Counter-Drone Radar Market Size, Share & Industry Analysis, By Radar Type (2D Radar, 3D Radar, and 4D Radar), By Radar Technology (AESA Radar, PESA Radar, Mechanically Scanned Radar, and Hybrid Scanned Radar), By Frequency Band (S-Band, C-Band, X-Band, Ku-Band, and K-Band), By Range (Short Range (Up to 5 km), Medium Range (5–15 km), and Long Range (Above 15 km)), By Deployment Mode (Fixed-Site Radar, Tripod / Portable Radar, Vehicle-Mounted Radar, and Naval / Shipborne Radar), By End User (Army, Air Force, Navy, and Special Operations Forces), and Regional Forecast, 2026-2034

Counter-Drone Radar Market Size and Future Outlook

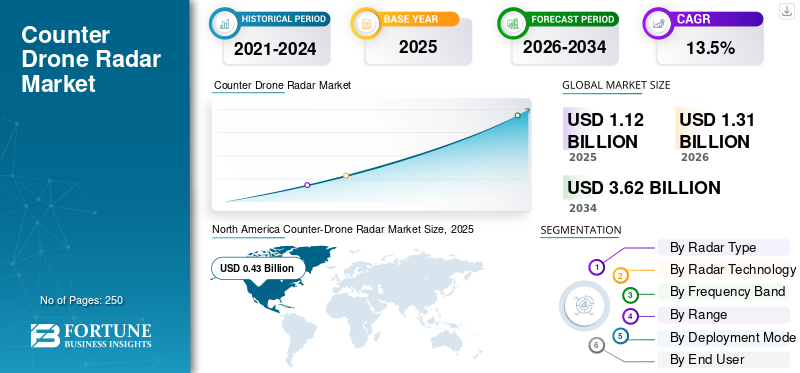

The global counter-drone radar market size was valued at USD 1.12 billion in 2025. The market is projected to grow from USD 1.31 billion in 2026 to USD 3.62 billion by 2034, exhibiting a CAGR of 13.5% during the forecast period. North America dominated the counter-drone radar market with a market share of 48.16% in 2025.

Counter-drone radar technology serves as a critical defense layer, utilizing high-resolution detection and sophisticated signal processing to mitigate the risks posed by unmanned aerial systems (UAS). The global market for these technologies is rapidly expanding, driven by the increasing proliferation of commercial and military drones, the rise of autonomous and dark flight capabilities, and the urgent strategic requirement to secure critical infrastructure and battlefield airspace against low-observable threats.

Leading industry players such as HENSOLDT, Leonardo S.p.A., and Saab AB are advancing innovations that ensure robust airspace awareness. These efforts include the implementation of 3D AESA (Active Electronically Scanned Array) radar architectures and micro-doppler signal processing to distinguish drones from birds, low-probability-of-intercept (LPI) designs, and multi-sensor fusion platforms that integrate radar with electro-optical/infrared (EO/IR) systems for precise target classification and rapid threat neutralization.

Download Free sample to learn more about this report.

Counter Drone Radar Market Key Takeaways

- 2025 Market Size: USD 1.12 billion

- 2026 Market Size: USD 1.31 billion

- 2034 Forecast Market Size: USD 3.62 billion

- CAGR: 13.5% from 2026–2034

- North America dominated the market with a 48.16% share in 2025.

- The 3D radar segment is expected to lead the market during the forecast period.

- The AESA radar segment dominated the market in 2025.

North America

North America reached USD 0.43 billion in 2025 and is projected to grow to USD 0.50 billion in 2026.

Europe

Europe is projected to register the fastest CAGR of 15.3% during 2026–2034.

Asia Pacific

Asia Pacific is expected to witness strong growth, driven by military modernization and border security investments.

U.S.

The market reached USD 0.39 billion in 2025, supported by strong defense procurement and C-UAS programs.

Japan

The market reached USD 0.03 billion in 2025, driven by increasing investments in defense modernization.

Read More

COUNTER-DRONE RADAR MARKET TRENDS

Integration of AI into Radar Systems is an Emerging Market Trend

The rapid advancement and integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is a transformative catalyst for the market. As drone technology evolves toward increased autonomy and low-observability, traditional signal processing methods are increasingly insufficient to maintain airspace integrity. The adoption of AI-enabled radar serves as a critical driver for market growth by addressing the following technical and operational imperatives.

