Encapsulation Resins Market Size, Share & Industry Analysis, By Type (Epoxy, Polyurethane, Silicone, and Others), By Application (Electronics & Consumer Devices, Automotive & E-Mobility, Industrial & Electrical Equipment, Energy & Utilities Infrastructure, and Others) and Regional Forecast, 2026-2034

ENCAPSULATION RESINS MARKET SIZE AND FUTURE OUTLOOK

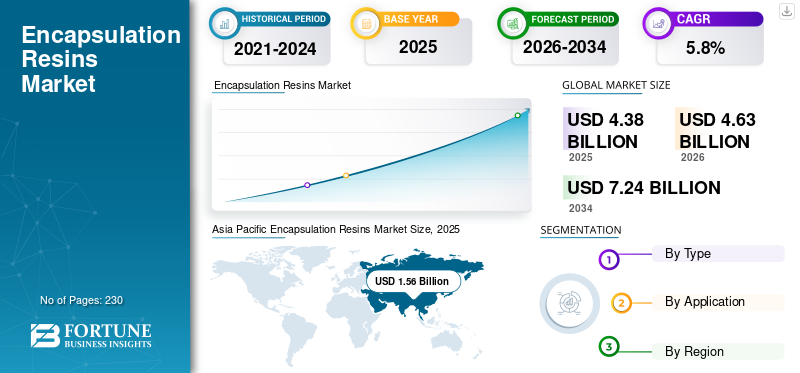

The encapsulation resins market size was USD 4.38 billion in 2025. The market is projected to grow from USD 4.63 billion in 2026 to USD 7.24 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period. Asia Pacific dominated the encapsulation resins market with a market share of 35.62% in 2025.

Encapsulation resins are formulated polymer systems used to surround, seal, and protect electronic, electrical, and industrial components from moisture, dust, vibration, thermal cycling, chemicals, corrosion, and electrical stress. They are typically based on epoxy, polyurethane, silicone, or specialty chemistries and are used in PCBs, sensors, transformers, power modules, LEDs, EV electronics, battery systems, and renewable-energy equipment. A major market driver is the rapid growth of electrification and power electronics, particularly in electric vehicles, charging infrastructure, solar inverters, battery energy storage, and smart-grid systems. In these applications, component reliability, insulation, thermal management, and long service life are critical. Henkel Adhesive Technologies, Dow, Shin-Etsu Chemical Co., Ltd., Momentive and Huntsman are few key players operating in the market.

Download Free sample to learn more about this report.

ENCAPSULATION RESINS MARKET TRENDS

Shift from Basic Protection to Performance Engineering is Emerging Market Trend

A major trend in the industry is the shift from simple component protection toward advanced, performance-engineered materials. As electronic devices are increasingly used in harsher environments, customers require resins that can deliver moisture resistance, electrical insulation, vibration protection, thermal stability, flame resistance, and long-term reliability. This is driving stronger demand for silicone gels, thermally conductive epoxies, flame-retardant systems, low-stress materials, and customized formulations. Suppliers are also moving beyond standard resin sales by offering application support, qualification assistance, and system-level material solutions for increasingly complex electronic and electrical assemblies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Electrification Leading to Increase in Demand for Reliable Electronic Protection Drives Market Growth

The key demand driver for encapsulation resins market growth is the rapid expansion of electrification across mobility, energy, industrial, and infrastructure sectors. Electric vehicles, charging systems, renewable-energy equipment, battery storage, smart grids, automation, and connected devices all require reliable protection for sensitive electrical and electronic components. Encapsulation resins help protect power modules, sensors, inverters, battery systems, control units, transformers, and circuit boards from heat, moisture, chemicals, vibration, and electrical stress. As more products become electronically controlled and power-dense, manufacturers increasingly rely on encapsulation solutions to improve durability, safety, and operating life.

