Electric Vehicle Fluids Market Size, Share & Industry Analysis, By Fluid Type (Battery Thermal Management Fluids, E-Transmission/E-Axle Fluids, and Others), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Propulsion Type (BEV and HEV), and Regional Forecast, 2026-2034

Electric Vehicle Fluids Market Size and Future Outlook

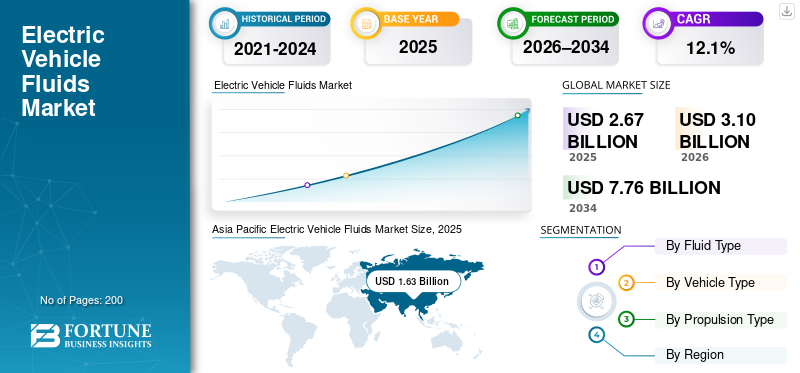

The global electric vehicle fluids market size was valued at USD 2.67 billion in 2025. The market is projected to grow from USD 3.10 billion in 2026 to USD 7.76 billion by 2034, exhibiting a CAGR of 12.1% during the forecast period. Asia Pacific dominated the electric vehicle fluids market with a market share of 61.05% in 2025.

The market comprises specialized liquids used in EVs, including thermal management fluids, coolants, lubricants, and transmission fluids. These fluids support battery cooling, power electronics efficiency, component protection, and overall vehicle performance, safety, durability, and operational efficiency across electric passenger and commercial vehicles.

Key market drivers include rising EV adoption, growing demand for battery thermal management, stricter efficiency and safety standards, advancements in fluid formulations, and increased focus on vehicle durability and performance optimization.

Key players focus on advanced thermal and dielectric fluid innovation, strategic partnerships, and EV OEM alignment. Key companies in the market include Shell, ExxonMobil, Castrol (BP), TotalEnergies, FUCHS, Valvoline, and BASF, who are driving technology leadership and global market penetration.

Download Free sample to learn more about this report.

Electric Vehicle Fluids Market Key Takeaways

- 2025 Market Size: USD 2.67 billion

- 2026 Market Size: USD 3.10 billion

- 2034 Forecast Market Size: USD 7.76 billion

- CAGR: 12.10% from 2026–2034

- Asia Pacific dominated the electric vehicle fluids market with a 61.05% share in 2025.

- The Battery Thermal Management Fluids segment accounted for the largest market share in 2025.

- The Passenger Cars segment held the dominant market share in 2025.

North America

North America market is the third-largest regional market in 2025.

Asia Pacific

Asia Pacific held 61.05% share in 2025, valued at USD 1.63 billion.

Europe

Europe is the second-largest regional market and is projected to grow at a CAGR of 11.70%.

U.S.

Market estimated at USD 0.26 billion by 2026.

Japan

Asia Pacific remained a key market, driven by strong EV adoption and manufacturing activities in Japan during 2025.

Read More

ELECTRIC VEHICLE FLUID MARKET TRENDS

Shift toward Dielectric and Immersion Cooling Fluids as a Key Market Trend

A major trend in the market is the growing adoption of dielectric and immersion cooling fluids. As battery energy density and power output increase, conventional air or indirect liquid cooling methods are reaching their performance limits. Immersion cooling allows direct contact between fluids and battery cells or electronic components, offering superior heat transfer and improved safety. OEMs are increasingly exploring this technology to support fast charging, extend battery life, and enhance vehicle performance. This trend is driving innovation in fluid chemistry, with a focus on low conductivity, chemical stability, and recyclability, reshaping product portfolios and long-term technology roadmaps.

