Direct Satellite to Phone Cellular Market Size, Share & Industry Analysis, By Service (Emergency/Safety Services, Real-Time Messaging, Narrowband/Low-Rate Data, Cellular Broadband), By Standards (3GPP NTN – NR-NTN, 3GPP NTN – IoT-NTN, & Pre-standard D2D), By Satellite Network Architecture (Bent-pipe/Transparent payload, Regenerative payload, & Beamforming approach), By Orbit (LEO, MEO, & GEO), By Use Case (Consumer coverage extension, Public safety/disaster resilience, Enterprise remote workforce, Transportation corridors, Critical infrastructure, Defense), & Regional Forecast, 2026-2034

Direct Satellite to Phone Cellular Market Size and Future Outlook

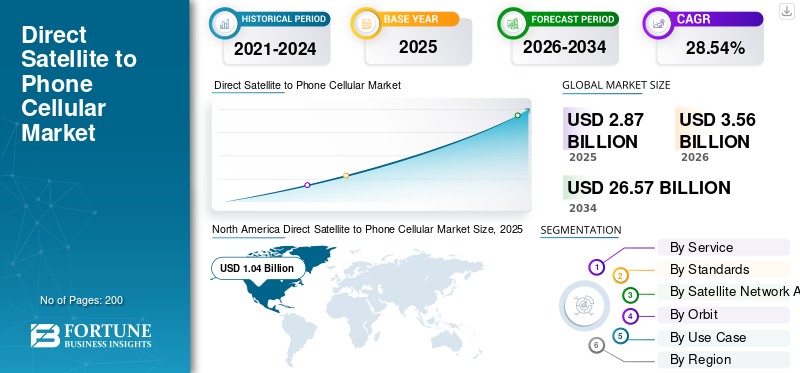

The global direct satellite to phone cellular market size was valued at USD 2.87 billion in 2025. The market is projected to grow from USD 3.56 billion in 2026 to USD 26.57 billion by 2034, exhibiting a CAGR of 28.54% during the forecast period. North America dominated the direct satellite to phone cellular market with a market share of 36.23% in 2025.

Direct‑to‑cell, or direct satellite‑to‑phone, is a technology that enables ordinary LTE‑capable smartphones and cellular‑IoT modems to connect directly to satellites in low Earth orbit (LEO), without relying on terrestrial cell towers. This extends voice, SMS, and basic data coverage to remote, rural, and off‑grid areas. The market encompasses satellite-based network‑in‑space infrastructure, MNO integrations, and services for emergency communications, IoT, maritime, aviation, public safety, and consumer connectivity. Additionally, the growth is driven by increasing demand for global roaming, emergency SOS, and 5G/IoT expansion into remote areas.

Key players include Starlink (SpaceX), which operates a large‑scale LEO based direct‑to‑cell constellation and partners with global operators such as T‑Mobile, Optus, and Telstr. Further, Lynk Global focuses on narrowband SMS and voice‑centric satellite‑to‑phone services.

Download Free sample to learn more about this report.

DIRECT SATELLITE TO PHONE CELLULAR MARKET TRENDS

Integration With Standard LTE‑Enabled Smartphones is a Market Trend

A key recent trend is the integration of direct‑to‑cell satellite links with standard LTE enabled smartphones, eliminating the need for dedicated satellite handset hardware. Providers such as Starlink and other non-terrestrial network operators are configuring LEO satellites to act as LTE‑type “cell towers in space,” using existing LTE protocols so that unmodified consumer phones can connect directly via text, voice, and low‑bandwidth data.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Connectivity in Remote, Rural, and Underserved Areas to Drive Market Growth

The rising demand for connectivity in remote, rural, and underserved areas is a major driver of the direct satellite to phone cellular market growth, as terrestrial mobile satellite networks are often too costly or impractical to deploy in sparsely populated or geographically challenging regions. Governments and regulators are increasingly treating satellite connectivity as a critical tool to close the digital divide, incorporating LEO‑based backhaul and direct‑to‑device links into national broadband and emergency communication plans.

MARKET RESTRAINTS

Regulatory Uncertainty in Managing Spectrum Use and Coordination Pose as a Market Restraint

Regulatory uncertainty is a significant market restraint as direct satellite-to-phone services and related satellite infrastructure must reuse or share terrestrial mobile spectrum while avoiding harmful interference. However, national regulators have not yet harmonized rules or licensing frameworks. Agencies such as Ofcom and the FCC are only now defining how satellite‑to‑cell links can operate in mobile bands, including interference limits and spectrum‑sharing arrangements, which delays commercial rollouts and raises compliance complexity.

MARKET OPPORTUNITIES

Convergence of 3GPP‑based Non‑Terrestrial‑Network Standards Creates New Market Opportunities

The convergence of 3GPP‑based non‑terrestrial‑network (NTN) standards with 5G/6G creates a major new opportunity by enabling smartphones and IoT devices to connect directly to satellites using the same protocols as terrestrial mobile networks. Open 3GPP NTN specifications allow satellite operators and terrestrial operators to build a single, interoperable network layer, reducing reliance on proprietary air interfaces and accelerating ecosystem scale.

