EV Thermal Management Systems Market Size, Share & Industry Analysis, By System Type (Battery Thermal Management System (BTMS), Power Electronics Thermal Management, Electric Motor Thermal Management, Cabin Thermal Management (HVAC), and Integrated Thermal Management Systems), By Technology (Air Cooling, Liquid Cooling, and Others), By Component (Compressor, Heat Exchanger, Cooling Plates/Cold Plates, Pumps & Valves, Thermal Interface Materials (TIMs), and Others), By Vehicle Type (Passenger Car, Van, Bus, and Truck), By Propulsion Type (BEV and HEV), and Regional Forecast, 2026–2034

EV Thermal Management Systems Market Size and Future Outlook

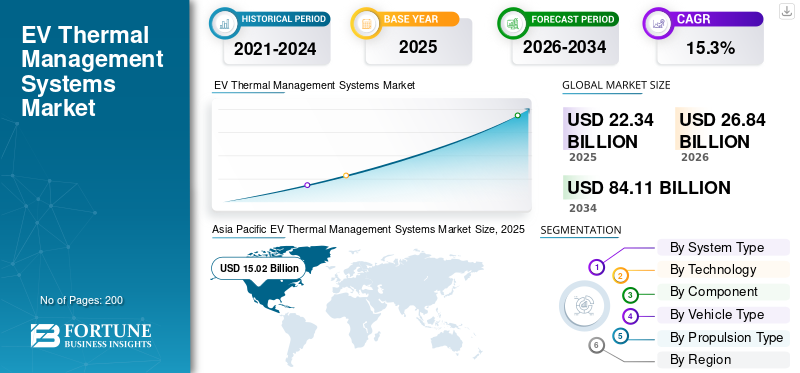

The EV thermal management systems market size was valued at USD 22.34 billion in 2025. The market is projected to grow from USD 26.84 billion in 2026 to USD 84.11 billion by 2034, exhibiting a CAGR of 15.3% during the forecast period. Asia Pacific dominated the EV thermal management systems market with a market share of 67.23% in 2025.

The market comprises technologies and components designed to regulate temperature across critical electric vehicle systems, including batteries, power electronics, and cabins. These systems enhance performance, safety, and lifespan by maintaining optimal thermal conditions. The market includes liquid and air cooling systems, refrigerants, heat exchangers, and control units, driven by rising EV adoption, fast charging needs, and advancements in battery technologies and energy efficiency requirements.

Key drivers of the market include rising global electric vehicle adoption, increasing demand for rapid charging capabilities, and the need to enhance battery performance and lifespan. Stringent emission regulations, advancements in battery technologies, and growing focus on passenger comfort and energy efficiency further accelerate the adoption of advanced thermal management solutions.

Major players in the market include Denso Corporation, Valeo SA, Hanon Systems, MAHLE GmbH, BorgWarner Inc., and Modine Manufacturing Company, competing through advanced cooling technologies, integrated thermal architectures, energy-efficient solutions, and innovations in battery thermal control to enhance vehicle performance, safety, and driving range.

Download Free sample to learn more about this report.

EV Thermal Management Systems Market Key Takeaways

- 2025 Market Size: USD 22.34 billion

- 2026 Market Size: USD 26.84 billion

- 2034 Forecast Market Size: USD 84.11 billion

- CAGR: 15.3% from 2026-2034

- Asia Pacific dominated the EV thermal management systems market with a 67.23% share in 2025.

- The integrated thermal management systems segment is projected to grow at a CAGR of 16.5% during the forecast period.

- The air cooling segment is projected to grow at a CAGR of 11.2% during the forecast period.

Asia Pacific

Asia Pacific remained the largest regional market, supported by strong EV production across China, Japan, and South Korea.

Europe

Europe held the second-largest market and is projected to grow at a CAGR of 13.4% during the forecast period.

North America

North America ranked as the third-largest market, driven by increasing EV adoption across the U.S. and Canada.

U.S.

The market is estimated at USD 2.02 billion in 2026, accounting for a major share of global revenues.

Japan

The market is estimated at USD 0.86 billion in 2026, representing around 3.1% of global sales.

