Electric Drive Unit Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCVs, and HCVs), By Propulsion (BEV and Hybrid), By Drivetrain (Front-Wheel Drive, Rear-Wheel Drive, and All-Wheel Drive), By Component (Electric Motor, Power Electronics, Transmission/Gearbox, Differential, and Others), By Power Output (Below 100 kW, 100-250 kW, and Above 250 kW), By Sales Channel (OEM and Aftermarket), and Regional Forecasts, 2026-2034

Electric Drive Unit Market Size and Future Outlook

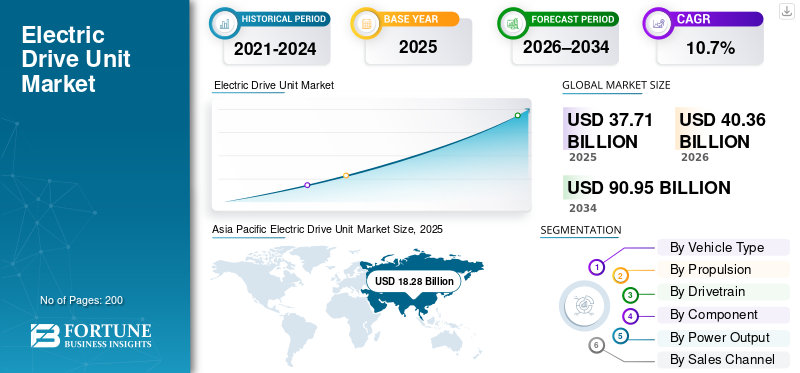

The global electric drive unit market size was valued at USD 37.71 billion in 2025. The market is projected to grow from USD 40.36 billion in 2026 to USD 90.95 billion by 2034, exhibiting a CAGR of 10.7% during the forecast period. Asia Pacific dominated the electric drive unit market with a market share of 48.47% in 2025.

The global market refers to the ecosystem of integrated propulsion modules used in electrified vehicles, typically combining an electric motor, inverter (power electronics), transmission/gear reduction and depending on design differential and thermal/cooling hardware. In simple terms, an electric drive unit integrates electric power conversion and torque delivery into a compact package that helps OEMs improve packaging, efficiency and cost. The market is expanding as electric mobility scales and the demand for electric vehicles rises across passenger cars and commercial fleets. Policy tightening is a major catalyst: the EU strengthened CO₂ standards toward a 2035 target for new cars and vans, which continues to push electrification planning and platform rollouts.

Furthermore, the drive unit market size will increasingly be shaped by three themes. First, higher integration reduces parts count and improves manufacturability, which supports stronger market growth even when pricing pressure increases. Second, battery technologies and the shift to 800V architectures accelerate adoption of SiC power electronics, improving efficiency and helping reduce operational costs for users through better energy use. Third, localization of supply chains from semiconductors to motors and gearsets will matter more as governments incentivize domestic capacity and OEMs de-risk sourcing.

Applications span vehicles BEVs, hybrids (including mild hybrids), e-axles for SUVs and light trucks, and electrified drivelines for LCVs/HCVs used in last-mile delivery and regional haul. As the key market moves from early adoption to scale, leading players such as Bosch, Magna and Valeo are investing in platform-ready, modular electric drive systems, and launching higher-efficiency products to capture market share in the fastest growing EV segments.

Download Free sample to learn more about this report.

ELECTRIC DRIVE UNIT MARKET TRENDS

“X-in-1” Integration Becomes New Design Standard Pose as Market Trend

A clear trend is deeper integration moving from 3-in-1 to “X-in-1” e-axles that bundle motor, inverter, gearbox, and additional functions into one unit. This improves packaging, reduces assembly steps, and supports cost-down efforts, strengthening market growth. It also helps suppliers offer modular electric drive systems across multiple vehicle platforms, accelerating increasing adoption in mass-market segments.

- For instance, Nidec and Renesas announced collaboration on next-generation E-Axle semiconductor solutions, aimed at integrated “X-in-1” systems combining motor and power electronics for EVs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Tightening Emissions Rules and Government Incentives Accelerate Electrification Demand

Stronger CO₂ and emissions policies are pushing OEMs to shift away from traditional internal combustion engine vehicles, expanding vehicles BEVs and hybrid portfolios. This increases the demand for such drive units as new platforms scale globally. Policy-driven rollout also supports supplier investment in localized capacity, improving supply chains and speeding commercialization leading to significant electric drive unit market growth.

