Digital Biomanufacturing Market Size, Share & Industry Analysis, By Offering (Software & Platforms, Hardware & Connected Equipment, and Services), By Type (Manufacturing Execution & Electronic Batch Records, Automation & Process Control, Digital Twins, Modeling & Simulation, AI, Machine Learning & Advanced Analytics, Quality & Laboratory Informatics, and Others), By Application (Process Development & Scale-up, Commercial GMP Manufacturing Execution, and Others), By End User (Pharmaceuticals & Biotechnology Companies, CMOs & CDMOs, and Others), and Regional Forecast, 2026-2034

Digital Biomanufacturing Market Size and Future Outlook

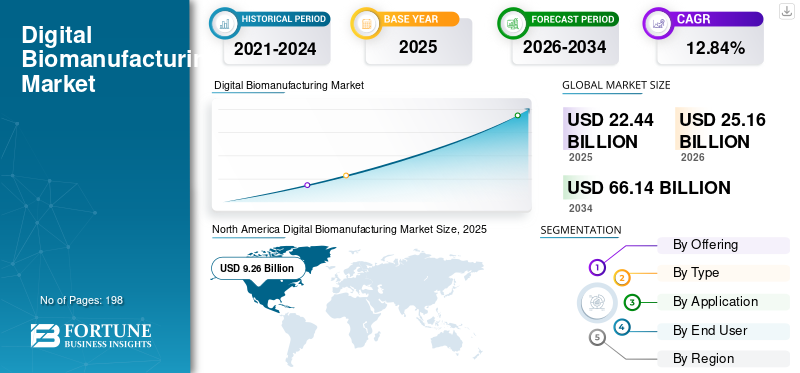

The global digital biomanufacturing market size was valued at USD 22.44 billion in 2025. The market is projected to grow from USD 25.16 billion in 2026 to USD 66.14 billion by 2034, exhibiting a CAGR of 12.84% during the forecast period. North America dominated the digital biomanufacturing market with a market share of 41.27% in 2025.

Digital biomanufacturing systems are utilized to digitalize, automate, monitor, and optimize biologics manufacturing workflows across process development, scale-up, GMP production, quality control, batch release, and technology transfer. The global market is expanding as the demand for biologics, biosimilars, vaccines, cell therapies, gene therapies, and recombinant proteins is rapidly increasing. Moreover, rising adoption of single-use systems, growing CDMO outsourcing, increasing need for faster technology transfer, and the shift from paper-based batch records to connected digital workflows are supporting demand across global biomanufacturing facilities.

Key players operating in the global market include Siemens, Sartorius AG, Danaher Corporation (Cytiva), and Emerson Electric Co. These companies are focusing on portfolio expansion, technological advancements, and strategic collaborations to strengthen their market presence.

Download Free sample to learn more about this report.

DIGITAL BIOMANUFACTURING MARKET TRENDS

Shift toward Automation and Real-Time Process Control is a Major Trend Observed in Global Market

The transition to automation and immediate process management is emerging as a significant trend in the global digital biomanufacturing sector as biopharma producers depart from manual, disjointed, and paperwork-driven production methods. The production of biologics demands strict regulation of factors including pH, dissolved oxygen, temperature, feed rate, pressure, and flow, as even minor variations in the process may influence yield, purity, and the success of the batch. Consequently, firms are putting money into linked bioreactors, automated skids, DCS/SCADA systems, PAT tools, and real time monitoring platforms to enhance process reliability and lower the risk of batch failures. This trend is further backed by the necessity to link various vendor systems and manufacturing methods across developmental, clinical, and commercial-scale processes. Automation and real-time management enable manufacturers to minimize manual involvement, enhance data accuracy, speed up problem-solving, and facilitate quicker scaling. This holds particular significance for CDMOs and manufacturers of advanced therapies, where adaptable production, swift technology transfer, and immediate visibility are essential. These factors are supporting the overall global digital biomanufacturing market growth.

