Digital Twin in Healthcare Market Size, Share & Industry Analysis, By Offering (Software and Services), By Type (Process Twins, System Twins, Whole Body Twins, and Others), By Application (Personalized Medicine, Workflow Optimization & Capacity Management, Medical Device Design, Testing & Validation, Surgical Planning, Medical Education & Training, and Others), By Therapeutic Area (Cardiovascular Disorders, Metabolic Disorders, & Other Disorders), By End User (Pharmaceutical and Biotechnology Companies, Medical Device Manufacturers, and Others), and Regional Forecast, 2026-2034

Digital Twin in Healthcare Market Overview

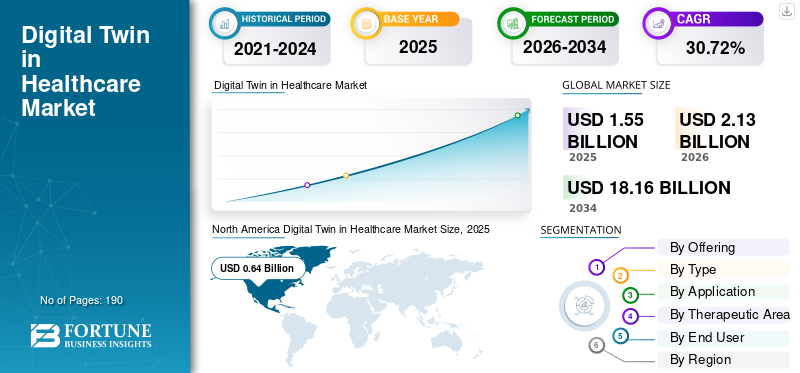

The global digital twin in healthcare market size was valued at USD 1.55 billion in 2025. The market is projected to grow from USD 2.13 billion in 2026 to USD 18.16 billion by 2034, exhibiting a CAGR of 30.72% during the forecast period. North America dominated the digital twin in healthcare market with a market share of 41.29% in 2025.

The global digital twin in healthcare market is expected to grow steadily in the coming years, driven by the rising need for more precise, data-driven, and efficient healthcare delivery to improve patient care. Digital twin technology creates virtual models of patients, organs, hospital operations, or medical systems using real-world clinical, imaging, and operational data. Such data helps healthcare providers, life sciences companies, and medical device manufacturers test scenarios before making clinical decisions. As healthcare systems continue to focus on personalized treatments, predictive analytics, and operational efficiency, the demand for digital twin platforms and related services is increasing across the market. Companies are also investing in virtual twin technology for disease modeling, organ simulation, and hospital optimization, further supporting market expansion.

- For instance, in February 2025, Dassault Systèmes launched the next phase of its Living Heart initiative, expanding the use of virtual twin technology in healthcare and exploring broader applications across additional organs to address wider medical challenges.

Leading healthcare industry players, such as Symplr, Quest Analytics, Availity, and HiLabs, are expanding their offerings to boost their market position.

Download Free sample to learn more about this report.

Digital Twin in Healthcare Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.55 Billion

- 2026 Market Size: USD 2.13 Billion

- 2034 Forecast Market Size: USD 18.16 Billion

- CAGR: 30.72% from 2026–2034

- North America dominated the digital twin in healthcare market with a 41.29% share in 2025.

- The body part twins segment accounted for the largest share of the market in 2025.

- The personalized medicine segment accounted for the largest share of the market in 2025.

North America

North America generated USD 0.64 billion in 2025, driven by digital health adoption and healthcare IT investments.

Europe

Europe is projected to reach USD 0.54 billion in 2026, driven by organ modeling and precision medicine research.

Asia Pacific

Asia Pacific is projected to reach USD 0.51 billion in 2026, driven by healthcare digital transformation and care delivery improvements.

U.S.

The digital twin in healthcare market is projected to reach USD 0.80 billion in 2026.

Japan

The digital twin in healthcare market is projected to reach USD 0.11 billion in 2026.

