CV Depot Charging Market Size, Share & Industry Analysis, By Charging Infrastructure Type (AC Charging, DC Fast Charging, and Ultra-fast), By Vehicle Type (Electric Buses, Electric Trucks, and Electric Light Commercial Vehicles (eLCVs)), By Depot Type (Private Fleet Depots, Public Charging Depots, and Municipal/Government Fleet Depots), By Charger Power Output (Below 50 kW, 50–150 kW, 150–350 kW, and Above 350 kW), By End User (Logistics & E-commerce Companies, Public Transport Authorities, Industrial & Utility Fleets, and Third-party Charging Operators), and Regional Forecast, 2026–2034

CV Depot Charging Market Size and Future Outlook

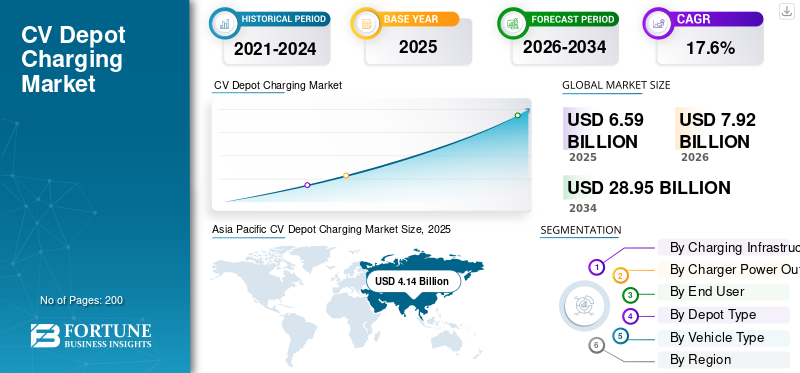

The global CV depot charging market size was valued at USD 6.59 billion in 2025. The market is projected to grow from USD 7.92 billion in 2026 to USD 28.95 billion by 2034, exhibiting a CAGR of 17.6% during the forecast period. Asia Pacific dominated the cv depot charging market with a market share of 62.82% in 2025.

CV depot charging refers to a centralized charging infrastructure installed at fleet depots for electric trucks and buses. It enables efficient and scheduled charging, supporting optimized fleet operations, energy optimization, and reduced downtime. Market growth is driven by increasing fleet electrification, stringent emission regulations, rising fuel costs, advancements in charging infrastructure, government incentives, and growing demand for efficient, scalable, and cost-effective commercial vehicle operations.

Major players in the market include ABB, Siemens, Shell Recharge, BP Pulse, ChargePoint, and Tesla. These players are competing through high-power charging solutions, smart energy management, network expansion, and integrated digital fleet charging platforms.

Download Free sample to learn more about this report.

CV DEPOT CHARGING MARKET TRENDS

Integration of Smart Energy Management Systems Drives Market Growth

The market is witnessing a strong shift toward integrating smart energy management systems within depot charging infrastructure. These systems enable real-time monitoring, load balancing, and optimized energy consumption, helping fleet operators reduce electricity costs and avoid grid overloads. Advanced software platforms are also facilitating predictive maintenance and charging scheduling based on fleet usage patterns. This type of CV depot charging market trends is further supported by increasing digitalization and IoT adoption, allowing operators to maximize asset utilization while ensuring operational efficiency and sustainability in large-scale commercial vehicle charging depots.

- For instance, in January 2026, Hypercharge Networks launched Hypercorp Energy Solutions, integrating battery energy storage systems (BESS) with its Equion platform using smart load controls, site monitoring, demand response integration, and SaaS-based energy management to optimize EV charging efficiency and grid utilization.

Increasing Need for Reduced Vehicle Downtime to Boost Market Expansion

The increasing need for reduced vehicle downtime is driving the adoption of high-power charging solutions for electric vehicles in depot environments. Chargers with higher output capacities enable faster charging of electric trucks and buses, ensuring vehicles are ready for operations within shorter timeframes. This trend is particularly significant for logistics and public transport fleets operating on tight schedules. As battery capacities increase, the demand for ultra-fast charging infrastructure is also rising, prompting manufacturers to develop scalable and high-efficiency charging systems tailored to commercial fleet requirements.