MARKET RESTRAINTS

Premium Resin Costs Limiting Adoption in Cost-Sensitive Applications Restrains Market Growth

A key market restraint is the higher cost of advanced encapsulation resin systems compared with simpler protective alternatives. Specialty silicones, thermally conductive epoxies, flame-retardant formulations, optical encapsulants, and low-stress materials often require expensive raw materials, engineered fillers, strict processing, and extensive testing. In price-sensitive consumer electronics, appliances, basic electrical assemblies, and low-voltage applications, customers may reduce resin usage, select lower-cost grades, or use conformal coatings where full encapsulation is not essential. Long qualification cycles also make material substitution difficult, which can slow adoption of newer or more sustainable formulations despite their performance benefits.

MARKET OPPORTUNITIES

Increasing need for Thermal Management Opens a Lucrative Growth Opportunities

A major opportunity lies in encapsulation resins designed for thermal management, fire safety, and high-reliability power electronics. As devices become smaller, more powerful, and more exposed to demanding operating conditions, customers need materials that protect components while also helping manage heat and electrical stress. This creates strong opportunities for thermally conductive epoxies, silicone encapsulants, flame-retardant polyurethane systems, and hybrid materials. Applications including EV powertrains, battery systems, solar inverters, charging equipment, data infrastructure, and industrial automation are creating demand for premium formulations that offer higher performance and stronger differentiation for suppliers.

MARKET CHALLENGES

Complex Design Trade-Offs Make Material Selection Difficult and Limits Market Growth

A critical challenge in the industry is the complexity of selecting the right material for each application. Epoxy offers strength and adhesion but can be rigid and difficult to rework. Polyurethane offers flexibility and shock resistance but may be less suitable for high-temperature environments. Silicone resins provides low-stress protection and thermal cycling resistance but is typically more expensive. Filled systems improve thermal conductivity but can increase viscosity, processing difficulty, and equipment wear. Poor material selection can lead to cracking, voids, incomplete curing, adhesion failure, or field reliability issues, making validation and supplier support significant.

SEGMENTATION ANALYSIS

By Type

High-Strength Electrical Insulation Requirements to Drive Epoxy Segment

Based on the type, the market segment includes epoxy, polyurethane, silicone and others.

The epoxy segment is anticipated to hold the largest encapsulation resins market share during the forecast period. Demand for epoxy-based encapsulation resins is primarily driven by their strong fit in electrical insulation, structural protection, and harsh-environment applications. Epoxy systems offer high adhesion, mechanical strength, chemical resistance, and dielectric performance, making them suitable for transformers, power modules, relays, sensors, industrial controls, and automotive electronics. As electrification expands across vehicles, renewable energy, grid equipment, and factory automation, manufacturers increasingly use epoxy encapsulants to improve component durability, reduce field failures, and protect electronics from moisture, vibration, and electrical stress.

Demand for silicone-based encapsulation resins is also growing driven by the growth of sensitive, high-value electronics exposed to thermal cycling, vibration, and outdoor conditions. Silicone systems provide flexibility, low mechanical stress, temperature stability, and strong resistance to moisture and weathering, making them well suited for EV electronics, LEDs, solar inverters, sensors, battery systems, and power modules. As electronic assemblies become smaller, more power-dense, and more reliability-critical, silicone encapsulants are increasingly preferred where component protection must be achieved without emphasizing on delicate circuits. The segment is anticipated to rise with a CAGR of 6.5% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Automotive Electrification Is Raising Electronic Protection Requirements and Driving Automotive & E-Mobility Segment Growth

Based on the application, the market is segmented into electronics & consumer devices, automotive & E-mobility, industrial & electrical equipment, energy & utilities infrastructure and others.

The automotive & E-mobility segment is anticipated to hold the dominant share during the forecast period. Demand for encapsulation resins in automotive and e-mobility is driven by the rapid increase in vehicle electrification and electronic content. EVs, hybrids, and advanced vehicles require protected battery management systems, inverters, onboard chargers, DC-DC converters, ADAS modules, sensors, and charging connectors. These components face heat, vibration, moisture, electrical stress, and long service-life expectations. Encapsulation resins help improve reliability, insulation, flame resistance, and durability, making them increasingly critical as automakers shift toward safer, more power-dense electric platforms. This, in turn drives segment growth.