MARKET CHALLENGES

High Cost and Technical Complexity Present a Major Market Challenge

High cost and technical complexity are major challenges for the market, as operators must deploy large LEO constellations, multi beam payloads, and complex ground‑segment networks while still aligning with terrestrial‑mobile standards. Each satellite requires substantial upfront investment in launch, power, and intersatellite link infrastructure, and network level fault tolerance increases design and operational burden. On the user side, integrating satellite ready modems or chipsets into smartphones without degrading battery life which complicates consumer scale adoption.

Segmentation Analysis

By Service

High performance and Reliability in Disaster to Boost Emergency/Safety Services Segmental Growth

On the basis of service, the market is segmented into emergency/safety services, real-time messaging, narrowband/low-rate data, cellular broadband, and others.

The emergency/safety services segment is anticipated to account for the largest direct satellite to phone cellular market share. The segmental growth is attributed to resolve the crucial and dangerous issue of communication breakdowns in remote locations or during emergencies.

The cellular broadband segment is expected to rise with a highest CAGR of 29.71% over the forecast period.

By Standards

Specialized and Niche Applications to Boost Pre-standard D2D Segment Growth

Based on standards, the market is segmented into 3GPP NTN – NR-NTN, 3GPP NTN – IoT-NTN, and pre-standard D2D.

In 2025, the pre-standard D2D segment dominated the global market. Pre-standard carriers have concentrated on developing specialized chipsets that can be easily integrated into consumer phones or, as witnessed in the case of Starlink/T-Mobile, made to function with already-existing LTE devices. These factors mentioned above have driven the segmental growth.

The 3GPP NTN – NR-NTN segment is projected to grow at a high CAGR of 29.17% over the forecast period.

By Satellite Network Architecture

Usage in Low-Bandwidth IoT and Emergency Services to Boost Bent-pipe/Transparent Payload Segment Growth

Based on the satellite network architecture, the market is segmented into bent-pipe/transparent payload, regenerative payload, and beamforming approach.

The bent-pipe/transparent payload segment is anticipated to witness a dominating market share over the forecast period. Bent-pipe payloads are ideal for applications such as SOS emergency signaling, text messaging (SMS), and IoT sensor tracking (telemetry) at remote locations since they only need to convey little data packets, which lowers satellite costs and power consumption.

The beamforming approach segment is projected to grow at a high CAGR of 29.15% over the forecast period.

By Orbit

Scalability and High Throughput to Boosts LEO Segment Growth

Based on the orbit, the market is segmented into LEO, MEO, and GEO.

The LEO segment is anticipated to witness a dominating market share over the forecast period. The segmental growth is driven by LEO constellations, which are designed for high-capacity and high-data throughput services, allowing them to support a growing number of users. As the number of satellites in a constellation increases, the quality of service also improves.

The GEO segment is projected to grow at a CAGR of 27.12% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Use Case

Increasing Demand for Mobile Connectivity to boost Consumer Coverage Extension Segment Growth

Based on use case, the market is segmented into consumer coverage extension, public safety/disaster resilience, enterprise remote workforce, transportation corridors, critical infrastructure, defense, and others.

The consumer coverage extension segment dominated the market share. The segmental dominance is due to the increasing need for ubiquitous mobile connectivity on common cellphones, particularly for location-based applications in remote or off-network locations, emergency communications, and basic internet.

In addition, the enterprise remote workforce segment is projected to grow at a high CAGR of 29.45% during the study period.

Direct Satellite to Phone Cellular Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Direct Satellite to Phone Cellular Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 0.84 billion, and also maintained the leading share in 2025, with USD 1.04 billion. North America leads in direct satellite-to-phone cellular networks, driven by U.S. centric projects and regulatory policy experimentation.

U.S. Direct Satellite to Phone Cellular Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.79 billion in 2026, accounting for roughly 29.04% CAGR. The U.S. is the most advanced single‑market for direct satellite‑to‑phone services, combining FCC‑backed spectrum‑policy with operator‑satellite‑partnerships. AT&T and AST SpaceMobile are rolling out satellite‑to‑cell coverage for consumers and public‑safety users via BlueBird‑series satellites.

Europe

Europe is projected to record a steady growth rate of 28.21% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 1.01 billion by 2026. Europe’s approach is shaped by 5G‑NTN‑standardisation at ETSI/3GPP and EU‑level digital‑infrastructure‑and‑public‑safety‑agendas. The European Space Agency and EU‑funded 5G‑SATCOM‑style projects are supporting trials of satellite‑to‑cellular‑backhaul and emergency‑connectivity.

U.K. Direct Satellite to Phone Cellular Market

The U.K. market in 2026 is estimated at around USD 0.33 billion, representing roughly 28.57% CAGR during the study period. The region participates through European standardization and national digital resilience plans, with Ofcom exploring how satellite to cell links can be hosted in existing mobile bands under strict interference management conditions.