- For instance, in January 2026, XCharge North America partnered with Energy Plus to deploy a 44-unit GridLink battery-integrated depot in Brooklyn. It delivers 9.46 MWh storage, bidirectional energy flow, off-peak load shifting, and supports 88 charging spaces for high-demand urban fleets.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stringent Emission Norms to Augment Market Expansion

Governments across regions are implementing stringent emission norms and carbon reduction targets, compelling fleet operators to transition toward electric commercial vehicles. Policies such as zero-emission mandates, low-emission zones, and carbon taxation are pushing companies to adopt cleaner transportation alternatives. As fleets electrify, the need for dedicated depot charging infrastructure increases significantly. This regulatory push accelerates vehicle adoption and creates a parallel demand for reliable and scalable charging solutions, thereby driving sustained growth in the CV depot charging industry.

- For instance, in 2024, global electric bus sales surpassed 70,000 units, driven primarily by renewed growth in China, while markets outside China grew modestly by 5%, though sales nearly tripled compared to 2020 levels.

Expansion of the E-commerce and Last-mile Delivery Services to Boost Market Demand

The rapid growth of e-commerce and last-mile delivery services is significantly increasing the number of commercial vehicles on the road. Fleet operators are under pressure to enhance operational efficiency while reducing environmental impact, leading to growing adoption of electric vehicles. This directly boosts the demand for depot-based charging infrastructure, where vehicles can be charged overnight or during idle periods. The scalability and centralized nature of depot charging make it an ideal solution for large logistics fleets, thereby supporting strong market expansion.

- For instance, in January 2025, Amazon ordered over 200 Mercedes-Benz eActros 600 electric trucks with 600+ kWh batteries and 500 km range, deploying 360 kW chargers enabling 20–80% charging in ~1 hour to support high-mileage logistics operations.

Growing Public-private Partnerships in Accelerating Infrastructure Development Fuels Market Growth

Various governments are offering subsidies, tax benefits, and funding programs to promote the deployment of electric vehicle charging infrastructure. These incentives reduce the initial capital investment required for setting up depot charging systems, encouraging fleet operators and private investors to adopt such solutions. Public-private partnerships are also playing a crucial role in accelerating infrastructure deployment. As financial barriers decrease, more companies are investing in charging depots, thereby contributing to the overall growth and maturity of the market.

- For instance, in March 2026, Outpost invested in EV Realty to expand shared electric truck depot infrastructure across U.S. freight corridors. This enables immediate access to grid-ready sites while developing high-power charging hubs for scalable fleet electrification and reduced upfront costs.

MARKET RESTRAINTS

High Initial Capital Investment to Hamper Market Expansion

Despite long-term cost benefits, the high upfront investment required for depot charging infrastructure remains a significant barrier. Costs associated with grid upgrades, installation of high-power chargers, and integration of energy management systems can be substantial. Small and medium-sized fleet operators often face financial constraints, limiting their ability to invest in such infrastructure. Additionally, uncertainty around return on investment and evolving charging technology standards further discourages adoption, thereby restraining market growth in certain segments.

MARKET OPPORTUNITIES

Integration of Renewable Energy Sources into Depot Charging Systems Provides Several Growth Opportunities

The integration of renewable energy sources such as solar and wind into depot charging systems presents a significant opportunity for market players. By generating clean energy on-site, operators can reduce dependence on grid electricity and lower operating costs. Energy storage systems further enhance this capability by storing excess energy for later use. This approach improves sustainability and provides long-term cost advantages, making it an attractive proposition for fleet operators seeking efficient and eco-friendly charging solutions.

- For instance, in August 2025, Renewable Properties secured USD 20 million to develop a 4MW EV depot in California, featuring 16 DC fast chargers (50-350 kW) and 48 Level 2 units, supporting medium-duty fleets and grid-integrated charging expansion.

