Advanced Wound Care Market Size, Share & Industry Analysis, By Product Type (Advanced Wound Dressings {Alginate Dressings, Hydrogel Dressings, Film Dressings, Hydrocolloid Dressings, Antimicrobial Dressings, Foam Dressings, and Others}, Wound Care Devices {Negative Pressure Wound Therapy (NPWT), Hyperbaric Oxygen Therapy), Extracorporeal Shock Wave Therapy (ESWT), and Others}, and Active Wound Care), By Indication (Diabetic Foot Ulcers, Pressure Ulcers, and Others), By End User (Hospitals, Clinics and Others), and Regional Forecast, 2026-2034

Advanced Wound Care Market Size Overview

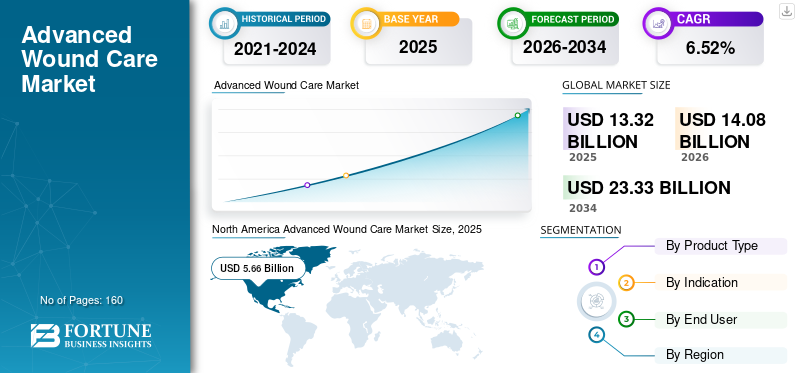

The global advanced wound care market size was valued at USD 13.32 billion in 2025 and is expected to grow from USD 14.08 billion in 2026 to USD 23.33 billion by 2034, exhibiting a CAGR of 6.52% during the forecast period 2026-2034. North America dominated the advanced wound care market with a market share of 42.52% in 2025.

Various studies estimate that around 1% to 2% of the population in developed countries will suffer from a chronic wound once in their lifetime. Besides, developing countries present a large pool of patients suffering from chronic wounds such as diabetic foot ulcers and pressure ulcers, among others. The rising number of patients undergoing surgeries globally has led to a surge in the patient population suffering from surgical wounds. A chronic wound can be classified as one that fails to progress through the phases of healing in an orderly and timely sequence and shows no significant improvement in 30 days.

In contrast, acute wounds heal quickly through the routine process of inflammation, tissue formation, and remodeling. Wound care products such as NPWT, skin grafts, and substitutes are designed exclusively to treat chronic and acute wounds.

The rising prevalence of chronic diseases, such as diabetes, limited mobility, vascular conditions, and others, increases patients' risk of developing chronic wounds. Among all wound types, diabetic foot ulcers are one of the most common types of chronic wounds affecting people across the globe. Moreover, the rising number of traumas, accidents, and surgeries leads to acute wounds. Thus, the increasing cases of chronic and acute wounds surge the demand for these products, propelling the global advanced wound care market growth in the forthcoming years.

According to an NCBI article published in 2021, approximately 310 million surgeries are performed each year across the globe. Out of these, about 40-50 million surgeries are performed in the U.S. and about 20 million in Europe.

Thus, rising surgical procedures, along with various other factors, are anticipated to propel market growth.

Countries globally had reallocated healthcare resources, such as hospital beds, nurses, essential personnel, and medical devices, to manage COVID-19 patients. This has resulted in the exemption of wound care from the essential procedures list and implementation in the elective procedures list in most countries. Healthcare facilities, including specialized wound care clinics and hospitals with dedicated advanced wound care departments, were closed with the number of beds available in these settings as they are utilized for COVID-19 patients. This has significantly impacted the number of patient visits to wound centers and outpatient departments, especially in the U.S. and European countries. However, the market regained normalcy in the post-pandemic period due to the resumption of various surgeries, an increase in patient visits, and rising demand for these products.