Read More

EV THERMAL MANAGEMENT SYSTEMS MARKET TRENDS

Shift Toward Heat Pump-Based Systems to Enhance Energy Efficiency is Emerging Market Trend

A prominent trend in the market is the increasing adoption of heat pump-based technologies. Unlike traditional resistive heating systems, heat pumps efficiently transfer heat, significantly reducing energy consumption and preserving battery range, particularly in cold climates. Automakers are rapidly integrating heat pump systems to improve overall vehicle efficiency and meet consumer expectations for longer driving ranges. This trend is further supported by advancements in refrigerants and system design, enabling better performance across varying environmental conditions. As EVs become more mainstream, the focus on optimizing auxiliary energy consumption is growing, positioning heat pump technology as a critical component in next-generation thermal management systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising EV Adoption and Battery Performance Needs Drive Market Growth

The rapid global adoption of electric vehicles is a primary driver for the EV thermal management systems market growth. As EV sales increase across passenger and commercial vehicle segments, the need for efficient thermal regulation becomes critical to ensure optimal battery performance, safety, and longevity. Batteries are highly sensitive to temperature fluctuations, which can impact charging speed, range, and degradation rates. Additionally, the growing demand for fast-charging infrastructure intensifies heat generation, requiring advanced cooling solutions. Automakers are increasingly integrating sophisticated thermal systems to enhance vehicle efficiency and comply with performance expectations. Government incentives and stricter emission norms further accelerate EV penetration, indirectly boosting the demand for advanced thermal management technologies.

MARKET RESTRAINTS

High System Complexity and Cost Constraints to Limit Market Penetration

One of the key restraints in the market is the high cost and complexity associated with advanced thermal solutions. Unlike conventional vehicles, EVs require integrated thermal architectures that simultaneously manage batteries, power electronics, and cabin environments. This increases design complexity and necessitates the use of advanced materials and components such as liquid cooling circuits, sensors, and control units. These systems can significantly raise the overall vehicle cost, posing challenges for mass-market adoption, especially in price-sensitive regions. Additionally, the need for continuous innovation and customization for different vehicle platforms further increases development costs for manufacturers, limiting scalability and slowing down adoption across smaller OEMs.

MARKET OPPORTUNITIES

Advancements in Integrated Thermal Architectures to Unlock New Growth Potential

The development of integrated and multi-functional thermal management systems presents significant opportunities for market growth. Modern EV platforms are shifting toward centralized thermal systems that combine battery cooling, cabin conditioning, and powertrain temperature control into a single architecture. This integration improves energy efficiency, reduces component redundancy, and enhances overall vehicle performance. With the rise of next-generation EVs, including high-performance and long-range vehicles, OEMs are investing in smart thermal solutions that utilize heat pumps and advanced refrigerants. These innovations not only improve energy utilization but also extend driving range, making them highly attractive to consumers. As automakers prioritize system optimization, suppliers have opportunities to develop compact, cost-effective, and scalable thermal solutions.

MARKET CHALLENGES

Thermal Runaway Risks and Safety Concerns to Challenge Market Expansion

One of the major challenges in the market is addressing safety risks associated with battery thermal runaway. Lithium-ion batteries can generate excessive heat under certain conditions such as overcharging, physical damage, or manufacturing defects, potentially leading to fire hazards. Designing systems that can effectively detect, prevent, and mitigate such risks is complex and requires continuous innovation. Manufacturers must develop highly responsive thermal control mechanisms, integrate advanced sensors, and ensure fail-safe system performance under extreme conditions. Additionally, stringent safety regulations and testing standards increase development timelines and costs. Ensuring reliability while maintaining efficiency remains a critical challenge for thermal system providers in the evolving EV landscape.

Segmentation Analysis

By System Type

Critical Role in Battery Safety and Performance to Drive BTMS Segment Dominance

Based on system type, the market is categorized into Battery Thermal Management System (BTMS), power electronics thermal management, electric motor thermal management, Cabin Thermal Management (HVAC), and integrated thermal management systems.

The Battery Thermal Management System (BTMS) segment held the dominant EV thermal management systems market share due to its essential role in maintaining optimal battery temperature, directly impacting EV safety, performance, and lifespan. Increasing battery capacities and fast charging requirements generate significant heat, necessitating advanced cooling solutions. OEMs prioritize BTMS integration to prevent degradation and thermal runaway, safeguarding reliability and regulatory compliance.

The integrated thermal management systems segment is projected to grow at a CAGR of 16.5% over the forecast period. Rising focus on system-level efficiency and component consolidation is driving adoption, as OEMs seek to reduce energy consumption, improve range, and optimize overall thermal performance.

By Technology

Superior Heat Dissipation Efficiency and High-Performance EV Demand to Drive Liquid Cooling Segment Dominance

Based on technology, the market is categorized into air cooling, liquid cooling, and others.

The liquid cooling segment dominates the market due to its superior ability to manage high thermal loads in modern electric vehicles. Increasing battery capacities, fast charging requirements, and high-performance EVs generate substantial heat, making liquid cooling essential for maintaining efficiency and safety. OEMs widely adopt liquid-based systems for batteries and power electronics, ensuring optimal temperature control, extended component lifespan, and improved vehicle reliability across varying operating conditions.

The air cooling segment is projected to grow at a CAGR of 11.2% over the forecast period. Its cost-effectiveness, simpler design, and suitability for low to mid-range EVs are driving adoption, particularly in emerging markets and compact vehicle segments prioritizing affordability.

