Dog Food Market Size, Share & Industry Analysis, By Price Range (Economy, Medium, and Premium), By Packaging (Pouches, Cans, Bags, and Others), By Product Type (Dry Food [Kibble Pallets, Wet Food, and Treats & Snacks [Training Treats, Functional Treats, and Dental Treats]), By Source (Animal-based [Chicken, Beef, Pork, and Others] and Plant-based), By End-Use (Puppy, Adult, and Senior), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Pet Food Stores, Online Channels, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

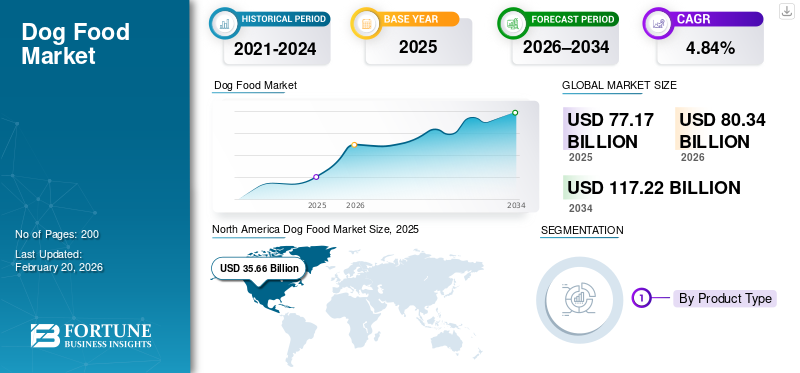

Dog Food Market Size and Future Outlook

The global dog food market size was valued at USD 77.17 billion in 2025. The market is projected to grow from USD 80.34 billion in 2026 to USD 117.22 billion by 2034, exhibiting a CAGR of 4.84% during the forecast period. North America dominated the dog food market with a market share of 46.21% in 2025.

Dog food comprises nutritionally balanced formulations designed to meet canine dietary requirements across life stages, breeds, and activity levels. Products range from dry kibble and wet foods to functional treats and premium fresh-style offerings. Growth in the market is structurally supported by rising global dog ownership, increasing pet humanization, demand for premiumization of pet diets, and growing awareness of life-stage and condition-specific nutrition. Urbanization, dual-income households, and expanding e-commerce penetration are further accelerating demand for convenient, high-quality premium, and specialized dog food products globally.

Large multinational manufacturers such as Mars Petcare, Nestlé Purina PetCare, Hill’s Pet Nutrition, General Mills, and J.M. Smucker Company dominate the market, leveraging vertically integrated sourcing, advanced nutritional R&D, and expansive global distribution networks.

Download Free sample to learn more about this report.

Dog Food Market Trends

Rapid Growth of Plant-Based and Alternative Protein Dog Food to Shape Industry Growth

The rapid expansion of plant-based and alternative protein dog food is increasingly reshaping the global market demand, driven by converging trends in pet humanization, sustainability concerns, and heightened awareness of animal protein supply-chain risks. Pet owners, particularly millennials and Gen Z, are extending their own dietary values, such as flexitarianism, veganism, and environmental responsibility, to their pets. This has accelerated demand for dog food formulations based on plant proteins (pea, lentil, chickpea, soy, oats) and novel or alternative proteins such as insect meal, algae, and fermentation-derived proteins.

- The American Pet Products Association (APPA) reports that United States pet food expenditure exceeded USD 64 million in 2023, with strong growth concentrated in premium, functional, and specialty diets, including plant-based and limited-ingredient formulations.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Global Dog Ownership and Pet Humanization to Drive Industry Expansion

Rising global dog ownership, combined with the accelerating trend of pet humanization, is fundamentally transforming the nutritional landscape of the global market. Dogs are increasingly perceived as family members rather than companion animals, prompting pet owners to prioritize pet health, longevity, and preventive nutrition in ways that closely mirror human dietary behavior. This shift is driving strong demand for nutritionally upgraded pet food products, including premium, natural, organic, functional, and breed- or life-stage-specific formulations.