Download Free sample to learn more about this report.

ADVANCED WOUND CARE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 13.32 billion

- 2026 Market Size: USD 14.08 billion

- 2034 Forecast Market Size: USD 23.33 billion

- CAGR: 6.52% from 2026–2034

- North America dominated the advanced wound care market with a 42.52% share in 2025.

- Advanced wound dressings are projected to hold a 61.96% market share in 2026.

- Hospitals are expected to account for a 39.10% market share in 2026.

North America

North America generated USD 5.66 billion in 2025 and maintained its leadership due to high chronic wound prevalence and favorable reimbursement policies.

Europe

Europe reached USD 4.15 billion in 2025, supported by rising awareness of chronic wound treatment and growing product adoption.

Asia Pacific

Asia Pacific accounted for USD 1.80 billion in 2025, driven by increasing healthcare spending and investments in advanced wound management solutions.

U.S.

The market is projected to reach USD 5.29 billion in 2026, supported by a large patient pool and high wound treatment expenditures.

Japan

The market is projected to reach USD 0.49 billion in 2026, benefiting from growing demand for advanced wound care products and improved healthcare services.

Read More

Advanced Wound Care Market Trends

Shifting Focus to Introduce Active Therapies for Wound Management

Currently, patients across the globe are seeking urgent and effective treatment for chronic wounds comprising pressure ulcers, diabetic foot ulcers, and venous ulcers, among others. Active wound care products, including biological skin equivalents and growth factors, have an established and clinically proven efficiency in the treatment of hard-to-heal chronic wounds. To cater to the rising demand, the key players are shifting their focus to introduce novel bioactives in the market. For instance:

- In July 2022, Tides Medical, a biologics company, launched a tri-layer skin graft, “Artacent”, for treating complex or difficult-to-treat wounds.

- In February 2021, Axio Biosolutions received a CE mark for MaxioCel, an advanced wound dressing based on bioactive microfiber gelling for an accelerated wound healing process.

Similarly, AI-integrated treatments for wound healing have also gained traction in recent years. Artificial intelligence uses near-field sensing technology that provides sufficient data to assist in making treatment decisions and evaluating the efficacy of drugs in wound care.

- For instance, as per the data published by the National Center for Biotechnology Information in May 2022, artificial intelligence can predict tissue regeneration by connecting intelligent wearable sensors with advanced wound dressing bandages.

Thus, the launch and approval of next-generation active wound care products by various players have been instrumental in boosting the adoption of skin grafts, collagen dressings, and other active therapies. This factor is anticipated to support the growth of the market during the advanced wound care market forecast period.

Download Free sample to learn more about this report.

Advanced Wound Care Market Growth Factors

Rising Prevalence of Chronic and Acute Wounds to Fuel Demand for Dressings and Devices

The increasing prevalence of chronic wounds, such as diabetic foot ulcers, venous leg ulcers, and acute wounds, including surgical, and traumatic wounds globally, is expected to increase the number of patients undergoing treatment for chronic wounds. Moreover, the increasing burden of chronic disorders among the old-age population and the rising number of accidents are the major factors leading to an increase in the population suffering from various wounds, aiding the market growth.

According to the World Health Organization (WHO) 2022 report, the number of people over 60 years old will increase from 1 billion in 2020 to 2.1 billion by 2050.

- Additionally, as per WHO 2022, 20 million – 50 million people suffer from non-fatal injuries due to road crash traffic.

Also, the launch of technologically advanced products with better wound healing properties compared to traditional wound care products is expected to bolster the market growth.

- For instance, in October 2023, DuPont announced the launch of its new DuPont Liveo MG 7-9960 Soft Skin Adhesive. This low-cyclic silicone soft skin adhesive (SSA) is designed for advanced wound care dressings and adhering medical devices to the skin for long wear time and gentle removal.

- Similarly, in August 2022, 3M made some advancements in 3M Veraflo Therapy (negative pressure wound therapy system with instillation) for faster, easier, less painful dressings.

