Electric Commercial Vehicle Market Size, Share & Industry Analysis, By Vehicle Type (Van, Truck, and Bus), By Propulsion Type (BEV and PHEV), By Power Output (Less than 150 kW, 150-250 kW, and Above 250 kW), By Range (Less Than 150 Mile, 150 to 300 Mile, and Above 300 Mile), and Regional Forecast, 2026-2034

Electric Commercial Vehicle Market Size & Trends Insights

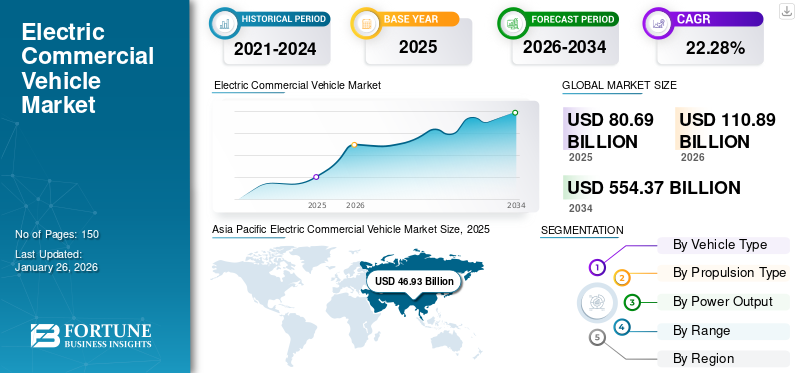

The global electric commercial vehicle market size was valued at USD 80.69 billion in 2025 and is projected to grow from USD 110.89 billion in 2026 to USD 554.37 billion by 2034, exhibiting a CAGR of 22.28% during the forecast period. Asia Pacific dominated the electric commercial vehicle market with a market share of 58.16% in 2025.

The global electric commercial vehicle market growth is driven by the increasing demand for sustainable and cost-effective transportation solutions, stringent government regulations on emissions, and advancements in battery technology.

Download Free sample to learn more about this report.

ELECTRIC COMMERCIAL VEHICLE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 80.69 Billion

- 2026 Market Size: USD 110.89 Billion

- 2034 Forecast Market Size: USD 554.37 Billion

- CAGR: 22.28% from 2026–2034

- Asia Pacific dominated the electric commercial vehicle market with a 58.16% share in 2025.

- Vans are projected to account for 80.29% of the global market in 2026.

- BEVs are expected to hold a dominant 90.12% market share in 2026.

Asia Pacific

Asia Pacific generated USD 46.93 billion in 2025 and is projected to reach USD 65.00 billion in 2026.

Europe

Europe accounted for USD 22.03 billion in 2025 and is expected to grow to USD 30.19 billion in 2026.

North America

North America reached USD 8.60 billion in 2025 and is projected to expand to USD 11.61 billion in 2026.

U.S.

The electric commercial vehicle market is projected to reach USD 10.17 billion by 2026.

Japan

The electric commercial vehicle market is projected to reach USD 0.93 billion by 2026.

Read More

The Electric Commercial Vehicle (ECV) market encompasses the production, distribution, and sales of electric vehicles designed for commercial applications. These vehicles include a wide range of types, such as trucks, vans, buses, and specialized utility vehicles used for transporting goods, people, and equipment. ECVs are powered by electric motors and run on rechargeable batteries, eliminating the need for traditional internal combustion engines.

The market includes a variety of vehicle types, such as trucks, buses, and vans. Electric trucks range from light-duty delivery vans to heavy-duty trucks. Companies, such as Tesla, Daimler, and Volvo are at the forefront of developing electric trucks that can meet the demands of various commercial applications.

Electric vans are particularly popular for urban delivery services due to their compact size and lower emissions. Major players include Ford, Mercedes-Benz, and Nissan. Electric buses are increasingly being adopted by public transportation authorities to reduce operational costs and environmental impact. Leading manufacturers include BYD, Proterra, and New Flyer.

Leading automotive manufacturers such as Tesla, Daimler, and BYD are investing heavily in R&D to develop advanced ECVs. Startups and niche players, such as Rivian and Arrival, are also making significant contributions. This development drives the market growth during the forecast period.

Electric Commercial Vehicle Market Trends

Advancements in Autonomous Driving to Set a Positive Trend for Market Growth

Autonomous driving technology is profoundly impacting the market for electric commercial vehicles, fostering innovation and acceptance. As businesses strive to boost efficiency and lower operational expenses, merging autonomous systems with electric vehicles offers an appealing solution, ensuring enhanced safety, decreased emissions, and streamlined logistics. The emergence of self-driving vehicles is transforming the landscape of commercial transport. Through progress in artificial intelligence, machine learning, and sensor technologies.