Read More

DIGITAL TWIN IN HEALTHCARE MARKET TRENDS

Elevating Use of Digital Twins in Personalized Medicine is Emerging as a Key Market Trend

The global digital twin in healthcare market is increasingly moving toward more personalized, predictive models of care. Digital twin technology helps create virtual models of individual patients, organs, or disease pathways by combining clinical data, biomarkers, and real-time health information. As a result, healthcare providers can test treatment pathways, predict responses, and support more tailored care decisions before applying them in the real world. This improves clinical precision, supports better patient outcomes, and increases confidence in data-driven treatment planning. Due to these advantages, the growing use of digital twins in personalized medicine is emerging as a major trend, supporting the market's expansion.

- For instance, in August 2025, Twin Health received an investment of USD 53.0 million to accelerate the company’s expansion among health plans in retail, healthcare, financial services, and technology.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Healthcare Digitalization to Drive Market Growth

The broader digitalization of healthcare systems across hospitals, clinics, and life sciences organizations is driving the global digital twin in healthcare market growth. As healthcare providers continue to adopt connected devices, digital records, cloud platforms, AI tools, and real-time data systems, the foundation for digital twin deployment becomes much stronger. Digital twins depend on continuous data inputs, interoperability, and digital workflows to create accurate virtual models of patients, assets, and care pathways. As a result, healthcare organizations are becoming more capable of using digital twins to test scenarios, improve resource planning, support clinical decisions, and enhance operational efficiency. As digitalization in healthcare is improving data availability and system connectivity, it is driving a stronger demand for digital twin platforms across the market.

Moreover, key companies are focusing on regulatory approvals and new product launches to strengthen their market position.

- For instance, in November 2023, GE HealthCare launched the Genesis portfolio as part of its cloud strategy. This development supported its plans to strengthen its cloud-enabled offerings and the adoption of digital innovation in healthcare. Such developments are important for the market as expanding cloud-based and connected digital infrastructure makes it easier for healthcare organizations to deploy advanced digital twin platforms for workflow simulation, capacity planning, and data-driven decision-making.

MARKET RESTRAINTS

High Implementation and Integration Costs to Limit Market Growth

The global digital twin in healthcare market faces a key restraint of high implementation and integration costs. These digital twin solutions require strong digital infrastructure, continuous data flow, cloud capacity, advanced analytics, and integration with hospital systems such as EHRs, imaging platforms, and connected devices. Due to these factors, healthcare organizations often need to make large upfront investments in technology, data management, and specialized talent before they can use these platforms at scale. This increases the financial burden on hospitals and other end users, especially those working with limited IT budgets or fragmented legacy systems. As a result, many providers adopt digital twin solutions slowly, which slows broader market growth.

- For instance, in January 2026, MedCity News highlighted that healthcare innovation continues to face integration-related barriers, with disconnected systems and infrastructure gaps slowing the practical deployment of advanced digital solutions. This reflects a key restraint for digital twin adoption, as these platforms require seamless integration with existing healthcare IT environments to scale effectively.

MARKET OPPORTUNITIES

Rising Use of Remote Monitoring and Connected Health Data is Creating New Opportunities for Digital Twin Platforms

A major growth opportunity for this market is the rising use of remote monitoring and connected devices, especially as more healthcare systems adopt wearable devices, smartphone-linked tools, home-based monitoring solutions, and connected care platforms. The volume of real-time patient data available for analysis is increasing. As digital twins rely on continuous, dynamic data inputs to better reflect patient conditions, this trend makes digital twin models more practical and valuable in real-world healthcare settings. As a result, companies can use digital twins more effectively for early-risk detection, disease progression tracking, personalized intervention, and ongoing care optimization. This creates a strong opportunity for market growth, especially as healthcare providers shift toward preventive, decentralized, and data-enabled care delivery.

- For instance, in July 2025, Medtronic announced a renewed multi-year partnership with Philips to expand access to patient monitoring technology. This development is important for the market as the wider deployment of connected monitoring technologies increases the flow of real-time patient data, strengthening the foundation for digital twin platforms in healthcare. As connected monitoring ecosystems expand, they are expected to create stronger commercial opportunities for digital twin adoption across hospitals and broader care settings.

