Copper Clad Laminates Market Size, Share & Industry Analysis, By Product Type (Rigid CCL, Flexible CCL, High Performance CCL, Advanced Substrate CCL, and Metal Core CCL), By End Use (Consumer Electronics, Computing & Data Infrastructure, Telecommunication, Automotive, Industrial & Power, and Others), and Regional Forecast, 2026-2034

Copper Clad Laminates Market Size and Future Outlook

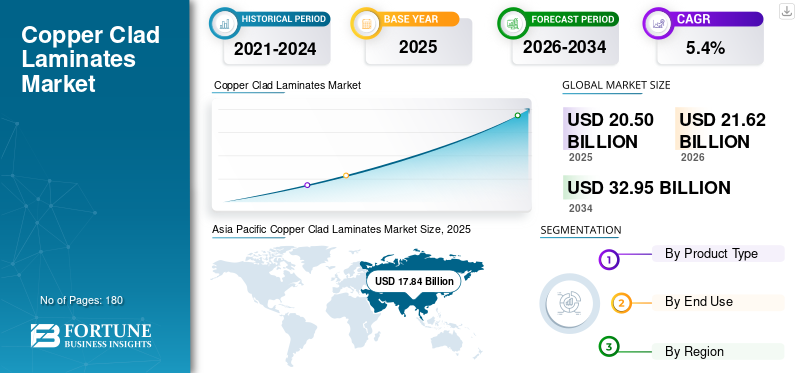

The global copper clad laminates market size was valued at USD 20.50 billion in 2025. The market is projected to grow from USD 21.62 billion in 2026 to USD 32.95 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the copper clad laminates market with a market share of 87.02% in 2025.

Copper clad laminates (CCL) are highly engineered base materials used in the production of printed circuit boards (PCBs), in which CCLs are bonded to a substrate material, such as glass fiber cloth, paper, or a composite material, and are impregnated with resin and laminated to copper foil on one or both sides. These laminates serve as the foundational conductive platform for forming electronic circuits. The rising penetration of artificial intelligence infrastructure, 5G technologies, advanced driver-assistance systems, and high-performance consumer electronics is driving the global market. AI servers, GPUs, telecom base stations, automotive control units, power electronics, and high-density interconnect boards require laminate materials with low dielectric loss and better dimensional control under demanding operating conditions. Therefore, market growth is increasingly being supported by the shift toward higher-value laminate solutions rather than only volume expansion in conventional PCB materials.

The global market is shaped by a concentrated group of established laminate manufacturers with strong capabilities in resin formulation, glass-fabric treatment, copper-foil integration, and precision lamination technologies.

Key players include Kingboard Laminates, Shengyi Technology, Nan Ya Plastics, Elite Material Co. (EMC), AGC Inc., and Doosan Electro-Materials. Continuous investments in high-performance resin systems, low-loss material platforms, supply chain localization, and capacity expansion for premium laminate grades continue to strengthen their competitive positioning in the evolving global electronics materials ecosystem.

Download Free sample to learn more about this report.

Copper Clad Laminates Market Key Takeaways

- 2025 Market Size: USD 20.50 billion

- 2026 Market Size: USD 21.62 billion

- 2034 Forecast Market Size: USD 32.95 billion

- CAGR: 5.4% from 2026–2034

- Asia Pacific dominated the market with an 87.02% share in 2025.

- The rigid CCL segment held the largest market share in 2025.

- The consumer electronics segment accounted for the largest market share in 2025.

Asia Pacific

Asia Pacific led the market with USD 17.84 billion and an 87.02% share in 2025.

North America

North America reached USD 1.23 billion in 2025 and is projected to grow at a 4.9% CAGR.

Europe

Europe recorded USD 1.03 billion in 2025 and is expected to expand at a 4.6% CAGR.

U.S.

The market is projected to reach USD 1.24 billion by 2026.

Japan

The market is a key contributor, supported by its advanced electronics and semiconductor manufacturing industry.