- According to the American Pet Products Association, over 70% of dog owners consider the quality of their pet's food a top priority, with many viewing nutrition as a foundational element for their pet’s health and longevity.

Market Restraints

Volatility in Animal Protein and Grain Prices Impacting Cost Structures to Hamper Market Growth

Volatility in animal protein and grain prices has become a critical cost-structure challenge for the global industry, directly affecting raw material sourcing, formulation economics, and margin stability. Meat ingredients such as chicken, beef, lamb, and fish meal, along with key grains including corn, wheat, and rice, account for a substantial share of total production costs in dog food manufacturing. These inputs are highly exposed to external shocks such as climate variability, disease outbreaks (avian influenza and African swine fever), geopolitical disruptions, energy and fertilizer price inflation, and trade policy shifts. As a result, product manufacturers face frequent cost fluctuations that complicate long-term pricing strategies and contract sourcing.

Market Opportunities

Expansion of E-Commerce and Subscription-Based Dog Food Models Boosts Industry Expansion

The expansion of e-commerce and subscription-based dog food models is structurally transforming distribution, consumer engagement, and revenue visibility within the global market. Digital channels enable pet food brands to bypass traditional retail constraints, offering direct-to-consumer (DTC) access, broader product assortments, and enhanced price transparency. Subscription-based models, in particular, align closely with the recurring consumption nature of dog food, allowing brands to lock in predictable demand while improving inventory planning and customer lifetime value.

- According to the Pet Food Institute and Packaged Facts, over 30% of U.S. dog owners purchased dog food online in 2024, with subscription models gaining traction for dry food and treats.

SEGMENTATION ANALYSIS

By Product Type

Dry Food Segment Dominates due to Ease of Storage

On the basis of product type, the global market is segmented into dry food, wet food, and treats & snacks.

Dry food dominates the global market, accounting for the largest share with a market size of USD 29.07 billion in 2025. Its leadership is supported by affordability, long shelf life, ease of storage, and suitability for bulk feeding, particularly among medium- and large-breed dogs.

Wet food represents the fastest-growing product segment, expanding at a CAGR of 8.07% during 2026–2034. Growth is driven by rising preference for high-palatable, moisture-rich diets that support hydration, digestion, and dental health, particularly for senior and small-breed dogs.

To know how our report can help streamline your business, Speak to Analyst

By Source

Animal-Based Proteins Maintain Leadership due to Strong Consumer Trust in Meat-Centric Formulations

On the basis of source, the global market is segmented into animal-based and plant-based.

The animal-based segment dominates the market, with a value of USD 39.50 billion in 2025, reflecting strong consumer trust in meat-centric formulations aligned with canine dietary needs. Chicken remains the leading protein source due to its affordability, digestibility, and wide availability, followed by beef and pork. Animal-based formulations are widely perceived as nutritionally superior, particularly for muscle development, energy, and palatability.

The plant-based segment, valued at USD 2.04 billion in 2025, represents a smaller global dog food market share but is the fastest-growing source market, registering a CAGR of 10.76%.

By Price Range

Medium Segment Leads the Market due to Balanced Positioning Between Quality and Affordability

On the basis of price range, the global market is segmented into economy, medium, and premium.

The medium price range segment leads the global market, accounting for USD 18.78 billion in 2025. This segment benefits from its balanced positioning between quality and affordability, appealing to mass-market consumers seeking improved nutrition without premium-level pricing.

The premium segment is also the fastest-growing price category, projected to expand at a CAGR of 6.51% during 2026–2034, supported by premiumization within accessible price points.

By Packaging

Bags Segment Lead due to High Consumption of Dry Dog Food

On the basis of the packaging, the global market is segmented into pouches, cans, bags, and others.

Bags hold the dominant position in the global market, accounting for the largest share with a market size of USD 21.82 billion in 2025. This dominance is primarily attributed to the high consumption of dry dog food, particularly kibble and pellets, which are predominantly packaged in bags.

Pouches represent the fastest-growing packaging segment, projected to expand at a CAGR of 7.30% during 2026-2034. Growth is driven by increasing demand for portion-controlled, single-serve, and premium wet dog food formats, and functional and fresh-style products.

