Digital Wound Measurement Devices Market Size, Share & Industry Analysis, By Product Type (Contact Digital Measuring Devices, Non-contact Digital Measuring Devices, and Others), By Technology (2D Imaging-Based Devices, 3D Imaging-Based Devices, Laser-Based Devices, and Others), By Wound Type (Chronic Wounds and Acute Wounds), By End-user (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Digital Wound Measurement Devices Market Size and Future Outlook

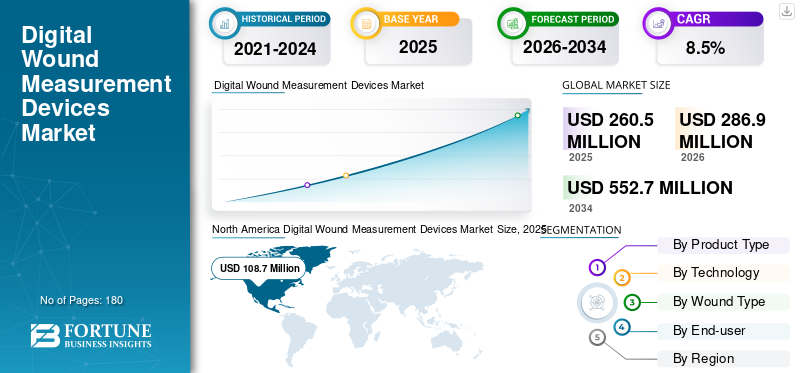

The digital wound measurement devices market size was valued at USD 260.5 million in 2025. The market is projected to grow from USD 286.9 million in 2026 to USD 552.7 million by 2034, exhibiting a CAGR of 8.5% during the forecast period. North America dominated the digital wound measurement devices market with a market share of 41.72% in 2025.

The market encompasses hardware and software-enabled systems that capture, document, and monitor wound dimensions with greater consistency than manual methods. These devices may rely on contact probes, optical imaging, 2D or 3D visualization, or laser-assisted measurement to support wound assessment across hospitals, ambulatory surgery centers, and specialty clinics. Demand is rising as wound care becomes more data-driven, and providers increasingly need visual, traceable records to support treatment planning, follow-up, and care continuity. The market is also benefiting from the growing burden of chronic wounds, especially those associated with diabetes, vascular disease, pressure injuries, and aging populations. Similarly, healthcare systems are pushing for better documentation quality, more standardized assessments, and greater workflow efficiency, all of which favor digital tools over rulers, paper notes, and subjective estimation.

Furthermore, ARANZ Medical Limited, Swift Medical Inc., MolecuLight Inc., and Net Health held the largest market share, driven by increased investments and strategic initiatives, including new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

DIGITAL WOUND MEASUREMENT DEVICES MARKET TRENDS

Shift Toward Non-Contact, Imaging-Led, and More Standardized Assessment is Reshaping the Market

A significant market trend is the movement away from purely manual or contact-based measurement toward imaging-led assessment that is faster, more repeatable, and easier to document. Non-contact systems are appealing as they align with modern infection-control practices, reduce discomfort in sensitive wounds, and produce visual records that can be reviewed later. Similarly, providers increasingly value systems that support standardization across clinicians, especially in large hospitals and multi-site wound programs. This is helping imaging-based platforms gain ground, particularly those that combine measurement with photo capture, software analysis, and structured documentation.

Another notable trend is the gradual expansion from simple dimension tracking toward broader wound assessment workflows, including depth visualization, healing progression review, and digital care coordination. As hospitals and clinics become more comfortable with technology-enabled documentation, demand is shifting from basic measurement tools to solutions that help create a more complete and defensible clinical record. That trend should continue to favor vendors whose products blend usability, consistency, and documentation strength.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Burden of Chronic and Complex Wounds is Expanding Need for Better Measurement