Additionally, the integration of electric powertrains with autonomous driving features is anticipated to result in considerable savings in costs over time. Electric vehicles usually incur lower maintenance expenses than conventional combustion engines, and when combined with autonomous technology, they can function more efficiently, minimizing fuel usage and deterioration.

Download Free sample to learn more about this report.

The regulatory landscape is also changing to adapt to these developments. Governments are starting to acknowledge the possible advantages of self-driving electric vehicles, resulting in favorable policies and infrastructure creation. This fosters a positive atmosphere for manufacturers and service providers to put money into research and development, further accelerating the electric commercial vehicle market growth.

For instance, In January 2025, Alexander Dennis (NFI Group Inc) announced that it had completed the first Enviro100AEV autonomous electric bus for the Connector project in Cambridge ahead of track testing. The bus will now enter a period of track-based testing to calibrate and fine-tune Fusion Processing’s CAVStar automated drive system before delivery to Cambridge.

Market Dynamics

Market Drivers

Decreasing Battery Costs for Electric Vehicles to Propel Market Growth

The cost of lithium-ion batteries, a crucial component of electric vehicles, has been decreasing due to economies of scale and technological advancements. This reduction in battery costs makes electric commercial vehicles more economically viable, driving market growth. Between 2008 and 2023, the cost of EV battery packs decreased by approximately 90%, from USD 1,415 per kilowatt-hour (kWh) to USD 139/kWh. This dramatic reduction is attributed to advancements in battery technology, improved manufacturing processes, and increased production volumes.

Further cost reductions are anticipated. By 2026, battery prices are expected to drop by almost 50% from 2023 levels, is projected to reach around USD 80/kWh. Lower battery costs significantly reduce the upfront costs of electric commercial vehicles, making them more attractive to businesses. This shift helps achieve total cost of ownership (TCO) parity with diesel vehicles, especially when considering lower operational costs due to cheaper electricity and reduced maintenance operations.

In February 2025, the Indian Government announced the elimination of basic customs duty (BCD) on imports of a range of materials, including lead, zinc, and cobalt, that go into making lithium-ion batteries and on select capital goods used in the manufacturing of electric vehicles, in a move that will likely make these zero-emission vehicles cheaper to own. BCD will be removed 35 different types of capital goods - or machinery - used for lithium-ion battery manufacturing. This will bring down the cost of setting up an EV battery manufacturing factory in India.

MARKET RESTRAINTS

Limited Charging Infrastructure May Hamper Market Growth

The availability of charging stations is often inadequate, particularly in emerging markets, which can lead to range anxiety and operational challenges. A key challenge is the insufficient number of charging stations, particularly in urban and rural areas where commercial vehicles operate. This scarcity can lead to range anxiety among fleet operators, who may worry about the ability to recharge vehicles during long routes or after completing deliveries. Without a robust network of charging facilities, companies may hesitate to invest in electric vehicles, fearing operational disruptions. This limited charging infrastructure hinders the market growth.

Market Opportunities

Rising E-Commerce and Last Mile Delivery to Propel Market Growth

The shift toward e-commerce and last-mile delivery services is creating a surge in demand for electric vans and trucks, which are well-suited for urban environments. Companies are also recognizing the long-term financial benefits of electric fleets, including reduced maintenance costs and government incentives.

In June 2024, Honda Motor Co., Ltd. announced that it would begin sales in Japan of a new commercial-use mini-EV (electric vehicle), the N-VAN, on October 10, 2024. The N-VAN e: is a commercial-use mini-EV model developed by adding user-friendly features unique only to EVs to the gasoline-powered N-VAN, which has been popular as a versatile vehicle that accommodates a broad range of customer needs for both commercial and recreational uses.

Electric commercial vehicles offer numerous advantages for last-mile delivery, including reduced emissions, lower operating costs, and quieter operations, which are particularly beneficial in urban environments. With cities increasingly prioritizing sustainability and reducing air pollution, the integration of ECVs into delivery fleets aligns with these goals, making them an attractive choice for businesses.

Segmentation Analysis

Request for Customization to gain extensive market insights.

By Vehicle Type

Rising Last-Mile Delivery Services Boosted the Demand for Vans

The market is segmented into van, bus and truck, based on vehicle type.

The van segment is projected to reach 80.29% of the global market share in 2026. Vans are widely used for last-mile delivery services in urban areas, where emissions are a significant concern. Companies, such as Amazon, UPS, and DHL have been investing heavily in electric van fleets to reduce their carbon footprint and meet sustainability goals. This advancement boosts the demand for the electric commercial vehicle market throughout the forecast period.