By End-Use

Adult Dog Food Dominates Demand Owing to Its Ability to Support Maintenance Nutrition

Based on end-use, the global market is segmented into puppy, adult, and senior.

The adult segment accounts for the largest share of the market, valued at USD 24.84 billion in 2025, reflecting the dominance of adult dogs within the global canine population. Adult formulations are designed to support maintenance nutrition, energy needs, and weight management, making them the most widely consumed category across all regions.

Senior is the fastest-growing segment, projected to expand at a CAGR of 7.58% during the forecast period.

By Distribution Channel

Supermarkets/hypermarkets Segment Lead due to Their Broad Product Assortments

Based on distribution channel, the global market is segmented into supermarkets/hypermarkets, specialty pet food stores, online channels, and others.

Supermarkets and hypermarkets dominate dog food distribution, accounting for USD 17.87 billion in 2025, due to their broad product assortments, competitive pricing, and high footfall. These channels are particularly strong for dry food and economy-to-medium priced products, supported by promotional offers and private-label penetration.

Online channels represent the fastest-growing segment, expanding at a CAGR of 7.93% during 2026-2034, with a market size of USD 8.85 billion in 2025.

Dog Food Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, the Middle East & Africa.

North America

North America Dog Food Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market and accounted for USD 35.66 billion in 2025, maintaining its position as the largest regional market globally. Growth is supported by high dog ownership rates, strong premiumization trends, and widespread adoption of veterinary-recommended and life-stage-specific diets.

U.S. Dog Food Market

The U.S. accounted for approximately USD 27.76 billion in 2025, driven by high per-pet spending, strong adherence to AAFCO nutritional standards, and advanced retail infrastructure. Subscription-based dry food and functional treat purchases are accelerating through e-commerce platforms.

Europe

Europe reached a market size of USD 15.43 billion in 2025, supported by high pet ownership, stringent regulatory oversight, and growing demand for premium and sustainable dog food products. Germany, the U.K., and France lead regional consumption. Europe is projected to grow at a CAGR of 4.90%.

Germany Dog Food Market

Germany accounted for approximately USD 2.38 billion in 2025, driven by strong consumption of dry and functional dog food and high compliance with FEDIAF nutritional guidelines.

Asia Pacific

The Asia Pacific market was valued at USD 11.60 billion in 2025 and represents the fastest-growing regional market, projected to grow at a CAGR of 7.28% during 2026-2034. Dog food market growth is driven by rapid urbanization, rising disposable incomes, and increasing product adoption in metropolitan areas.

Japan Dog Food Market

Japan represents one of the most mature and structurally distinct dog food markets in the Asia Pacific, characterized by a strong focus on small-breed dogs, senior nutrition, and premium-quality formulations. In Japan, the market was valued at approximately USD 2.84 billion in 2025, accounting for a significant share of the Asia Pacific regional market.

South America and the Middle East & Africa

South America accounted for USD 11.15 billion in 2025, supported by expanding middle-class populations and the rising pet humanization of pets. The Middle East & Africa market reached USD 3.33 billion in 2025, remaining relatively nascent but showing steady growth potential.

South Africa Dog Food Market

The South African market was valued at approximately USD 0.71 billion in 2025. South Africa remains the largest market in Africa, supported by rising awareness of commercial dog food benefits and increasing availability through modern retail formats.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Emphasis on Ingredient Sourcing and Marketing to Meet Consumer Needs

The global market is moderately to highly consolidated, with a small group of multinational corporations controlling a significant share of global revenues through extensive brand portfolios, vertically integrated supply chains, and strong regulatory compliance capabilities. Large manufacturers maintain a competitive advantage by controlling ingredient sourcing, formulation science, processing technology, and marketing, enabling rapid response to meet consumer preferences.

Key Players in the Dog Food Market

|

Rank |

Company Name |

|

1 |

Mars Petcare |

|

2 |

Nestlé Purina PetCare |

|

3 |

Hill’s Pet Nutrition |

|

4 |

General Mills |

|

5 |

J.M. Smucker Company |

List of Key Dog Food Companies Profiled

- Mars Petcare (U.S.)

