Europe Armored Vehicle Turret System Market Size, Share and Industry Analysis, By Platform (By Military Armored Vehicles and By Infantry Fighting Vehicles), By Component, By Turret Type (Manned Turret, Unmanned Turret, Remote Controlled Weapon System (RCWS), and Hybrid, Modular Mission Turret), By Caliber Range, By Weapon Category, By Offering Type. By Procurement Type, By End User and Regional Forecasts 2026-2034

Europe Armored Vehicle Turret System Market Size and Future Outlook

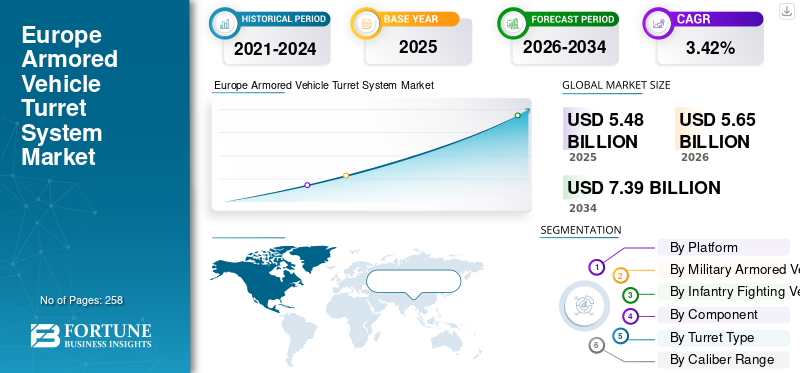

The Europe armored vehicle turret system market size was valued at USD 5.48 billion in 2025. The market is projected to grow from USD 5.65 billion in 2026 to USD 7.39 billion by 2034, exhibiting a CAGR of 3.42% during the forecast period. Germany dominated the europe armored vehicle turret system market with a market share of 20.26% in 2025.

The turret systems of armored vehicles are rotating, armored weapon stations installed primarily on tanks, infantry fighting vehicles, armored personnel carriers, and certain naval and airborne variants. They combine weapons such as guns or missile launchers with fire control computers, electro-optical/infrared sensors, stabilization systems, and armor protection to provide accurate fire even when the platform is moving. Modern turrets are increasingly designed for manned, unmanned, and remotely controlled operation, enabling crews to engage "under armor" and avoid direct fire exposure.

In Europe, the demand for turret systems is increasing in tandem with defense budgets, with the modernization of armored vehicles and land systems, fueled by increasing geopolitical tensions, particularly after the Russia-Ukraine conflict, and a return to the focus on NATO's 2% of GDP guideline for defense spending. European developments tend to focus on upgrading existing legacy platforms with new medium-caliber and remote-controlled turrets, as well as advanced sensors and active protection systems, rather than simply acquiring new, clean-sheet designs.

In terms of competitive structure, the industry is moderately concentrated around a nucleus of major international primes such as Rheinmetall, BAE Systems, Elbit Systems, Leonardo, and General Dynamics, alongside certain niche players such as Kongsberg, John Cockerill, Moog, and Rafael. Rival firms compete on the basis of integrating advanced fire control, electro-optics, stabilization, and increasingly AI-based target recognition capabilities, as well as on modular designs that can be retrofitted to a variety of host platforms.

Download Free sample to learn more about this report.

Europe Armored Vehicle Turret System Market Trend

AI-Enabled Sensor Fusion and Cognitive Fire Control Redefine Precision Engagement Catalyze the Market Trends

Artificial intelligence integration within turret sensor suites fuses electro-optical, infrared, synthetic aperture radar, and hyperspectral inputs to achieve persistent 360-degree situational awareness at operationally relevant ranges exceeding 10 kilometers.

Cognitive fire control algorithms, leveraging neural processing architectures, execute predictive threat engagement under 2-second timelines, adapting ballistic solutions to dynamic maneuvers and environmental perturbations in real time.

