Data Center Accelerator Market Size, Share & Industry Analysis, By Accelerator Type (GPU, ASIC, FPGA, DPU/IPU/SmartNIC and Others), By Deployment (Cloud, On-premise and Hybrid), By End-user (Hyperscalers/CSPs and Colocation Providers and Enterprises) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

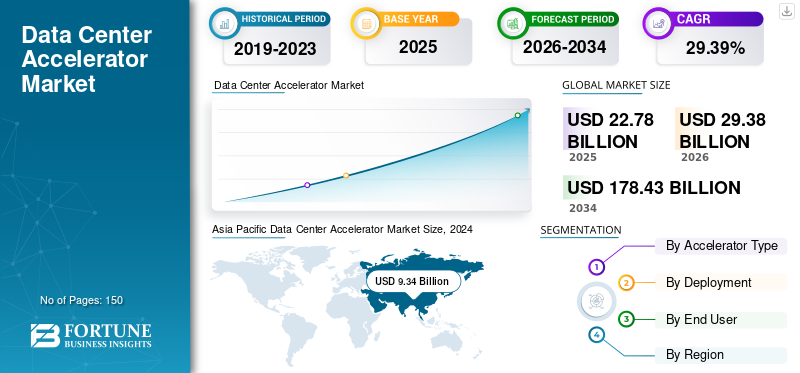

The global data center accelerator market size was valued at USD 29.38 billion in 2025. The market is projected to grow from USD 37.92 billion in 2026 to USD 249.10 billion by 2034, exhibiting a CAGR of 26.53% during the forecast period. Asia Pacific dominated the data center accelerator market with a market share of 41.37% in 2025.

Data center accelerator refers to a specialized hardware including AI accelerators, GPUs, FPGAs and ASICs that are designed to augment the computing performance for tasks such as analytics, AI, and high performance workloads. The market is growing steadily driven by the increase in cloud services adoption, data traffic, demand for energy efficient and faster processing, as well as surging AI and machine learning workloads.

Different key players operating in the market include NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, Google LLC, Amazon Web Services, Inc., Microsoft Corporation and others. These companies use strategies such as developing advanced AI-optimized chips, offering customized accelerator architectures, forming partnerships with different cloud providers and investing rapidly in research and development for higher throughput and lower power consumption.

Download Free sample to learn more about this report.

Data Center Accelerator Market Key Takeaways

- 2025 Market Size: USD 29.38 billion

- 2026 Market Size: USD 37.92 billion

- 2034 Forecast Market Size: USD 249.10 billion

- CAGR: 26.53% from 2026–2034

- Asia Pacific dominated the data center accelerator market with a 41.37% share in 2025.

- The GPU segment held the largest market share in 2024, generating USD 6.52 billion in revenue.

- The Cloud segment is expected to lead the market, accounting for 75.12% of global revenue in 2026.

North America

North America accounted for 29.86% of global revenue in 2025, supported by increasing adoption of AI workloads and advanced cloud computing platforms.

Europe

Europe represented 19.48% of the global market in 2025, driven by expanding digital transformation initiatives and growing enterprise demand for accelerated computing.

Asia Pacific

Asia Pacific remained the leading regional market, reaching USD 12.16 billion in 2025 and benefiting from strong investments in AI infrastructure and hyperscale data centers.

U.S.

The U.S. market is projected to reach USD 6.67 billion by 2026, fueled by strong investments from hyperscalers and cloud service providers in AI-enabled data center infrastructure.

Japan

The Japan market is projected to reach USD 3.74 billion by 2026, supported by rising AI adoption, high-performance computing deployments, and growing demand for advanced data processing capabilities.

Read More

MARKET DYNAMICS

Market Drivers

Growing Demand for Generative AI and HPC Applications Drives the Market Development

The rapidly growing demand for High Performance Computing (HPC) and AI applications is a prominent driver boosting the data center accelerator market growth. Various generative AI models including large language models, autonomous systems and image generators demand massive parallel processing as well as low-latency computation that is difficult to gain through conventional CPUs.

Similarly, HPC workloads across scientific simulations, research and advanced analytics are based on accelerators to monitor the complex calculations at a scale. With enterprises, research institutions, and cloud providers adopting such technologies, the demand for AI accelerators, GPUs and specialized hardware is expected to surge, thus boosting the market growth.

