Embolotherapy Market Size, Share & Industry Analysis, By Product (Embolic Agents {Liquid Embolic Agents and Microspheres}, Embolization Coils {Detachable Coils and Pushable Coils}, Flow Diverters, Detachable Balloons, Vascular Plugs/Plug Systems, and Support Devices), By Application (Oncology, Peripheral Vascular Diseases, Neurology, Urology & Nephrology, and Others), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Embolotherapy Market Size and Future Outlook

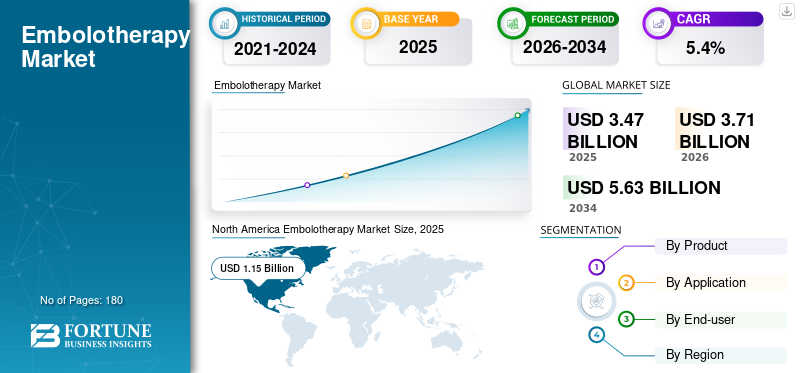

The global embolotherapy market size was valued at USD 3.47 billion in 2025. The market is projected to grow from USD 3.71 billion in 2026 to USD 5.63 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. North America dominated the global embolotherapy market with a market share of 33.14% in 2025.

Embolotherapy is a minimally invasive, catheter-based approach that intentionally blocks blood flow to abnormal vessels or target tissue, commonly used to treat tumors, control acute hemorrhage, manage vascular malformations, or treat aneurysms with flow diverters and coils. The therapy demand is rising as clinicians and health systems prefer procedures that can shorten the length of stay, reduce surgical trauma, and expand treatment eligibility for older or higher-risk patients. The clinical pull is especially strong in interventional oncology and neurovascular care, where procedure volumes track disease burden and specialist adoption.

- For example, WHO’s cancer agency highlighted that ~20 million new cancer cases were estimated globally in 2022 and warned that service capacity remains uneven, creating strong pressure for scalable, image-guided therapies.

Furthermore, Medtronic, Stryker Corporation, Boston Scientific Corporation, and Terumo Corporation hold the largest market share. This is driven by surging investments and strategic initiatives, such as new product launches and collaborations.

Download Free sample to learn more about this report.

Embolotherapy Market Key Takeaways

- 2025 Market Size: USD 3.47 Billion

- 2026 Market Size: USD 3.71 Billion

- 2034 Forecast Market Size: USD 5.63 Billion

- CAGR: 5.4% from 2026–2034

- North America dominated the embolotherapy market with a 33.14% share in 2025.

- The oncology segment is projected to hold a 41.4% share in 2026.

- The hospitals segment is expected to account for an 85.4% share in 2026.

Asia Pacific

Asia Pacific is expected to reach USD 0.93 billion in 2026.

North America

North America generated USD 1.15 billion in 2025.

Europe

Europe is projected to reach USD 1.01 billion in 2026, growing at a 4.4% CAGR during the forecast period.

U.S.

The embolotherapy market is projected to reach USD 1.07 billion in 2026, accounting for approximately 29.0% of global revenue.

Japan

The embolotherapy market is projected to generate USD 0.20 billion in 2026, contributing nearly 5.3% of the global market.

Read More

EMBOLOTHERAPY MARKET TRENDS

Preferential Shift toward Next-gen Embolic Agents and Improvement in Deliverability

A defining trend is the shift from “commodity embolization” toward engineered embolic materials and precision delivery systems. In embolic agents, the emphasis is on predictable deployment, sustained drug elution, and the ability to support repeat interventions.