- For instance, in April 2026, OptiValue Tek received a multi-million dollar GeM contract from the government for its AI-powered Integrated Counter-UAV Defence System (ICUDS), bolstering India's defense against aerial threats.

Conventional radar systems often struggle to differentiate between small unmanned aerial systems (UAS) and environmental noise such as avian flight patterns or moving vegetation. AI algorithms are integrated in these systems for high-fidelity micro-doppler signature analysis to effectively filter out non-threatening clutter, thereby reducing the noise which drives the product demand.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Military Drone Threats and Layered Air-Defense Modernization to Propel Market Growth

The market is being driven by the rapid battlefield and base-security threat created by small UAVs, loitering munitions, and low-cost attack drones. Modern drones are no longer only surveillance assets. They are increasingly used for precision strikes, artillery correction, swarm-style saturation, and attacks on fixed military infrastructure. This is forcing armed forces to invest in radar systems that can detect low-flying, slow-moving, low-radar-cross-section targets earlier and more reliably than legacy air-surveillance sensors.

- For instance, in April 2026, the U.S. military deployed Ukraine's Sky Map command-and-control platform at Prince Sultan Air Base in Saudi Arabia to counter Iranian drone attacks that damaged aircraft and killed personnel. They integrate radars with Ukraine's Sky Map platform, which fuses data from radars, over 10,000 acoustic sensors, optical systems, and cameras to create a real-time threat map for detecting low-flying Iranian Shahed drones.

Therefore, the radar is becoming a priority detection layer as it provides persistent surveillance, target tracking, and cueing support for EO/IR cameras, electronic warfare, guns, missiles, and interceptor drones. Rising threats from drones drive the adoption of laser systems and radars for precise detection and tracking for public safety and national security. There is also an increase in the demand for strong for 3D and 4D AESA radars, vehicle-mounted radars, medium-range systems, and mobile SHORAD-linked sensors, which drives the counter-drone radar market growth during the forecast period.

MARKET RESTRAINTS

Technical Detection Limitations May Limit Market Expansion

A key restraint for the market is the technical difficulty of reliably detecting, tracking, and classifying small drones in complex operating environments. Small UAVs often fly low and slow, carry limited radar signatures, and may appear similar to birds or other small airborne objects on radar screens. In battlefield, border, urban, and base-defense environments, ground clutter, terrain masking, electromagnetic interference, weather effects, and dense object movement can reduce detection confidence. The U.S. GAO notes that some counter unmanned aerial system technologies have limited ability to detect and track small UAS, while electromagnetic interference and birds can reduce detection performance or generate false detections.

MARKET OPPORTUNITIES

Networked, Mobile C-UAS Architectures Presents Growth Opportunities

The market is expected to witness strong opportunities from the military shift toward networked and mobile counter-UAS architectures. Armed forces are increasingly moving beyond standalone radar deployment and prioritizing sensor systems that can operate within a wider defense network. This creates demand for radars capable of supporting real time detection, tracking, classification, and target handoff across multiple defensive layers. The opportunity is particularly strong for radar solutions that can be integrated with command-and-control platforms, electro-optical systems, electronic warfare assets, and kinetic or non-kinetic effectors.

For instance, in April 2026, Echodyne's EchoShield radars have been selected as the primary sensors for Trust Automation's rapidly deployable RD-SUADS, under a USD 490 million USAF IDIQ contract. The system, equipped with up to four EchoShield units, detects, classifies, and tracks drones at 3-4.5 km ranges in both mobile and fixed configurations. The market opportunity is further supported by the need for persistent surveillance around airbases, forward operating areas, naval assets, and strategic military infrastructure.

MARKET CHALLENGES

Interoperability Gaps and Rapid Threat Evolution to Create Market Challenges

A major challenge for the market is that radar systems must operate as part of a larger, fast-changing C-UAS architecture rather than as standalone sensors. Military users need radars to connect seamlessly with EO/IR cameras, RF sensors, jammers, command-and-control systems, guns, missiles, directed-energy systems, and interceptor drones. In practice, this is difficult as many armed forces use mixed legacy systems, different data standards, and vendor-specific interfaces.

