Copper Scrap Market Size, Share & Industry Analysis, By Source (New Scrap and Old Scrap), By Grade (No.1 Copper, No.2 Copper, Bare Bright Copper, Insulated Copper Wire, and Shredded & Mixed Copper Scrap), By End Use (Building & Construction, Electricity & Telecommunication, Electronics & Appliances, Automotive & Transportation, Industrial Machinery, Renewable Energy, and Others), and Regional Forecast, 2026-2034

Copper Scrap Market Size and Future Outlook

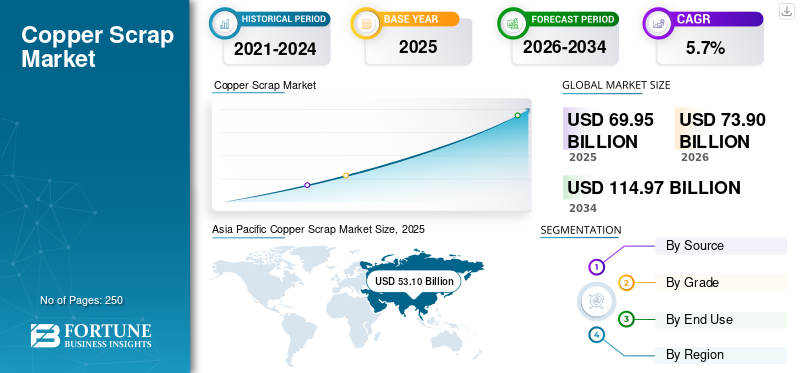

The global copper scrap market size was valued at USD 69.95 billion in 2025. The market is projected to grow from USD 73.90 billion in 2026 to USD 114.97 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the copper scrap market with a market share of 75.91% in 2025.

Copper scrap refers to recycled copper materials generated from manufacturing offcuts (new scrap) and end-of-life products (old scrap) such as electrical wires, cables, electronics, appliances, vehicles, and building materials. Through collection, sorting, dismantling, shredding, and refining, scrap is converted into usable secondary copper units that can be re-melted and reused across industries. Copper scrap is valued for its high recyclability and conductivity, making it a critical raw material for electricity & telecommunication networks, electronics, building & construction, automotive systems, and renewable energy infrastructure. Demand for copper scrap is primarily driven by rising electrification, expansion of power grid and charging infrastructure, increasing penetration of EVs, and growing copper-intensive renewable deployments, alongside sustainability goals that favor recycled inputs to reduce carbon footprint.

The market is led by large scrap recyclers, metal traders, and integrated copper producers that maintain strong positions through extensive sourcing networks, advanced processing, and sorting capabilities. Major players such as Aurubis, Sims Limited, European Metal Recycling (EMR), OmniSource, Nucor, Glencore, and Hindalco strengthen competitiveness through scale, regional yard networks, logistics control, and investments in processing efficiency to improve recovery and grade quality.

Download Free sample to learn more about this report.

Copper Scrap Market Key Takeaways

- 2025 Market Size: USD 69.95 Billion

- 2026 Market Size: USD 73.90 Billion

- 2034 Forecast Market Size: USD 114.97 Billion

- CAGR: 5.7% from 2026–2034

- Asia Pacific dominated the copper scrap market with a 75.91% share in 2025.

- The building & construction segment accounted for the largest market share in 2025.

- The shredded & mixed copper scrap segment is projected to register the fastest growth during the forecast period.

Asia Pacific

Asia Pacific generated USD 53.10 billion in 2025 and is projected to reach USD 53.22 billion in 2026.

North America

North America accounted for USD 4.92 billion in 2025 and is expected to reach USD 5.18 billion in 2026.

Europe

Europe reached USD 9.64 billion in 2025 and is projected to grow at a 4.6% CAGR.

U.S.

The copper scrap market is projected to reach USD 4.68 billion in 2026.

Japan

Growing investments in electronics manufacturing, electrification, and sustainable metal recycling continue to support copper scrap market growth.

Read More

COPPER SCRAP MARKET TRENDS

Rising Shift Toward Low-Carbon Copper Sourcing to Favor Product Adoption

A key market trend is the growing preference for low-carbon copper, which is driving buyers toward recycled inputs. OEMs, utilities, and electronics manufacturers increasingly seek recycled copper to reduce Scope 3 emissions and strengthen ESG positioning. This is encouraging recyclers to improve material traceability, increase recovery yields, and offer a consistent quality supply. As more end users introduce recycled-content goals, scrap is becoming a strategic procurement lever rather than only a cost-based purchase. Similarly, refiners and integrated producers are investing in complex recycling capabilities to process lower-grade and mixed materials into usable copper units. This shift is strengthening demand for organized scrap sourcing and high-efficiency processing.

