Electronic Stability Control System Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Vehicle (Hatchback, Sedan, SUV, MPV) and Commercial Vehicle (Light Commercial Vehicle, Heavy Commercial Vehicle)), By Component (Hydraulic Modulator, Sensors, and ECU), and Regional Forecasts, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

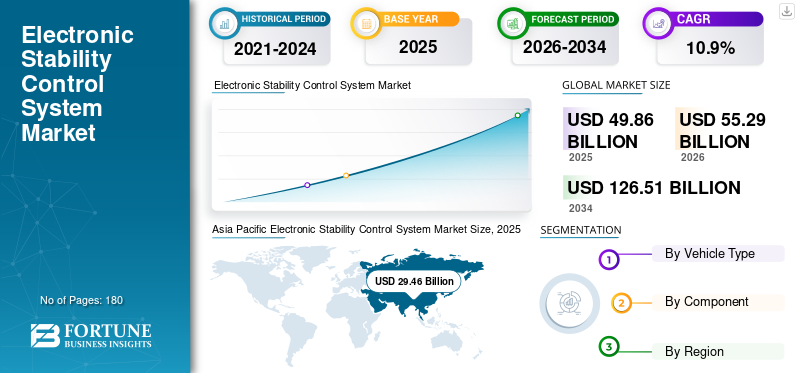

The global electronic stability control system market size was valued at USD 49.86 billion in 2025. The market is projected to grow from USD 55.29 billion in 2026 to USD 126.51 billion by 2034, exhibiting a CAGR of 10.90% during the forecast period. Asia Pacific dominated the electronic stability control system market with a market share of 59.09% in 2025. The Electronic Stability Control System Market in the U.S. is projected to grow significantly, reaching an estimated value of USD 10669.40 million by 2030.

Electronic Stability Control (ESC) System, also known as the electronic stability program, is an active safety system that can be fitted to cars, coaches, buses, and trucks. The system is an extension of antilock braking technology, consisting of a speed sensor and independent breaking for all the wheels. The primary objective of ESC is to prevent vehicle skidding under various driving conditions and situations.

This market is expected to grow healthy due to the increasing demand for advanced vehicles with high-end safety features. ESC controls the lateral stability of the vehicle during unusual situations. Global vehicle safety organization NCAP has also updated its protocols to make ESC a standard feature in newly sold vehicles to achieve a 5-star rating. With increasing road and vehicle safety demand, many manufacturers have equipped ESC as a standard vehicle fitment. Governments in different countries have made ESC mandatory on heavy vehicles to increase accident avoidance rates.

Governments globally have been implementing stricter safety regulations for automobiles. Many countries, including the U.S., European Union, and Australia, have made these systems mandatory in new vehicles. This has been a critical driver for the adoption of these systems. Moreover, consumers have become more conscious of vehicle safety features with growing awareness of road safety. ESC systems are recognized as effective safety technologies, providing improved vehicle stability and reducing the risk of accidents, especially in challenging driving conditions. These systems have evolved, incorporating additional features and functionalities. Enhanced versions, such as Electronic Stability Programs (ESP) and advanced ESC systems, offer improved performance and functionality, further driving the market growth.

Download Free sample to learn more about this report.

Electronic Stability Control System Market Key Takeaways

- 2025 Market Size: USD 49.86 billion

- 2026 Market Size: USD 55.29 billion

- 2034 Forecast Market Size: USD 126.51 billion

- CAGR: 10.90% during 2026–2034

- Asia Pacific dominated the market with a 59.09% share in 2025.

- The Passenger Vehicle segment held the largest market share in 2025.

- The Hydraulic Modulator segment is projected to account for 58.7% of the market in 2026.

Asia Pacific

Asia Pacific valued at USD 29.46 billion in 2025 and projected to reach USD 32.67 billion in 2026.

North America

Government mandates and rising consumer focus on vehicle safety support steady market growth.

Europe

Stringent vehicle safety regulations and OEM competition continue driving ESC system adoption.

U.S.

Electronic stability control system market is projected to reach USD 10,669.40 million by 2030.

Japan

Mandatory safety regulations and advanced vehicle manufacturing support sustained ESC system demand.

Read More

ELECTRONIC STABILITY CONTROL SYSTEM MARKET TRENDS

Development and Adoption of Autonomous Mobility to Drive the Electronic Stability Control System Market Growth

The market is extremely surging due to the growing road safety demand. Market players in the automotive industry have invested heavily in Research & Development (R&D) to advance ESC systems. R&D efforts are focused on enhancing the capabilities and effectiveness of ESC systems, improving their performance, and expanding their applicability. Companies such as Bosh are investing heavily in the R&D of these systems. Autonomous vehicles rely heavily on various sensors, cameras, and advanced control systems to navigate and operate safely on the roads. Safety is paramount in autonomous mobility, as these vehicles must operate without human intervention. These systems play a vital role in ensuring the stability and control of the vehicle, especially during dynamic driving situations. As autonomous mobility advances, the demand for electronic stability control systems as a crucial safety component will likely increase.