Segmentation Analysis

By Radar Type

Need for Altitude-Range-Azimuth Precision for Low-Flying Drone Detection to Propel 3D Radar Segment Growth

Based on radar type, the market is divided into 2D radar, 3D radar, and 4D radar.

The 3D radar segment is expected to hold a leading share of the market as military users require altitude, range, and azimuth data for reliable drone tracking and engagement support. Unlike 2D radar, 3D radar provides a more complete air picture, making it better suited for detecting low-flying UAVs, quadcopters, and loitering threats operating near bases, borders, and forward positions. The product demand is supported by the increasing need to cue electro-optical sensors, electronic warfare systems, guns, missiles, and interceptor drones with higher positional accuracy.

- For instance, in July 2025, HENSOLDT received an order worth more than EUR 340 million (USD 394.6 million) to supply TRML-4D high-performance radars and SPEXER 2000 3D MkIII short-range radars to strengthen Ukraine’s air-defense architecture.

The 4D radar segment is anticipated to rise at the fastest CAGR of 14.7% over the forecast period.

By Radar Technology

High-Speed Beam Steering and Multi-Target Tracking Needs to Propel AESA Radar Segment Growth

By radar technology, the market is segmented into AESA radar, PESA radar, mechanically scanned radar, and hybrid scanned radar.

The AESA radar segment dominated the market in 2025 and is projected to witness strong growth as military counter-drone operations increasingly require faster beam steering, multi-target tracking, and high update-rate surveillance. AESA systems are well suited for detecting small, low-radar-cross-section drones in cluttered environments while supporting simultaneous search, track, and cueing functions. The product demand is being driven by the shift toward mobile SHORAD, base defense, convoy protection, and integrated counter-UAS systems where rapid reaction time is critical.

- For instance, in October 2024, Leonardo DRS introduced a counter-drone directed-energy Stryker demonstrator using RADA RPS92 next-generation Multi-Mission Hemispheric AESA radars for 360-degree surveillance and target tracking.

The hybrid scanned radar segment is estimated to register the fastest CAGR of 12.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Frequency Band

Suitability for Small Aerial Target Detection to Support X-Band Segmental Dominance

By frequency band, the market is segmented into S-Band, C-Band, X-Band, Ku-Band, and K-Band.

The X-band segment is expected to account for a major counter-drone radar market share due to its strong suitability for detecting small aerial targets with improved resolution. X-band radars are widely used in tactical surveillance, short-range air defense, and C-UAS applications where accurate tracking of low-altitude drones is required. As armed forces prioritize small-drone detection and effector cueing, X-band radar systems are expected to remain central to military counter-drone architectures.

- For instance, in November 2025, Poland selected Saab’s A26 submarine design for its Orka program, with the platform promoted for very low acoustic and magnetic signatures and Saab’s Baltic Sea stealth experience.

The Ku-Band segment is projected to show a steady CAGR of 13.7% over the forecast period.

By Range

Rising Demand for Airbase Protection to Support Medium Range Segmental Dominance

By range, the market is segmented into short range (up to 5 km), medium range (5–15 km), and long range (above 15 km).

The medium range segment is expected to hold major share in the market as it represents the most operationally balanced range class for military counter-drone radar deployment. The segment growth is driven by the need to protect airbases, forward operating locations, ammunition depots, command sites, and maneuver forces from drones approaching at low altitude. This range category is expected to remain highly attractive as militaries seek deployable systems that balance coverage, cost, and operational flexibility.

The long range (above 15 km) segment is estimated to register a steady CAGR of 12.7% over the forecast period.

By Deployment Mode

Escalating Radar Systems Demand to Propel Vehicle-Mounted Radar Segment Growth

On basis of deployment mode, the market is segmented into fixed-site radar, tripod / portable radar, vehicle-mounted radar, and naval / shipborne radar.

The vehicle-mounted radar segment is projected to record major market share as military counter-drone requirements shift from static site protection toward mobile force protection and maneuver warfare. Vehicle-mounted systems allow armed forces to protect convoys, mobile air-defense units, forward operating areas, and rapidly changing battlefield positions. The product demand is supported by the growing need for radar systems that can be redeployed quickly. As counter-UAS operations become more expeditionary and tactical, vehicle-mounted radar is expected to gain a larger role in military procurement.

