Drone Motor Market Size, Share & Industry Analysis, By Motor Type (Brushless Motor, Brushed Motor, and Others), By Drone Type (Fixed Wing, Rotary Wing, and Hybrid), By Power Capacity (Below 50 W, 51 to 100 W, and Above 100 W) By Application (Aerial Photography, Agriculture, Construction, Military, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

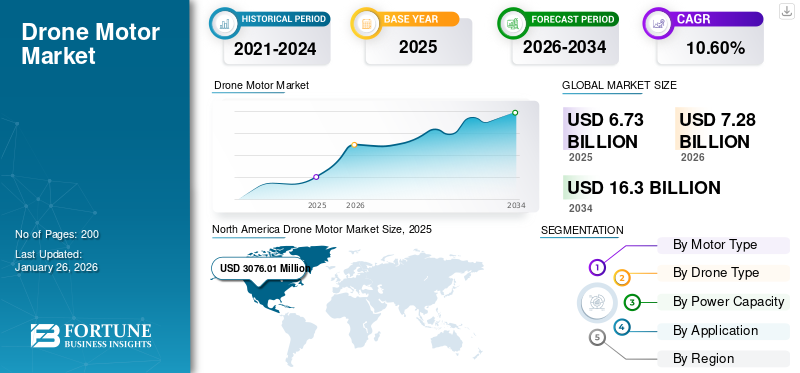

The global drone motor market size was valued at USD 6732.1 million in 2025. The market is projected to grow from USD 7280.8 million in 2026 to USD 16301.1 million by 2034, exhibiting a CAGR of 10.6% during the forecast period. North America dominated the drone motor market with a market share of 45.69% in 2025.

Unmanned Aerial Vehicle (UAV) motors are electric motors specifically designed to power unmanned aerial vehicles, also known as drones. These are crucial for converting electrical energy into mechanical energy, which generates the thrust needed for drones to take off, hover, maneuver, and land. The motor is fixed to the frame arm, with one end connected to the propeller, which generates downward thrust through rotation. Drones change their flight state by varying the speed of the motor.

UAV motors primarily come in two types, namely brushed and brushless. Brushed motors are simpler, more economical, and suitable for low-cost or toy drones. Brushless DC (BLDC) motors are highly preferred due to their efficiency, reliability, and durability. BLDC motors provide smoother operation, higher power output, and precise control over speed and direction, making them ideal for various drone applications. Key components of a BLDC motor include the stator, rotor, bearings, and controller. Stator consists of coils of wire that generate a magnetic field when electric current passes through them. The rotor, containing permanent magnets, interacts with this magnetic field, causing rotation. Bearings reduce friction, allowing smooth rotor movement, and the controller regulates the motor's speed and direction based on signals from the pilot. Many government agencies and private players have made significant investments in drone technology adoption. Key players in the market include DJI, Hacker Motor GmbH, KDE Direct, Parrot Drone SAS, T-motor, and among others.

The COVID-19 pandemic had a profound impact on the drone motor market, initially causing significant disruptions. However, the need for contactless delivery services later drove investments in drone logistics, while regulatory relaxations in many countries facilitated broader applications of drones.

Download Free sample to learn more about this report.

Drone Motor Market Trends

Advancements in Brushless DC Motor Technology, Leading to the Creation of Sensorless Motor is an Emerging Trend in the Market

Advances in BLDC motor technology have led to the emergence of sensorless motor drives, marking a significant trend in the market that promises to reduce costs and enhance performance. Traditionally, BLDC motors relied on position sensors to accurately control their operation, which added complexity and increased manufacturing costs. However, recent innovations in control algorithms allow these motors to utilize back electromotive force (EMF) detection to determine rotor position without external sensors.

The reduction in costs associated with sensorless motor drives is highly beneficial for various applications, including consumer electronics, automotive systems, and industrial automation. By eliminating the need for position sensors, manufacturers can lower their production expenses and pass those savings on to consumers. This affordability opens up new market opportunities and applications where previously cost-prohibitive technologies can now be implemented. As industries increasingly seek energy-efficient solutions that also offer high performance, sensorless motors are becoming a preferred choice.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Significant Investments from Governments and Private Entities into Drone Technology bolster the Market Growth

Significant investments in drone technology from governments and private entities are driving the drone motor market growth, particularly in regions such as India, where the government is actively promoting the drone sector as a key area for economic development. For instance, in November 2024, the Indian government reserved substantial funding through initiatives, such as the Production-Linked Incentive (PLI) scheme, which aims to attract approximately USD 6.7 billion in investments over the next three years. This funding is designed to stimulate local manufacturing of drones and their components, thereby enhancing domestic capabilities and reducing reliance on imports.