- For instance, in April 2026, Rockwell Automation and Cytiva together introduced the Figurate SCADA system to eliminate digital obstacles in biopharmaceutical The platform is built to operate with various instrument vendors and modalities, offering the connectivity essential for digital integration and real-time monitoring in contemporary bioprocessing.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Biologics, Biosimilars, Vaccines, and Advanced Therapy Production to Boost Market Growth

The increasing production of biologics, biosimilars, vaccines, and advanced therapies is a significant factor propelling the global market, as these products necessitate meticulously controlled, data-intensive, and compliant manufacturing settings. In contrast to traditional small-molecule production, biologics manufacturing consists of delicate upstream cell culture, downstream purification, quality control testing, batch documentation, and release processes, where minor variations can influence yield, purity, and product quality. As businesses grow their capacities for monoclonal antibodies, recombinant proteins, vaccines, cell therapies, and gene therapies, they require MES/eBR, automation, PAT, QMS/LIMS, data systems, and real-time monitoring solutions to handle process intricacy. Digital systems assist manufacturers in minimizing manual errors, enhancing batch uniformity, speeding up scale-up, facilitating technology transfer, and reinforcing regulatory documentation. This requirement is particularly intense among CDMOs, where various client processes need to be coordinated within adaptable GMP facilities. Consequently, expansion in biologics and advanced therapy pipelines directly boosts expenditure on integrated, automated, and data-oriented biomanufacturing infrastructure.

- For instance, in August 2025, WuXi Biologics announced that its WuXiUP intensified perfusion culture platform achieved end-to-end, fully automated continuous drug substance production at pilot scale.

MARKET RESTRAINTS

High Cost of Implementation to Limit Market Growth

Significant implementation expenses serve as a limitation for the global digital biomanufacturing sector, as these initiatives necessitate considerably more than just acquiring software. Businesses need to invest in MES/eBR setup, automation integration, PAT deployment, data transfer, equipment linkage, cybersecurity, validation, employee training, and ongoing support. In GMP settings, all digital workflows are required to comply with stringent documentation, audit trail, data integrity, and validation standards, leading to increased project time and expenses. Smaller biopharma firms, academic GMP facilities, and local producers might postpone adoption since the initial investment can be hard to validate prior to large-scale production. Connecting with outdated equipment and systems from various vendors adds to expenses, particularly when facilities utilize older bioreactors, skids, historians, LIMS, and QMS platforms. Consequently, numerous firms embrace digital biomanufacturing gradually rather than launching complete end-to-end digital systems simultaneously, hindering immediate market penetration.

MARKET OPPORTUNITIES

Regulatory and Policy Support for Advanced Manufacturing to Offer Lucrative Opportunities for Market Growth

Regulatory and policy support for advanced manufacturing is creating a strong opportunity for the global market, as manufacturers are being encouraged to adopt technologies that improve process reliability, product quality, and supply continuity. Digital biomanufacturing tools such as automation platforms, PAT, digital twins, robotics, MES/eBR, and real-time monitoring systems directly support these goals by reducing manual variability and improving process control. As regulators provide clearer pathways for advanced manufacturing technologies, biopharma companies and CDMOs have stronger confidence to invest in digitally enabled production systems. This is especially important for cell and gene therapies, biologics, and complex medicines where manufacturing consistency and scalability are major challenges. Regulatory support can also shorten development timelines and improve inspection readiness, making digital transformation more commercially attractive. Therefore, companies that develop validated, automated, and digitally connected manufacturing platforms are likely to benefit from faster adoption and stronger customer demand. All these factors would drive the market growth in the coming years.

- For instance, in April 2025, Cellares announced that its Cell Shuttle received the U.S. FDA’s Advanced Manufacturing Technology designation from CBER for automated cell therapy manufacturing.