Market Restraints

High Cost and Power Consumption of Accelerators to Deters the Market Growth

The higher power consumption and cost act as a major challenge for the market growth. Advanced FPGAs, GPUs, and AI chips demand a significant capital investment, thus making its adoption challenging for smaller and cost-sensitive data centers. Their growing operational cost especially cooling requirement and electricity usage also increases the total cost. With accelerators becoming more powerful, the demand for energy is rising, thus creating an efficiency challenge and limiting the deployment across regionals with sustainability regulations and higher energy prices.

Market Opportunities

Rising Adoption of Edge and Cloud AI Infrastructure Offers Lucrative Growth Opportunities

The growing adoption of cloud AI infrastructure and edge Ai provides a lucrative opportunity for the market. With companies shifting the AI processing to cloud based solutions and deploying edge devices to gain real time data, the demand for high performance and lower latency accelerators in growing.

Additionally, cloud providers are demanding scalable FPGA, GPU and ASIC solutions that aids in handling complex AI workloads, whereas, edge environment demands an energy efficient and compact accelerator. This expansion enables vendors to provider a specialized and diverse hardware across both the ecosystems.

DATA CENTER ACCELERATOR MARKET TRENDS

Shift Toward AI-Optimized Data Centers Has Emerged as a Prominent Market Trend

A major trend reshaping the market is growing shift toward AI-optimized data centers driven by the expansion of machine learning, AI and generative AI workloads. Traditional data center architectures are inefficient to meeting the massive memory and computational needs of AI models. This enables operators to adopt GPUs, custom AI accelerators and TPUs.

Such AI centric designs tend to improve the throughput, enhance energy efficiency and reduce the latency. Cloud providers and enterprises also restructure the infrastructure to support the large scale training and inference, thus integrating the specialized hardware, networking solutions and software stacks.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Accelerator Type

Exceptional Versatility of GPU in Parallel Processing Boosts the Segment Growth

Based on accelerator type, the market is segmented into GPU, ASIC, FPGA, DPU/IPU/SmartNIC and Others.

In 2024, GPU segment held the largest data center accelerator market share and with a revenue of USD 6.52 billion. This is due to its exceptional versatility in parallel processing, making it ideal for machine learning, AI and HPC. Additionally, its flexibility, efficiency in handling complex workloads, and stronger software ecosystem also strengthens the segment growth. The GPU segment is projecteed to dominate the market with a share of 69.22% in 2026.

The ASIC segment held highest CAGR of 33.45% in 2024. This growth is attributed to its exceptional efficiency, speed, and optimization capability for specific tasks including AI inference and encryption. Its customized architecture tends to reduce the power use and boosts the performance, making it highly ideal for large-scale data center workloads.

By Deployment

Flexibility, Scalability and Ability of Cloud Solutions Drives Segment Growth

The market is divided into cloud, on-premise, and hybrid, based on deployment.

Among these, cloud segment dominated the market with a revenue share of USD 6.92 Billion in 2024. The Cloud segment is expected to lead the market, contributing 75.12% globally in 2026. The segment’s dominance is attributed to the cloud’s flexibility, scalability and ability to support the resource intensive analytics and AI workloads, thus driving the rapid adoption of high-performance accelerators.

On the other hand, the on premise deployment holds the second-largest market share due to different organizations prioritizing maximum security, performance and control for sensitive data and critical workloads. Additionally, industries including healthcare, finance, and government prefer on-site infrastructure to ensure minimize data exposure, compliance and achieve consistent high speed processing without reliance on external cloud environments.

By End User

To know how our report can help streamline your business, Speak to Analyst

Massive Infrastructure Investments Drive Hyperscalers/CSPs Segment Growth

The market is divided Hyperscalers/CSPs, colocation providers, and enterprises based on end user.

Among these, the Hyperscalers/CSPs segment dominated the market with a revenue share of USD 6.49 billion in 2024. The Hyperscalers/CSPs segment is projecteed to dominate the market with a share of 70.02% in 2026. This growth stems from the massive infrastructure investments, ongoing deployment of advanced accelerators to boost performance, rapid expansion of AI workloads, higher scalability and efficiency across the global cloud platforms.

Enterprises holds the second-largest share in the market due to its increasing reliance on accelerators to augment the performance for internal workloads including data analytics, AI, automation and real time decisions.

DATA CENTER ACCELERATOR MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

Asia Pacific Data Center Accelerator Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 8.77 Billion, contributing 29.86% to global market revenue, and is projected to grow to USD 11.34 Billion in 2026. The region holds second largest share backed by the advancements in digital infrastructure, widespread adoption of AI and stronger cloud usage. Additionally, presence of major tech companies and hyperscale data centers across the U.S., further drives the demand for high-performance accelerator technologies across the region. The U.S. market is projected to reach USD 6.67 billion by 2026.