Download Free sample to learn more about this report.

DRIVING FACTORS

Increasing Government Regulations Related to Vehicle Safety Globally to Propel Market Growth

The increasing safety standards and increasing government regulations regarding road and vehicle safety are significant factors driving the growth of the market. These systems have been compulsory for new vehicles in the European Union from November 2011 onward. The regulation requires all new vehicles to be equipped with these systems that meet specific performance and functionality standards. This regulation was implemented to improve road safety and diminish the threat of accidents caused by loss of control. The introduction of this regulation significantly increased the demand for these systems in the market. Automakers were required to incorporate ESC systems into their vehicles to comply with the legislation, leading to a surge in the installation of electronic stability control systems. This, in turn, propelled market growth as manufacturers had to ramp up production and supply to meet the regulatory requirements.

There is a growing effort among governments globally to harmonize safety regulations to ensure consistent standards across different regions. This harmonization aims to facilitate international trade and the exchange of vehicles across borders. As more countries align their regulations with international standards that include mandatory ESC system installation, the market is expected to expand.

RESTRAINING FACTORS

Limited Availability of Raw Materials May Restrain Market Growth

The limited availability of raw materials can restrain the market growth. The components used in producing ESC systems, such as electronic components, sensors, and specialized materials, may experience supply disruptions due to natural disasters, geopolitical issues, trade restrictions, or unforeseen events such as the COVID-19 pandemic. These disruptions can lead to shortages or delays in the production of these systems, affecting market growth. When the availability of raw materials is limited, the prices tend to rise. Escalating costs of raw materials can impact the manufacturing costs of these systems. This can impact the demand and overall growth of the market. Manufacturers may explore alternative materials or technologies in response to raw material unavailability. However, adopting alternative materials can lead to additional research and development efforts and testing, potentially compromising ESC systems' performance or reliability. This can result in delays and impact the pace of market growth.

SEGMENTATION ANALYSIS

By Vehicle Type Analysis

Passenger Vehicle Segment Dominates the Market Owing to the Growing Safety Awareness due to Rise in Number of Road Accidents

Based on vehicle type, the market is segmented into passenger vehicle (Hatchback, Sedan, SUV, MPV) and commercial vehicle (Light Commercial Vehicle, Heavy Commercial Vehicle).

The passenger vehicle segment dominated the market in 2025 with the leading electronic stability control system market share. The increasing demand for passenger vehicles is expected to drive these systems. With a growing emphasis on safety, consumers increasingly know the importance of advanced safety features in vehicles. ESC systems, known for their effectiveness in preventing loss of control and enhancing stability, are considered vital safety features. As consumer demand for safer vehicles rises, passenger vehicles equipped with ESC systems also increase. Automakers strive to differentiate their vehicles in the highly competitive market. Advanced safety features, including these systems, can be a significant selling point for passenger vehicles. Automakers often market ESC systems as a key safety technology, attracting consumers who prioritize safety features, thus driving the demand for these systems.

The growing commercial vehicle segment is expected to grow significantly over the forecast period. Commercial vehicles, such as buses and trucks, often carry heavy loads and operate in diverse driving conditions. These systems help improve the stability and handling of these vehicles, especially during situations such as sudden lane changes, high-speed maneuvers, or adverse road conditions. The integration of these systems enhances safety for commercial vehicles and drivers, passengers, and other road users, making them a valuable feature for fleet operators and buyers. The increasing sales of commercial vehicles are one of the substantial factors propelling the growth of the market.

By Component Analysis

To know how our report can help streamline your business, Speak to Analyst

Early Adoption of Hydraulic Modulators is anticipated to Boost Segment Growth

The market is divided into hydraulic modulator, sensors, and ECU based on component.

The hydraulic modulator segment is projected to dominate the market with a share of 58.7% in 2026. Hydraulic modulators have been used in these systems for several years and have proven effective in enhancing vehicle stability. They are based on hydraulic pressure modulation and work with the vehicle's brake system to control stability. Hydraulic modulators are known for their robustness, reliability, and relatively low cost, making them a preferred choice for many automotive manufacturers. Automakers have widely adopted hydraulic modulators in many vehicles equipped with ESC systems. This dominance is partly due to the early introduction of ESC systems, where hydraulic modulators were the prevalent technology. While hydraulic modulators have historically dominated the market, the market will gradually shift toward other technologies as automakers and suppliers continue to innovate and adapt to changing requirements and preferences.