- For example, Terumo Europe’s April 2024 launch of BioPearl, a resorbable drug-eluting microsphere, illustrates how manufacturers are differentiating through material science and longitudinal treatment considerations instead of merely through particle sizing.

In parallel, deliverability is being treated as a product category in its own right. New microcatheter designs are being developed with a focus on trackability, torque, embolic compatibility, and longer working lengths for radial access.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Use of Minimally Invasive Embolization across Oncology and Vascular Disease to Fuel the Market Growth

A primary factor driving embolotherapy market growth is the widening clinical footprint of embolization as a first-line or adjunct therapy in multiple high-volume conditions. In oncology, embolization is closely linked to liver cancer care pathways. Companies continue to invest in drug-eluting and next-generation microspheres to improve repeatability and preserve future treatment options. On the vascular side, growth is supported by the shift from open surgery toward endovascular management of aneurysms, AVMs, and bleeding, where embolization coils, plugs, and flow diverters are central.

- For instance, in May 2024, Merit Medical announced FDA 510(k) clearance for its Siege vascular plug and related embolic delivery products, which illustrate the ongoing portfolio build-out in peripheral embolization tools.

Thus, the underlying disease burden and the expanding patient pool that need embolization therapy are likely to boost the global market.

MARKET RESTRAINTS

Reimbursement Variability, Evidence Gaps by Indication, and Budget Constraints to Limit Market Growth

Despite strong clinical momentum, adoption is uneven as embolotherapy spans many indications with different evidence strengths and payer expectations. Hospitals may readily adopt established use cases but are slower to scale newer outpatient or niche procedures when reimbursement is unclear or documentation requirements are heavy. Moreover, embolotherapy is a device-intensive procedure that often requires microcatheters, guidewires, coils/agents, and, at times, adjunct imaging tools. Hence, procurement teams scrutinize total case cost and frequently push OEMs and distributors on pricing and contracting terms.

Furthermore, the lack of hospital and healthcare infrastructure in emerging and developing countries restricts market growth. Hence, embolization adoption can lag in lower-resource settings, even when clinical need is high. This combination, cost control, variable reimbursement maturity, and uneven infrastructure, creates friction that can delay broad-based uptake.

MARKET OPPORTUNITIES

Underpenetrated Countries, Outpatient Expansion, and Imaging/Software that Improves Consistency to Create Significant Growth Opportunities

The biggest upside lies in markets where embolization is clinically relevant but underutilized due to specialist shortages and limited cath lab capacity, as well as in procedures moving from tertiary centers into high-throughput hospital systems and selected outpatient settings. Growth opportunities also arise when companies make embolotherapy easier to execute well, reducing variability between operators and shortening procedure time.

On the device side, differentiated embolic agents and delivery tools can expand repeat-treatment pathways and broaden patient eligibility. Moreover, as clinical trial ecosystems mature and regulators continue to clear next-generation devices, manufacturers gain room to pursue indication expansions and upgrade cycles that lift ASPs in premium segments.

MARKET CHALLENGES

Complexity of Procedure, Lack of Trained Interventionalists, and Inconsistent Supply Chains to Challenge Market Growth

Embolotherapy’s complexity is a real market challenge. Outcomes depend on devices as well as on anatomy, catheter technique, embolic selection, and intraprocedural decision-making. This makes training and reproducibility central issues, especially as embolization expands beyond top-tier academic centers. Even within mature segments such as neurovascular flow diversion, post-market performance management remains critical.

Another challenge is aligning product innovation with real-world purchasing constraints. Hospitals often evaluate embolotherapy through total procedure economics, including multiple disposables per case, contrast/imaging utilization, and staff time. When systems are under budget pressure, OEMs can face slow adoption of premium embolics or next-gen platforms unless clinical differentiation is clear and reimbursement is stable.

Finally, geographic scalability is hard. WHO’s February 2024 note that many countries do not adequately finance priority cancer and palliative services reflects broader capacity gaps, limited imaging infrastructure, fewer trained interventionalists, and inconsistent supply chains, which can suppress the adoption of embolization even when clinical need exists. Addressing these challenges requires products and training ecosystems, evidence generation, and service models that fit local health-system realities.