- For instance, Canada’s Electric Vehicle Availability Standard sets phased targets toward 100% ZEV sales by 2035, creating clearer demand signals and encouraging new EV supply and component localization.

MARKET RESTRAINTS

Cost Pressure and Complex Sourcing Slow Near-Term Adoption Constraining Market Size

Even as electrification grows, price sensitivity and sourcing complexity can constrain the drive unit market size. High-voltage inverters, magnets, and semiconductor content can be exposed to volatility, while OEMs demand lower prices over time. When battery technologies and power electronics compete for limited materials and capacity, supply chains can tighten, delaying launches or limiting availability, moderating market growth in cost-sensitive segments.

- For instance, the IEA highlights rising demand for batteries and critical minerals as EV sales expand, underscoring how upstream constraints can affect component availability and cost.

MARKET OPPORTUNITIES

Shift Toward 800V Architectures and SiC Inverters Open Premium Efficiency Window

A major opportunity is the shift toward 800V platforms and SiC power electronics, which improve efficiency and charging performance. As OEMs chase lower energy consumption and reduced operational costs, suppliers that deliver compact, high-density e-drive packages can win long-term programs and expand market share. This supports significant growth as mid-to-premium vehicles and performance SUVs move to higher-voltage architectures.

- For instance, At IAA Mobility 2023, Valeo highlighted a next-generation electric axle using an 800V SiC inverter for higher efficiency and power density evidence of the market’s high-voltage direction.

MARKET CHALLENGES

Balancing Efficiency Gains with Affordability at Scale Limits Market Growth

A persistent challenge is delivering better performance and efficiency while keeping system costs affordable as volumes scale. OEMs want smaller, lighter electric drive systems and improved range, but they also push aggressive cost targets. Inflationary pressures and localization requirements can raise near-term capex. If suppliers cannot stabilize supply chains and manufacturing yields, price reductions may outpace cost-down, limiting profitability despite market growth.

- For instance, the IEA notes that EV battery and critical mineral demand grows with EV sales, which can create cost and sourcing pressure across the electrified powertrain value chain.

Segmentation Analysis

By Vehicle Type

SUVs Dominate Due to Strong Consumer Demand for High Power Requirements

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, LCVs, and HCVs.

SUVs dominate as they combine strong consumer demand with higher power requirements, which increases e-drive unit value per vehicle. Electrified SUVs often need higher torque, more robust thermal systems, and on many trims dual-motor setups, lifting average content. This keeps SUVs a top contributor to overall electric drive unit market share and value growth.

- For instance, BorgWarner secured 800V eMotor business for future XPeng SUV models, reflecting how SUV programs drive high-value e-propulsion content.

The HCV segment is expected to grow at a CAGR of 14.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

BEVs Lead as Thermal Needs Extend to Electrification Scales

On the basis of propulsion, the market is segmented into BEV and hybrid.

BEVs lead the global market as refrigerant compression must be electric, and thermal needs extend beyond the cabin to batteries and electronics. BEVs dominate as they rely entirely on the electric drive unit for propulsion, typically requiring higher-power e-drive architectures than hybrids. As electric mobility expands into more markets, BEV platform rollouts multiply, lifting the overall value pool for motors, inverters, and gearsets. This sustains strong long-term demand for integrated e-drive units.

- For instance, the IEA’s Global EV Outlook tracks the continued expansion of electric car markets worldwide, supporting BEV-driven e-powertrain scale-up.

The BEV segment is expected to grow at a CAGR of 12.1% over the forecast period.

By Drivetrain

Front-Wheel Drive Leads due to Growing Demand for High-Volume Electrified Platforms

On the basis of drivetrain, the market is segmented into front-wheel drive, rear-wheel drive, and all-wheel drive.

Front-wheel drive dominates as many high-volume electrified platforms prioritize packaging efficiency, lower weight, and cost-effective architecture especially in compact cars and crossovers. FWD layouts support simpler integration and lower total system cost while meeting mainstream performance needs. As OEMs scale electrification, standardized front e-drive packages become the default choice for volume programs.

- For instance, Bosch highlights compact eAxle integration (motor, power electronics, and transmission) that suits mass-market packaging needs.

The all-wheel drive segment is expected to grow at a CAGR of 12.8% over the forecast period.

By Component

Electric Motors Dominates as it Boosts Performance, Efficiency, and System Value

On the basis of component, the market is segmented into electric motor, power electronics, transmission/gearbox, differential, and others.

