing roughly 4.30% of global market revenues.

U.K. Convenience Food Market

The U.K.’s market reached approximately USD 33.36 billion in 2025, equivalent to around 3.99% of global market sales.

South America and Middle East and Africa

South America is expected to experience significant growth in this market over the forecast period. The South America market in 2025 recorded USD 61.02 billion, and the region is projected to exhibit strong growth in the future. The market in South America is experiencing steady demand for convenience food products. The retail infrastructure in such countries is growing rapidly, which is boosting the market’s growth. Instant and ambient foods constitute the largest market segments, and they are popular among price-conscious consumers. Moreover, frozen and ready-to-cook (RTC) products are experiencing increased adoption in Brazil, Chile, and Argentina. Manufacturers are offering value packs and manufacturing products made from locally sourced inputs to maintain affordability. The Middle East and Africa region reached USD 80.20 billion in 2025. The Middle East and Africa market is poised for substantial structural growth, supported by ongoing urbanization and rising population levels. There is an increased uptake of instant and ambient convenience foods such as frozen, chilled, and premium ready meals. Some of the key market drivers of the Middle East market include expansion of retail infrastructure, expansion of modern grocery formats, and the rapid growth of quick-commerce platforms. However, a lack of strong cold-chain infrastructure and high price sensitivity in several African regions hinder convenience foods market growth.

UAE Convenience Food Market

The UAE market is set to grow at a CAGR of 5.84% during the forecast period. Ambient products and ready-to-eat products are the major products consumed in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Investments to Expand March Reach

The global convenience food market is moderately consolidated, with large multinational companies such as Nestlé, Unilever, Kraft Heinz, Conagra Brands, and General Mills operating across multiple countries and competing in various product segments. Regional companies are also competing with these companies by strengthening their product portfolios and offering localized flavors at competitive prices tailored to local consumer preferences. As consumers increasingly shift toward product differentiation, companies are focusing on health-oriented, protein-enriched foods with clean-label claims. Moreover, with the rise of e-commerce and quick-commerce distribution channels, manufacturers are investing in new packaging solutions and establishing distribution partnerships with local e-commerce service providers to compete and expand market reach.

LIST OF CONVENIENCE FOOD COMPANIES PROFILED

- Nestlé S.A. (Switzerland)

- Unilever plc (U.K.)

- Conagra Brands, Inc. (U.S.)

- Kraft Heinz Company (U.S.)

- General Mills, Inc. (U.S.)

- Ajinomoto Co., Inc. (Japan)

- McCain Foods Limited (Canada)

- Tyson Foods, Inc. (U.S.)

- BRF S.A. (Brazil)

- Maruha Nichiro Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Conagra Brands, Inc., one of the leading food manufacturers, launched more than 50 delicious new frozen foods in the market. This includes single-serve and multi-serve meals, vegetable side dishes, and gluten-free and plant-based meals.

- May 2025: Kraft and Heinz company launched a new snack product in the market, namely Lunchable PB&J. This is a dippable snack which is made of crustless peanut butter and jelly.

- November 2024: Nestlé expanded its plans to expand its convenience food production operations by investing USD 150 million to expand a frozen meals production facility in the U.S. market.

- March 2024: Nestle launched a new frozen-food brand named Vital Pursuit that aimed at consumers who are using weight loss drug GLP-1 drugs such as Ozempic and Wegovy.

- May 2023: Kraft Heinz launched a frozen version of its signature Macaroni & Cheese product in the market. This product is available in Original Cheddar and Four Cheese versions across major retail stores in the U.S. market.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.86% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Form, By Distribution Channel, By Storage Condition, and By Region |

|

By Product Form |

· Ready-to-Eat (RTE) · Ready-to-Heat (RTH) · Ready-to-Cook (RTC) · Instant Shelf-Stable Foods |

|

By Distribution Channel |

· Supermarkets & Hypermarkets · Convenience Stores · Online Retail & Quick Commerce · Others |

|

By Storage Condition |

· Frozen · Ambient/Shelf-Stable

|

|

By Region |

North America (By Product Form, By Distribution Channel, By Storage Condition, and Country)

Europe (By Product Form, By Distribution Channel, By Storage Condition, and Country)

Asia Pacific (By Product Form, By Distribution Channel, By Storage Condition, and Country)

South America (By Product Form, By Distribution Channel, By Storage Condition, and Country)

Middle East and Africa (By Product Form , By Distribution Channel, By Storage Condition, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 835.38 billion in 2025 and is projected to reach USD 1,386.03 billion by 2034.

In 2025, the market value stood at USD 262.68 billion.

The market is expected to exhibit a CAGR of 5.86% during the forecast period.

By distribution channel, the supermarkets & hypermarkets segment led the global market in 2025.

Urban lifestyles and time scarcity are the key factors driving the market.

Nestle S.A., Unilever plc, and Conagra Brands, Inc. are the top players in the market.

Asia Pacific held the largest market share in 2025.

Growth of e-commerce is the key market trend.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us