Segmentation Analysis

By Product

Wide Adoption of Embolic Agents in Several Procedures to Drive the Segment Growth

Based on product, the market is segmented into embolic agents, embolization coils, flow diverters, detachable balloons, vascular plugs/plug systems, and support devices. Furthermore, embolic agents are further classified into liquid embolic agents and microspheres. Similarly, embolization coils are further classified into detachable coils and pushable coils.

The embolic agents segment holds the largest revenue as they are used in high volume across repeated procedures and multiple indications, especially in interventional oncology and peripheral embolization.

Additionally, the vascular plugs/plug systems segment is projected to grow at a CAGR of 5.5% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Wide Product Utilization in Oncology to Propel the Segment Growth

By application, the market is classified into oncology, peripheral vascular diseases, neurology, urology & nephrology, and others.

The oncology segment leads the embolotherapy market share as embolization is deeply embedded in loco-regional cancer care, particularly for liver tumors, where catheter-based therapies are used when surgery is not feasible or as part of multi-step management. Moreover, product innovation also clusters around oncology use cases, drug-eluting and next-gen microspheres, and workflow tools designed to make complex embolizations more predictable, supporting higher utilization. Moreover, the segment is projected to hold a 41.4% share in 2026.

Additionally, the urology & nephrology segment is estimated to grow at a CAGR of 9.2% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals to Propel the Segment Growth

On the basis of end-user, the market is classified into hospitals and ASCs, specialty clinics, and others.

The hospitals and ASCs segment dominates as embolotherapy is image-guided, device-intensive, and often performed in hybrid ORs, angio suites, or advanced cath labs that require capital equipment, trained teams, and 24/7 support for urgent bleeding and neurovascular events. Large centers also run the highest-throughput oncology and neurovascular programs, which drive steady demand for embolic agents, coils, plugs, and flow diverters. Furthermore, the segment is set to hold 85.4% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 7.9% during the forecast period.

Embolotherapy Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Embolotherapy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, with a value of USD 1.08 billion, and reached USD 1.15 billion in 2025. North America’s embolotherapy market is pushed forward by a steady shift toward minimally invasive care for oncology, hemorrhage control, and complex vascular disease, especially where faster recovery and shorter hospital stays matter. The region also benefits from deep procedure capacity, and a strong willingness to adopt newer embolic technologies when they improve deliverability, imaging follow-up, or procedural efficiency. Furthermore, high healthcare spending supports quicker diffusion of premium devices and combination therapies, which is important for interventional oncology and peripheral embolization use cases.

U.S. Embolotherapy Market

In 2026, the U.S. market is estimated to touch USD 1.07 billion, capturing 29.0% of total global revenue.

Europe

Europe is expected to achieve a 4.4% growth rate in the coming years, the second-highest globally, reaching USD 1.01 billion by 2026. Europe’s growth is underpinned by demographics and system-level demand. An aging population increases the pool of patients with cancer, peripheral vascular disease, and aneurysm/bleeding risk conditions where embolization is frequently used either as definitive therapy or as an adjunct. Broad coverage across many countries and relatively high baseline healthcare spending sustain the adoption of embolotherapy across tertiary centers, while structured care pathways create a predictable procedure flow.

U.K. Embolotherapy Market

The U.K. market is projected to reach USD 0.15 billion by 2026, accounting for 4.0% of the global market revenue.

Germany Embolotherapy Market

Germany's embolotherapy market is estimated to reach about USD 0.19 billion by 2026, representing roughly 5.1% of the global revenue.

Asia Pacific

In 2026, the Asia Pacific embolotherapy market is predicted to be valued at USD 0.93 billion, ranking as the third-largest globally. The region is the fastest-growing in terms of volume as it has the largest patient pool and rising treatment capacity, even though lower OEM ASPs and uneven reimbursement often moderate revenue per case. Growth is concentrated in major urban hospitals where cath-lab density and specialist availability are improving and where governments/private providers are investing in advanced imaging and IR services.