Europe

The Europe market accounted for USD 5.72 Billion in 2025, representing 19.48% of the global industry, and is expected to reach USD 7.34 Billion in 2026. This growth is driven by the presence of major cloud providers, growing adoption of AI and rapid deployment of digital technologies across the region. Additionally, stronger investments in advanced computing infrastructure and government based digital programs also reinforces the region’s position as a major market contributor. The UK market is projected to reach USD 1.84 billion by 2026. The Germany market is projected to reach USD 1.55 billion by 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 12.16 Billion in 2025, capturing 41.37% of the global market share, and is projected to reach USD 15.83 Billion in 2026. The region is also noticing fastest growth rate majorly due to rising cloud adoption. Additionally, the surge in digitalization and large-scale data center expansion across major economies boosts the overall regional market growth. The Japan market is projected to reach USD 3.74 billion by 2026. The China market is projected to reach USD 4.54 billion by 2026. The India market is projected to reach USD 2.93 billion by 2026.

South America

The South American market is expected to reach USD 1.62 billion in 2025. Growth in the region is comparatively slower than in North America, Europe, and Asia Pacific due to limited investments in advanced technologies, slower deployment of modern data center infrastructure, and relatively lower adoption of cloud computing and AI-driven workloads. However, increasing digitalization initiatives and growing demand for data storage and processing capabilities are expected to support steady market expansion over the forecast period.

Middle East & Africa

The Middle East & Africa market generated USD 1.1 Billion in 2025, representing 3.76% of the global market landscape, and is expected to reach USD 1.39 Billion in 2026. Market growth remains moderate due to slower adoption of advanced data center technologies and lower cloud penetration in several countries across the region. Nevertheless, investments in digital transformation programs, smart city projects, and emerging AI applications are creating new opportunities for market development. Within the region, GCC countries are anticipated to account for a significant share, reaching approximately USD 0.35 billion in 2025, supported by increasing investments in technology infrastructure and data center expansion.

Latin America

Latin America accounted for USD 1.62 Billion in 2025, representing 5.52% of the global market share, and is projected to reach USD 2.02 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focusing on Investing Research and Development to Sustain their Market Positions

The data center accelerator industry is highly competitive with key players including NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, Google LLC, Amazon Web Services, Inc., Microsoft Corporation and others operating in it. These companies are focusing on partnerships, vertical integration, and growing investments in research and development.

LIST OF KEY DATA CENTER ACCELERATOR COMPANIES PROFILED

- NVIDIA Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Intel Corporation (U.S.)

- Google LLC (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Cerebras Systems, Inc. (U.S.)

- SambaNova Systems, Inc. (U.S.)

- Graphcore Ltd. (U.K.)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Google announced its plan to launch TPU AI chips into space. The company will partner with Planet Labs on 'Project Suncatcher,' which will initially see two satellites launch by early 2027 to explore the potential of larger-scale space data center clusters.

- In October 2025, Qualcomm Technologies, Inc. announced the launch of its next-generation AI inference-optimized solutions for data centers. the Qualcomm AI200 and AI250 chip-based accelerator cards, and racks. Building off the Company’s NPU technology leadership, these solutions offer rack-scale performance and superior memory capacity for fast AI inference at high performance per dollar per watt—marking a major leap forward in enabling scalable, efficient, and flexible generative AI across industries.

- In June 2025, Amazon announced plans to invest a new total of USD 12.9 billion from 2025 to 2029 to expand, operate, and maintain its data center infrastructure in Australia. The country’s largest publicly-announced global technology investment will support the strong growth in customer demand for cloud computing and artificial intelligence (AI), accelerating AI adoption and capability, and the continued modernization of Australian organizations of all sizes.

- In February 2025, AMD announced the launch of Instinct MI325X accelerators with 256GB HBM3e memory and 6TB/s bandwidth, assuring 1.4x higher inference performance as compared to competitors and allowing businesses to attain better results with less GPUs.

- In January 2021, NVIDIA Corporation has expanded its vGPU software to help workstations and AI applications run faster. With the company's virtual GPU (vGPU) technology, Organizations can deliver greater scalability and performance to their employees by using GPU-accelerated virtual machines from the data center or cloud.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the data center accelerator market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 26.53% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD billion) |

| Segmentation |

By Accelerator Type

By Deployment

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 29.38 billion in 2025 and is projected to reach USD 249.10 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 26.53% during the forecast period.

Growing demand for Generative AI and HPC Applications drives the market growth.

NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, Google LLC, Amazon Web Services, Inc., Microsoft Corporation and others are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 12.16 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us