RESTRAINING FACTORS

High Cost Associated with Devices and Active Therapies to Limit their Adoption

Despite higher prevalence of chronic and acute wounds globally, certain factors are limiting the market growth. Among them is the high cost associated with advanced wound products and limited reimbursement for these products in emerging countries. According to an economic analysis between wound dressings and NPWT, the average cost of NPWT pumps in the U.S. is around USD 90, while that of wound dressing is around USD 3.

Although various studies have demonstrated that the overall cost of treatment by wound dressings is comparatively higher (estimated at USD 350) than NWPT (estimated at USD 200) per person, these costs are higher when compared to traditional wound dressings. The cost of treatment is higher for advanced wound care devices, including negative pressure wound therapy and skin grafts, and the cost escalates as the wound progresses from acute to chronic.

In addition, chronic wounds affect more than 40.0 million patients globally and represent a severe growing burden for the healthcare systems, with yearly costs estimated to exceed USD 15.00 billion by 2022.

- For instance, as per the data published by Engineered Regeneration in June 2022, in Europe, 4.0 million patients suffer from chronic wounds per year, requiring 25%–50% of acute hospital beds. Furthermore, costs associated with chronic wound treatments represent at least 4.0% of the national annual budget.

Also, the lack of adequate reimbursement policies, especially in emerging countries, has limited the adoption of products and devices. A significant proportion of the overall cost of treatment in emerging countries is out-of-pocket cost, which further limits the uptake of advanced wound dressings and devices for treating chronic wounds. Considering the above factors, people in these regions prefer traditional wound care products to advanced ones.

Advanced Wound Care Market Segmentation Analysis

By Product Type Analysis

High Efficiency and Lower Cost to Propel Advanced Wound Dressings Demand

Based on product type, the market is segmented into advanced wound dressings, wound care devices, and active wound care. The advanced wound dressings segment is projected to dominate the market with a share of 61.96% in 2026. The lower cost of wound dressings and its high efficiency in exudate management of wounds are expected to boost its adoption. Further, the launch of new advanced wound dressing products with enhanced properties is projected to contribute to the market growth.

- For instance, in January 2023, ConvaTec Group PLC launched ConvaFoam in the U.S. The product is an advanced foam dressing with improved absorbed fluid handling, improved adhesion, and a superabsorbent layer for difficult-to-treat wounds.

The active wound care segment is likely to register a substantial CAGR during the forecast period due to increasing applications of active therapies, such as skin grafts and biologics, for treating hard-to-heal chronic wounds. The benefits associated with active dressings, such as prevention of heat loss, protein and electrolyte loss, and permitting autolytic debridement, among others are contributing to market growth. An additional factor includes increase in research & development to introduce various active wound care products.

To know how our report can help streamline your business, Speak to Analyst

However, the wound care devices segment is expected to grow at a significant CAGR during the forecast period due to the increasing number of market players engaged in introducing advanced devices such as single-use NPWT in the global market.

By Indication Analysis

Diabetic Foot Ulcers Segment Dominated the Market Owing to Higher Prevalence and High Cost of Treatment

On the basis of indication, the market is categorized into diabetic foot ulcers, pressure ulcers, surgical wounds, and others. The diabetic foot ulcers segment is projected to dominate the market with a share of 39.75% in 2026, owing to the rising prevalence of diabetes across the globe. According to various research, patients suffering from uncontrolled diabetes are at a higher risk of developing diabetic foot ulcers, further contributing to the rising demand for advanced wound care products among these patients.

- According to the International Diabetes Federation 2021 published statistics, an estimated 571 million were living with diabetes globally, which is expected to increase to 643 million and 783 million by 2030 and 2045, respectively.

- Further, as per an article published by NCBI in 2022, the prevalence of diabetic foot ulcer is approximately 6.3% across the globe.

The surgical wounds segment is anticipated to project a significant CAGR during the forecast period owing to the increase in the number of surgical procedures coupled with the increasing incidences of surgical site infections (SSI) among patients.