MARKET CHALLENGES

Shortage of Skilled Digital Biomanufacturing Professionals Pose a Prominent Challenge to Market Growth

The lack of qualified digital biomanufacturing experts poses a significant challenge since the industry needs individuals who are proficient in both GMP bioprocessing and sophisticated digital systems. Digital biomanufacturing initiatives require experts in MES/eBR, automation, PAT, data integration, AI/ML, digital twins, validation, cybersecurity, and quality informatics; however, these abilities are frequently distributed among various teams. This slows down implementation, heightens reliance on external system integrators, and escalates project expenses for biopharma firms and CDMOs. The difficulty is greater in medium-sized businesses and developing areas, where attracting and keeping digital-bioprocessing professionals is more challenging. Even when firms acquire sophisticated systems, a lack of internal expertise can hinder configuration, validation, user training, and complete adoption. Consequently, the labor shortage may slow down the rate at which businesses translate digital investments into tangible manufacturing enhancements. All the factors cumulatively affect the market growth.

- For instance, in September 2025, JobsOhio, in partnership with the Ohio Life Sciences Association and One Columbus, announced a biomanufacturing workforce initiative to train people for operator and technician roles in pharmaceutical manufacturing and biotechnology.

Segmentation Analysis

By Offering

Hardware & Connected Equipment Segment Dominated Due to High Capital Spending on Connected Bioprocessing Infrastructure

In terms of offering, the market is divided into services, software & platforms, and hardware & connected equipment.

The hardware & connected equipment segment led the global digital biomanufacturing market share in 2025. As digital biomanufacturing depends heavily on connected physical infrastructure such as automated bioreactors, single-use systems, and others. The segment is also supported by rising biologics, biosimilars, vaccine, and cell and gene therapy manufacturing capacity, where new facilities require digitally integrated upstream and downstream systems. Compared with software licenses or services, connected bioprocessing equipment carries higher upfront capital value, which keeps this segment dominant in sales-based market share.

- For instance, in April 2025, Culture Biosciences launched Stratyx 250, described as the first cloud-integrated mobile bioreactor for cell culture process development. The system provides flexibility, automation, and remote process control, showing how connected equipment is becoming central to modern digital biomanufacturing workflows.

The services segment is anticipated to rise with a CAGR of 14.61% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type

Automation & Process Control Segment Dominated Due to Need for Consistent, Real-time Control of Biomanufacturing Operations

Based on type, the market is classified into manufacturing execution & electronic batch records, automation & process control, process analytical technology & real-time monitoring, digital twins, modeling & simulation, AI, machine learning & advanced analytics, bioprocess data management & integration, quality & laboratory informatics, and others.

The automation & process control segment accounted for the dominant market share in 2025. The segment's leadership is due to the fact that biologics manufacturing requires continuous control of critical parameters such as pH, dissolved oxygen, temperature, agitation, pressure, flow rate, and feed strategy. These systems are essential across upstream cell culture, downstream purification, filtration, chromatography, and fluid-management workflows, where small deviations can affect yield, purity, and batch consistency. The segment also benefits from the expansion of biologics, biosimilars, vaccines, and cell and gene therapy facilities, where automation is usually the first digital layer deployed before advanced analytics and digital twins. Furthermore, the segment is set to hold 26.7% of market share in 2026.

- For instance, in May 2025, Emerson introduced an expanded life sciences software suite within its DeltaV Automation Platform to improve seamless data mobility across the development and commercialization pipeline.

The AI, machine learning & advanced analytics segment is anticipated to rise with a CAGR of 20.89% over the forecast period.

By Application

Commercial GMP Manufacturing Execution Segment Dominated Due to Need for Compliant Batch Execution and Paperless Production Workflows

On the basis of application, the market is divided into process development & scale-up, commercial GMP manufacturing execution, real-time process monitoring & control, quality management & batch release, technology transfer & facility digitalization, and others.

In 2025, the market share was primarily led by the commercial GMP manufacturing execution segment. The segment’s leadership is supported by rising commercial-scale production of monoclonal antibodies, vaccines, biosimilars, and advanced therapies, where batch consistency and inspection readiness are critical. Therefore, recurring use across large GMP facilities and direct linkage with compliant production operations keep commercial GMP manufacturing execution as the leading application segment. Furthermore, the segment is set to hold 27.1% of market share in 2026.