The naval / shipborne radar segment is projected to grow at a steady CAGR of 12.7% over the forecast period.

By End User

Battlefield Drone Proliferation and Land-Force Protection Priorities to Propel Segment Growth

On basis of end user, the market is segmented into army, air force, navy, and special operations forces.

The army segment is expected to dominate the market as land forces face the highest exposure to small UAVs, loitering munitions, and battlefield reconnaissance drones. Armies require radar systems for base protection, forward operating areas, convoy security, artillery and air-defense site protection, and mobile maneuver-force defense. The segment growth is driven by the need to detect drones before they can conduct surveillance, target acquisition, precision strikes, or swarm-style disruption

The navy segment is expected to register the fastest CAGR of 15.9% over the forecast period.

Counter-Drone Radar Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Counter-Drone Radar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025 with a valuation of USD 0.43 billion and is estimated to reach USD 0.50 billion in 2026. The region experiences strong growth due to large U.S. defense procurement base, mature counter-small UAS programs, advanced radar suppliers, and continued increasing investments in layered air-defense architectures. The market growth in the region is driven by the need to protect military bases, forward-deployed forces, air-defense sites, strategic installations, and mobile maneuver units from small UAVs, loitering munitions, and drone-swarm threats. Moreover, there is strong adoption of counter radar systems to address critical gaps in short-range air defense during rising massed, low-altitude threats in naval and coastal operations, which is driving North America anti drone market which further helps the global market growth during the forecast period.

- For instance, in April 2026, Elbit Systems (U.S.) demonstrated its Iron Shield counter-drone system to U.S. Marines, designed to protect littoral zones, ports, and ships from swarm attacks and low-flying threats. The package integrates X-band AESA radar with layered interceptors for real-time detection, tracking, and neutralization of drones and cruise missile-like targets.

U.S. Counter-Drone Radar Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market reached a value of around USD 0.39 billion in 2025. The U.S. is expected to remain the largest country-level market due to its established C-UAS procurement structure, active Army-led programs, large overseas deployment footprint, and strong domestic radar manufacturing ecosystem. The market growth is supported by requirements for force protection, airbase defense, critical installation security, mobile SHORAD integration, and protection of forward operating locations.

Europe

The Europe market is projected to record the fastest CAGR of 15.3% during 2026 to 2034. The regional market growth is due to Russia-Ukraine war, recurring drone incursions, eastern-flank reinforcement, and the urgent requirement to protect airbases, depots, ammunition sites, borders, mobile forces, and command infrastructure. The regional growth is supported by NATO’s increasing focus on integrated counter-drone systems, interoperability testing, and rapid fielding of technologies capable of detecting and tracking low-altitude drone threats. European countries are also investing in modular and mobile radar solutions that can support both fixed-site protection and tactical battlefield deployment.

- For instance, in September 2025, NATO launched Eastern Sentry after Russian drone violations of Polish airspace, with the initiative including traditional capabilities and newer technologies designed to address drone-related challenges along the eastern flank.

U.K. Counter-Drone Radar Market

The U.K. market reached a value of around USD 0.07 billion in 2025, representing roughly 6.5% of the global revenues.

Germany Counter-Drone Radar Market

The Germany market reached approximately USD 0.08 billion in 2025, equivalent to around 7.2% of global sales.

Asia Pacific

The Asia Pacific market is projected to witness strong growth owing to expanding military modernization, border tensions, island-defense requirements, naval-base protection, and airbase security needs across China, India, Japan, South Korea, Australia, and other Indo-Pacific markets. The regional market growth is supported by the rising need for radar systems capable of monitoring low-altitude airspace around forward bases, military installations, coastal areas, and mobile defense formations. China and India account for the largest regional demand base due to scale, defense-industrial depth, and military modernization.

- For instance, in August 2025, the Australian Government accelerated the acquisition of counter-drone capabilities for the Australian Defence Force as part of a long-term investment plan to protect personnel and military assets. This supports the regional demand outlook for radar-supported counter-drone architectures.

Japan Counter-Drone Radar Market

The Japan market reached a value of around USD 0.03 billion in 2025, accounting for roughly 2.5% of global revenues.