Machine learning models trained on synthetic battlefields enable autonomous target classification with 97% confidence intervals against civilian discrimination challenges, as validated through NATO's 2025 Tactical Interoperability Demonstrations. Quantum-enhanced edge computing processors mitigate electronic warfare degradation, preserving first-shot lethality in GPS-denied and RF-saturated spectra.

Distributed aperture systems with gallium arsenide detectors deliver hyperspectral discrimination of camouflage netting at 8km slant ranges, fundamentally altering reconnaissance-strike complexes. Adaptive optics countermeasures neutralize laser dazzlers while enhancing EO/IR resolution through atmospheric turbulence compensation.

Download Free sample to learn more about this report.

Market Dynamics

MARKET DRIVER

Rising Geopolitical Tensions and Defense Modernization Driving Market Development

Strategic imperatives in Europe are propelling demand for advanced turret systems as NATO members prioritize fleet modernization amid persistent threats from Eastern borders. Elevated defense spending, with nations such as Poland and the Baltics accelerating armored vehicle upgrades, underpins a procurement cycle emphasizing modular turrets for rapid deployment and interoperability.

Collaborative frameworks such as the European Defence Fund (EDF) streamline funding for next-generation systems, fostering joint development efforts across member states. OEMs including Rheinmetall report sustained contract inflows, exemplified by their February 2025 announcement of a turret integration deal for German Boxer vehicles, enhancing firepower and survivability.

Border security enhancements in response to hybrid warfare tactics further amplify requirements for remotely operated turrets with precision strike capabilities. National industrial policies incentivize local production, reducing supply chain vulnerabilities while bolstering economic multipliers through job creation in high-tech manufacturing hubs.

MARKET RESTRAINT

Budgetary Constraints and Fiscal Prioritization Hamper the Market Expansion Pace

Austerity measures persisting in several European economies cap defense outlays, forcing trade-offs between turret systems and competing priorities such as air and cyber domains. Inflationary pressures on raw materials, including rare earths for sensors, erode purchasing power for high-end turrets, compelling OEMs to optimize cost architectures.

Delays in multinational funding disbursements under EDF, as noted in the European Commission's December 2025 audit, hinder prototype acceleration.

Stringent export licensing regimes restrict technology transfers, constraining scale economies for dual-use turret components. Workforce skill shortages in precision engineering hubs such as Bavaria and Piedmont slow production ramps, with industry associations reporting 20% vacancy rates in 2025.

Overreliance on legacy supply chains exposes vulnerabilities to disruptions, as seen in post-2024 semiconductor shortages impacting electro-optic modules. Political fragmentation in coalition governments stalls long-lead turret programs, exemplified by Belgium's paused Piranha turret upgrade in September 2025 per NATO procurement logs.

MARKET OPPORTUNITY

Strategic Autonomy and Export Potential Unlock New Revenue Streams and Opportunities for Market Growth

EU Push for technological sovereignty positions turret OEMs to capture intra-European upgrades, with PESCO projects channeling funds to indigenous developers. Expanding Middle East and Indo-Pacific markets offer offset-driven entry points, leveraging modular designs for regional variants.

Rheinmetall's April 2025 MoU with Qatar for turret co-production exemplifies diversification. Digital twin technologies enable predictive maintenance contracts, transforming one-time sales into recurring revenue over 20-year lifecycles. Hybrid propulsion integrations create upsell paths for next-gen turrets, aligning with net-zero mandates.

European strategic autonomy imperatives, reinforced through the EU's 2025 Strategic Compass update, position turret system providers to dominate upgrade programs for legacy platforms such as the Puma and Warrior fleets, prioritizing sovereign supply chains that mitigate transatlantic dependencies.

MARKET CHALLENGES

Industrial Fragmentation and Supply‑Chain Vulnerabilities Weigh On the Market Growth

Europe's armored‑vehicle sector is marked by overlapping platforms, non‑standardized turret interfaces, and parallel national solutions, limiting economies of scale and interoperability benefits. Critical subsystems, engines, optics, electronics, and some protection technologies often depend on non‑EU suppliers, exposing turret programs to export‑license risk and geopolitical shocks. Capacity constraints, underinvestment in heavy manufacturing, and legacy facilities restrict the ability to ramp production rapidly in response to urgent operational requirements, as highlighted by the demand surge triggered by the Russia–Ukraine war.