A major force behind market growth is the steady increase in patients living with wounds that require repeated follow-up rather than one-time evaluation. Chronic wounds are closely tied to diabetes, immobility, vascular insufficiency, and advanced age. Thus they are becoming more visible as populations age and long-term disease management becomes more demanding. In these cases, wound assessment is not just about measuring length and width once, it is about tracking progress over time, identifying delayed healing, and supporting timely changes in treatment. Digital measurement devices meet this need by helping create a visual history of the wound and reducing variation between caregivers. They are particularly valuable in settings where multiple clinicians may see the same patient over several visits. Better documentation also supports reimbursement, internal quality monitoring, and communication across care teams. As wound care pathways become more structured, providers are placing greater value on tools that improve consistency, reduce guesswork, and make it easier to showcase healing progress in day-to-day practice.

MARKET RESTRAINTS

Budget Pressure and Uneven Clinical Adoption Continue to Restrain Market Growth

Despite clear clinical value, the market still faces a practical restraint and the product adoption does not move at the same speed across all healthcare settings. Many providers remain price-sensitive, especially smaller facilities, outpatient centers with limited budgets, and institutions in cost-constrained markets. In such environments, digital wound measurement devices may be viewed as appropriate but not essential, particularly when manual tools are familiar and inexpensive.

Another barrier is workflow disruption. Even when a device improves documentation quality, clinicians may hesitate if it adds steps, requires training, or does not integrate smoothly with existing records systems. Some facilities also struggle to justify investment when case volumes are moderate or when procurement teams prioritize direct treatment devices over assessment tools. In addition, the market includes a mix of imaging, measurement, and documentation solutions, which can complicate purchasing decisions. As a result, the value proposition often needs to be proven not only in clinical terms but also in terms of time savings, reporting quality, and operational efficiency before product’s wider adoption.

MARKET OPPORTUNITIES

Digital Documentation, Telehealth, and Connected Care Can Create Significant Growth Opportunities

One of the significant opportunities in this market lies in the broader digital transformation of wound care. As providers move toward connected documentation, remote review, and more standardized care pathways, wound measurement devices can evolve from standalone tools into part of a larger clinical information ecosystem. This creates room for growth beyond the initial hardware sale. Vendors can position their offerings around image archiving, wound progression tracking, care coordination, and integration with electronic records. The opportunity is especially attractive in home-based care and post-acute settings, where consistent wound monitoring is often difficult but increasingly necessary. Publicly available U.S. data also show the scale of home health activity, underscoring the appeal of tools that can support documentation outside traditional hospital walls. Over time, solutions that make wound data easier to capture, share, and interpret across locations are likely to gain traction. Companies that combine measurement accuracy with workflow simplicity and interoperability could benefit most as healthcare providers look for tools that support both clinical decision-making and continuity of care.

MARKET CHALLENGES

Proving Clinical Value Across Diverse Care Settings Remains a Core Challenge

The market’s biggest challenge is not simply device development; it is proving consistent value across highly varied care environments. Wound care is delivered in hospitals, surgery centers, specialty clinics, long-term care facilities, and home-based settings, and each setting has different staffing models, documentation habits, and purchasing priorities. A device that works well in a specialized wound center may not be readily adopted in a general hospital ward or a resource-limited outpatient setting.

There is also the challenge of translating technical capability into measurable outcomes that matter to buyers, such as better documentation quality, smoother audits, improved oversight of healing, or more efficient staff workflows. In many cases, providers do not just need a better measurement tool as they demand a solution that fits into the way care is already delivered. That makes training, interoperability, and ease of use just as important as accuracy. Vendors that cannot simplify deployment or clearly articulate the return on investment may find that clinical interest does not always translate into broad commercial adoption.

Segmentation Analysis

By Product Type

Faster Assessment and Ease in Documentation Leads to Non-contact Digital Measuring Device Segment Dominance

Based on product type, the market is segmented into contact digital measuring devices, non-contact digital measuring devices, and others.

To know how our report can help streamline your business, Speak to Analyst

Non-contact digital measuring devices are expected to hold the highest digital wound measurement devices market share. This is due to a simple practical advantage as they allow clinicians to assess wounds without physically touching the site while also capturing images that support measurement and documentation. This matters in modern wound care, where infection control, patient comfort, and repeatable follow-up carry real weight.

