Data Transmission Service Market Size, Share & Industry Analysis, By Service Type (Enterprise WAN, Leased Lines, Wavelength Services, Wholesale Connectivity, Managed SD-WAN, and Others), By Customer Type (Large Enterprises, SMEs, Carriers & ISPs, and Others), By Network Type (Fiber-based Networks, Wireless Backhaul, and Others), and Regional Forecast, 2026 - 2034

KEY MARKET INSIGHTS

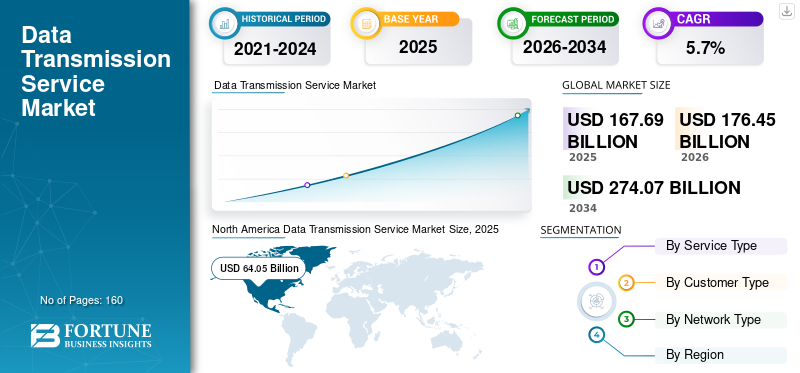

The global data transmission service market size was valued at USD 167.69 billion in 2025. The market is projected to grow from USD 176.45 billion in 2026 to USD 274.07 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. North America dominated the global data transmission service market with a market share of 38.2% in 2025.

The market is witnessing steady growth, driven by rising data traffic volumes and increasing demand for reliable, high-speed connectivity across enterprises and service providers. Data transmission services refer to network services that enable the secure and efficient transfer of data across wide-area networks, data centers, and cloud environments. These services support critical business operations by ensuring seamless communication, low latency, and high availability of data across geographically distributed infrastructures.

The market is further supported by rapid adoption of cloud computing, expansion of data centers, and ongoing deployment of advanced network technologies such as fiber-based infrastructure and 5G. Enterprises across industries are increasingly relying on data transmission services to support digital transformation initiatives, enhance operational efficiency, and enable real-time data-driven applications.

Furthermore, key industry players such as AT&T, Verizon, Lumen Technologies, BT Group, and Tata Communications are focusing on expanding fiber networks, enhancing managed connectivity offerings, and strengthening global network reach to meet evolving enterprise connectivity requirements.

Download Free sample to learn more about this report.

DATA TRANSMISSION SERVICE MARKET TRENDS

Rising Cloud and Data Center Interconnect Demand is a Prominent Market Trend

The increasing adoption of cloud computing and data center interconnect services has emerged as a prominent trend in the market. Enterprises are increasingly distributing workloads across multiple cloud environments and data centers, driving demand for high-capacity, low-latency transmission services. This trend is strengthening the role of managed enterprise connectivity solutions in supporting seamless data flow across geographically dispersed infrastructures.

- For instance, Google Cloud has highlighted the growing importance of high-performance network connectivity to support multi-cloud and hybrid cloud architectures for enterprise customers.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Data Traffic Volumes are Accelerating Market Growth

The rapid increase in global data traffic is a major driver of the data transmission service market. Expanding use of digital platforms, video streaming, enterprise applications, and real-time communication tools is placing greater demands on network capacity and reliability. Enterprises and service providers are increasingly investing in advanced data transmission services to ensure consistent performance and network scalability.

- For example, Cisco has emphasized that rising data consumption across enterprise and consumer networks is driving the need for higher-capacity and more resilient transmission infrastructure.

MARKET RESTRAINTS

High Infrastructure Investment Requirements to Limit Market Expansion

High capital investment requirements associated with building and maintaining advanced transmission infrastructure pose a significant restraint on market growth. Deployment of fiber-based networks, network upgrades, and ongoing maintenance involve substantial costs, which can limit service expansion in certain regions and constrain smaller service providers. These challenges may slow network rollouts, particularly in emerging markets where infrastructure development is still evolving.

- For instance, the International Telecommunication Union has noted that high deployment costs remain a barrier to expanding high-capacity connectivity infrastructure in developing regions.

MARKET OPPORTUNITIES

5G Deployment and Edge Computing Expansion to Create Growth Opportunities

The ongoing rollout of 5G networks and the expansion of edge computing are expected to create significant growth opportunities for the data transmission service market. These technologies require robust, low-latency data transmission to support applications such as real-time analytics, autonomous systems, and immersive digital experiences. Service providers are increasingly enhancing transmission networks to support 5G backhaul and edge connectivity, opening new opportunities for advanced data transmission services.