China Counter-Drone Radar Market

The China market is projected to be one of the largest markets worldwide. The 2025 revenues of the country market hit around USD 0.07 billion representing roughly 6.0% of global sales.

India Counter-Drone Radar Market

The India market touched a value of around USD 0.05 billion in 2025, accounting for roughly 4.2% of the global revenues.

Latin America and Middle East & Africa

The region represents a smaller but strategically relevant market. The regional product adoption remains selective and is mainly linked to military base protection, border surveillance, anti-smuggling operations, strategic-site defense, and border security modernization. Brazil is the largest country-level market due to its broader defense scale, military aviation base, and security modernization requirements, while Mexico and the rest of Latin America are expected to develop gradually from a smaller installed base.

The growth in the Middle East & Africa is driven primarily by the Middle East, where Saudi Arabia, UAE, Israel, Qatar, and other Gulf markets are increasing investment in base defense, air-defense modernization, border protection, and strategic military-site security. The region has a strong requirement for radar systems capable of detecting drones and loitering threats around airbases, energy-linked strategic sites, command facilities, and deployed military formations.

Saudi Arabia Counter-Drone Radar Market

The Saudi Arabia market reached a value of around USD 0.01 billion in 2025, accounting for roughly 0.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Partner with Defense Agencies and Militaries to Maintain Dominant Positions

The global counter-drone radar market is defined by collaborations among militaries, defense agencies, C-UAS integrators, major radar manufacturers, and sensor-fusion specialists delivering advanced low-RCS detection radars, multi-beam AESA arrays, cognitive Doppler processing, and AI-driven threat-classification platforms for diverse operational environments. The market leadership is increasingly shaped by players that can support modular and scalable radar coverage, seamless integration with existing C4ISR and effector-management systems, fleet-wide hardening against low-signature drone swarms, and agile technology insertion across forward bases, mobile platforms, naval vessels, and next-generation layered air-defense architectures.

LIST OF KEY COUNTER-DRONE RADAR COMPANIES PROFILED

- HENSOLDT AG (Germany)

- Leonardo S.p.A. (Italy)

- Israel Aerospace Industries (Israel)

- Saab AB (Sweden)

- Lockheed Martin Corporation (U.S.)

- Thales S.A. (France)

- Echodyne Corp. (U.S.)

- Robin Radar Systems B.V. (Netherlands)

- Blighter Surveillance Systems Limited (U.K.)

- Weibel Scientific A/S (Denmark)

- Fortem Technologies Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Echodyne was selected as the primary radar provider for Trust Automation’s Small-Unmanned Air Defense Systems platform, with EchoShield radar integrated into a U.S. Air Force counter-UAS program under a USD 490 million IDIQ contract.

- December 2025: HENSOLDT and Rheinmetall signed a long-term framework agreement for SPEXER 2000 radars. The deal covers large-quantity deliveries for ground-based air-defense applications, including drone-defense solutions and Skyranger 30.

- October 2025: Saab received a USD 46 million U.S. Army order for Giraffe 1X radars, with deliveries scheduled from 2026 to support air-defense and counter-UAS capabilities for security cooperation partners.

- October 2025: Israel Aerospace Industries introduced a next-generation multi-layered C-UAS solution at AUSA 2025. The new solution incorporates radar and electro-optical sensors with AI-enabled command-and-control and modular interceptors for drone-swarm defense.

- March 2025: MatrixSpace launched its Portable 360 Radar for rapid counter-drone operations. It offers a rugged AI-enabled radar kit for panoramic close-airspace awareness in mobile and temporary deployment environments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Radar Type, By Radar Technology, By Frequency Band, By Range, By Deployment Mode, By End User, and Region |

| By Radar Type |

|

| By Radar Technology |

|

| By Frequency Band |

|

| By Range |

|

| By Deployment Mode |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.12 billion in 2025 and is projected to reach USD 3.62 billion by 2034.

In 2025, North America’s market value stood at USD 0.43 billion.

The market is expected to exhibit a CAGR of 13.5% during the forecast period of 2025-2034.

By radar technology, the AESA radar segment led the market in 2025.

Rising military drone threats and layered air-defense modernization is a key factor driving market expansion.

HENSOLDT AG (Germany), Leonardo S.p.A. (Italy), Israel Aerospace Industries (Israel), and Saab AB (Sweden) are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us