MARKET DYNAMICS

MARKET DRIVERS

Rising Electric Vehicle Adoption to Drive Specialized Fluid Demand

The rapid global adoption of electric vehicles is a primary driver for the electric vehicle fluids market. Increasing EV sales across passenger and commercial segments are expanding the installed base, requiring advanced thermal management, cooling, and lubrication solutions. Unlike internal combustion vehicles, EVs rely heavily on efficient heat dissipation for batteries, power electronics, and electric motors to ensure safety, performance, and longevity. This creates sustained demand for high-performance coolants, dielectric fluids, and specialized lubricants. Government incentives, stricter emission regulations, and OEM electrification strategies are accelerating EV adoption, directly boosting the demand for EV-specific fluids. As EV platforms diversify across vehicle classes and power outputs, the fluid demand per vehicle is also increasing, strengthening long-term electric vehicle fluids market growth.

- According to the International Energy Agency (IEA), the electric car sales in 2025 were expected to exceed 20 million worldwide to represent more than one-quarter of cars sold worldwide. The sales were up 35% year-on-year in the first three months of 2025, with record first-quarter sales in all major markets.

MARKET RESTRAINTS

Limited Fluid Replacement Frequency to Restrain Growth in Market Revenue

Electric vehicles require significantly fewer routine fluid changes as they lack engines, multi-speed transmissions, and exhaust systems. Many EV fluids, particularly coolants and e-drive lubricants, are designed for long service intervals or lifetime use under normal operating conditions. This reduces recurring aftermarket demand and limits volume growth, especially in the early years of EV ownership. While OEM fill demand continues to rise with EV production, lower replacement frequency restrains long-term revenue expansion. This structural difference in maintenance behavior compared to ICE vehicles moderates overall market growth despite increasing EV parc size.

MARKET OPPORTUNITIES

Expansion of Fast-Charging Infrastructure to Create New Growth Opportunities

The rapid expansion of fast- and ultra-fast-charging infrastructure presents a significant opportunity for the electric vehicle fluids market. High charging speeds generate substantial heat in batteries, cables, and power electronics, increasing the need for advanced thermal management solutions. This is driving the demand for next-generation coolants and immersion fluids capable of managing extreme temperature loads while maintaining electrical safety. As charging networks expand globally, especially along highways and in urban hubs, OEMs and infrastructure providers are increasingly collaborating with fluid suppliers to develop tailored solutions. This trend opens new revenue streams beyond vehicles, extending EV fluid applications into charging systems and energy management equipment.

- In April 2025, IONITY announced the procurement of Alpitronic HYC1000 units and the rollout of up to 600 kW charging points in H2 2025. Higher heat loads strengthen the need for advanced battery/electronics thermal fluids.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Ensuring Material Compatibility across Diverse EV Platforms to Challenge Market Expansion

A key challenge in the electric vehicle fluids market is ensuring consistent material compatibility across rapidly evolving EV architectures. Batteries, seals, coatings, and electronic components vary widely by OEM and model, requiring fluids to perform reliably without causing degradation, corrosion, or electrical risk. Continuous innovation in battery chemistries and lightweight materials further complicates formulation stability and validation. Fluid manufacturers must invest heavily in testing and OEM-specific approvals, increasing research and development timelines and operational complexity. Managing this compatibility challenge at scale is critical to maintaining product reliability, OEM trust, and long-term market competitiveness.

Segmentation Analysis

By Fluid Type

Rising Battery Safety Requirements to Drive Battery Thermal Management Fluids Segmental Dominance

Based on segmentation by fluid type, the market is classified into battery thermal management fluids, e-transmission/e-axle fluids, and others.

The battery thermal management fluids segment dominate the electric vehicle fluids market due to their critical role in maintaining optimal battery temperature, safety, and performance. As battery packs account for a significant share of EV cost and directly influence range and lifespan, OEMs prioritize advanced cooling solutions. Increasing fast-charging adoption, higher-energy-density batteries, and stricter safety standards are accelerating the adoption of high-performance coolants and dielectric fluids across passenger and commercial EVs, ensuring sustained OEM-fill demand and long-term volume growth.

The e-transmission/e-axle fluids segment is the second-largest and is projected to grow at a CAGR of 11.5% over the forecast period. The rising adoption of integrated e-drive units, which combine motors, gearboxes, and power electronics, is driving the demand for multifunctional fluids that provide lubrication, cooling, and electrical compatibility, particularly in high-performance and premium electric vehicles.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

High Global EV Passenger Car Parc and OEM Electrification Focus to Drive Passenger Car Segmental Dominance

Based on vehicle type, the market is categorized into passenger cars and commercial vehicles.