Furthermore, the government's commitment to developing the drone industry is further reflected in its initiatives, such as the "Drone Shakti" scheme initiated in February 2022, which promotes Drone-As-A-Service (DrAAS) and encourages startups to innovate within this space. The Union Budget for 2022-23 highlighted the importance of drones in agriculture, surveillance, and logistics, with specific provisions for skilling programs to train a new generation of drone pilots.

Private sector involvement is equally crucial in driving growth within the market. Companies are increasingly investing in research and development to enhance drone capabilities, focusing on improvements in battery life, payload capacity, and operational efficiency. For instance, in October 2023, firms such as Amazon announced that they are exploring drone delivery systems, while local startups are developing specialized drones for agriculture and logistics. These private investments complement government efforts, creating a robust environment for technological advancements that can meet diverse market needs.

Market Restraints

Excessive Heat Generation During Operations affects the Overall Performance, Restricting Market Expansion

Drone motors, particularly those with high KV ratings, typically generate considerable heat during operation, which can pose challenges for performance and reliability. The KV rating indicates the number of revolutions per minute (RPM) a motor will achieve per volt applied without any load. For instance, a motor with a KV rating of 2200 will spin at 22,000 RPM if supplied with 10 volts. While high KV motors are advantageous for achieving rapid speeds, they also draw more current and produce more heat while under load. This heat generation is a critical concern, as excessive temperatures can lead to thermal overload, damaging the motor and concerned electronic components such as Electronic Speed Controllers (ESCs) and batteries. Moreover, the implications of poor heat management extend beyond immediate performance issues, leading to premature failure of motor components, thus resulting in costly repairs and increased downtime for drone operations.

Common methods to manage heat include using heat sinks, improving airflow around the motor, and incorporating temperature sensors that can trigger automatic shutdowns or throttle reductions when temperatures exceed safe limits. However, these cooling solutions can add weight and complexity to the drone's design, potentially compensating for the performance benefits gained from high KV motors.

Market Opportunities

Increased Versatility of Drones in Various Sectors Offer Major Growth Opportunities

The increasing versatility of drones across various sectors presents a major growth opportunity due to their ability to improve efficiency, reduce costs, and enhance safety. Drones are highly preferred in industries such as construction, agriculture, oil and gas, logistics, and even military applications. For instance, in agriculture, drones equipped with advanced sensors can monitor crop health and optimize resource management, leading to better yield and reduced waste.

As drone technology continues to advance, its potential applications are expanding. Innovations such as improved battery life, enhanced payload capacities, and advanced imaging technologies are enabling drones to tackle more complex tasks across various industries. The ongoing development of regulatory frameworks also plays a critical role in facilitating broader adoption of drone technology, ensuring safe and efficient operations while unlocking new opportunities for the market.

SEGMENTATION ANALYSIS

By Motor Type

Brushless Motors Dominated the Market Owing to Their Efficiency, Reliability, Durability, and High Power-To-Weight Ratio

By motor type, the market is classified into brushless motor, brushed motor, and others.

The Brushless Motor segment is projecteed to dominate the market with a share of 44.20% in 2026 and will be the fastest-growing segment from 2026 to 2034. Brushless motors operate without brushes, which reduces friction and energy loss. This design allows them to convert a higher percentage of electrical energy into mechanical energy, resulting in longer flight times and reduced battery consumption. The efficiency of brushless motors is particularly crucial for drones that require extended operational periods or need to carry heavier payloads, as it maximizes their range and effectiveness in varied applications.

The brushed motor segment is anticipated to show significant growth during the study period. Brushed motors are inexpensive to manufacture. This low cost makes them a viable option for entry-level drones, toy drones, and educational projects where budget constraints are a primary concern.

By Drone Type

Growing Usage in Surveying and Mapping Boosted the Fixed Wing Segment Growth

Based on drone type, the market is segmented into fixed wing, rotary wing, and hybrid.

The fixed wing segment held the largest global drone motor market share 43.59 in 2026 and will be the fastest-growing segment for the 2026-2034 period. This growth is propelled by the wide usage of fixed-wing drones for applications that need long flight time and have a large distance. Such drones are efficient for tasks, including large-scale surveying, mapping, and surveillance. The segment is likely to capture 43% of the market share in 2025.