- Nestlé Purina PetCare (Switzerland)

- Hill’s Pet Nutrition (Colgate-Palmolive) (U.S.)

- Affinia Petcare (U.S.)

- General Mills (U.S.)

- The J.M. Smucker Company (U.S.)

- WellPet LLC (U.S.)

- Diamond Pet Foods (U.S.)

- Unicharm Corporation (Japan)

- Deuerer Group (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Avanti Pet Care, a subsidiary of aquaculture firm Avanti Feeds, launched its Avant Furst dog food range in India. The initial lineup includes adult dog food and puppy food, both in Chicken & Vegetable flavor, designed for balanced nutrition across breeds. These formulas support immunity, growth, energy, and overall health.

- October 2025: Blue Buffalo launched its Love Made Fresh line nationwide, entering the USD 3 billion fresh pet food category. This move by General Mills positions the brand as the largest U.S. pet food company offering dry, wet, and fresh options, targeting dog owners who mix fresh food with kibble.

- August 2025: PawCo Foods launched Magic Cookie, a line of functional dog biscuits, to deliver targeted health benefits alongside sustainability. This expands their "Magic" product range, which debuted at SuperZoo 2025.

- April 2025: Godrej Consumer Products, through its subsidiary Godrej Pet Care, launched the 'Godrej Ninja' pet food brand in Tamil Nadu. Godrej Ninja is a scientifically formulated dry dog food developed at the Nadir Godrej Centre for Animal Research & Development, targeting gut health and immunity via probiotics, prebiotics, polyphenols, and 37 nutrients such as omega-3s and vitamins.

- September 2024: Growel Group, an Indian company specializing in aquaculture feeds and seafood processing since 1994, launched its pet food brand Carniwel. The brand targets premium yet affordable nutrition for dogs and cats across life stages, including puppies, kittens, adults, and seniors.

REPORT COVERAGE

The global dog food market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.84% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Source · Animal-based o Chicken o Beef o Pork o Others · Plant-based |

|

|

By Price Range · Economy · Medium · Premium |

|

|

By Packaging

|

|

|

By End-Use · Puppy · Adult · Senior |

|

|

By Distribution Channel · Supermarkets/Hypermarkets · Specialty Pet Food Stores · Online Channels · Others |

|

|

By Region · North America (By Product Type, Source, Price Range, Packaging, End-Use, Distribution Channel, and Country) • U.S. (By Distribution Channel) • Canada (By Distribution Channel) • Mexico (By Distribution Channel) · Europe (By Product Type, Source, Price Range, Packaging, End-Use, Distribution Channel, and Country) • U.K. (By Distribution Channel) • Germany (By Distribution Channel) • France (By Distribution Channel) • Italy (By Distribution Channel) • Spain (By Distribution Channel) • Rest of Europe (By Distribution Channel) · Asia Pacific (By Product Type, Source, Price Range, Packaging, End-Use, Distribution Channel, and Country) • China (By Distribution Channel) • Japan (By Distribution Channel) • India (By Distribution Channel) • Australia (By Distribution Channel) • Rest of Asia Pacific (By Distribution Channel) · South America (By Product Type, Source, Price Range, Packaging, End-Use, Distribution Channel, and Country) • Brazil (By Distribution Channel) • Argentina (By Distribution Channel) • Rest of South America (By Distribution Channel) · Middle East & Africa (By Product Type, Source, Price Range, Packaging, End-Use, Distribution Channel, and Country) • South Africa (By Distribution Channel) • UAE (By Distribution Channel) • Rest of the MEA (By Distribution Channel) |

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 77.17 billion in 2025 and is anticipated to reach USD 117.22 billion by 2034.

At a CAGR of 4.84%, the global market will exhibit steady growth over the forecast period.

By product type, the dry food segment leads the market.

North America held the largest market share in 2025.

Rising global dog ownership and pet humanization are key factors driving the market.

Mars Petcare, Nestlé Purina PetCare, Hills Pet Nutrition, General Mills, and J.M. Smucker Company are the leading companies in the market.

The rapid growth of plant-based and alternative protein dog food is the key industry trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us