The electric truck segment is emerging as one of the fastest-growing segments, driven by demand from logistics companies and fleet operators seeking to reduce their carbon footprint and operational costs. In August 2024, Volvo Truck and DSV signed an agreement for 300 electric heavy trucks. The deal is one of the most significant commercial orders to date for Volvo electric trucks. With the order, DSV will have one of the largest company fleets of heavy electric trucks in Europe.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

Rising Investment In the Development of EV Technologies By Manufactures Drive the Market Growth for BEV

By propulsion type, the market can be segmented into BEV and PHEV.

The BEV (battery electric vehicle) segment is expected to lead the market, contributing 90.12% globally in 2026. Major automotive manufacturers are significantly investing in the development of electric vehicle technologies. For instance, companies, such as Volvo and Ford are committing substantial resources to expanding their electric vehicle portfolios, which directly impacts the demand for commercial vehicles. In April 2024, BYD announced that the company plans to launch its first pure electric pickup truck in 2024. BYD has been aggressively pushing its electric vehicles into the various Global markets.

The PHEV (Plug-in Hybrid Electric Vehicle) segment held the second-largest market share. Continuous improvements in hybrid technology enhance vehicle performance and efficiency. Innovations in battery technology, such as solid-state batteries, promise increased range and reduced costs, making hybrids more appealing. Manufacturers are also focusing on developing new hybrid models with advanced features that attract consumers. This development drives the segment growth.

By Power Output

Increasing Adoption of Light Duty Commercial Vehicles Boost the Demand for 150 kW Segment Growth

Based on power output, the market is segmented into less than 150 kW, 150-250 kW, and above 250 kW.

The less than 150 kW segment is the dominant segment. The segmental growth is attributed to the increasing adoption of light-duty commercial vehicles. Partnerships and collaborations among manufacturers, technology providers, and governments are fostering an environment conducive to growth in this segment.

The above 250 Kw segment held a significant market share. This surge is driven by advancements in technology, increasing demand for sustainable transportation solutions, and the need for efficient logistics in various industries. Electric vehicles with higher power outputs are becoming essential for heavy-duty applications, including freight and public transport.

By Range Analysis

150 to 300 Mile Segment Commanded the Market Due to Rising Demand for Efficient and Sustainable Transportation Solutions

Based on range type, the market is segmented into less than 150 mile, 150 to 300 mile and above 300 mile.

The 150 to 300 mile segment is projected to reach 64.15% of the global market share in 2026. The segmental growth is attributed to the increasing demand for efficient and sustainable transportation solutions. As businesses seek to reduce their carbon footprint and operational costs, electric vehicles within this range are becoming the preferred choice for logistics and delivery services. The anticipated growth in this segment is expected to contribute to the overall expansion of the electric commercial vehicle market.

The above 300-mile segment held a significant market share, driven by improvements in battery energy density and charging infrastructure. Technologically advanced lithium-ion batteries can now provide ranges of up to 500 miles on a single charge, making them viable for long-haul operations. Additionally, the development of fast-changing technologies has reduced downtime, enhancing the operational efficiency of electric fleets.

ELECTRIC COMMERCIAL VEHICLE MARKET REGIONAL OUTLOOK

In terms of geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific Electric Commercial Vehicle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific Dominated the Market Due to Favorable Government Initiatives for Vehicle Electrification

The Asia Pacific region captured 58.16% of the global market in 2025, generating USD 46.93 billion in revenue, and is projected to reach USD 65 billion in 2026. Asia Pacific, particularly China, is the largest market for electric commercial vehicles. This region is characterized by rapid industrialization, urbanization, and government policies that favor EV adoption. China is a global leader in EV battery production and vehicle manufacturing. This devolvement increases the demand for the electric commercial vehicle market during the forecast period. The Japan market is projected to reach USD 0.93 billion by 2026, the China market is projected to reach USD 61.56 billion by 2026, and the India market is projected to reach USD 0.66 billion by 2026.

Europe

In 2025, the Europe market stood at USD 22.03 billion, representing 27.31% of global demand, and is projected to grow to USD 30.19 billion in 2026. The market for electric commercial vehicles has grown significantly in Europe in recent years due to stringent environmental policies and a strong commitment to reducing carbon emissions. The region is home to several leading manufacturers and has a well-developed charging infrastructure. The European Union's emission reduction targets, such as the European Green Deal, are pushing the adoption of ECVs. Both public and private sectors are investing heavily in EV infrastructure and R&D. The UK market is projected to reach USD 4.74 billion by 2026 and the Germany market is projected to reach USD 9.21 billion by 2026.