SEGMENTATION ANALYSIS

By Platform

Growing Modernization Program of Military Armored Vehicles within the Region Drives the Market Growth

By platform, the market is divided into military armored vehicles and infantry fighting vehicles.

Among the platform segment, the military armored vehicles sub-segment dominated the market in 2025. The segment accounted for a 53.12% share in 2025. The growth is expansions, European forces are emphasizing modernization of existing MBTs (e.g., Leopard 2 and Challenger 2 upgrades). Consequently, new tank procurements are limited (aside from notable orders by countries such as Poland), and increasing investment in tanks is going into mid-life upgrades and collaborative future tank programs, resulting in a strong fleet incremental Europe armored vehicle turret system market growth.

The infantry fighting vehicles sub-segment is estimated to be growing during the forecast period with a CAGR of 11.95% and accounted for a 46.88% share.

By Military Armored Vehicles

Ongoing Russia/Ukraine War Drives MBT Fleet Growth for Border Security

By military armored vehicle, the segment is further divided into main battle tank (MBT), light / medium tank, air-defense / counter-UAS vehicle, self-propelled artillery vehicle, mortar carriers vehicle, anti-tank / missile combat vehicles, direct-fire assault guns / fire-support vehicles, and rocket / loitering-munition launch vehicles.

Among the military armored vehicles segment, the main battle tank (MBT) sub-segment dominated the market in 2025, accounted for 39.15% share. The growth of Major European MBT programs is focused on modernisation and interoperability. The U.K's Challenger 3 upgrade (Rheinmetall‑BAE joint venture) replaces Challenger 2's rifled gun with a 120 mm smoothbore turret, adds modular armor, advanced sights, and Trophy APS. In addition, Germany is planning to procure 105 new Leopard 2A8 tanks (120 mm turret guns) under a USD 2.99 billion deal for its forces (including a brigade in Lithuania)

Air-Defense / Counter-UAS Vehicle sub-segment is estimated to be the fastest growing during the forecast period with a CAGR of 3.76% and accounted for 23.03% share.

By Infantry Fighting Vehicles

Increasing Investments in Scout Vehicles and Armored Personnel Carrier APCs Fuel Market Growth

By infantry fighting vehicles, the segment is further divided into armored reconnaissance/surveillance vehicle, amphibious armored vehicle, armored personnel carrier, uncrewed ground vehicle (UGV), command-and-control (C2) vehicle, and electronic warfare / sigint / comint vehicle.

Among infantry fighting vehicles, the armored personnel carrier segment dominated the market in 2025. The segment accounted for a 54.53% share in 2025. The growth is driven by Germany, and other European armies are investing heavily in dedicated scout vehicles. In October 2025, the Bundeswehr contracted General Dynamics for ~274 new Luchs‑2 reconnaissance vehicles, each outfitted with networked sensor suites and communications gear supplied by Hensoldt and Rheinmetall.

Moreover, NATO armies such as France (Jaguar 6×6) and Sweden (CV90 variants) follow suit, fielding turreted scout vehicles with advanced mast-mounted radars and day-night optics. Germany's contract even includes an option to buy 82 more scouts (for a total of 356) into the next decade, underscoring that growth in this segment is driven by multi-role turret packages that blend reconnaissance sensors with organic firepower.

The Uncrewed Ground Vehicle (UGV) sub-segment is anticipated to grow at the highest CAGR of 7.41% during the forecast period.

By Component

Rising Retrofit/MRO Demand Boosts Sighting, Observation & Target Acquisition, and Other Components

By component, the segment is further divided into structural & mechanical assemblies, armament & weapon integration, fire control & ballistic processing, sighting, observation & target acquisition, electro-optical & infrared subsystems, laser & directed sensor elements, drive, actuation & stabilization systems, power supply & energy management, and others.