Additionally, the contact digital measuring devices segment is projected to grow at a CAGR of 3.6% during the forecast period.

By Technology

2D Imaging Segment Holds Largest Share as It Balances Utility, Cost, and Ease of Use

By technology, the market is classified into 2D imaging-based devices, 3D imaging-based devices, laser-based devices, and others.

The 2D imaging-based devices accounts for the largest share of the market. Their strength lies in their practicality rather than in complexity. They give clinicians a quick way to capture wound images, estimate dimensions, and build a visual timeline without the cost and learning curve often associated with more advanced systems. Moreover, the segment is projected to hold a 50.1% share in 2026.

Additionally, the 3D imaging-based devices segment is estimated to grow at a CAGR of 12.3% during the forecast period.

By Wound Type

Chronic Wounds Dominate as They Require Repeated Monitoring Over Longer Treatment Cycles

By wound type, the market is classified into chronic wounds and acute wounds.

The chronic wounds are expected to represent the largest share of revenue. Chronic wounds demand ongoing measurement, documentation, and reassessment over weeks or months rather than a single short episode of care. Diabetic foot ulcers, pressure injuries, venous leg ulcers, and other slow-healing wounds often require serial evaluations to judge whether healing is progressing as expected. Moreover, the segment is projected to hold a 61.6% share in 2026.

Additionally, the acute wounds segment is estimated to grow at a CAGR of 7.5% during the forecast period.

By End-user

Hospitals and ASCs Holds Largest Share as They Combine Patient Volume, Infrastructure, and Procurement Capacity

On the basis of end-user, the market is classified into hospitals & ASCs, specialty clinics, and others.

Hospitals and ASCs are projected to account for the largest market share. These settings typically manage high patient volumes, broad wound case mixes, and more formal documentation requirements than smaller facilities. They also tend to have stronger procurement capabilities, better access to digital infrastructure, and a clearer pathway for integrating wound assessment tools into clinical workflows. Furthermore, the segment is set to hold 61.7% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 10.4% during the forecast period.

Digital Wound Measurement Devices Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Digital Wound Measurement Devices Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 98.8 million, reached USD 108.7 million in 2025. North America is expected to maintain a leading position in the market due to its advanced healthcare infrastructure, high adoption of medical imaging and digital documentation tools, and strong presence of wound care specialists across hospitals and outpatient settings. The region is also seeing growing demand for accurate and standardized wound assessment solutions as the burden of chronic wounds, including diabetic foot ulcers and pressure injuries, continues to rise.

U.S. Digital Wound Measurement Devices Market

In 2026, the U.S. market is forecasted to represent USD 104.7 million, capturing 36.5% of total global revenue.

Europe

Europe is expected to achieve a 7.3% growth rate in the coming years, the second-highest globally, reaching USD 80.2 million by 2026. Europe is projected to witness steady growth driven by an aging population, the rising incidence of chronic wounds, and a growing focus on improving wound care quality across institutional settings. Countries such as Germany, the U.K., and France are investing in better clinical documentation and standardized wound management practices, thereby supporting demand for digital wound measurement devices.

U.K. Digital Wound Measurement Devices Market

The U.K. market is projected to reach USD 11.2 million by 2026, accounting for 3.9% of the global market revenue.

Germany Digital Wound Measurement Devices Market

Germany's market is forecasted to reach about USD 14.3 million by 2026, representing roughly 5.0% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 56.0 million, ranking as the third-largest globally. Asia Pacific is expected to register the fastest growth during the forecast period, driven by expanding healthcare infrastructure, improved access to advanced wound care, and rising awareness of digital wound assessment tools across major healthcare sectors. Countries such as China, India, and Japan are witnessing a growing burden of diabetes and age-related chronic wounds, which is creating demand for more efficient wound monitoring solutions.

Japan Digital Wound Measurement Devices Market

Japan is projected to generate approximately USD 10.4 million in revenue by 2026, contributing nearly 3.6% to the global market.