The rotary wing segment is anticipated to witness significant growth during the study period. These are valued for their stability and portability, making them ideal for tasks requiring precise navigation and close-quarters operations. Industries, including construction, energy, telecommunications, and utilities, are increasingly adopting multi-rotor drones for routine inspections, preventive maintenance, and asset monitoring. The segment is likely to record a strong CAGR of 10.4% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Power Capacity

51 To 100 W Segment Led the Market Due to Its Increased Power Efficiency

By power capacity, the segment is categorized into below 50 w, 51 to 100 w, and above 100 w.

The 51 to 100 W segment expected the market 44.54 in 2026. Drone motors in the 51 to 100 W range are designed to be light in weight without sacrificing performance. This is crucial for drones, as excess weight reduces flight time and maneuverability. Efficient power consumption contributes directly to extended flight times, a critical factor for commercial applications such as infrastructure inspection, agricultural monitoring, and delivery services. These factors collectively contribute to the segmental growth in the market. The segment is expected to acquire a CAGR of 10.69% during the forecast period.

The above 100 W segment in power capacity is anticipated to show moderate growth during the study period. Motors rated above 100 W showcase rising demand for drones due to their ability to provide greater payload capacities, longer flight times, and improved overall performance. These motors are specifically designed to meet the rigorous demands of heavy-lift drones, which require robust power output to carry significant weights while maintaining efficiency and stability during flight.

Below 50W segment is expected to capture 44% of the market share in 2025.

By Application

Aerial Photography Segment Commanded the Market Due to Growing Focus on Project Planning and Monitoring

By application, the market is categorized into aerial photography, agriculture, construction, military, and others.

The aerial photography segment is likely to dominate the market share of 37.47% in 2026. Drones equipped with high-resolution cameras and stabilized gimbals offer exceptional flexibility and maneuverability for capturing aerial images and videos. These capabilities are particularly crucial across industries such as real estate, construction, tourism, and entertainment, where aerial footage provides valuable insights, enhances marketing efforts, and supports project planning and monitoring.

The agriculture segment is projected to grow with a CAGR of 25% during the forecast period. Agriculture drones are outfitted with cutting-edge sensors and high-resolution cameras, facilitating precision mapping and surveying of agricultural landscapes. These drones facilitate precision farming by providing farmers with real-time, high-resolution data for informed decision-making. Drones can optimize resource allocation, reduce waste, and enhance overall crop health.

DRONE MOTOR MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Drone Motor Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 45.69% to the global market in 2025, with a valuation of USD 3.08 billion, and is projected to reach USD 3.33 billion in 2026. This is attributed to the increasing use of drones for spying and surveillance in the North American region, particularly the U.S. The rising adoption of drones in the construction industry for routine site inspections, driven by government regulations, also contributes to this dominance. The U.S. government investments in research and development are also aiding in advancements in drone technologies, prioritizing efficiency, durability, and operational capabilities, which stimulates market growth in North America. In January 2025, the U.S. Air Force granted Firestorm Labs a contract worth USD 100 million for manufacturing its small unmanned aerial systems. The project required the California-based startup to provide its leading drones, related support services, and research and development efforts for various applications. The U.S. market size is estimated to be USD 2438.9 million in 2026.

Europe

Europe accounted for USD 1.47 billion in 2025, representing 21.77% of the global market share, and is projected to reach USD 1.59 billion in 2026. The increasing adoption of drones in logistics, particularly for efficient delivery solutions in urban areas, is driving the market. Advancements in motor technology are also improving drone performance, allowing greater payloads and longer ranges, which supports sustainability initiatives by reducing carbon footprints. Government investments in research and development (R&D) are crucial in advancing drone technologies. The market in U.K. is likely to be USD 546.2 million in 2026, whereas Germany is expected to be USD 400 million in 2026.

Asia Pacific

The Asia Pacific market was valued at USD 1.18 billion in 2025, capturing 17.57% of global revenue, and is estimated to reach USD 1.28 billion in 2026. The rise in drone usage across various industries, including agriculture, construction, filmmaking, education, and logistics, is boosting the demand for high-performance drone motors in the region. Businesses across the region are increasingly leveraging drones for tasks such as precision farming, surveying, and delivery services, highlighting the need for reliable and efficient motors. The market size in China is likely to be USD 455.9 million in 2026. On the other hand, the market in India is poised to be USD 339.5 million in 2026 and Japan is anticipated to hit USD 215 million in 2026.

In February 2025, Countries participating in Japan’s Official Security Assistance (OSA) program showed interest in Tokyo’s dual-use drones, leading the East Asian nation to examine the possibility of exporting them. Japan’s Ministry of Foreign Affairs has asked for the OSA budget to be raised from around USD 20 million to nearly USD 53 million for the next fiscal year, beginning in April.