- For instance, in May 2025, BioPhorum published its “Advancing MES solutions for biomanufacturing: Manifesto progress report 2025,” which emphasized advancements in MES solutions for biomanufacturing facilities and the necessity of tackling deployment, configuration, integration, and support issues in tightly regulated manufacturing settings. This highlights the increasing significance of MES-driven commercial GMP implementation in biomanufacturing plants.

The technology transfer & facility digitalization segment is anticipated to rise with a CAGR of 20.41% over the forecast period.

By End User

Pharmaceuticals & Biotechnology Companies Segment Led Market Due to Strong In-house Biologics Manufacturing and Digital Capacity Expansion

Based on end user, the market is segmented into pharmaceuticals & biotechnology companies, academic & research institutes, CMOs & CDMOs, and others.

The pharmaceuticals & biotechnology companies segment dominated the market share in 2025. The dominance of the segment is attributed to the fact that these companies invest heavily in digital biomanufacturing products & services to improve batch consistency, regulatory readiness, and supply reliability. Moreover, in-house manufacturers also need digital tools to support complex product pipelines, high-value biologics portfolios, multi-site production networks, and faster scale-up from development to commercial manufacturing. All these factors drive the segmental growth over the projected period. Furthermore, the segment is set to hold 57.2% of market share in 2026.

- For instance, in August 2025, Genentech and Roche broke ground on a state-of-the-art manufacturing facility in Holly Springs, North Carolina, which is expected to incorporate modern biomanufacturing technologies along with advanced automation and digital capabilities.

In addition, CMOs & CDMOs are projected to witness 15.60% growth rate during the forecast period.

Digital Biomanufacturing Market Regional Outlook

Based on region, the global market is divided into Asia Pacific, Latin America, Europe, North America, and the Middle East & Africa.

North America

North America Digital Biomanufacturing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America’s market was valued at USD 8.24 billion in 2024 and dominated the global market. In 2025, the region maintained its leading position, with USD 9.26 billion. The regional growth is driven by extensive network of commercial biologics, vaccines, biosimilars, cell therapies, and gene therapy production sites, particularly in the U.S. Moreover, this region shows significant use of MES/eBR, automation, PAT, QMS/LIMS, digital twins, and AI-driven process analytics as producers emphasize batch uniformity, quicker scaling, and compliance preparedness.

U.S. Digital Biomanufacturing Market

The U.S. market led the North American region and is projected to be approximately valued at USD 9.42 billion in 2026, representing about 37.5% of the global market.

Europe

Europe’s market is growing at a CAGR of 11.63% during the forecast period. Europe’s growth is driven by its established biologics manufacturing base across European countries, strong demand for digital manufacturing systems, and supportive regulatory policies.

U.K. Digital Biomanufacturing Market

The U.K. market is estimated to be valued at around USD 1.10 billion in 2026, representing roughly 4.4% of global revenues.

Germany Digital Biomanufacturing Market

Germany’s market is projected to reach approximately USD 1.43 billion in 2026, equivalent to around 5.7% of global sales.

Asia Pacific

The Asia Pacific’s market size is expected to reach a valuation of USD 5.70 billion by 2026. The region is projected to experience the highest growth driven by the quick development of biologics, biosimilars, vaccines, and CDMO production capabilities in China, India, South Korea, Singapore, Japan, and Australia. The area is shifting from cost-effective production to intricate biologics and advanced therapies, enhancing the demand for automation, interconnected devices, digital batch records, PAT, and bioprocess data systems.

Japan Digital Biomanufacturing Market

The Japanese market is estimated to be valued at around USD 1.27 billion in 2026, accounting for roughly 5.1% of global revenues.

China Digital Biomanufacturing Market

China’s market is projected to reach revenues of around USD 2.03 billion in 2026, representing roughly 8.1% of global sales.

India Digital Biomanufacturing Market

The Indian market is estimated to be valued at around USD 0.82 billion in 2026, accounting for roughly 3.2% of global revenues.