The electric motor dominates component value as it is central to torque delivery and scales with vehicle performance targets. Higher power density, improved winding approaches, and thermal designs directly influence efficiency and drivability, keeping motor development a core battleground. Even as integration rises, the motor remains the main value block inside the e-drive unit.

- For instance, Bosch notes its eAxles combine the electric motor with power electronics and transmission in one compact unit.

The power electronics segment is expected to grow at a CAGR of 13.4% over the forecast period.

By Power Output

Mid-Range Power Band Leads as it Balances Performance and Cost Efficiency

On the basis of power output, the market is segmented into below 100 kW, 100-250 kW, and above 250 kW.

The 100–250 kW band dominates as it covers mainstream passenger EVs and many electrified SUVs where the best mix of performance, efficiency, and cost sits. It also aligns with high-volume platform targets, making it the largest addressable power class for integrated e-drive suppliers across regions.

- For instance, Magna’s next-generation eDrive unveiled at CES 2024 targets up to 250 kW peak output, reflecting the mass-market power band focus.

The above 250 kW segment is expected to grow at a CAGR of 13.7% over the forecast period.

By Sales Channel

OEM Dominates Due to Design and Lifetime Durability

On the basis of sales channel, the market is segmented OEM and aftermarket.

OEM dominates as electric drive units are engineered as core propulsion modules installed at the factory with long service life. Replacement rates are low, and aftermarket volumes remain limited compared to the huge flow of new vehicle production. As OEMs accelerate electrification, most incremental demand stays in new-build programs.

- For instance, BorgWarner’s iDM supply award for a leading Chinese OEM’s hybrid vehicles shows OEM nominations remain the primary revenue pathway.

The aftermarket segment is expected to grow at a CAGR of 15.3% over the forecast period.

Electric Drive Unit Market Regional Outlook

By region, the global market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Electric Drive Unit Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valuing at USD 18.28 billion, and also maintained the leading share in 2024, with USD 15.45 billion. Asia Pacific dominates as it concentrates EV production scale, component ecosystems, and policy-driven electrification. China’s long-term NEV plan supports sustained rollout, while Japan and South Korea anchor advanced motors, inverters, and precision components, strengthening supply chains and enabling cost-down at volume. As affordability improves and local platforms proliferate, Asia Pacific remains the largest contributor to global e-drive value.

- For instance, DENSO announced Suzuki’s first BEV, “eVITARA”, adopts an eAxle developed with BluE Nexus and AISIN, highlighting Asia Pacific-led integration and production scaling.

China Electric Drive Unit Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 13.12 billion, representing roughly 34.8% of the global market.

India Electric Drive Unit Market

India market in 2025 was valued at around USD 0.66 billion, accounting for roughly 1.8% of global revenues.

North America

North America is projected to record a growth rate of 11.8% in the coming years, which is highest among all regions, and is projected to reach a valuation of USD 7.70 billion by 2026. North America will grow steadily as emissions rules tighten and OEMs localize electrified platforms for trucks, SUVs, and commercial fleets. The U.S. is supposed to remain the center of investment due to regulatory momentum and domestic manufacturing incentives, helping stabilize supply chains and accelerate adoption. Growth will be strongest where electrified pickups/SUVs and medium-duty delivery vehicles scale.

U.S. Electric Drive Unit Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 6.61 billion in 2026, representing roughly 17.5% of the global market.

Europe

Europe is estimated to reach USD 11.10 billion in 2026 and secure the position of the second-largest region in the market. Europe will grow as CO₂ compliance targets push OEMs to expand BEV lineups and improve drivetrain efficiency. The region also emphasizes localized manufacturing and high-efficiency power electronics, supporting sustained investment in integrated e-axles and 800V solutions.

Germany Electric Drive Unit Market

Germany market value in 2025 was recorded at around USD 0.63 billion, accounting for roughly 6.6% of global revenues.

U.K. Electric Drive Unit Market

The U.K. market in 2025 was valued at around USD 0.47 billion, accounting for roughly 4.9% of global revenues.