Development of Charging-as-a-Service Models Expands Market Accessibility

The emergence of Charging-as-a-Service (CaaS) models is creating new growth opportunities in the market. These models allow fleet operators to deploy charging infrastructure without significant upfront investment, as service providers handle installation, maintenance, and operations. This reduces financial risks and accelerates adoption, particularly among smaller fleet operators. Additionally, flexible payment structures and subscription-based models make charging solutions more accessible, thereby expanding the potential customer base and driving market growth.

- For instance, in January 2026, L-Charge raised USD 10 million to scale modular off-grid EV charging solutions, offering charging-as-a-service with rapid deployment, bypassing grid constraints and enabling fleet electrification within weeks across logistics and last-mile delivery segments.

MARKET CHALLENGES

Limitations of Existing Grid Infrastructure to Hinder Product Demand

One of the key challenges in the market is the limitation of existing grid infrastructure to support large-scale depot charging. High-power charging systems require substantial electricity supply, which can strain local grids, especially in urban or industrial areas. Upgrading grid infrastructure involves regulatory approvals, time, and additional investment, delaying project implementation. Furthermore, coordination between utilities, charging providers, and fleet operators is often complex, creating bottlenecks in deployment and slowing down overall market growth.

Segmentation Analysis

By Charging Infrastructure Type

Increasing Fleet Electrification Boosts DC Fast Charging Segment Growth

Based on charging infrastructure type, the market is segmented into AC charging, DC fast charging, and ultra-fast.

The DC fast charging segment dominates the market due to its ability to deliver rapid and reliable charging for commercial vehicle fleets operating under tight schedules. Fleet operators prioritize minimizing downtime, making DC fast chargers ideal for depot environments with high vehicle utilization. Their compatibility with medium- and heavy-duty electric vehicles, along with scalability for large depots, ensures widespread adoption. Increasing fleet electrification and operational efficiency requirements further strengthen demand for DC fast charging infrastructure across logistics and public transport sectors.

- For instance, in March 2026, Splitvolt launched V-40 (40 kW) and S-80 (up to 160 kW dual-output) DC fast chargers with OCPP integration, RFID access, and compact modular design. It enables scalable mid-power depot charging for fleets with space and grid constraints.

The ultra-fast segment is projected to grow at a CAGR of 20.3% during the forecast period. Rising demand for minimal charging time, increasing battery capacities, and the need for high-throughput fleet operations are accelerating adoption across large-scale commercial depots and long-haul applications.

By Charger Power Output

Balanced Offering of Charging Speed Boosts 50–150 kW Segment Growth

Based on charger power output, the market is segmented into below 50 kW, 50–150 kW, 150–350 kW, and above 350 kW.

The 50–150 kW segment dominates the market due to its balanced offering of charging speed, infrastructure cost, and grid compatibility. It is widely adopted across depot charging setups for medium-duty commercial vehicles, where overnight or scheduled charging is sufficient. Fleet operators prefer this range as it minimizes capital expenditure while ensuring reliable operations. Its scalability and ease of integration into existing grid systems further support strong adoption across logistics, municipal, and public transport fleet depots globally.

- For instance, in November 2025, Indonesia expanded EV charging infrastructure by 299% to 3,233 charging stations, deploying AC (7–22 kW), DC fast (50–150 kW), and ultra-fast (200–400 kW) systems, supporting large-scale electrification and private sector participation growth.

The above 350 kW segment is projected to grow at a CAGR of 22.7% during the forecast period. Increasing demand for ultra-fast turnaround times, rising battery capacities, and the expansion of long-haul electric fleets are driving the adoption of high-power charging solutions across advanced depot infrastructure.

By End User

Large Fleet Electrification of Bus Fleets to Reduce Urban Emissions Encourage Public Transport Authorities Segment Growth

Based on end user, the market is segmented into logistics & e-commerce companies, public transport authorities, industrial & utility fleets, and third-party charging operators.