MARKET CHALLENGES

Limited Clinical Validation and Complex Workflow Integration to Challenge Product Adoption

The global digital twin in healthcare market is growing, but it still faces a major challenge in transitioning from pilot projects to broad real-world deployment. Digital twin platforms need accurate clinical data, strong interoperability, and clear alignment with day-to-day healthcare workflows to deliver reliable results. Due to this, healthcare providers often require more evidence that these models can work consistently across different care settings, patient populations, and hospital systems. Moreover, integrating digital twins into existing clinical and operational workflows can be difficult when data systems are fragmented or legacy infrastructure is still in place. As a result, adoption often lags expectations, creating a significant challenge to broader market expansion.

- For instance, in January 2026, Medallion released its 2026 State of Payer Enrollment and Medical Credentialing Report, which described a widening operational crisis in healthcare, stating that credentialing and enrollment delays are increasingly tied to revenue leakage, rising provider churn, and burnout across the healthcare ecosystem. This highlights how prolonged onboarding and enrollment cycles continue to create friction in provider network operations, making them a clear challenge for the market.

Segmentation Analysis

By Offering

Software Segment Led due to Primary Investment Priority of Buyers

Based on offering, the market is categorized into software and services.

The software segment dominated the market, as digital twins are primarily adopted on simulation platforms, cloud-based planning tools, analytics engines, and workflow orchestration systems. These software layers are the core of the value proposition, since they convert raw healthcare data into usable models for prediction, planning, testing, and decision-making. As buyers first invest in the platform that creates and runs the twin, software is likely to account for the largest share of the market. In addition, healthcare organizations prefer scalable software environments that can be updated, integrated, and expanded across multiple use cases over time. This makes software the main commercial layer through which digital twin capabilities are delivered and monetized in the market.

- For instance, in March 2025, GE HealthCare highlighted the expansion of its Genesis cloud portfolio to improve digital innovation adoption and care coordination. Such software-focused expansion supports the view that software remains the leading revenue-generating layer in this market.

The services segment is expected to grow at a CAGR of 32.33% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type

Body Part Twins Segment Dominated, Driven by its Ability to Integrate into a Clinical Workflow

Based on type, the market is segmented into process twins, system twins, whole-body twins, body-part twins, and others.

In 2025, the body part twins accounted for the largest share of the market. Healthcare providers and technology developers are witnessing stronger commercial traction for organ- and anatomy-specific models than for full whole-body twins. A focused twin of the heart, brain vasculature, or another anatomical structure is easier to validate, integrate into a clinical workflow, and link more directly to a specific intervention or care decision. As these models solve a clearly defined problem and require less complexity than a full-body representation, they are being adopted faster in real-world settings. They also offer more immediate value in procedure planning, device interaction analysis, and patient-specific modeling; as a result, body part twins are more commercially feasible within the type segment.

- For instance, in February 2025, Dassault Systèmes announced the next phase of its Living Heart Project, featuring AI-powered virtual twins and a customizable whole-heart simulation. This type of progress in heart-specific modeling shows that body-part twins are advancing more quickly than broader whole-body models.

The others segment is projected to grow at a CAGR of 31.80% during the forecast period.

By Application

Personalized Medicine Segment Led Owing to Rising Use of AI-based Analytics

Based on application, the market is segmented into personalized medicine, workflow optimization & capacity management, medical device design, testing & validation, drug discovery & development, surgical/interventional planning, medical education & training, and others.

Personalized medicine accounted for the largest share of the market. Digital twin technology is increasingly being used to create patient-specific models that help predict disease progression, treatment response, and care outcomes more accurately. This gives healthcare providers and technology companies a stronger reason to invest in digital twin platforms where the value is directly linked to better clinical decision-making and more individualized treatment pathways. In addition, the growing use of real-time patient data, biomarkers, imaging, and AI-based analytics is making personalized digital twin models more practical in real-world settings. Due to this, personalized medicine is emerging as the most commercially important application area in the market.