Rest of the World

Rest of the world growth will be driven by improving EV affordability, expanding charging networks, and fleet electrification in logistics and transit. Imports and local assembly will gradually broaden model availability, while selective incentives support adoption in priority corridors. As scale builds, demand for durable, cost-optimized e-drive units will rise.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape Driven by Need to Support Rapid Transition toward Electric Mobility

The competitive landscape of the global market is characterized by intense rivalry among established Tier-1 suppliers, powertrain specialists, and vertically integrated automotive groups. Competition is driven by the need to support the rapid transition away from traditional internal combustion engine vehicles toward electric mobility, as OEMs scale vehicles BEVs and hybrid platforms globally. Market participants compete on technology depth, manufacturing scale, cost efficiency, and their ability to secure long-term OEM programs in a key market undergoing structural change.

Leading players focus strongly on developing highly integrated electric drive systems that combine motors, inverters, and transmissions into compact units. This integration helps OEMs reduce vehicle weight, optimize packaging, and lower operational costs, making suppliers more attractive partners as electrification volumes rise. At the same time, companies are investing in next-generation battery technologies compatibility and higher-voltage architectures to improve efficiency and performance, which directly influences market share in premium and mass-market segments.

Another important strategy is strengthening regional manufacturing and localization. By expanding production footprints across Asia Pacific, Europe, and North America, suppliers improve resilience of supply chains and align with government-led localization policies and government incentives. Strategic partnerships, joint ventures, and co-development agreements with OEMs are also common, enabling faster innovation cycles and shared risk as demand for electric vehicles continues its increasing adoption trend.

Price competitiveness remains critical as the drive unit market size grows and OEMs push for cost reductions. As a result, suppliers emphasize modular product platforms that can be deployed across multiple vehicle types, from passenger cars to commercial vehicles, supporting significant growth while protecting margins. Overall, competitive advantage increasingly depends on the ability to balance scale, innovation, and cost efficiency in a fastest growing electrified powertrain environment.

- For instance, in January 2024, Magna unveiled its next-generation 800V electric drive unit at CES, focusing on higher efficiency and compact integration to strengthen its position in the global market.

LIST OF KEY ELECTRIC DRIVE UNIT COMPANIES PROFILED

- Bosch (Germany)

- ZF Friedrichshafen AG (Germany)

- Magna International (Canada)

- BorgWarner Inc. (U.S.)

- Valeo (France)

- Continental AG (Germany)

- Schaeffler AG (Germany)

- DENSO Corporation (Japan)

- AISIN Corporation (Japan)

- BluE Nexus (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Isuzu Motors announced a strategic agreement with Accelera by Cummins to source a fully integrated battery-electric powertrain for its upcoming medium-duty electric trucks in North America. The partnership supports Isuzu’s electrification roadmap while strengthening localized electric drive unit supply chains.

- January 2025: DENSO announced that Suzuki’s first battery electric vehicle, the “e VITARA,” will adopt an eAxle jointly developed with BluE Nexus and AISIN. The collaboration highlights growing use of integrated electric drive systems to improve efficiency, packaging, and scalability for global EV platforms.

- October 2024: Schaeffler confirmed completion of the merger of Vitesco into Schaeffler. The combination strengthens the group’s electrified powertrain and motion-technology portfolio.

- October 2024: Slovakia and Hyundai Mobis signed an MoU for a new EV parts plant investment in Nováky. The project reflects growing European localization of electrification component production.

- September 2024: ZF announced it will supply the CeTrax 2 dual electric central drive for Ford Trucks’ heavy-duty electric rigid truck showcased at IAA Transportation 2024. The agreement also covers future electric drive variants as models enter production.

- May 2024: AISIN and SUBARU announced collaboration and shared production of eAxles for next-generation electrified vehicles. The partnership focuses on efficiency, downsizing, and industrialization readiness.

- March 2024: BorgWarner announced additional eMotor business wins with XPeng, including 800V oil-cooled high-voltage hairpin eMotors for upcoming SUV models. The deal strengthens BorgWarner’s position in high-voltage traction motors.

REPORT COVERAGE

The global electric drive unit market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Propulsion, Drivetrain, Component, Power Output, Sales Channel, and Region |

| By Vehicle Type |

|

| By Propulsion |

|

| By Drivetrain |

|

| By Component |

|

| By Power Output |

|

| By Sales Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 37.71 billion in 2025 and is projected to reach USD 90.95 billion by 2034.

In 2025, the market value stood at USD 18.28 billion.

The market is expected to exhibit a CAGR of 10.7% during the forecast period.

SUV segment led the market by vehicle type.

The rising electrification is driving the global market.

Bosch, Valeo, ZF Friedrichshafen and Magna are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us