Latin America and Middle East & Africa

The growth in the Middle East & Africa and Latin America regions is anticipated to be moderate in the coming years. Key factors such as rising local biologics, biosimilar, vaccine, and fill-finish manufacturing activity, focus on reducing import dependence, government-backed healthcare manufacturing localization, and increasing investments in pharmaceutical & biotechnology infrastructure are expected to boost the market growth in these regions. The Latin America’s market is estimated to be valued at around USD 1.38 billion in 2026.

GCC Digital Biomanufacturing Market

The GCC market is projected to reach approximately USD 0.44 billion by 2026, representing about 1.8% of industry revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated Automation, MES, and Data Platforms to Support Key Players’ Market Positions

The global digital biomanufacturing market reflects a moderately fragmented market competitiveness, with prominent players such as Siemens, Sartorius AG, Danaher Corporation (Cytiva), Emerson Electric Co., and Rockwell Automation accounting for a significant portion of market revenue. Broad portfolios of these companies, strong focus on integrated platforms, and wide geographic presence are some of the factors supporting the leading position of these companies in the global market.

- For instance, in April 2025, Sartorius Stedim Biotech entered into a strategic partnership with Tulip Interfaces to develop digital manufacturing applications for biomanufacturing visibility and optimization. The partnership focuses on combining Sartorius’ bioprocessing expertise with Tulip’s frontline operations technology to support digital transformation in single-use bioprocessing, reduce process variability, and improve regulatory compliance.

Other significant participants include Körber AG, Aspen Technology, Benchling, TetraScience, Inc., and Schneider Electric. These firms are also emphasizing cloud based MES deployment, SCADA connectivity, PAT integration, AI-enabled process analytics, and quality/lab informatics expansion to improve manufacturing efficiency, accelerate technology transfer, and support enterprise-wide digital biomanufacturing adoption.

LIST OF KEY DIGITAL BIOMANUFACTURING COMPANIES PROFILED

- Siemens (Germany)

- Sartorius AG (Germany)

- Danaher Corporation (Cytiva) (U.S.)

- Emerson Electric Co. (U.S.)

- Körber AG (Germany)

- Aspen Technology (U.S.)

- Benchling (U.S.)

- TetraScience, Inc. (U.S.)

- Schneider Electric (France)

KEY INDUSTRY DEVELOPMENTS

- January 2026: WuXi Biologics launched PatroLab, a digital twin platform for bioprocess development and manufacturing. The platform combines real-time process monitoring, Raman-based PAT, and predictive in-silico modeling to improve process control, reduce process risk, and support consistent biologics manufacturing.

- November 2025: TetraScience and Bayer expanded their partnership to advance scientific data management. Bayer is expanding deployment of TetraScience’s Scientific Data Foundry across pharmaceutical and crop science R&D operations.

- October 2025: Thermo Fisher Scientific Inc. showcased enhanced Accelerator Drug Development capabilities and a strategic collaboration with OpenAI at CPHI Frankfurt 2025.

- October 2025: Benchling unveiled new capabilities at Benchtalk 2025, including Benchling AI and automated data-analysis capabilities for biotech workflows.

- September 2025: Merck and Siemens deepened their strategic partnership to accelerate AI and data-driven drug development and manufacturing. The collaboration focuses on digital-first solutions to close workflow gaps in drug discovery and biomanufacturing by integrating Merck’s SaaS products with Siemens’ digital ecosystem.

REPORT COVERAGE

The global digital biomanufacturing market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. The global market report provides understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.84% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Type, Application, End User, and Region |

| By Offering |

|

| By Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 22.44 billion in 2025 and is projected to reach USD 66.14 billion by 2034.

In 2025, the North America’s market value stood at USD 9.26 billion.

The market is expected to exhibit a CAGR of 12.84% during the forecast period of 2026-2034.

By offering, the hardware & connected equipment segment is expected to lead the market.

Rising demand for biologics & biosimilars, growing need for GMP compliance and paperless batch documentation and increasing focus on process intensification and manufacturing efficiency are primarily driving market expansion.

Siemens, Sartorius AG, Danaher Corporation (Cytiva), and Emerson Electric Co. are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us