Read More

COPPER CLAD LAMINATES MARKET TRENDS

Trend toward Miniaturization and Increasing Use of High-Frequency Materials to Fuel Product Adoption

The trend toward miniaturization across consumer electronics, communication devices, automotive modules, and computing hardware is significantly increasing the adoption of advanced copper clad laminates. As electronic systems become more compact and functionally dense, PCB materials must support finer circuitry, improved dimensional stability, enhanced heat resistance, and reliable electrical performance within limited board space. The growing use of high-frequency materials is becoming essential as 5G infrastructure, AI servers, high-speed networking equipment, and radar-based automotive systems require faster signal transmission with minimal loss. This is driving demand for low-loss, low-dielectric, and high-Tg laminate grades that can maintain signal integrity in complex multilayer board designs. Therefore, miniaturization and high-frequency performance requirements are steadily driving the market toward more specialized, higher-value CCL products.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth in Electric Vehicles and Rising Demand for Consumer Electronics to Drive Market Growth

The significant growth of electric vehicles and the rising demand for consumer electronics are driving expansion in the global market. Electric vehicles require more printed circuit boards across battery management systems, power control units, infotainment modules, onboard chargers, and advanced driver-assistance systems, thereby increasing demand for a product capable of meeting these requirements. Continued demand for smartphones, laptops, wearable electronic devices, gaming systems, and smart home products is driving large-scale PCB production across compact, function-dense electronic applications. These end-use sectors require products with strong thermal stability, electrical insulation, dimensional consistency, and long-term durability. Therefore, the growing demand for advanced electronic systems and next-generation PCB materials in electric vehicles and consumer electronics is set to drive the global copper clad laminates market growth during the forecast period.

MARKET RESTRAINTS

Strict Certification Requirements May Limit Market Expansion

One of the key restraints in the global market is the combination of lengthy qualification cycles, strict certification requirements, and persistent cost pressures across the electronics value chain. CCL materials are deeply embedded in PCB reliability, thermal behavior, and electrical performance, making customers cautious when shifting between suppliers or adopting new formulations without extensive testing and validation. At the same time, periodic producer price revisions indicate continued pressure on raw materials and operating costs, which can limit adoption in cost-sensitive applications. Compliance and certification-related issues can also disrupt customer confidence and the continuity of qualification. For example, disclosures by Panasonic Industry Co., Ltd. regarding irregularities in third-party certification processes, followed by product withdrawals or revisions, illustrate how certification issues can affect market trust and supply relationships. Therefore, commercial scaling in this market is often slower and more complex than underlying demand growth, particularly in applications requiring high reliability and long-term performance validation.

MARKET OPPORTUNITIES

Expansion of 5G Infrastructure and Rising Deployment of AI Servers to Create Several Growth Opportunities

The expansion of 5G infrastructure and the growing deployment of AI servers are creating lucrative opportunities in the global market by accelerating demand for high-performance PCB materials. Advanced telecommunication systems, including 5G base stations, telecom transmission equipment, and high-speed networking systems, require laminate materials with low dielectric loss, stable signal transmission, and strong thermal resistance to support high-frequency performance. Similarly, AI servers and data center hardware rely on complex multilayer boards that require superior dimensional stability, heat management, and reliable electrical performance under high processing loads. This is increasing the market potential for low-loss, high-speed, and specialty copper clad laminates used in advanced communication and computing applications. Therefore, the ongoing buildout of next-generation digital infrastructure is shifting demand toward premium-value laminate solutions and opening attractive growth opportunities for specialized CCL manufacturers.

- For instance, according to 5G Americas, 5G adoption is experiencing significant growth, with global connections exceeding 2.25 billion in April 2025, expanding 4 times faster than 4G.

Segmentation Analysis

By Product Type

Rigid CCL Dominates the Market Owing to Its Extensive Use Across Various Industries

Based on product type, the market is segmented into Rigid CCL, Flexible CCL, High-Performance CCL, Advanced Substrate CCL, and Metal Core CCL.

Rigid CCL segment accounts for the largest share of the global market due to its extensive use in multilayer and double-sided printed circuit boards across consumer electronics, industrial systems, networking equipment, and automotive electronics. These laminates offer strong dimensional stability, electrical insulation, mechanical strength, and process compatibility, making them suitable for high-volume PCB manufacturing. Their widespread adoption in conventional and performance-driven electronic applications continues to support market dominance.

High-performance CCL is expected to grow at a CAGR of 5.9% during the study period. They are experiencing strong demand as electronic systems increasingly require superior thermal resistance, low dielectric loss, high glass transition temperature, and stable electrical performance under demanding operating conditions. These materials are used in high-speed computing, telecom infrastructure, advanced automotive electronics, industrial automation, and mission-critical electronic assemblies where conventional laminate grades may not be sufficient. Therefore, the growing emphasis on performance optimization, operating stability, and advanced application compatibility will steadily expand the segment’s growth.