Germany Direct Satellite to Phone Cellular Market

Germany’s market is projected to reach approximately USD 0.28 billion in 2026. Germany’s role is defined by a strong 5G‑NTN R&D ecosystem and active spectrum‑regulation. The Federal Network Agency (BNetzA) scrutinizes interference risks from satellite‑to‑cell networks and monitors international‑5G‑NTN‑developments.

Asia Pacific

Asia Pacific region is estimated to reach USD 1.02 billion in 2026 and secure the position of the third-largest region in the market and fastest growing during the study period. Across Asia Pacific, governments and regulators witness satellite‑to‑cell as a tool for rural connectivity and disaster resilience, particularly in geographically dispersed archipelagos and large off grid populations.

Japan Direct Satellite to Phone Cellular Market

The Japan market in 2026 is estimated at around USD 0.18 billion, accounting for roughly 29.39% of CAGR during the forecast period. Japan is a high-income telecom market with advanced 5G‑NTN research and development, supported by national spectrum and satellite policy bodies.

China Direct Satellite to Phone Cellular Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.34 billion. China is advancing a tightly controlled, state directed, satellite communications ecosystem, with 5G‑NTN experiments tied to national space and telecom agencies.

India Direct Satellite to Phone Cellular Market

The Indian market size in 2026 is estimated at around USD 0.18 billion. India positions satellite to cellular as a digital inclusion and rural connectivity enabler, with spectrum policy and regulatory consultations explicitly referencing satellite‑to‑mobile‑services for areas beyond terrestrial coverage.

Rest of the World

The rest of the world region includes the Middle East & Africa and Latin America. In these regions, regulators increasingly regard satellite to cell as a way to bridge vast rural coverage gaps and support national broadband plans. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.15 billion and USD 0.09 billion in 2026, respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Product Innovation to Fuel Market Expansion

The direct satellite‑to‑phone cellular market is moderately consolidated, with major LEO satellite operators such as Starlink (SpaceX), Lynk Global, and AST SpaceMobile integrated into global mobile‑network operators including T‑Mobile, AT&T, and emerging carriers, alongside device makers and 5G‑equipment vendors shaping the ecosystem.

Strategic partnerships between satellite network operators and MNOs are the core growth engine, enabling bundled services, shared infrastructure, and regulatory‑risk‑sharing, while product innovation focuses on extending coverage, reducing latency, and enhancing interference resilient air interfaces and low power uplinks for standard LTE smartphones, all anchored in 5G‑NTN‑standardisation.

LIST OF KEY DIRECT SATELLITE TO PHONE CELLULAR COMPANIES PROFILED

- SpaceX (U.S.)

- AST SpaceMobile (U.S.)

- Lynk Global (U.S.)

- Viasat (U.S.)

- Iridium Communications (U.S.)

- Globalstar (U.S.)

- Skylo Technologies (U.S.)

- Omnispace (U.S.)

- Thuraya (Al Yah Satellite Communications) (UAE)

- Telesat (Telesat Canada) (Canada)

KEY INDUSTRY DEVELOPMENTS

- February 2026: At a Conference, a SpaceX policy manager stated that the company's cellular Starlink aims for speeds of up to 150 Mbps per user as it gets ready to expand its capacity and add new satellites.

- February 2026: Iridium Communications Inc. introduced the Iridium 9604, a small, multifunctional Internet of Things module that combines GNSS positioning, LTE-M cellular connectivity, and Iridium Short Burst Data (SBD) satellite services into one platform.

- October 2025: A first-of-its-kind direct-to-device (D2D) demonstration containing native Short Message Service (SMS) messaging on the Android smartphone was completed in Mexico by Viasat, Inc., a global leader in satellite communications.

- April 2025: The first direct-to-handset (D2H) communication test utilizing direct-to-device (D2D) technology in L-band was successfully completed in Brazil by Viasat, Inc. Two smartphones were witnessed in the ground-breaking experiment communicating directly via satellite using 3GPP NTN standards without the use of additional terrestrial infrastructure.

- January 2024: With the goal of allowing mass-market devices to access messaging and SOS services outside of cellular coverage starting in 2026, Iridium Communications intends to make its low Earth orbit constellation compatible with 5G standards.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 28.54% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service, Standards, Satellite Network Architecture, Orbit, Use Case, and Region |

| By Service |

|

| By Standards |

|

| By Satellite Network Architecture |

|

| By Orbit |

|

| By Use Case | |

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.87 billion in 2025 and is projected to reach USD 26.57 billion by 2034.

In 2025, the market value stood at USD 1.04 billion.

The market is expected to exhibit a CAGR of 28.54% during the forecast period.

By service, the emergency/safety services segment is expected to dominate the market.

The rising demand for connectivity in remote, rural, and underserved areas is a key driver anticipated to drive the market growth.

SpaceX (U.S.), AST SpaceMobile (U.S.), Lynk Global (U.S.), Viasat (U.S.), and Iridium Communications (U.S.) are few key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us