- The U.S. is boosting copper recycling through federal investments, such as the Department of Energy’s (DOE) USD 270 million for advanced, sustainable recycling infrastructure. By designating copper as a critical mineral, the U.S. aims to reduce a 30% supply gap by leveraging the Inflation Reduction Act incentives for improved sorting and refining technology.

MARKET DYNAMICS

MARKET DRIVERS

Accelerating Electrification and Grid Expansion to Drive Copper Scrap Demand

Copper scrap demand is rising as electrification expands across power generation, transmission, and end-use consumption. Grid upgrades, renewable integration, and rollout of charging infrastructure are increasing copper intensity in cables, transformers, switchgear, and related electrical systems. This creates steady pull for secondary copper units as recyclers and refiners can supply copper with lower embedded emissions than primary copper production. In addition, many downstream buyers are improving recycled-content sourcing to meet sustainability targets and strengthen supply security amid tight copper markets. As power and telecom networks expand in both developed and emerging economies, scrap flows from replacement cycles will also increase. The aforementioned facts are set to reinforce the role of recycled copper in meeting incremental demand, driving the global copper scrap market growth during the forecast period.

Moreover, the transition toward EVs and renewables is structurally increasing copper demand, raising the need for recycled copper as a cost- and carbon-efficient input. EVs use more copper than conventional vehicles in wiring harnesses, motors, inverters, and charging systems. Also, EVs require four to five times more copper than internal combustion engine vehicles, totaling roughly 83 kg per battery electric car. In the EV sector, the demand is driven by the intensive use of copper in motors, batteries, wiring harnesses, and charging infrastructure.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Price Volatility and Trade Frictions May Hamper Market Growth

Copper scrap pricing is closely linked to refined copper prices and regional supply-demand balances, creating volatility for both recyclers and buyers. Sudden changes in copper prices can impact scrap collection volumes, trading activity, and procurement decisions. In addition, trade restrictions, inspection requirements, and shifting rules on scrap exports/imports can disrupt international flows and tighten local availability. This is particularly relevant for mixed and lower-grade scrap that relies on cross-border processing routes. These factors increase working capital pressure, complicate contract pricing, and amplify margin risk for key players. As a result, while demand is structurally strong, short-term predictability remains constrained by price and policy swings.

MARKET OPPORTUNITIES

Growing Renewable Energy and High-Copper Infrastructure to Offer Lucrative Market Opportunities

Renewable energy expansion is creating one of the fastest-growing demand pockets for copper scrap. Solar and wind projects require extensive cabling and power electronics, while grid reinforcement needs higher copper usage in transformers and transmission equipment. As these deployments scale, demand for reliable recycled copper inputs rises to support stable manufacturing and reduce embedded emissions. In parallel, electrification initiatives in transport, buildings, and industrial systems are raising copper intensity across economies. This creates strong long-term demand visibility for scrap processors and traders. Players that secure feedstock networks and align quality with downstream requirements are positioned to benefit most from the structural shift.

Segmentation Analysis

By Source

New Scrap Dominates Due to Higher Purity and Strong Industrial Generation

Based on the source, the market is segmented into new scrap and old scrap.

New scrap dominated the market share as it is generated directly from manufacturing processes such as wire and cable production, metal fabrication, and industrial machining, making it cleaner and easier to process. Its higher purity and lower contamination levels improve recovery efficiency and reduce refining complexity, which is preferred by downstream buyers seeking consistent quality units. The segment is projected to grow rapidly due to expanding manufacturing output in copper-intensive industries and rising demand for high-quality recycled copper.

Old scrap is projected to grow at a CAGR of 5.0%, supported by gradual growth in end-of-life recovery from buildings, vehicles, and appliances. However, collection efficiency and quality variability remain constraints. Demand for scrap will be driven by the need to supplement primary mining shortfalls to support the global energy transition. The demand is driven by the need for sustainable, recycled materials in EVs, renewable energy infrastructure, and construction, all of which require high-purity copper.

By Grade

No.2 Copper Dominates Due to Broad Availability and Strong Downstream Acceptance

Based on grade, the market is segmented into No. 1 copper, No. 2 copper, bare bright copper, insulated copper wire, shredded & mixed copper scrap, and others.