Rest of the World

The Rest of the World region captured 14.97% of the global market in 2025, generating USD 1.01 billion in revenue, and is projected to reach USD 1.08 billion in 2026. The UAV motor market is also analyzed across Latin America and the Middle East & Africa. The Middle East & Africa is expected to be the fourth-largest market in 2025. The increasing use of drones in these regions for various applications, including agriculture and military purposes, is driving market expansion. In February 2025, Sentrycs has been awarded a multi-million-dollar contract in Latin America for a national defense project. It is the largest installation of counter-drone systems in the region. The initial phase includes deploying advanced C-UAS systems to enhance airspace security across critical areas, such as military bases, special operations forces, VIP convoys, and national borders, with a focus on combating narcotics trafficking and criminal activity.

Competitive Landscape

Key Industry Players

Key players Focus on Several Strategies to Maintain a Competitive Edge, Including Research and Development Investments

Leading players in the UAV motor market are strategically focused on maintaining a competitive edge through several initiatives. A primary focus is investing in research and development to create advanced drone motor technologies that offer higher efficiency, improved performance, and enhanced reliability. These advancements are crucial as they directly impact the capabilities of drones, enabling better flight times, greater payload capacities, and enhanced maneuverability.

Continuous innovation in motor technology allows companies to meet the increasing demands of various industries, including military, security, commercial, and recreational sectors, which rely on sophisticated drone motors for their operations. In May 2024, Angel Aerial Systems launched its innovative trio airframe, and Rotor Lab assisted the businesses in the advanced strategic capabilities accelerator's innovation challenge.

LIST OF KEY DRONE MOTOR COMPANIES PROFILED

- DJI (China)

- Hacker Motor GmBH(Germany)

- KDE Direct (U.S.)

- Parrot Drone SAS (France)

- T-motor (China)

- Nidec Corporation (Japan)

- Neumotors (U.S.)

- Faulhaber Group (Germany)

- Sunnysky Motors (China)

- Mad Motor Components Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- January 2025 – Red Cat Holdings, Inc., a company specializing in drone technology that combines robotic hardware and software for military, government, and commercial uses, announced that it has obtained new orders for its Edge 130 drone from the Army National Guard and another U.S. Government Agency (OGA), amounting to USD 518,000.

- January 2025 –DroneShield Limited has secured a USD 9.7 million contract with a major Latin American military customer, facilitated through a local reseller known for its extensive defense contract experience. This deal signifies DroneShield’s growing presence in the Latin American market and highlights the demand for its counter-drone systems as the company continues its strategic expansion in the region.

- July 2024 – The Australian government planned to invest more than USD 100 million to enhance the ADF’s collection of drones for Australian military personnel. The purchase of two small unmanned aerial systems (SUAS) will strengthen the ADF’s capacity to perform surveillance and reconnaissance. It will add to the ADF’s current inventory of drones, which features various payload options.

- August 2023 –Indonesia purchased 12 surveillance and reconnaissance drones valued at USD 300 million from Turkish Aerospace Industries, intended for use by its military to enhance the country's defenses. The 12 Anka drone units are anticipated to be delivered prior to November 2025.

- May 2023-The U.S. Army chose five companies to create prototypes in a competition aimed at ultimately equipping the service with a Future Tactical Unmanned Aircraft System. Aerovironment, Griffon Aerospace, Northrop Grumman, Sierra Nevada Corp., and Textron Systems received contracts ranging from USD 1 million to USD 25 million to engage in five development phases and four option periods over the forthcoming three years.

REPORT COVERAGE

The report outlines competitive dynamics by assessing business segments, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The global UAV motor market research analysis provides a detailed insight into the market segments. Besides this, the report offers insights into the global market trends, Porter’s five forces analysis, supply chain trends, factors increasing demand for drone motors, and company profile, as well as highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the growth of the developed market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.6% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation

|

By Motor Type

|

|

By Drone Type

|

|

|

By Power Capacity

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the global drone motor market size was valued at USD 6732.1 million in 2025. The market is projected to grow from USD 7280.8 million in 2026 to USD 16301.1 million by 2034,

The market is likely to grow at a CAGR of 10.60% over the forecast period (2026-2034).

The top drone motor producers in the industry are DJI (China), Hacker Motor (U.S.), KDE Direct (U.S.), Parrot Drone SAS (France), T-motor (China), Nidec Corporation (Japan), and Constar Micromotor Co. Ltd (China).

North America dominated the market with a market size of USD 3076.01 million in 2025.

The fixed wing segment led the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us