- For example, Ericsson has highlighted the critical role of high-capacity transport networks in enabling 5G services and next-generation digital applications.

Segmentation Analysis

By Service Type

Growing Complexity of Enterprise IT Environments and Need for Uninterrupted Data Flow Across Locations to Drive Enterprise WAN Dominance

Based on the service type, the market is divided into enterprise WAN, leased lines, wavelength services, wholesale connectivity, managed SD-WAN, and others.

In 2025, the enterprise WAN segment held the largest data transmission service market share. The dominance of this segment is primarily attributed to increasing enterprise reliance on secure, high-capacity, and geographically distributed network connectivity to support cloud computing, data center interconnection, and digital business operations. Enterprise WAN services enable organizations to connect branch offices, data centers, and cloud environments with consistent performance and reliability. The growing complexity of enterprise IT environments and the need for uninterrupted data flow across locations have reinforced the importance of enterprise WAN solutions, supporting sustained demand across industries.

The managed SD-WAN segment is anticipated to rise with a CAGR of 6.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Customer Type

Customized Connectivity Solutions with Enhanced Security, Service-Level Agreements, and Global Coverage Led to Large Enterprises Dominance

Based on customer type, the market is segmented into large enterprises, SMEs, carriers & ISPs, and others.

The large enterprises segment accounted for the highest share in 2025, driven by extensive network requirements, high data volumes, and mission-critical connectivity needs. Large organizations operate complex, multi-location infrastructures and increasingly depend on robust data transmission services to support cloud migration, digital transformation, and real-time business applications. Additionally, large enterprises often require customized connectivity solutions with enhanced security, service-level agreements, and global coverage, further strengthening their reliance on professional data transmission service providers.

The SMEs segment is projected to grow at a CAGR of 6.3% over the forecast period.

By Network Type

Ability to Deliver High Bandwidth, Low Latency, and Reliable Data Transmission Over Long Distances Propelled Fiber-Based Networks Segmental Dominance

Based on the network type, the market is segmented into fiber-based networks, wireless backhaul, and others.

In 2025, the fiber-based networks segment held the largest market share, supported by its ability to deliver high bandwidth, low latency, and reliable data transmission over long distances. Fiber infrastructure is widely adopted for enterprise connectivity, data center interconnection, and backbone network deployments. The increasing deployment of fiber networks to support 5G backhaul, cloud services, and growing data traffic volumes continues to reinforce the dominance of fiber-based data transmission services.

The wireless backhaul segment is projected to grow at a CAGR of 6.1% over the forecast period.

Data Transmission Service Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Data Transmission Service Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest share of the market in 2024 and maintained its leading position in 2025, with a market value of USD 64.05 billion. The region’s dominance is supported by strong enterprise IT spending, early adoption of advanced networking technologies, and a mature cloud and data center ecosystem. Widespread deployment of high-capacity fiber networks and growing demand for secure, managed enterprise connectivity continue to drive data transmission service market growth.

U.S Data Transmission Service Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 58.12 billion in 2026. The country’s market is driven by high data consumption, widespread cloud adoption, and advanced digital infrastructure. Continued investments in 5G, fiber networks, and data centers are strengthening demand for reliable and high-performance connectivity services.

Europe

Europe recorded a market valuation of USD 41.15 billion in 2026. The regional market is driven by increasing demand for secure and resilient data connectivity across industries, supported by enterprise digitalization initiatives and modernization of telecom and fiber infrastructure. Cross-border business operations and rising data governance requirements are also encouraging adoption of managed data transmission services.

U.K Data Transmission Service Market

The U.K. market in 2026 is estimated at around USD 7.06 billion, representing roughly 4.0% of global revenues.

Germany Data Transmission Service Market

Germany’s market is projected to reach USD 7.33 billion in 2026, equivalent to around 4.2% of global sales.

Asia Pacific

Asia Pacific is expected to register the fastest growth during the forecast period and reach a valuation of USD 52.15 billion in 2026. Growth is supported by rapid mobile and broadband penetration, accelerated cloud adoption, and expansion of digital services across enterprises. Increasing investments in 5G rollout, hyper scale data centers, and regional connectivity corridors are strengthening demand for high-performance data transmission services.

Japan Data Transmission Service Market

The Japan market in 2026 is estimated at around USD 7.00 billion, accounting for roughly 4.0% of global revenue.

China Data Transmission Service Market

China’s market in 2026 is projected to reach USD 17.61 billion, representing roughly 10.0% of global market.

India Data Transmission Service Market

The India market in 2026 is estimated at around USD 6.52 billion, accounting for roughly 3.7% of global market.