Demand in energy and utilities infrastructure is driven by rising investment in renewable energy, battery storage, smart grids, and power distribution systems. Solar inverters, wind turbine electronics, stationary energy storage, smart meters, grid monitoring devices, transformers, and utility power modules require protection from moisture, thermal cycling, dust, electrical stress, and outdoor exposure. Encapsulation resins support long-term reliability and reduce failure risk in mission-critical infrastructure. As power networks become more decentralized, digitalized, and renewable-heavy, demand for durable protective resin systems continues to grow. The segment is anticipated to rise with a CAGR of 6.3% over the forecast period.

ENCAPSULATION RESINS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Encapsulation Resins Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounts for the largest market share and is expected to maintain its dominance during the forecast period. In this region, the major demand driver is electronics and consumer device manufacturing, supported by EVs, batteries, semiconductors, LEDs, and renewable-energy electronics. China, Japan, South Korea, India, and ASEAN countries form the world’s largest electronics production ecosystem, creating large-volume demand for encapsulation resins in PCBs, chargers, sensors, appliances, displays, modules, and power supplies. Similarly, EV production, solar inverters, battery systems, and industrial automation are increasing demand for higher-performance silicone and epoxy systems. The region’s scale and manufacturing depth make it the largest consumption base, driving market growth.

Japan Encapsulation Resins Market

Japan’s market was at USD 0.18 billion in 2025, equivalent to around 4.1% of global sales.

China Encapsulation Resins Market

China’s market reached USD 0.78 billion in 2025, equivalent to around 17.8% of global sales.

India Encapsulation Resins Market

India’s market was valued at USD 0.21 billion in 2025, equivalent to around 4.8% of global e sales.

North America

In North America, the major demand driver for encapsulation resins is the growth of automotive and e-mobility electronics, supported by grid modernization and data infrastructure. EV platforms, battery management systems, onboard chargers, inverters, DC-DC converters, ADAS modules, and charging systems require protection from heat, vibration, moisture, and electrical stress. The U.S. also has strong demand from aerospace, defense electronics, industrial automation, and data-center power systems, which support use of high-performance epoxy, silicone, and thermally conductive encapsulants. This makes reliability-critical electronics the key growth engine for the regional market.

U.S. Encapsulation Resins Market

The U.S. market is projected to be one of the largest worldwide, and its revenues was at USD 0.95 billion in 2025, representing roughly 21.7% of global sales.

Europe

In Europe, demand is primarily driven by automotive and e-mobility, particularly premium vehicles, EV power electronics, battery systems, ADAS modules, and charging infrastructure. European automakers and component suppliers require encapsulation resins that support long service life, flame resistance, thermal cycling performance, and electrical insulation. Additionally, demand from renewable-energy systems, rail electronics, industrial automation, and grid infrastructure also boosts the market, where components must operate reliably under demanding environmental conditions. Europe’s strong focus on electrification, energy transition, and high-reliability engineering supports steady adoption of epoxy, silicone, and polyurethane encapsulation systems.

U.K. Encapsulation Resins Market

U.K.’s market was at USD 0.13 billion in 2025, equivalent to around 3.0% of global sales.

Germany Encapsulation Resins Market

Germany’s market reached USD 0.31 billion in 2025, equivalent to around 7.1% of global sales.

Latin America

In Latin America, product demand is mainly driven by industrial and electrical equipment, supported by automotive electronics and renewable-energy infrastructure. Brazil and Mexico consume encapsulation resins in transformers, motors, pumps, relays, switchgear, power supplies, industrial controls, connectors, and appliance electronics. Mexico’s automotive and electronics manufacturing base supports demand for sensors, modules, and EV-related components, while Brazil’s industrial and utility sectors support electrical insulation and rugged protection applications. Solar, grid upgrades, telecom, and mining equipment are additional demand drivers where encapsulation resins help improve reliability in harsh operating environments.

Brazil Encapsulation Resins Market

Brazil’s market was at USD 0.12 billion in 2025, equivalent to around 2.7% of global sales.