By End User Analysis

Rising Number of Admissions to Propel Hospitals Segment Growth

In terms of end user, the market is segmented into hospitals, clinics, homecare settings, and others. The hospitals segment is projected to dominate the market with a share of 39.10% in 2026, and is anticipated to continue its dominance. The dominance is due to increased hospital admissions of patients suffering from acute or chronic wounds.

- For instance, as per the data published by Duke-NUS, a school of the National University of Singapore, in December 2023, chronic wounds cost Singapore an estimated USD 260.6 million yearly, accounting for nearly 0.07% of its GDP. The bulk of the costs comes from hospital admissions for chronic wounds.

The clinics segment is expected to exhibit a remarkable CAGR during the forecast period due to increasing stand-alone clinics in emerging and developed countries.

Furthermore, the homecare settings segment may register substantial growth by the end of the forecast period owing to the rising preference shift of patients from hospital to homecare settings.

REGIONAL INSIGHTS

North America

North America Advanced Wound Care Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region captured 42.52% of the global market in 2025, generating USD 5.66 billion in revenue, and is projected to reach USD 6 billion in 2026. Rising prevalence of acute and chronic wounds and higher treatment costs associated with pressure ulcers, diabetic foot ulcers, and surgical wounds is expected to boost adoption. For instance, according to the Agency for Healthcare Research and Quality estimations, the total medical cost for managing pressure ulcers in the U.S. ranged from USD 9.1 to USD 11.6 billion per year. Furthermore, adequate reimbursement policies in the U.S. and Canada are responsible for North America’s dominance in the market. The U.S. market is projected to reach USD 5.29 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 4.15 billion in 2025, accounting for 31.15% share, and is expected to reach USD 4.38 billion in 2026. This is due to rising awareness regarding the availability of treatment for chronic wounds and the surging demand for these products. The UK market is projected to reach USD 0.69 billion by 2026, and the Germany market is projected to reach USD 1.27 billion by 2026.

- For instance, in February 2021, Axio Biosolutions received CE mark for its advanced wound care product MaxioCel. The solution is based on bioactive microfiber gelling technology for an accelerated wound healing process for chronic wounds such as pressure ulcers, diabetic foot ulcers, and others.

Asia Pacific

In 2025, Asia Pacific generated USD 1.8 billion, contributing 13.48% to global market revenue, and is projected to grow to USD 1.91 billion in 2026. This is on account of increasing per capita healthcare spending. In addition, market players in this region make heavy investments, which, in turn, will fuel the demand for advanced products for wound management. Furthermore, rising government initiatives to raise awareness for proper wound management are also expected to raise the adoption of these products. The Japan market is projected to reach USD 0.49 billion by 2026, the China market is projected to reach USD 0.62 billion by 2026, and the India market is projected to reach USD 0.23 billion by 2026.

- For instance, Wound Australia allocated a fund of USD 1.5 million in the 2022-23 Pre-Budget Submissions to create awareness regarding chronic wound prevention and treatment through national media and digital campaigns.

Also, the growing burden of chronic wounds in the region is responsible for the segmental growth. As per the data provided by the Australian Medical Association Limited, approximately 450,000 Australians currently live with a chronic wound, costing the health system around USD 3.00 billion per annum.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa markets accounted for a comparatively lower advanced wound care market share due to their underpenetrated markets. However, the increase in cases of acute and chronic wounds due to trauma, chronic illness, and accidents and rising market players’ efforts to expand their geographical reach in the regions are a few factors contributing to the market growth in the coming years. Middle East & Africa recorded a market size of USD 0.75 billion in 2025, capturing 5.63% of the global market share, and is projected to reach USD 0.79 billion in 2026. The Latin America market generated USD 0.96 billion in 2025, representing 7.22% of the global market landscape, and is expected to reach USD 1.01 billion in 2026.

- In May 2021, Sanuwave Health, Inc., a provider of next generation wound care products, and its partners signed a distribution agreement with Grupo Suprimed to sell the dermaPace system in Brazil.