The public transport authorities segment holds the largest market share due to large-scale electrification of bus fleets and government-led initiatives to reduce urban emissions. Fixed routes and centralized depot operations make charging infrastructure deployment more efficient and predictable. Significant public funding and policy support further accelerate adoption. Continuous fleet expansion in urban mobility systems, along with long operational hours, ensures consistent demand for reliable and high-capacity depot charging solutions across major cities globally.

- For instance, in February 2026, Helix Water District developed a USD 11 million EV depot with 87 chargers (40–640 kW) and 5.9 MW capacity, integrating AI-based load management to support medium- and heavy-duty fleet electrification and shared public-sector charging.

The third-party charging operators segment is projected to grow at a CAGR of 19.6% during the forecast period. Increasing outsourcing of charging infrastructure, rising charging-as-a-service models, and growing demand for scalable solutions are driving rapid adoption among fleet operators seeking reduced capital investment.

By Depot Type

Government Electrification Programs Drive Municipal/Government Fleet Depots Segment Demand

Based on depot type, the market is segmented into private fleet depots, public/shared charging depots, and municipal/government fleet depots.

The municipal/government fleet depots segment dominates the market due to large-scale electrification initiatives led by public authorities. These depots support buses, utility vehicles, and service fleets operating on fixed routes, enabling efficient centralized charging. Strong government funding, policy mandates, and long-term sustainability goals drive infrastructure deployment. Additionally, predictable usage patterns and high vehicle volumes ensure consistent demand for reliable, high-capacity charging systems across urban and intercity transport networks.

The public/shared charging depots segment is projected to grow at a CAGR of 19.6% during the forecast period. Increasing demand for flexible charging access, shared infrastructure models, and third-party service providers is accelerating adoption among diverse fleet operators seeking cost-efficient solutions.

By Vehicle Type

To know how our report can help streamline your business, Speak to Analyst

Electric Light Commercial Vehicles (eLCVs) Segment Leads due to their Extensive Use in Last-Mile Delivery

Based on vehicle type, the market is segmented into electric buses, electric trucks, and electric Light Commercial Vehicles (eLCVs).

The electric Light Commercial Vehicles (eLCVs) segment dominates the market due to their extensive use in urban logistics, e-commerce, and last-mile delivery operations. High fleet volumes, frequent daily usage, and predictable depot return cycles make them ideal for depot charging. Rapid electrification by logistics companies and the favorable total cost of ownership further support adoption. Additionally, their compatibility with medium-power charging infrastructure ensures cost-effective deployment, sustaining strong demand across urban fleet operations globally.

- For instance, in June 2025, Amazon deployed over 30,000 Rivian electric delivery vans across the U.S., featuring ADAS, 360° visibility, and integrated telematics. The company delivers over 1 billion packages annually while advancing large-scale fleet electrification and depot charging demand.

The electric buses segment is projected to grow at a CAGR of 18.8% during the forecast period. Increasing government investments in public transport electrification, fixed-route operations, and rising sustainability targets are accelerating the adoption of the CV depot charging infrastructure for large-scale bus fleets.

CV Depot Charging Market Regional Outlook

By geography, the market is categorized into Europe, North America, South America, Asia Pacific, and the Middle East & Africa.

Asia Pacific

Asia Pacific CV Depot Charging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest CV depot charging market share due to aggressive electrification of commercial vehicle fleets, particularly in China and India. Strong government mandates, subsidies, and large-scale public transport electrification programs drive infrastructure deployment. The region benefits from a high concentration of manufacturing capabilities and growing logistics demand. Additionally, rapid urbanization and expanding e-commerce sectors are increasing the need for efficient depot charging solutions. Continuous investments in grid expansion and energy infrastructure further support sustained CV depot charging market growth across the region.

- For instance, in January 2026, QUCEV expanded commercial EV manufacturing with a focus on heavy-duty vehicles, including 55T trucks and 28T haulage EVs. The company leverages BYD battery technology and scales production capacity to support industrial fleet electrification across logistics and construction sectors.

China CV Depot Charging Market

China’s market in 2026 is estimated to reach around USD 3.30 billion, accounting for roughly 41.6% of global revenues. Strong government mandates, large electric bus fleets, and domestic manufacturing leadership drive sustained infrastructure expansion and dominance.