By End Use

Consumer Electronics Segment Led the Market Due to High Production Volumes of Gadgets

Based on end use, the market is segmented into consumer electronics, computing & data infrastructure, telecommunication, automotive, industrial & power, and others.

Consumer electronics accounted for the largest global copper clad laminates market share in 2025, driven by high production volumes of smartphones, laptops, tablets, televisions, gaming devices, wearables, and smart home products. These applications require printed circuit boards that offer consistent electrical insulation, mechanical stability, and compatibility with compact, high-density electronic designs. Continuous product innovation, shorter replacement cycles, and rising integration of advanced features are supporting steady demand for both standard and performance-oriented CCL materials.

To know how our report can help streamline your business, Speak to Analyst

The telecommunications segment is growing at a CAGR of 5.1% during the forecast period, driven by the large-scale deployment of communication equipment, routers, switches, transmission systems, base stations, and network hardware. As telecom infrastructure evolves toward 5G and future high-frequency communication standards, there is an increasing need for laminates with lower dielectric loss, improved signal transmission, and greater thermal and dimensional stability. In addition, expanding broadband connectivity and investments in digital communications continue to support PCB material consumption.

Copper Clad Laminates Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Copper Clad Laminates Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 17.84 billion. The region is expected to maintain its leadership by 2026, reaching USD 18.81 billion, driven by its deeply integrated electronics manufacturing ecosystem and the strong concentration of PCB, semiconductor packaging, consumer electronics, and communication equipment production across China, Taiwan, Japan, and other Asian countries. Large-scale manufacturing of smartphones, computing systems, telecom infrastructure, and automotive electronics continues to support high laminate consumption.

China Copper Clad Laminates Market

China represented the largest country market in 2026, reaching USD 10.72 billion and accounting for approximately 50% of the global market value. Its commanding position is supported by the country’s massive PCB manufacturing base, extensive electronics assembly capacity, and strong presence across consumer electronics, telecom equipment, industrial systems, and automotive electronics.

To know how our report can help streamline your business, Speak to Analyst

Taiwan Copper Clad Laminates Market

Taiwan emerged as another significant market, reaching USD 2.83 billion in 2026, representing nearly 13% of the global market. The country’s importance stems from its strong position in advanced electronics manufacturing, semiconductor packaging, high-performance computing hardware, and sophisticated PCB production.

North America

The North American market was valued at USD 1.23 billion in 2025 and is projected to grow at a CAGR of 4.9% during the study period. Regional demand is supported by strong consumption across data infrastructure, automotive electronics, aerospace systems, industrial electronics, and specialized communication equipment. The market also benefits from increasing emphasis on domestic electronics manufacturing resilience, higher-value PCB applications, and advanced electronic system design.

U.S. Copper Clad Laminates Market

The U.S. market is expected to reach USD 1.24 billion by 2026, accounting for around 6% of global revenues. Demand in the country is supported by a broad end-use base spanning computing systems, telecom infrastructure, defense electronics, industrial controls, automotive electronics, and data center hardware. The U.S. market also reflects stronger adoption of technologically advanced PCB materials in applications requiring signal integrity, thermal stability, and reliability under complex operating conditions.

Europe

Europe reached USD 1.03 billion in 2025 and is likely to expand at a CAGR of 4.6% during the study period. The region represents a technically sophisticated yet relatively specialized market, with demand primarily linked to automotive electronics, industrial automation systems, power electronics, medical devices, and communication hardware. Although Europe does not match Asia in terms of large-scale electronics manufacturing volumes, it retains strategic importance through high-value, reliability-focused applications that require strong electrical performance and thermal endurance.

Germany Copper Clad Laminates Market

Germany is poised to account for USD 0.33 billion by 2026, representing nearly 2% of global market demand. Its position in the market is strongly supported by the country’s advanced automotive manufacturing base, leadership in industrial automation, and the growing use of electronics in power management and control systems.

U.K. Copper Clad Laminates Market

The U.K. market is expected to reach USD 0.15 billion by 2026, accounting for around 1% of global revenues. Market demand in the country is supported by the use of electronics across industrial systems, communication equipment, defense-related applications, instrumentation, and selected automotive and specialty manufacturing sectors.