South America and Middle East & Africa

South America is projected to reach a market valuation of USD 6.91 billion in 2026. Market growth is supported by gradual improvements in telecom infrastructure, expanding internet usage, and increasing enterprise demand for reliable connectivity to enable cloud migration and digital commerce. The Middle East & Africa market is expected to reach a valuation of USD 8.81 billion in 2026. Growth in the region is supported by national digital transformation programs, investments in fiber networks and data centers, and rising demand for secure connectivity across public and private sector organizations.

GCC Data Transmission Service Market

The GCC market is projected to reach around USD 3.49 billion in 2026, representing roughly 2.0% of global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Global Network Footprint and Managed Connectivity Portfolios by Key Players to Propel Market Progress

The market exhibits a semi-consolidated structure, led by prominent providers such as AT&T Inc., Verizon Communications Inc., Orange S.A., and Tata Communications Ltd. These players hold meaningful share due to their large backbone footprints, carrier-grade service portfolios, and continued investments in high-capacity transport and managed overlays (SD-WAN), alongside ecosystem collaborations that accelerate automation and service delivery.

- For instance, In May 2025, Orange Wholesale signed a strategic partnership with DCConnect Global to advance network automation and enable API-driven, on-demand provisioning, extending automated services to thousands of endpoints across dozens of countries.

In addition, market competitiveness is reinforced by other global and regional operators such as Vodafone group, BT International, Telefónica, and NTT, which remain visible in global managed SD-WAN/provider benchmarking and continue to strengthen their enterprise connectivity stacks through platform partnerships and footprint expansion.

LIST OF KEY DATA TRANSMISSION SERVICE COMPANIES PROFILED

- AT&T Inc. (U.S.)

- BT Group plc (U.K.)

- China Telecom Corporation Limited (China)

- Deutsche Telekom AG (Germany)

- Lumen Technologies, Inc. (U.S.)

- NTT Communications Corporation (Japan)

- Orange S.A. (France)

- Tata Communications Ltd. (India)

- Telefónica S.A. (Spain)

- Verizon Communications Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Tata Communications announced the integration of a new submarine cable system TGN-IA2 into its network fabric to support scalable bandwidth and high-capacity data transfer for enterprises, hyperscalers, and service providers across intra-Asia routes and onward connectivity to the U.S., Europe, the Middle East & Africa, and India.

- April 2025: Amphenol Corporation announced the acquisition of CommScope’s connectivity solutions business to expand its broadband, wireless, and data center connectivity portfolio.

- March 2025: Prysmian Group acquired Channell Commercial Corporation to expand its U.S. footprint and strengthen fiber-optic and data connectivity infrastructure supporting high-capacity data transmission networks.

- February 2025: Qualcomm completed the acquisition of Alphawave Semi to enhance its high-speed interconnect and data center networking capabilities amid rising bandwidth demand.

- January 2025: iBASIS acquired selected wholesale connectivity assets from Telstra Group, strengthening its international network reach and carrier-to-carrier data transmission services.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.7% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type, Customer Type, Network Type, and Region |

|

By Service Type |

· Enterprise WAN · Leased Lines · Wavelength Services · Wholesale Connectivity · Managed SD-WAN · Others |

|

By Customer Type |

· Large Enterprises · SMEs · Carriers & ISPs · Others |

|

By Network Type |

· Fiber-based Networks · Wireless Backhaul · Others |

|

By Region |

· North America (By Service Type, Customer Type, Network Type, and Country) o U.S. (By Network Type) o Canada (By Network Type) o Mexico (By Network Type) · Europe (By Service Type, Customer Type, Network Type, and Country) o Germany (By Network Type) o U.K. (By Network Type) o France (By Network Type) o Italy (By Network Type) o Rest of Europe · Asia Pacific (By Service Type, Customer Type, Network Type, and Country) o China (By Network Type) o Japan (By Network Type) o India (By Network Type) o South Korea (By Network Type) o Rest of Asia Pacific · South America (By Service Type, Customer Type, Network Type, and Country) o Brazil (By Network Type) o Argentina (By Network Type) o Rest of South America · Middle East & Africa (By Service Type, Customer Type, Network Type, and Country) o GCC (By Network Type) o South Africa (By Network Type) o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 167.69 billion in 2025 and is projected to reach USD 274.07 billion by 2034.

In 2025, the market value stood at USD 64.05 billion.

The market is expected to exhibit a CAGR of 5.7% during the forecast period of 2026-2034.

By service type, the enterprise WAN segment is expected to lead the market.

The market is driven by rising data traffic, cloud adoption, and increasing demand for high-capacity enterprise connectivity.

AT&T, Verizon, Lumen Technologies, BT Group, Tata Communications, and Orange S.A. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us