Japan Embolotherapy Market

The Japan market is projected to generate approximately USD 0.20 billion in revenue by 2026, contributing nearly 5.3% to the global market.

China Embolotherapy Market

China’s embolotherapy market is estimated to reach approximately USD 0.26 billion by 2026, contributing about 7.1% to global revenues.

India Embolotherapy Market

The India market is poised to contribute approximately USD 0.10 billion to the embolotherapy market by 2026, corresponding to about 2.7% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa markets are anticipated to witness moderate growth, with Latin America expected to reach around USD 0.36 billion by 2026. The Latin America market growth is largely driven by an expanding oncology workload and the need to improve access to modern, less resource-intensive interventions. As cancer cases rise, health systems and private providers increasingly prioritize scalable treatment pathways, including minimally invasive options that can reduce inpatient burden.

GCC Embolotherapy Market

By 2026, the GCC market is expected to generate approximately USD 0.07 billion, accounting for nearly 1.8% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The global embolotherapy market is moderately concentrated and competitive, with large multinational medical device manufacturers dominating. Major players compete on the basis of novel product innovation, regulatory approvals, clinical evidence, and strategic partnerships to develop and commercialize minimally invasive devices for clinical needs. Key players such as Medtronic, Stryker Corporation, Boston Scientific Corporation, and Terumo Corporation hold the largest market share.

Other key players in market comprise Johnson & Johnson, Abbott Laboratories, Merit Medical Systems, Inc., and Cook Medical, among others. These companies compete based on ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve procedural outcomes.

LIST OF KEY EMBOLOTHERAPY COMPANIES PROFILED

- Medtronic (Ireland)

- Stryker Corporation (U.S.)

- Boston Scientific Corporation (U.S.)

- Terumo Corporation (Japan)

- Johnson & Johnson (U.S.)

- Abbott Laboratories (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Cook Medical (U.S.)

- Braun (Germany)

- Balt Group (France)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Boston Scientific announced a definitive agreement to acquire Penumbra. This acquisition will help expand Boston Scientific's cardiovascular portfolio and further address the increasing prevalence of vascular diseases.

- November 2025: Kaneka Corporation began selling its i-ED COIL, a brain aneurysm embolization coil, in Europe in October. The product obtained EC certification under the EU Medical Device Regulation in July and will be distributed primarily in Europe through Kaneka Medical Europe N.V.

- September 2025: Penumbra Inc., the world’s leading thrombectomy company, secured CE Mark for its SwiftPAC neuro embolization coil. Commercially available in Europe, the coil forms part of the Swift™ Coil System.

- September 2025: Sirtex Medical, a leading manufacturer of minimally invasive interventional oncology solutions, received an expanded CE Mark approval for SIR-Spheres Y-90 resin microspheres for the treatment of patients with liver cancer.

- September 2025: Siemens Healthineers company Varian announced that its Embozene microspheres received CE Marking for GAE (Genicular Artery Embolisation) for knee osteoarthritis. This achivement makes Embozene the first and only embolic agent to secure the GAE-specific CE Mark.

- July 2025: Sirtex Medical, a major interventional oncology solutions manufacturer, announced that the U.S. FDA approved SIR-Spheres Y-90 resin microspheres for the treatment of unresectable HCC (hepatocellular carcinoma) in the U.S.

- June 2025: Embolization, Inc., received 510(k) clearance from the U.S. FDA for its Nitinol Enhanced Device (NED). The NED is a vascular embolization device intended for venous and arterial embolization in the peripheral vasculature.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Application, End-user, and Region |

|

By Product |

|

|

By Application |

|

|

By End-user |

|

|

By Geography |

Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.47 billion in 2025 and is projected to reach USD 5.63 billion by 2034.

In 2025, the market value stood at USD 1.15 billion.

The market is expected to exhibit a CAGR of 5.4% during the forecast period of 2026-2034.

The embolic agents segment leads the market by product.

The key factors driving the market are the expanding use of minimally invasive embolization across oncology and vascular disease.

Medtronic, Stryker Corporation, Boston Scientific Corporation, and Terumo Corporation are some of the major players in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us