No. 2 copper holds the largest market share as it is widely available across demolition, industrial replacement, and dismantling streams while still meeting common downstream processing needs. It offers a practical balance between volume availability and usable copper content, supporting strong adoption by recyclers, traders, and secondary refiners. The segment’s further growth is supported by steady recovery from construction, industrial equipment replacement, and broad scrap generation.

Shredded & mixed copper scrap is expected to grow at the fastest CAGR of 6.4%, driven by higher shredding activity, greater recovery from mixed streams, and investments in sorting/upgrading technologies that expand usable supply. Shredding copper scrap increases its value by 15–30% as it creates uniform, high-purity, and meltable material that is easy to transport. It also improves the efficiency of downstream machinery, such as granulators and separators.

By End Use

Building & Construction Dominates Due to High Copper Use in Wiring and Infrastructure

Based on end use, the market is segmented into building & construction, electricity & telecommunication, electronics & appliances, automotive & transportation, industrial machinery, renewable energy, and others.

To know how our report can help streamline your business, Speak to Analyst

The building & construction segment accounted for the largest global copper scrap market share in 2025. The massive demand is mainly due to strong copper usage in electrical wiring, plumbing systems, HVAC equipment, and ongoing repair and replacement activity. Demolition, renovation, and infrastructure upgrades generate consistent scrap flows, while new construction demand supports downstream consumption of recycled copper units.

Electricity & telecommunication represents another major application, where copper scrap is utilized in power cables, transformers, grid expansions, and telecom networks, and demand remains high due to copper’s superior conductivity and recyclability without performance loss. Ongoing grid modernization, renewable power integration, and fiber-optic network expansion are accelerating recovery and reuse of copper components. The segment is projected to grow at a CAGR of 5.5% over the forecast period, reflecting sustained investments in electrification and communication infrastructure.

Automotive & transportation is expected to grow at a CAGR of 6.6% during, reflecting massive EV adoption and greater focus on sustainable material cycles within the transportation sector. Increasing copper intensity in EVs, charging infrastructure, rail systems, and lightweight mobility platforms is raising both primary demand and end-of-life scrap recovery. Vehicle electrification, in particular, significantly boosts copper usage in motors, inverters, and battery systems, creating future recyclable streams.

Copper Scrap Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Copper Scrap Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market in 2025, reaching USD 53.10 billion, and is projected to reach USD 53.22 billion in 2026. The region’s leadership is supported by its massive base of electronics manufacturing, wire & cable production, construction activity, and fast-growing renewable deployments. The region also benefits from strong downstream smelting and refining capacity that supports large-scale absorption of recycled copper units. Rising electrification, expanding grid infrastructure, and continued industrial growth reinforce long-term demand for secondary copper units.

China Copper Scrap Market

China market is expected to reach USD 35.34 billion in 2026, accounting for approximately 48% of global revenues. Demand is supported by China’s dominant wire & cable manufacturing base, large electronics and appliance production ecosystem, and extensive construction and infrastructure activity. Rapid growth in EV supply chains and renewable installations further increases copper intensity, strengthening demand for recycled copper units.

India Copper Scrap Market

The India market will reach USD 6.43 billion in 2026, representing roughly 9% of global revenues. This growth is driven by rapid electrification, expansion of power distribution networks, strong growth in building construction, and rising copper consumption in industrial machinery and consumer electrical products. Surge in renewable energy and steady expansion of domestic manufacturing are also supporting higher uptake of secondary copper units.

North America

North America reached USD 4.92 billion in 2025 and is projected to increase to USD 5.18 billion in 2026. Demand is supported by replacement-driven scrap generation, strong domestic recycling networks, and steady consumption from construction, industrial maintenance, and electrical applications. Increasing investment in grid modernization and electrification supports demand for recycled copper.

U.S. Copper Scrap Market

The U.S. market will be valued at USD 4.68 billion in 2026, accounting for approximately 6% of global revenues. Demand is supported by steady construction and renovation activity, replacement-driven scrap generation, and consistent consumption from power infrastructure, telecom upgrades, and industrial maintenance.

Europe

Europe is projected to grow at 4.6% over the coming years, and reached a valuation of USD 9.64 billion in 2025. The region is shaped by mature recycling systems, a strong regulatory focus on the circular economy, and steady demand from electrical infrastructure, industrial manufacturing, and building refurbishment cycles. Europe is more specification-led, with greater emphasis on traceability and quality consistency, which supports demand for processed grades.