Among the components, the sighting, observation & target acquisition segment dominated the market in 2025. The segment accounted for a 21.82% share. The growth is driven by the Turret designs, which increasingly include panoramic and stabilized sight systems for all-weather, 360° coverage. For instance, HENSOLDT is supplying 288 sets of digital optronic sight systems (PERI RTWL HD commander's sight and WAO HD gunner's sight) for Germany's Boxer RCT30/Schakal turrets, a shift to "software-enabled" vision units in lieu of analog periscopes. The Leopard 2A8 demonstrator was unveiled with an omnidirectional observation system and digital sights.

The laser & directed sensor elements sub-segment is anticipated to grow at the fastest growth rate of 6.33% during the forecast period.

By Turret Type

Manned Turrets Fleet Dominates the Market Share With Existing Working Conditions in the Current Fleets

By turret type, the segment is further divided into manned turret, unmanned turret, Remote Controlled Weapon System (RCWS), hybrid, and modular mission turret.

Among the turret types, the manned turret segment dominated the market in 2025. The segment accounted for a 76.64% share. Large crewed turrets remain core to Europe's heavy AFVs. For example, Germany awarded KMW a contract in 2023 for 18 new Leopard 2 A8 main battle tanks (delivery from 2025), each with a fully manned 120 mm turret. Italy's recent upgrade of 76 Freccia IFV Plus vehicles similarly features a new Leonardo X-GUN 30 mm manned turret capable of airburst ammunition.

The hybrid sub-segment is projected to grow at the highest CAGR of 5.81% during the forecast period, and accounted for the 3.04% share.

By Caliber Range

Increasing Adoption of Large Caliber Guns, such as 31-40 mm, in Different Types of Vehicles Catalyze the Segmental Growth

By caliber range, the segment is further divided into below 12.7 mm, 13–20 mm, 21–30 mm, 31–40 mm, 41–60 mm, 61–90 mm, 91–105 mm, 106–125 mm, and below 155 mm.

Among the caliber range, the 31-40 mm segment dominated the market in 2025. The segment accounted for a 23.39% share in 2025. The growth is anticipated due to the larger medium-caliber cannons (35–40 mm) being adopted in Europe, especially for new IFVs and reconnaissance vehicles. For instance, the UK's Ajax family uses a 40 mm CT40 cased-telescoped autocannon in its turret, while the next-generation French EBRC Jaguar (not yet in service) has a 40 mm CTA International gun instead of the old 90 105 mm. Recent orders highlight this trend: Denmark and Sweden's new CV9035 MkIIIC IFVs will carry 35 mm Bushmaster guns in their turrets (an increase from 30 or 40 mm), and Sweden is fitting its CV90s with 35 mm Mk 44 cannons.

The Below 155 mm sub-segment is anticipated to grow at the fastest rate with a CAGR of 4.40% during the forecast period and accounted for 6.76% share.

By Weapon Category

European Armies Boost Demand for Multi-Weapon Turrets Catalyze the Segmental Growth

By weapon category, the segment is further divided into medium/large caliber cannon turrets, autocannon turrets, machine gun turrets, anti-tank guided missile (ATGM) turret systems, air-defense turret systems (guns/missiles), multi-weapon turrets (cannon + coax + atgm, etc.), and non-lethal/special mission turrets (rare, niche applications).

Among the weapon category, multi-weapon turrets (cannon + coax + ATGM, etc.) sub-segment dominated the market in 2025. The segment accounted for a 26.54% share. In addition, the segment is also projected to be the fastest growing with a CAGR of 5.06% during the forecast period. Multi-weapon turret systems are becoming increasingly mainstream as European armies seek to compress firepower into fewer, modular platforms. John Cockerill's 3030 and 3105 turrets, mounting cannons, ATGMs, and coaxial MGs, are actively marketed across Europe and have been trialed in Belgium, Turkey, and Czech programs.

Air-defense turret systems (guns/missiles) sub-segment is anticipated to grow at the highest CAGR of 4.53% during the forecast period and accounted for the 8.92% market share.

By Offering Type

Growing New Armored Vehicles with Advanced New Turret Systems Adoption by Major Countries Drives the Segmental Growth

By offering type, the segment is further divided into new turret procurement, retrofit & upgrade kits, mid-life overhaul, spares & sustainment, and software upgrades.