To know how our report can help streamline your business, Speak to Analyst

List of Key Companies in the Advanced Wound Care Market

3M, Smith & Nephew, and ConvaTec to Lead the Market Owing to Strong Product Portfolio

The market is consolidated due to a strong product portfolio and remarkable distribution networks of major companies in emerging and developed countries. Smith & Nephew, ConvaTec, Inc., and 3M lead the market, accounting for a dominant revenue share in 2023.

However, the lack of strong barriers to entry may lead to a rising entry of domestic players in the worldwide market. This factor is expected to lead to a slightly fragmented market by the end of 2032.

- For instance, in July 2021, PolarityTE, Inc. announced the submission of an investigational new drug application (IND) to the U.S. FDA to seek authorization to initiate clinical trials for the SkinTE product in the treatment of chronic cutaneous ulcers.

Other key players include Integra Life Sciences, MiMedx, Coloplast Corp, Derma Sciences Inc., Tissue Regenix, Mölnlycke Health Care AB, and Organogenesis Inc., which also entered the market with advanced wound care products. The introduction of innovative products, such as NPWT and advanced wound dressings, and significant investments in developing bioactive therapies for treatment are some of the major strategies enabling companies to boost their market position.

- For instance, in January 2021, Integra LifeSciences acquired ACell, Inc. to expand its advantage wound care product portfolio. Also, through this acquisition, the company aimed to offer more comprehensive wound management solutions to its customers.

LIST OF TOP COMPANIES PROFILED:

- Smith & Nephew (U.K.)

- 3M (U.S.)

- MiMedx (Georgia)

- Coloplast Corp (Denmark)

- ConvaTec Inc. (U.K.)

- Tissue Regenix (U.S.)

- Derma Sciences Inc. (U.S.)

- Mölnlycke Health Care AB (Sweden)

- Organogenesis Inc. (U.S.)

- Integra LifeSciences (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- September 2023 – MiMedx Group, Inc. announced the launch of EPIEFFECT, the company’s latest addition to its portfolio of advanced wound care solutions.

- December 2022 – MiMedx Group, Inc. licensed worldwide exclusive rights to Turn Therapeutics’ proprietary antimicrobial technology platform, PermaFusion, for the development of biologic products focused on wound and surgical recovery applications. As a result of this, the company has expanded its wound & surgical product pipeline.

- November 2022 – Reddress Medical, a U.S. and Israel-based private wound care company, made its advanced wound care management system, ActiGraft+ system, commercially available in Puerto Rico.

- October 2022 – Healthium Medtech Limited launched Theruptor Novo, an advanced wound care product for the treatment of leg ulcers and diabetic foot ulcers.

- June 2022 – Smith+Nephew announced that it has built a new R&D and manufacturing facility for its Advanced Wound Management franchise on the outskirts of Hull, U.K.

- May 2022 – Winner Medical launched its advanced wound care products, including CMC dressings in France.

- August 2021 – MiMedx, one of the prominent players in the market, established a subsidiary in Tokyo, Japan to expand its geographical presence.

- May 2021 – Activheal launched a prescription dispensing service, ActiveCare Direct, for easy access to a comprehensive range of advanced wound dressings.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The global market research report provides a detailed analysis of the market and focuses on key aspects such as leading companies, competitive landscape, products, applications, and end users. It also offers insights into trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market's growth in recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.52% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Indication

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 14.08 billion in 2026 and is projected to reach USD 23.33 billion by 2034.

In 2025, the market in North America stood at USD 5.66 billion.

The market will exhibit steady growth at a CAGR of 6.52% during the forecast period (2026-2034).

Based on product type, the advanced wound dressings segment will lead the market.

Increasing prevalence of chronic and acute wounds, rising geriatric population, and introduction of wound care products by market players are the major factors driving the growth of the market. Additionally, launch of advanced technologies by market players, such as active therapies and NPWT, is expected to drive the product adoption in the global market.

Smith & Nephew, 3M, and ConvaTec Group PLC are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us