China Digital Wound Measurement Devices Market

China’s market is forecast to reach approximately USD 15.9 million by 2026, contributing about 5.5% to global revenues.

India Digital Wound Measurement Devices Market

India is forecast to contribute approximately USD 5.8 million to the market by 2026, corresponding to about 2.0% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate digital wound measurement devices market growth, with Latin America expected to reach around USD 17.4 million by 2026. Latin America market is growing due to the gradual expansion of specialty care services, rising awareness of advanced wound management, and increasing use of digital tools in urban healthcare facilities. Brazil and Mexico are expected to remain the key contributors to regional demand, supported by improving hospital infrastructure and rising focus on chronic disease management. The Middle East & Africa market is expected to witness moderate growth, supported by ongoing healthcare modernization, rising investment in hospital infrastructure, and increasing awareness of advanced wound care technologies in selected countries. Product demand is expected to be stronger in GCC countries and South Africa, where healthcare providers are more actively adopting digital medical devices and improving specialty care capabilities.

GCC Digital Wound Measurement Devices Market

By 2026, the GCC is expected to generate approximately USD 5.9 million in the market, accounting for nearly 2.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The market is moderately fragmented and innovation-led, with competition centered less on pure scale and more on measurement accuracy, workflow integration, imaging capability, and documentation efficiency. Leading players such as ARANZ Medical Limited, Swift Medical Inc., MolecuLight Inc., Net Health, eKare, Inc., WoundVision LLC, and Kent Imaging compete through different value propositions as some companies emphasize 3D or multimodal imaging, some focus on AI-enabled mobile workflows, and others differentiate through EHR integration, billing support, or infection-control-friendly non-contact assessment.

Moreover, other key players, such as Healthy.io and Perceptive Solutions, compete through ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve procedural outcomes.

LIST OF KEY DIGITAL WOUND MEASUREMENT DEVICES COMPANIES PROFILED

- ARANZ Medical Limited (New Zealand)

- Swift Medical Inc. (Canada)

- MolecuLight Inc. (Canada)

- Net Health (U.S.)

- eKare, Inc. (U.S.)

- WoundVision LLC (U.S.)

- Kent Imaging Inc. (Canada)

- io (Israel)

- Perceptive Solutions (U.S.)

- WoundMatrix, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: MolecuLight Inc., a global medical device company pioneering point-of-care fluorescence imaging for measuring bacterial load in wounds, announced it has secured a USD 27.5 million investment from Hayfin Capital Management LLP.

- October 2024: Swift Medical launched Skin & Wound 2, a next-generation AI-based digital wound care platform with FHIR support and tighter EMR integration.

- September 2024: ARANZ released Silhouette 4.18, adding new features and expanding platform functionality.

- September 2024: Swift Medical joined the PressureSmart consortium led by Medtronic to advance AI-based pressure injury prevention and post-discharge monitoring.

- August 2024: ARANZ highlighted a trans-Tasman partnership with iAgeHealth using virtual health technologies and diagnostic devices to improve wound care for older people.

- April 2024: Wound Care Plus, LLC announced a groundbreaking partnership with ARANZ Medical to integrate ARANZ Medical’s innovative Silhouette wound assessment solution into its wound care management practice.

- March 2024: Swift Medical announced a USD 9 million AI co-investment project with DIGITAL and consortium partners to commercialize tools such as SmartTissue, AutoDepth, and HealingIndex.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.5% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product Type,Technology, Wound Type, End-user, and Region |

| By Product Type |

|

| By Technology |

|

| By Wound Type |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 260.5 million in 2025 and is projected to reach USD 552.7 million by 2034.

In 2025, the North America market value stood at USD 108.7 million.

The market is expected to exhibit a CAGR of 8.5% during the forecast period of 2026-2034.

The non-contact digital measuring devices segment led the market by product type.

The key factors driving the market are the rising burden of chronic and complex wounds.

ARANZ Medical Limited, Swift Medical Inc., MolecuLight Inc., and Net Health are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us