- For instance, in August 2025, Twin Health announced the publication of results from a Cleveland Clinic-led study in NEJM Catalyst, stating that its AI Precision Treatment significantly improved outcomes in type 2 diabetes and reduced reliance on costly medications. Such development shows how digital twin-based personalized care models are moving beyond theory and generating measurable clinical outcomes in real-world use.

The drug discovery & development segment is projected to grow at a CAGR of 31.94% over the study period.

By Therapeutic Area

Cardiovascular Disorders Segment Dominated due to Stronger Ecosystem Support from Medtech Companies

Based on therapeutic area, the market is segmented into cardiovascular disorders, metabolic disorders, orthopedic disorders, and other disorders.

The cardiovascular disorders segment held the dominant digital twin in healthcare market share. The segment dominated as the heart and vascular system are among the earliest and most commercially advanced areas for digital twin use in healthcare. Structural heart interventions, valve planning, cardiovascular device simulation, and patient-specific procedural modeling already have visible market activity and specialized platforms. As cardiovascular care involves high-risk procedures, complex anatomy, and strong demand for pre-procedural planning, digital twins deliver immediate clinical and economic value. In addition, cardiovascular applications already have stronger ecosystem support from medtech companies, simulation developers, and clinical specialists compared with many other disease areas. This is helping cardiovascular use cases move faster from the innovation stage to practical adoption, which is why they are likely to hold the leading share within the therapeutic segmentation.

- For instance, in January 2024, FEops announced clinical utility data in the U.S. showing that its AI-enabled predictive pre-planning improved procedural efficiency for left atrial appendage occlusion. Such evidence supports the view that cardiovascular use cases are at the forefront of real-world digital twin adoption in healthcare.

The metabolic disorders segment is projected to grow at a CAGR of 32.07% over the study period.

By End User

Increasing Demand in Hospitals Boosted the Healthcare Payers and Providers Segment Growth

Based on end user, the market is segmented into pharmaceutical and biotechnology companies, medical device manufacturers, healthcare payers & providers, and others.

The healthcare payers and providers segment dominated the market. They are the primary users of digital twin technology in real-world healthcare delivery and operational planning. Digital twin platforms are increasingly being used by hospitals and health systems to simulate patient flow, improve capacity management, optimize staffing, and support more informed clinical and administrative decisions. As a result, healthcare payers and providers are likely to account for the largest share of the market, since they can apply digital twin solutions directly across hospital operations, care pathways, and service planning.

- For instance, in November 2025, Siemens Healthineers AG launched ActExcell Operational Twin, a solution designed to simulate complex scenarios and recommend operational improvements in hospital departments and broader healthcare environments.

The pharmaceutical and biotechnology companies segment is projected to grow at a CAGR of 31.31% over the study period.

Digital Twin in Healthcare Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Digital Twin in Healthcare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.47 billion and maintained its leading position in 2025 at USD 0.64 billion. The market is growing in the region strongly due to its relatively mature digital health foundation, high healthcare IT spending, and a stronger push toward interoperability and data exchange. As more providers connect records, imaging, and operational systems through standards-based infrastructure, digital twin platforms become easier to deploy for hospital operations, care planning, and advanced analytics.

U.S. Digital Twin in Healthcare Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.80 billion by 2026, accounting for roughly 37.47% of the global market sales.

Europe

Europe is projected to grow at 29.72% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.54 billion by 2026. Europe has strong activity in organ modeling, medical simulation, and precision medicine research, which is helping the market move from academic development toward broader clinical and commercial use.

U.K. Digital Twin in Healthcare Market

The U.K. market is estimated at around USD 0.11 billion by 2026, representing roughly 5.34% of the global market.

Germany Digital Twin in Healthcare Market

Germany's market is projected to reach approximately USD 0.12 billion by 2026, equivalent to around 5.75% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.51 billion by 2026 and secure the position of the third-largest region in the market. Asia Pacific is growing as healthcare systems across the region are rapidly expanding digital transformation efforts to improve access, efficiency, and long-term care delivery.

Japan Digital Twin in Healthcare Market

The Japanese market is estimated at around USD 0.11 billion by 2026, accounting for approximately 5.11% of the global market.

China Digital Twin in Healthcare Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated to reach around USD 0.16 billion, representing approximately 7.30% of global sales.