The demand for sensors is expected to grow during the forecast period. The demand for automotive electronic stability control system sensors is closely tied to the overall demand for ESC vehicle systems. As these systems become increasingly mandated or desired in vehicles for safety purposes, the demand for these system sensors also increases. With an increased focus on road safety, consumers are increasingly aware of the importance of advanced safety features in vehicles. These systems, a well-established safety technology, rely on various sensors to detect and respond to vehicle dynamics. As more consumers prioritize safety in vehicle purchases, the demand for ESC system sensors rises.

REGIONAL ANALYSIS

Asia Pacific

Asia Pacific Electronic Stability Control System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia to Hold the Highest Market Share Due to Increasing Awareness Regarding Road Safety among Vehicle Buyers

Asia Pacific dominated the market with a valuation of USD 29.46 billion in 2025 and USD 32.67 billion in 2026. The Asia Pacific region, particularly countries such as China and India, has experienced significant growth in vehicle sales over the past decade. As more vehicles are being sold and put on the roads, the demand for safety features, including ESC systems, has also increased. There is an increasing emphasis on vehicle safety in Asia, driven by regulatory requirements and consumer awareness. Governments in countries such as Japan, South Korea, China, and Australia have implemented regulations mandating the installation of these systems in new vehicles. This has led to a surge in demand for ESC systems to meet regulatory compliance.

Europe

Also, the demand for ESC systems is anticipated to grow in the Europe market. The demand for electronic stability control systems in Europe has been significant and continues to grow. Europe has been at the forefront of implementing stringent safety regulations and promoting vehicle safety, driving the demand for these systems. Market competition among OEMs further drives the demand for these systems in the region.

North America

In North America, the demand for ESC systems has been driven by several factors, including government regulations, consumer preferences, and increased awareness of vehicle safety. Government regulations mandating the inclusion of ESC systems in new vehicles have played a significant role in increasing their adoption. For instance, in the U.S., the National Highway Traffic Safety Administration (NHTSA) made ESC mandatory for all light vehicles starting from the 2012 model year.

Rest of the World

The Rest of World has been witnessing significant growth in the automotive sector, with a rising number of vehicles on the road. As road infrastructure continues to develop, there is an increasing emphasis on improving road safety. These systems play a vital role in enhancing vehicle stability and reducing the risk of accidents caused by skidding or loss of control, making them a desirable feature for many consumers.

KEY INDUSTRY PLAYERS

Robert Bosch GmbH is a Leading Players in the Market, with Well-established Market Network

Robert Bosch GmbH. is a leading Electronic Stability Program (ESP) provider in Gerlingen, Germany. The company provides ESP solutions to various major automakers such as Daimler. Bosch also provides ESP value-added functions, including software functions with added values. Moreover, Bosch has also developed the ESP system for motorcycles. The company has manufactured more than 250 million electronic stability control systems now.

LIST OF KEY COMPANIES PROFILED:

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Delphi Automotive LLP (U.K.)

- WABCO (France)

- Hitachi Automotive System Ltd. (Japan)

- Autoliv Inc. (Sweden)

- Knorr-Bremse AG (Germany)

- Mando Corp (South Korea)

- Johnson Electric (Hong Kong)

KEY INDUSTRY DEVELOPMENTS

- In May 2023, Continental Ag, one of the leading vehicle parts manufacturers, supplied Chinese vehicle manufacturer Changan with its innovative electronic brake systems for Electronic Stability Control, the MK 120 ESC.

- In May 2023, Hyundai, one of the leading auto manufacturers, confirmed safety features on its upcoming SUV Exter, which also involves an electronic stability control system with 6 airbags as standard fitment.

- In February 2023: ZF, a prominent German manufacturer specializing in active and passive vehicle safety systems, is optimistic about India's strong market potential for electronic stability control system supplies. The company has engaged in developmental initiatives for advanced active safety technologies for vehicles at its technical center in Hyderabad, India.

- In June 2022, Maruti Suzuki launched its all-new Brezza, equipped with advanced safety features such as airbags, ABS with EBD, ESC system, and others. These features are expected to support the new Brezza to accomplish a 5-star score in the Global NCAP crash test ratings.

- In January 2021, ZF Friedrichshafen AG, a leading global provider of ESC systems, launched its newest brake system designed for electric vehicles. This new brake control system will be standard in Volkswagen’s ID.3 & ID.4 models and Volkswagen Group’s globally marketed MEB modular e-drive system platform.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The market report provides detailed market analysis and focuses on key aspects such as leading companies, services, and product applications. Besides this, the report offers insights into the market trends and highlights vital industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the market's growth in recent years.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.9% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

|

|

By Component

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights reports that the global market was valued at USD 49.86 billion in 2025 and is projected to reach USD 126.51 billion by 2034.

The market is predicted to grow at a CAGR of 10.9% during the forecast period.

Growing awareness regarding road safety is expected to drive market growth.

Asia Pacific dominated the electronic stability control system market with a market share of 59.09% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us