Among offering type, the new turret procurement segment dominated the market in 2025. The segment accounted for a 35.91% share. New turret procurement continues to dominate spending across Europe as modernization accelerates. Germany's Leopard 2A8, France's Jaguar EBRC, and Hungary's Lynx KF41 orders each include newly manufactured turrets with advanced sensor-fused capabilities and modular firepower. These contracts reflect a broader shift toward next-gen digitalized turrets with automated target tracking, AI-assisted fire control, and integrated APS (Active Protection Systems).

Software upgrades sub-segment is projected to grow at the highest CAGR of 4.70% during the forecast period and accounted for the 15.34% market share.

By Procurement Type

Ongoing OEM Integrated Manufacturing and MRO Orders by Major Governments Catalyze the Segmental Growth

Based on procurement type, the segment is further divided into OEMs integrated, Government-Furnished Equipment (GFE), framework agreement, and local production / licensed assembly.

Among procurement type, the OEMs integrated segment dominated the market in 2025. The segment accounted for a 52.94% share. OEM-integrated procurement remains the most common and dominating method across Europe due to the advantages of system maturity, testing, and single-source accountability. Countries such as Hungary (Rheinmetall Lynx), France (Nexter Jaguar), and Germany (Boxer variants) are increasingly favoring full-system turret integration by original manufacturers for seamless compatibility.

The local production / licensed assembly sub-segment is anticipated to grow at the fastest rate with a 4.49% CAGR during the forecast period and accounted for 24.18% market share.

By End User

European Border Conflicts Drive Armed Forces Segmental Dominance

By the end user, the segment is further divided into armed forces, Special Operations Forces (SOF), paramilitary forces, homeland security, and peacekeeping forces.

Among end user, the armed forces segment dominated the market in 2025. The segment accounted for a 74.28% share in 2025. National armed forces remain the principal drivers of turret system modernization across Europe, accounting for the majority of new and upgraded platforms. Germany's Puma IFVs, France's SCORPION program (Jaguar, Griffon), and Italy's Centauro II all incorporate advanced turret systems, often integrating autocannons, ATGMs, and advanced sensors. Armed forces will continue to dominate turret system demand through 2030 due to fleet renewal and multi-domain integration requirements.

The paramilitary forces sub-segment is projected to have the fastest growing CAGR of 2.96% during the forecast period and accounted for the 3.62% of the Europe armored vehicle turret system market share.

To know how our report can help streamline your business, Speak to Analyst

Europe Armored Vehicle Turret System Market Country Outlook

By countries, the market is categorized into U.K., Germany, France, Italy, Spain, Russia, Nordic Countries, and the Rest of Europe.

U.K. Armored Vehicle Turret System Market

The U.K. market in 2025 is estimated at around USD 0.84 billion, and the estimated growth rate of 1.99% during the forecast period.

Germany Armored Vehicle Turret System Market

The Germany armored vehicle turret system market growth in 2025 is estimated at around USD 1.10 billion, and the estimated growth rate of 2.63% during the forecast period.

Nordic Countries Armored Vehicle Turret System Market

The Nordic Countries armored vehicle turret system market growth in 2025 is estimated at around USD 0.86 billion, and the estimated growth rate of 5.19% during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Modernization Programs of Europe Fleet Lead the Key Manufacturers to the Market Growth

The Europe armored vehicle turret system market is an oligopolistic space dominated by a small group of European and transatlantic primes, plus a handful of specialized turret houses and remote‑weapon‑station (RWS) providers. Competition is driven more by technology maturity, platform integration credentials, and lifecycle support than by headline unit price, within a framework of strong national‑content and industrial‑policy constraints.