India Digital Twin in Healthcare Market

The Indian market is estimated at around USD 0.05 billion by 2026, accounting for roughly 2.39% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.11 billion by 2026, driven by the ongoing modernization of hospital infrastructure and improved digital health connectivity. In the Middle East & Africa, the GCC is set to reach USD 0.05 billion by 2026.

South Africa Digital Twin in Healthcare Market

The South African market is projected to reach approximately USD 0.02 billion by 2026, accounting for roughly 0.91% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Emphasize New Product Launches to Strengthen Their Market Position

The global digital twin in healthcare market is highly consolidated, with companies such as Symplr, Quest Analytics, Availity, Synopsys, Inc., HiLabs, LexisNexis Risk Solutions, and HealthStream holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in March 2026, Synopsys, Inc. launched the Synopsys Electronics Digital Twin (eDT) Platform, an open solution to accelerate the creation, management, deployment, and use of electronics digital twins (eDTs) for product development, enabling physical AI systems.

Other notable players in the global market include Newgen Software Technologies Limited, CitiusTech, and Kyruus Health. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY DIGITAL TWIN in HEALTHCARE COMPANIES PROFILED

- Symplr (U.S.)

- Quest Analytics (U.S.)

- Availity (U.S.)

- HiLabs (U.S.)

- LexisNexis Risk Solutions (U.S.)

- HealthStream (U.S.)

- Verisys (U.S.)

- Newgen Software Technologies Limited (India)

- CitiusTech (U.S.)

- Kyruus Health. (U.S.)

- Synopsys, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Kyndryl launched the Kyndryl Digital Twin for the Workplace, a new AI-powered capability designed to help organizations avoid workflow disruption by anticipating and resolving technology issues. The solution is built on Microsoft Foundry and combines predictive intelligence, automation, and operational insight to improve the employee experience through automated IT service operations.

- February 2026: OUTSCALE, a Dassault Systèmes brand, partnered with Cerba HealthCare to develop “OUTSCALE Healthcare Sovereign Platform,” a healthcare patient journey solution.

- October 2025: Twin Health partnered with Peloton, the industry leader in connected fitness and wellness content and equipment. The partnership enabled Twin Health members to access Peloton’s expansive library of live and on-demand fitness classes, spanning cardio, strength training, yoga, meditation, and more. The AI Digital Twin recommends specific Peloton content that would help members achieve their metabolic health goals.

- October 2024: Dassault Systèmes launched a guide for the medical device industry that outlines how to use virtual twins to accelerate clinical trials. The guide was published following the successful completion of a five-year collaboration with the U.S. FDA.

- September 2023: Dassault Systèmes launched “Emma Twin,” an avatar designed to raise awareness of the key role virtual twins play in advancing healthcare and the innovations shaping the future of medicine.

REPORT COVERAGE

The report provides a detailed global analysis of the digital twin in healthcare market across key segments, including offering, type, application, therapeutic area, and end user. It examines how digital twin technology is used in personalized medicine, workflow optimization, medical device design, drug development, and surgical planning. It assesses its growing relevance across cardiovascular, metabolic, orthopedic, and other healthcare applications. The study further covers regional market trends across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa to highlight where adoption is accelerating and why. In addition, the report evaluates major growth drivers, restraints, opportunities, and challenges influencing market expansion. It also includes a competitive landscape analysis, key company profiles, and recent developments, such as product innovations, partnerships, and strategic investments, providing a comprehensive view of the current and future market outlook.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 30.72% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Type, Application, Therapeutic Area, End User, and Region |

| By Offering |

|

| By Type |

|

| By Application |

|

| By Therapeutic Area |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.55 billion in 2025 and is projected to reach USD 18.16 billion by 2034.

In 2025, the market value stood at USD 0.64 billion.

The market is expected to grow at a CAGR of 30.72% over the forecast period.

By offering, the software segment led the market.

Growing use of digital twins in personalized medicine is the key factor driving the market.

Symplr, Quest Analytics, Availity, Inc., HiLabs, and LexisNexis Risk Solutions are the major market players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us