Rest of World

The rest of the world market stood at USD 0.41 billion in 2025 and is anticipated to grow at a CAGR of 5.3% during the forecast period. The demand is anticipated on the back of emerging electronics manufacturing locations across Latin America, the Middle East, and other developing regions. Consumption is largely supported by industrial electronics, electrical systems, automotive electronic components, consumer device assembly, and gradually expanding PCB production capabilities. While the region remains comparatively smaller in absolute market size, it is benefiting from the diversification of electronics supply chains and the gradual development of localized manufacturing ecosystems.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Investment to Boost their Product Portfolio

The global market is moderately consolidated, with competition led by a defined group of large Asian and international manufacturers that combine scale, materials engineering, and close PCB-customer integration. Leading players such as Kingboard Laminates, Shengyi Technology, Nan Ya Plastics, Elite Material Co. (EMC), Taiwan Union Technology, Panasonic Industry, and Rogers Corporation maintain strong market positions through broad laminate portfolios and advanced material engineering capabilities. Companies across the sector are increasingly channeling capital into low-loss, high-speed laminates for AI servers and digital infrastructure, as reflected in Panasonic Industry’s MEGTRON expansion plans. At the same time, Ventec and Shengyi’s Thailand developments indicate a strategic push toward supply-chain resilience and localized production footprints. Therefore, market evolution is being driven by technology-focused investment strategies.

LIST OF KEY COPPER CLAD LAMINATES COMPANIES PROFILED

- AGC Inc (Japan)

- Chukoh Chemical Industries Ltd. (Japan)

- Doosan Corporation Electro-Materials (South Korea)

- ITEQ Corporation (Taiwan)

- Isola Group (U.S.)

- Kingboard Laminates (China)

- Mitsubishi Gas Chemical (MGC) (Japan)

- Nan Ya Plastics (Taiwan)

- Shengyi Technology (China)

- Rogers Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Panasonic Industry announced an investment worth approximately USD 0.05 billion for a new MEGTRON circuit board materials production line in Ayutthaya, Thailand. The expansion is intended to address rising demand for AI servers and strengthen the company’s ability to supply high-performance multilayer circuit board materials for next-generation computing and data infrastructure applications.

- September 2025: Panasonic Industry disclosed plans to invest approximately USD 110 million to double the production capacity of MEGTRON multi-layer circuit board materials in Thailand over the next five years. The investment is aimed at meeting growing demand from AI servers and ICT infrastructure, reinforcing Panasonic’s position in premium low-loss laminate materials.

- June 2025: Ventec International Group entered into a fulfillment and supply agreement with Matrix and simultaneously launched a new business unit, Ventec Americas. This development is intended to strengthen fulfillment, conversion, and supply capabilities for PCB base materials across North America, improving customer access to laminate and prepreg materials in the region.

- February 2025: Rogers Corporation launched RO4830 Plus laminates for 76–81 GHz automotive radar sensor applications. The product is designed to deliver stable dielectric performance and low insertion loss for millimeter-wave radar systems, thereby strengthening Rogers’ portfolio in high-frequency laminate materials used in advanced automotive electronics and ADAS platforms.

- February 2025: Resonac developed low thermal expansion copper clad laminates for next-generation semiconductor packages. The new material is designed to suppress package warpage as semiconductor packages increase in size and complexity, thereby enhancing suitability for advanced packaging applications that require tighter dimensional stability and improved reliability.

- December 2024: Shengyi Technology (Thailand) Co., Ltd. held the groundbreaking ceremony for its new facility in Chachoengsao Province, Thailand, marking a key milestone in the company’s global expansion strategy. The project represents Shengyi’s first major international manufacturing step in Southeast Asia and is expected to strengthen its regional presence in copper clad laminates and related electronic materials.

REPORT COVERAGE

The global copper clad laminates market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, End Use, and Region |

| By Product Type |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 20.50 billion in 2025 and is projected to reach USD 32.95 billion by 2034.

In 2025, the market value stood at USD 17.84 billion.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period.

By end use, the consumer electronics segment led in 2025.

Growth in electric vehicles and rising demand for consumer electronics are the key factors driving market growth.

Kingboard Laminates, Shengyi Technology, Nan Ya Plastics, Elite Material Co. (EMC), AGC Inc., and Doosan Electro-Materials are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

The trend toward miniaturization and the increasing use of high-frequency materials are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us