Japan CV Depot Charging Market

The Japanese market is estimated to reach around USD 0.26 billion by 2026, accounting for roughly 3.3% of global revenues. Growth is supported by smart city initiatives, technological innovation, and the gradual electrification of commercial transport fleets.

India CV Depot Charging Market

The Indian market in 2026 is estimated to reach around USD 0.66 billion, accounting for roughly 8.4% of global revenues. Rapid e-commerce growth, government incentives, and rising fleet electrification are accelerating infrastructure deployment and market expansion.

Europe

Europe accounts for the second-largest market share, driven by strict emission regulations and ambitious carbon neutrality targets. Governments are heavily investing in electric public transport and logistics electrification, boosting market demand. Well-established grid networks and supportive policies, such as subsidies and incentives, accelerate adoption. Additionally, increasing collaboration between public and private stakeholders is enhancing infrastructure deployment. The region’s strong focus on sustainability and clean mobility continues to drive steady and structured market expansion.

- For instance, in December 2025, BVG inaugurated a USD 162.7 million electric bus depot in Berlin, spanning 6.6 hectares and designed for 220 vehicles, supporting large-scale fleet electrification with expanded depot and terminal charging infrastructure, operational by 2027.

Germany CV Depot Charging Market

Germany’s market is estimated to reach around USD 0.25 billion by 2026, accounting for roughly 3.1% of global revenues. Strong automotive ecosystem, emission regulations, and logistics electrification are driving steady adoption of depot charging infrastructure.

U.K. CV Depot Charging Market

The U.K. market is estimated to touch around USD 0.31 billion by 2026, accounting for roughly 3.9% of global revenues. Government funding, net-zero targets, and electric bus adoption are accelerating the deployment of scalable depot charging solutions.

North America

North America represents the third-largest market share, supported by the rising adoption of electric trucks and buses across the U.S. and Canada. Government funding programs and private sector investments are accelerating charging infrastructure deployment. The expansion of e-commerce and logistics networks is further increasing demand for depot charging solutions. Additionally, technological advancements and the presence of major charging solution providers contribute to market growth. However, regional variations in policies and grid readiness create a moderately paced but steady expansion trajectory across the region.

- For instance, in March 2026, Massachusetts Clean Energy Center (MassCEC) expanded the MOR-EV Trucks program, offering rebates up to USD 100,000 per vehicle, supporting commercial fleet electrification, reducing acquisition costs, and accelerating the adoption of zero-emission trucks alongside charging infrastructure incentives.

U.S. CV Depot Charging Market

The U.S. market is estimated to reach around USD 0.74 billion by 2026, accounting for roughly 9.4% of global revenues. Increasing electric truck adoption, federal incentives, and expanding logistics networks are driving strong infrastructure investment and growth.

South America

South America is the fastest-growing region and is projected to expand at a CAGR of 20.6% during the forecast period. Countries such as Brazil and Chile are investing in electric bus fleets and sustainable urban mobility solutions. Growing awareness of environmental benefits and rising fuel costs are encouraging fleet electrification. International funding and partnerships are supporting infrastructure development. As regulatory frameworks evolve and pilot projects scale into full deployments, the region is witnessing rapid adoption of depot charging solutions.

- For instance, in August 2025, Buenos Aires launched its first all-electric bus line with 12 Chinese Asiastar buses, supporting urban fleet electrification trials and expanding international deployment of electric mobility solutions in Latin America.

Middle East & Africa

The Middle East & Africa region is experiencing gradual growth, driven by government initiatives to diversify energy sources and reduce dependence on fossil fuels. Investments in smart cities and sustainable urban mobility projects are supporting the adoption of electric commercial vehicles. Public transport electrification in select cities is creating demand for depot charging infrastructure. However, limited grid infrastructure and high initial investment costs pose challenges. Despite this, increasing policy support and pilot projects are expected to drive steady long-term market development.