Middle East & Africa

In the Middle East & Africa, demand is driven by energy and utilities infrastructure, supported by oil and gas electronics, telecom, and industrial equipment. Solar projects, grid expansion, utility transformers, smart meters, power distribution systems, and stationary energy equipment require encapsulation resins for moisture protection, insulation, thermal stability, and outdoor durability. Oil and gas facilities also use protected sensors, controls, pumps, motors, and communication equipment in harsh environments. As the region invests in power reliability, renewables, electrification, and infrastructure modernization, epoxy and silicone encapsulants gain relevance across mission-critical systems.

Saudi Arabia Encapsulation Resins Market

Saudi Arabia’s market was at USD 0.07 billion in 2025, equivalent to around 1.6% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Competition is Driven by the Presence of Large Specialty Chemical Companies and Silicone Producers

The global encapsulation resins industry is moderately consolidated, with competition led by large specialty chemical companies, silicone producers, adhesive formulators, and electronics-material specialists. Leading players compete on formulation know-how, thermal conductivity, dielectric performance, flame retardancy, cure speed, reliability testing, customization, and global technical support. The market is becoming more performance-driven as EVs, renewable energy, power electronics, sensors, and industrial automation require higher-reliability protection materials. Regional formulators remain important in cost-sensitive applications, but global suppliers dominate premium electronics and automotive-grade systems. Few of the major key players include Henkel Adhesive Technologies, Dow, Shin-Etsu Chemical Co., Ltd., Momentive and Huntsman, among others.

LIST OF KEY ENCAPSULATION RESINS COMPANIES PROFILED

- CHT Group (Germany)

- Dow (U.S.)

- Electrolube (U.K.)

- B. Fuller Company (U.S.)

- Henkel Adhesive Technologies (Germany)

- Huntsman (U.S.)

- Momentive (U.S.)

- Parker Hannifin Corp (U.S.)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Wacker Chemie AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Dow launched DOWSIL EG-4175 Silicone Gel, a protective material for next-generation IGBT modules in EVs and renewable energy systems. With resistance up to 180°C, self-healing properties and strong dielectric performance, the gel supports higher voltages, improved reliability, lower power losses and greater efficiency in advanced inverter applications.

- April 2024: Huntsman introduced new SHOKLESS polyurethane foam systems for EV battery cell potting, fixation and encapsulation. Designed for cell, module and pack protection, the lightweight foams offer thermal and structural support, fast processing, low viscosity and stable elastic performance from -35°C to 80°C, helping OEMs improve battery durability and safety.

- September 2022: Henkel commercialized Loctite Eccobond UF 9000AG, a semiconductor-grade capillary underfill for advanced flip chip packaging. The epoxy-based material combines high filler loading, ultra-low CTE, fast flow, low warpage and strong thermal reliability, supporting advanced silicon node integration in mobile, automotive electronics and computing applications.

- July 2022: Shin-Etsu Chemical and Taiwan’s ITRI jointly developed a new encapsulant material for Mini LED displays. Offering high transparency, light resistance, large-area moldability, strong adhesion and stress relaxation. The material has shown adaptability across transparent, flexible and high-definition displays.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Volume (Kiloton); Value (USD Billion) |

| Growth Rate | CAGR of 5.8% during 2026-2034 |

| Segmentation | By Type, By Application, and By Geography |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 4.38 billion in 2025 and is projected to record a valuation of USD 7.24 billion by 2034.

In 2025, Asia Pacific stood at USD 1.56 billion.

Registering a CAGR of 5.8%, the market will exhibit steady growth during the forecast period of 2026-2034.

The automotive & E-mobility application is expected to lead this market during the forecast period.

Global electrification expands demand for reliable electronic protection, driving market growth.

Henkel Adhesive Technologies, Dow, Shin-Etsu Chemical Co., Ltd., Momentive and Huntsman are the major players operating in the market.

Asia Pacific held the highest share in the market.

Rising demand for reliable, durable electronics across EV’s, renewable energy, industrial automation, and connected devices to drive wider adoption of encapsulation resins.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us