The passenger cars segment dominates the electric vehicle fluids market due to their large and rapidly expanding global EV parc. High production volumes of electric hatchbacks, sedans, and SUVs ensure strong OEM-fill demand for battery thermal management, e-axle, and cooling fluids. Frequent model launches, platform upgrades, and the rapid expansion of fast-charging capability in passenger EVs further elevate fluid performance requirements. Strong adoption across private ownership, urban electric mobility, and ride-hailing fleets sustains continuous demand, reinforcing the segment’s dominant contribution to overall market revenues.

The commercial vehicle segment is the second-largest and is projected to grow at a CAGR of 14.8% over the forecast period. Expanding electrification of delivery vans, buses, and medium-duty trucks is increasing the demand for robust thermal management and drivetrain fluids capable of handling higher loads, longer operating hours, and fast-charging cycles.

By Propulsion Type

High Battery Intensity and Advanced Thermal Requirements to Drive BEV Segmental Dominance

Based on propulsion type, the market is segmented into BEV and HEV.

The battery electric vehicles (BEVs) segment dominates the global electric vehicle fluids market share due to their complete reliance on large battery packs and high-power electric drivetrains. BEVs require advanced battery thermal management fluids, dielectric coolants, and e-axle lubricants to ensure safety, efficiency, and durability. Increasing BEV adoption across passenger cars and commercial fleets, coupled with the expansion of fast charging and higher-energy-density batteries, significantly increases per-vehicle fluid demand, reinforcing the segment’s leading share in the global market revenues.

The HEV segment is projected to grow at a CAGR of 15.2% over the forecast period. The continued adoption of hybrids as a transitional technology supports steady demand for both electric drivetrains and conventional thermal management fluids, particularly in regions with gradual electrification policies.

Electric Vehicle Fluids Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Electric Vehicle Fluids Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and remains the fastest growing electric vehicle fluids market, driven by a strong EV manufacturing ecosystem and accelerating adoption in China, Japan, South Korea, and India. China’s large-scale EV production, leadership in battery manufacturing, and rapid deployment of fast charging drive high demand for battery thermal management and e-drive fluids. Supportive government policies, cost-competitive production, and expanding passenger and commercial EV fleets further strengthen regional growth, resulting in the highest CAGR over the forecast period.

China Electric Vehicle Fluids Market

In 2025, the China market reached a value of around USD 1.54 billion, accounting for a significant share of global market revenues. Growth is supported by massive EV adoption, domestic battery production, and government electrification policies.

India Electric Vehicle Fluids Market

The India market touched a valuation of around USD 0.01 billion in 2025, accounting for a small but rapidly rising share of the global market revenues. Growth is fueled by EV incentives, urban electrification, and expanding local manufacturing.

Europe

Europe holds the second-largest share of the electric vehicle fluids market and is projected to grow at a CAGR of 11.7% during the forecast period. Strict CO₂ emission regulations, aggressive electrification targets, and a strong presence of global OEMs are accelerating EV production across Germany, France, and the Nordic countries. The growing adoption of fast-charging infrastructure and premium EV platforms is driving the demand for advanced thermal and dielectric fluids, supporting sustained regional expansion.

Germany Electric Vehicle Fluids Market

The Germany market hit a value of around USD 0.19 billion in 2025, accounting for a notable share of global market revenues. Growth is driven by premium EV production, stringent regulations, and demand for advanced thermal management solutions.

U.K. Electric Vehicle Fluids Market

The U.K. market touched a value of around USD 0.10 billion in 2025, accounting for a moderate share of the global market revenues. Growth is supported by EV transition targets, rising battery electric vehicle adoption, and aftermarket demand.

North America

North America represents the third-largest electric vehicle fluids market, driven by increasing BEV adoption in the U.S. and Canada. Federal and state-level incentives, expanding charging networks, and investments by major OEMs in electric platforms support demand growth. Higher uptake of electric pickups, SUVs, and commercial fleets increases requirements for robust battery cooling and drivetrain fluids, ensuring stable OEM-fill demand despite moderate aftermarket replacement cycles.

U.S. Electric Vehicle Fluids Market

The U.S. market is estimated at around USD 0.26 billion in 2026, accounting for a substantial share of global market revenues. Growth is propelled by EV sales expansion, battery innovation, and strong OEM investments.