- In October 2025, the Deliver-E Coalition was launched by major platforms to accelerate zero-emission deliveries, promoting EV adoption, fleet electrification, and shared best practices. It supports charging infrastructure expansion and reduces emissions through large-scale two- and three-wheeler electrification.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Players Forging Partnerships with Fleet Operators to Gain Competitive Edge

The market is moderately fragmented, with global energy majors, charging solution providers, and technology firms competing across regions. Major players such as ABB, Siemens, Shell Recharge, BP Pulse, ChargePoint, and Tesla compete through high-power charging systems, smart energy management, and integrated digital platforms. Companies are focusing on scalable depot solutions, software-driven load optimization, and partnerships with fleet operators. Strategic collaborations, acquisitions, and grid integration capabilities further strengthen competitive positioning.

- For instance, in November 2025, ABB deployed SCADA-based load management at Greenlane’s truck charging hub with 400 kW chargers, enabling dynamic load balancing, prioritized load shedding, and grid protection while supporting up to 200 electric trucks per day.

LIST OF KEY CV DEPOT CHARGING COMPANIES PROFILED

- ABB E-mobility (Switzerland)

- Siemens (Germany)

- ChargePoint (U.S.)

- bp pulse (U.K.)

- Shell Recharge (U.K.)

- Kempower (Finland)

- i-charging (Portugal)

- Alpitronic (Italy)

- Tritium (Australia)

- EVBox (France)

- Wallbox (Spain)

- EO Charging (U.K.)

- Blink Charging (U.S.)

- Eaton (Ireland)

- Delta Electronics (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Kempower deployed depot and on-route charging for NEW Group in Germany. The installation includes a 1.2 MW system with modular power units, 16 charging satellites, and 350 kW pantographs, enabling dynamic load distribution and efficient electric bus operations.

- January 2026: bp pulse announced a Class 6-8 electric truck charging hub in California, featuring high-power chargers for heavy-duty fleets. The project supports long-haul electrification and expands depot-based infrastructure across key freight corridors.

- December 2025: Singapore’s LTA launched a tender for liquid-cooled electric bus chargers with integrated management systems. The solution enables SoC-based smart charging across multiple depots, supporting scalable fleet electrification and optimized energy utilization.

- October 2025: Kempower deployed 16 power units and 44 control units in Karlsruhe. The development features dynamic power distribution, a ceiling-mounted space-saving design, and cloud-based ChargEye software for scalable and efficient electric bus fleet charging.

- June 2025: Illinois district deployed a charging depot for 25 electric school buses, incorporating managed charging systems to support daily operations, optimize energy usage, and advance zero-emission school transportation.

- May 2025: Venice deployed 44 ABB Terra 184 DC fast chargers (up to 180 kW) with 5 MVA grid capacity. The system enables overnight depot charging, real-time monitoring, and scalable energy management for electric bus fleet operations.

- October 2024: Siemens secured a contract with Unibuss to deploy Depot360 Managed Services, enabling smart charging, load shifting, peak shaving, and AI-based monitoring to optimize energy use and improve efficiency of a 259-electric-bus fleet.

- September 2024: New York inaugurated its largest electric bus depot in Buffalo. The facility features 36 overhead pantograph chargers and scalable substation infrastructure, supporting up to 50 buses and enabling full fleet electrification by 2035.

REPORT COVERAGE

The global CV depot charging market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Charging Infrastructure Type, By Charger Power Output, By End User, By Depot Type, By Vehicle Type, and By Region |

| By Charging Infrastructure Type |

|

| By Charger Power Output |

|

| By End User |

|

| By Depot Type |

|

| By Vehicle Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.59 billion in 2025 and is projected to reach USD 28.95 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 4.14 billion.

The market is expected to exhibit a CAGR of 17.6% during the forecast period.

The electric light commercial vehicles (ELCVs) segment leads the market in terms of vehicle type.

Stringent emission norms are the key factors driving the market.

Major players in the market include ABB, Siemens, Shell Recharge, BP Pulse, ChargePoint, and Tesla.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us