Across Europe, the turret system market is moderately concentrated, with the top 8–10 suppliers capturing a large majority of new‑build and upgrade opportunities. Market reports consistently identify Rheinmetall, BAE Systems, Leonardo, Elbit Systems, General Dynamics, Kongsberg, John Cockerill, and Rafael among the principal turret and RWS vendors active in European programs. Platform OEMs and integrated land‑systems houses (Rheinmetall, BAE, GDLS Europe, Nexter/KMW) often bundle proprietary turrets with vehicles, reinforcing vertical integration and raising entry barriers for stand‑alone turret challengers.

LIST OF KEY EUROPE ARMORED VEHICLE TURRET SYSTEM COMPANIES PROFILED

- Rheinmetall AG (Germany)

- KNDS Group (Netherlands)

- Leonardo S.p.A. (Italy)

- John Cockerill Defense S.A. (Belgium)

- Kongsberg Defence & Aerospace AS (Norway)

- Saab AB (Sweden)

- CTA International Ltd (U.K.)

- BAE Systems Hägglunds AB (Sweden)

- Huta Stalowa Wola S.A. (Poland)

- ROSOMAK S.A. (Poland)

- Diehl Defence GmbH & Co. KG (Germany)

- Thales S.A. (France)

- Safran Electronics & Defense (France)

- MBDA (U.K.)

KEY INDUSTRY DEVELOPMENT

- February 2026: German defense company Flensburger Fahrzeugbau Gesellschaft will build a new armored vehicle plant in Germany. The new site will produce combat armored vehicles based on the Patria 6×6 APC, as well as tracked engineering vehicles.

- February 2026: KNDS has awarded Hensoldt contracts worth around USD 472 million to supply digital optronic systems for German armored personnel carriers and main battle tanks. Delivery of the sensor packages is set to begin in 2027. Prototypes of the digital sighting systems for the Puma turret have already been delivered, with series deliveries for the Schakal scheduled to start in the fourth quarter of 2027.

- December 2025: Patria and Germany signed two contracts under the Common Armored Vehicle System (CAVS) program with a total value of over USD 2.11 billion. The contracts provide for the purchase of up to 876 Patria 6×6 armored vehicles in four variants. Among them are modifications with the Patria NEMO turret mortar system and the Kongsberg RS4 remote-controlled combat system.

- November 2025: Leonardo and Rheinmentall, as part of the Leonardo Rheinmetall Military Vehicles Joint Venture (50% Leonardo and 50% Rheinmetall AG), was awarded the first supply contract for 21 vehicles "A2CS Combat" for the Italian Army Leonardo and Rheinmetall will supply 21 tracked armoured vehicles for the Italian Army, 5 of which are Rheinmetall's Lynx KF-41 with the Lance turret followed by 16 newly configured vehicles equipped with the same chassis and Leonardo's Hitfist 30mm turret.

- April 2025: Elbit Systems Ltd. has been awarded a contract worth approximately USD 100 million to supply its advanced UT30 MK2 unmanned systems turret to General Dynamics European Land Systems (GDELS). The systems will be installed on the ASCOD armored fighting vehicles and supplied to a NATO European country.

REPORT COVERAGE

The Europe armored vehicle turret system market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and Europe armored vehicle turret system market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.42% from 2026-2034 |

| Unit | USD Billion |

| Segmentation | By Platform, By Military Armored Vehicles, By Infantry Fighting Vehicles, By Component, By Turret Type, By Caliber Range, By Weapon Category, By Offering Type, By Procurement Type, By End User |

|

By Platform

By Military Armored Vehicles

By Infantry Fighting Vehicles

By Component

By Turret Type

By Caliber Range

By Weapon Category

By Offering Type

By Procurement Type

By End User

|

|

| Countries |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.48 billion in 2025 and is projected to reach USD 7.39 billion by 2034.

The market is expected to exhibit a CAGR of 3.42% during the forecast period.

The Air-Defense / Counter-UAS Vehicle segment is expected to hold the highest CAGR over the forecast period.

Growing focus on geopolitical imperatives and defense modernization initiatives escalating European security demands and strategic investments are accelerating market expansion.

heinmetall, BAE Systems, Elbit Systems, Leonardo, and General Dynamics, alongside certain niche players such as Kongsberg, John Cockerill, Moog, Rafael, and so on.

Germany dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 258

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us