Rest of the World

The market in the rest of the world, including Latin America, the Middle East, and Africa, is witnessing gradual growth in the electric vehicle fluids market. Government-led electrification initiatives, rising fuel costs, and pilot deployments of electric buses and delivery fleets are driving initial demand. While EV penetration remains lower than in developed regions, improvements in infrastructure and regulatory support are expected to create long-term growth opportunities for fluid suppliers.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Leverage Global Distribution Networks and Portfolio Development as Key Strategies to Gain Edge

The electric vehicle fluids market is led by established global lubricant manufacturers and chemical companies, including Shell, ExxonMobil, BP Castrol, TotalEnergies, FUCHS, Valvoline, BASF, and Chevron. These Tier-1 players leverage deep formulation expertise, global distribution networks, and long-standing OEM relationships to maintain competitive advantage. Companies are increasingly developing EV-specific portfolios encompassing battery thermal-management fluids, dielectric coolants, and e-axle lubricants, aligned with evolving EV architectures. Strategic collaborations with EV OEMs, battery manufacturers, and power electronics suppliers enable early-stage co-development and platform-specific fluid validation. Market leaders are investing in advanced R&D, high-purity base stocks, and sustainability-focused formulations, including low-toxicity and recyclable fluids. Digital simulation, thermal modeling, and extensive testing capabilities support faster product commercialization. Additionally, players are expanding regional production, securing long-term OEM supply contracts, and pursuing acquisitions to strengthen technological capabilities and global market presence.

LIST OF KEY ELECTRIC VEHICLE FLUID COMPANIES PROFILED

- ExxonMobil Corporation (U.S.)

- Royal Dutch Shell plc (Netherlands)

- Castrol Limited (BP plc) (U.K.)

- TotalEnergies SE (France)

- Fuchs SE (Germany)

- Valvoline Inc. (U.S.)

- Petroliam Nasional Berhad (Malaysia)

- Saudi Arabian Oil Company (Saudi Aramco) (Saudi Arabia)

- PTT LUBRICANTS (PTT Group) (Thailand)

- ENEOS Corporation (Japan)

- Gulf Oil International Ltd (U.K.)

- Repsol S.A (Spain)

- Quaker Houghton (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: ExxonMobil continued to advance synthetic EV fluids that balance e-motor lubrication, thermal management, and electrical properties for next-generation electric drivetrains, boosting OEM collaborations.

- November 2025: Shell announced that its EV-Plus Thermal Fluid can manage thermal loads of entire BEV powertrains with a single-fluid design, reducing component complexity and boosting battery/power electronics cooling performance across extreme environments.

- October 2025: Prestone revealed its EVX collection of EV and hybrid thermal management fluids meeting new industry standards at The Battery Show North America.

- September 2025: Shell Lubricants developed an EV thermal management fluid enabling EV battery charging from 10% to 80% in under 10 minutes while maintaining safety and thermal stability.

- April 2025: Castrol launched high-performance fully synthetic EV Transmission Fluids (W2 and W5) tailored for wet e-motors to improve efficiency and durability.

- August 2024: Castrol launched a new range of high-performance fully synthetic EV fluids designed for wet e-motors used in electric vehicles, enhancing efficiency and durability for increasingly electrified drivetrains.

- May 2024: TotalEnergies Lubrifiants established the first standardized specifications for Electric Drive System (EDS) fluids to improve performance and consistency for EV and hybrid applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.1% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Fluid Type, By Vehicle Type, By Propulsion Type, and By Region |

|

By Fluid Type |

· Battery Thermal Management Fluids · E-Transmission / E-Axle fluids · Others |

|

By Vehicle Type |

· Passenger Cars · Commercial Vehicles |

|

By Propulsion Type |

· BEV · HEV |

|

By Geography |

· North America (By Fluid Type, By Vehicle Type, By Propulsion Type, and by Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Fluid Type, By Vehicle Type, By Propulsion Type, and by Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Fluid Type, By Vehicle Type, By Propulsion Type, and by Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Fluid Type, By Vehicle Type, By Propulsion Type, and by Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.67 billion in 2025 and is projected to reach USD 7.76 billion by 2034.

In 2025, the market value stood at USD 1.63 billion.

The market is expected to exhibit a CAGR of 12.1% during the forecast period of 2026-2034.

The passenger car segment leads the market by vehicle type.

The rising adoption of electric vehicles is a key factor driving the market.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us