Germany Copper Scrap Market

The Germany market will reach USD 2.35 billion in 2026, equivalent to around 3% of global revenues. Demand is supported by Germany’s strong industrial manufacturing base, electrical equipment production, and high standards for material recovery and recycling efficiency. Building refurbishment, machinery production, and transport-linked demand support stable consumption of processed copper scrap grades.

U.K. Copper Scrap Market

The U.K. market will record USD 1.44 billion in 2026, accounting for approximately 2% of global revenues. Demand is supported by ongoing infrastructure upgrades, building renovation cycles, and replacement of legacy telecom and power assets that generate recoverable copper. The growing emphasis on circularity and recycling standards also supports structured scrap collection and processing activities.

Rest of the World

Rest of the World reached USD 2.28 billion in 2025 and is projected to rise to USD 2.41 billion in 2026. Demand is supported by urbanization-led construction growth, gradual expansion of manufacturing, and rising electrification investments in select markets. Import dependence and developing processing capacity influence market structure, but long-term growth remains supported by infrastructure expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Circular Capacity Expansion and Secured Feedstock Strategies to Shape the Market Dynamics

The copper scrap market is led by large-scale recyclers and integrated metals players such as Aurubis, Sims Limited, European Metal Recycling (EMR), OmniSource, Nucor, Glencore, and Hindalco, supported by strong sourcing networks, processing infrastructure, and established downstream relationships with smelters, refiners, and industrial buyers. Players are increasingly competing on feedstock security, complex-scrap processing capability, recovery efficiency, and the ability to supply consistent grades across price cycles. Recent market developments show a clear strategic direction, including capacity expansions to handle complex recycling materials and multi-year supply tie-ups to lock in scrap flows. In parallel, recycling scale-up roadmaps and capital deployment for R&D-led recycling infrastructure are strengthening technology depth. As demand for low-carbon copper rises, competitive advantage will shift toward players that can secure long-duration scrap supply, efficiently upgrade mixed streams, and meet stricter quality standards over the forecast period.

LIST OF KEY COPPER SCRAP COMPANIES PROFILED

- Aurubis AG (Germany)

- Sims Limited (Australia)

- Commercial Metals Company (U.S.)

- European Metal Recycling (EMR) (U.K.)

- OmniSource Corporation (U.S.)

- Nucor Corporation (U.S.)

- Glencore (Switzerland)

- Hindalco (India)

- Jain Resource Recycling Pvt Ltd. (India)

- Okon Recycling (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Gravita India has completed the acquisition of Rashtriya Metals Industries Limited (RMIL) for USD 2.15 million, marking a major step in scaling up its copper recycling operations. In addition, the company has commissioned a lithium-ion battery recycling facility in Mundra.

- December 2025: Attero has unveiled plans to invest USD 16.5 million to scale up its recycling operations and strengthen its R&D capabilities across India, with a focus on e-waste, copper, and lithium-ion battery This investment will increase annual processing capacity by nearly 1 lakh tonnes through the establishment of five new facilities.

- August 2025: Aurubis highlighted ongoing ramp-up and commissioning timelines for its recycling growth projects, including Aurubis Richmond, which is planned to process large volumes of complex recycling materials annually once fully ramped.

- April 2025: Hindalco Industries has outlined a diversified growth roadmap centered on sustainability, enhanced recycling capabilities, and strategic capital deployment. During its Investor Day 2025, the company announced its target to expand recycling capacity fourfold by FY30, while strengthening aluminium’s positioning as a circular material with up to 75% recycled content.

- March 2024: BT signed a recycling deal with European Metal Recycling (EMR) to sell copper recovered from surplus copper cables removed during the UK’s transition to full-fibre infrastructure. The agreement supports copper extraction and recycling through 2028.

REPORT COVERAGE

The global copper scrap market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.7% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Source, By Grade, End Use, and Region |

| By Source |

|

| By Grade |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 69.95 billion in 2025 and is projected to reach USD 114.97 billion by 2034.

In 2025, the market value stood at USD 53.10 billion.

Recording a CAGR of 5.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The building & construction end use segment led in 2025.

Accelerating electrification and grid expansion is expected to drive market growth.

Aurubis, Sims Limited, European Metal Recycling (EMR), OmniSource, Nucor, Glencore, and Hindalco are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Rising shift toward low-carbon copper sourcing to favor product adoption

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us