North America

North America contributed approximately USD 8.6 billion to the global market in 2025, accounting for 10.66% share, and is expected to reach USD 11.61 billion in 2026. North America, particularly the U.S. and Canada, has seen robust growth in the electric commercial vehicle market. Stringent emission regulations and a growing emphasis on sustainability characterize this region. The availability of government incentives, such as tax credits and grants, has further fueled the adoption of electric commercial vehicles. The increasing E-commerce sector in U.S. drive the demand for electric commercial vehicle market. The U.S. market is projected to reach USD 10.17 billion by 2026.

Rest Of The World

In 2025, Rest of the World represented USD 3.13 billion, accounting for 3.88% of the worldwide market, and is projected to grow to USD 4.09 billion in 2026. The market growth in the rest of the world is attributed to urbanization and a growing need for sustainable transportation solutions. However, compared to other regions, the market is still in its early stages.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players are Emphasizing the Development of Better Battery Technologies for Commercial EVs

The major players in the market focuses on investing in technology and infrastructure. Continuous improvement in battery technology and the development of charging infrastructure are critical for reducing range anxiety and supporting fleet operators. Companies must align their offerings with increasing regulatory demands for emissions reductions. Sustainability initiatives are becoming pivotal for brand differentiation.

Key players in this market include Daimler AG, BYD, and Tesla. BYD is a global leader in electric vehicles, with a strong presence in the commercial vehicle segment. The company offers a wide range of electric buses, trucks, and vans. BYD is known for its cutting-edge battery technology and vehicle design. The company has a significant presence in international markets, particularly in Europe and North America. BYD has partnered with various municipalities and transit agencies to deploy electric buses and trucks and is investing heavily in research and development to improve battery efficiency and vehicle range.

LIST OF KEY ELECTRIC COMMERCIAL VEHICLE COMPANIES PROFILED

- BYD Inc. (China)

- AB Volvo (Sweden)

- Traton SE (Germany)

- Daimler Truck AG (Germany)

- Zhengzhou Yutong Bus Co., Ltd. (China)

- Ford Motor Company (U.S.)

- Tesla Inc. (U.S.)

- Proterra Inc. (U.S.)

- Rivian Automotive Inc. (U.S.)

- Tata Motors Limited (India)

- Olectra Greentech Limited (India)

- Paccar Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In November 2024, B solely by BYD’s own Blade Battery technology, with a capacity of up to 532 kWh. The vehicle incorporates BYD’s 6-in-1 Integrated Controller with Silicon Carbide technology, which combines 6 key electric elements in one plug-and-play formation, including 2 electric motor control units, 1 steering control unit, 1 air compressor controller, 1 DC-DC converter and 1 power distributor unit.

- In July 2024, Electrify Azerbaijan Company and BYD signed an agreement to modernize the passenger bus fleet in Azerbaijan. This agreement covers the purchase of electric buses, their servicing, and the establishment and localization of electric bus production in Azerbaijan. BYD plans to invest USD 60 million in Azerbaijan, creating new production areas for light-duty electric trucks, electric vehicles for municipal services, and electric passenger cars starting in 2026, with battery production for energy storage beginning in 2028.

- In November 2023, Rivian Automotive, Inc. announced that the company would enable other companies to purchase its custom-designed Rivian Commercial Van. This move delivers companies all around the world more opportunities to electrify their delivery fleets with state-of-the-art vehicles, which will help to reduce CO2 emissions further.

- In May 2023- Suzuki Motor Corporation (Suzuki), Toyota Motor Corporation (Toyota), and Daihatsu Motor Co., Ltd. announced that they would reveal prototype electric mini-commercial vans (BEVs) equipped with a jointly developed BEV system.

- In March 2023, Moscow signed a contract with KAMAZ for 1,000 electric buses. There are also plans to purchase another 200 electric buses from GAZ Group. Moscow currently runs 1,055 electric buses on 79 routes. Moscow plans to install nearly 200 ultra-fast charging stations for the electric buses, open a second electric bus park in the Mitino district northwest of Moscow, and launch 29 more eleYD introduced its new all-electric bus, the BD11, at Euro Bus Expo 2024. The 10.9-meter double-decker bus is poweredctric bus routes.

REPORT COVERAGE

The market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, vehicle types, and leading propulsion types. Besides this, the report offers insights into the market trends and highlights vital industry developments. In addition to the factors above, the report encompasses several factors contributing to the market's growth over recent years.

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 110.89 billion in 2026 to USD 554.37 billion by 2034, exhibiting a CAGR of 22.28%

In 2025, the Asia Pacific market size stood at USD 46.93 billion.

The market is projected to grow at a CAGR of 22.28% and exhibit steady growth during the forecast period.

The BEV is expected to be the leading segment in this market during the forecast period.

Decreasing battery costs for electric vehicles will propel the market growth.

Major players in this market include Daimler AG, BYD, and Tesla.

Asia Pacific dominated the market share in 2024.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us