To know how our report can help streamline your business, Speak to Analyst

By Component

Efficient Heat Transfer Requirements Across EV Systems to Drive Segment Dominance

Based on component segmentation, the market is categorized into compressor, heat exchanger, cooling plates/cold plates, pumps & valves, Thermal Interface Materials (TIMs), and others.

The heat exchanger segment dominates the market due to its critical role in regulating temperature across batteries, power electronics, and cabin systems. As EV architectures become more complex, efficient heat dissipation is essential to maintain performance and safety. Heat exchangers enable effective thermal transfer between fluids and components, supporting fast-charging and high-load operations. Their widespread integration across multiple subsystems ensures consistent demand, making them a core component in both standalone and integrated thermal management solutions.

Thermal Interface Materials (TIMs) segment is projected to grow at a CAGR of 13.4% over the forecast period. Increasing focus on enhancing thermal conductivity and minimizing heat resistance at component interfaces is driving demand, particularly in compact and high-performance EV designs.

By Vehicle Type

High EV Adoption and Extensive Passenger Vehicle Production to Drive Passenger Car Segment Dominance

Based on vehicle type, the market is categorized into passenger car, van, bus, and truck.

The passenger car segment dominates the market due to the high global adoption of electric passenger vehicles and large-scale production volumes. Increasing consumer preference for EVs, supported by government incentives and expanding charging infrastructure, drives demand for efficient thermal management systems. Passenger EVs require advanced battery and cabin thermal regulation to ensure performance, safety, and comfort. Additionally, continuous innovation by OEMs in range optimization and fast charging capabilities further strengthens the demand for sophisticated thermal solutions in this segment.

The truck segment is projected to grow at a CAGR of 15.4% over the forecast period. Rising electrification of heavy-duty vehicles and increasing demand for long-haul efficiency are driving the need for robust thermal systems to manage higher energy loads and ensure operational reliability.

By Propulsion Type

Full Electrification Trend and High Thermal Load Requirements to Drive BEV Segment Dominance

Based on propulsion type segmentation, the market is categorized into BEV and HEV.

The BEV segment dominates the market due to the complete reliance on battery systems, which require advanced thermal management for optimal performance, safety, and longevity. High-capacity batteries and fast-charging capabilities generate significant heat, necessitating efficient cooling solutions. Increasing push toward zero-emission mobility, supported by government incentives and stricter emission norms, is accelerating BEV adoption. Additionally, OEM focus on improving driving range and battery efficiency further strengthens the demand for sophisticated thermal management systems in this segment.

The HEV segment is projected to grow at a CAGR of 13.1% over the forecast period. Rising demand for transitional electrification solutions and lower infrastructure dependency are driving adoption, supporting steady demand for thermal systems managing both battery and internal combustion components.

EV Thermal Management Systems Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America and the Middle East & Africa.

Asia Pacific

Asia Pacific EV Thermal Management Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to its strong electric vehicle production ecosystem, led by China, Japan, and South Korea. High EV adoption, supported by government incentives, subsidies, and strict emission norms, drives demand for advanced thermal solutions. The presence of major battery manufacturers and OEMs further strengthens regional growth. Additionally, rapid expansion of charging infrastructure and increasing focus on battery efficiency and safety contribute to sustained demand for thermal management systems across passenger and commercial EV segments.

China EV Thermal Management Systems Market

The China market in 2026 is estimated at around USD 13.13 billion, accounting for a dominant share of market revenues. Large-scale EV production, government subsidies, and strong battery manufacturing ecosystem are fueling rapid market expansion.

Japan EV Thermal Management Systems Market

The Japan market in 2026 is estimated at around USD 0.86 billion, accounting for roughly 3.1% of sales. Strong hybrid and EV production, advanced automotive technologies, and focus on energy efficiency are driving steady demand for thermal solutions.

Europe

Europe holds the second largest market share and is projected to grow at a CAGR of 13.4% over the forecast period. Strong regulatory frameworks targeting carbon neutrality and widespread EV adoption are key growth drivers. Leading automakers are investing heavily in advanced thermal technologies to improve vehicle efficiency and meet regulatory standards. Increasing demand for premium EVs, coupled with innovations in heat pump systems and integrated architectures, further supports market expansion across the region.

U.K. EV Thermal Management Systems Market

The U.K. market in 2026 is estimated at around USD 0.81 billion, accounting for a notable share of global revenues. Government electrification targets, growing EV adoption, and investments in charging infrastructure are accelerating demand for efficient thermal systems.

Germany EV Thermal Management Systems Market

The Germany market in 2026 is estimated at around USD 1.36 billion, accounting for a significant share of revenues. Strong automotive manufacturing base, premium EV production, and innovation in thermal technologies are supporting market growth.

North America

North America represents the third-largest market, driven by increasing EV adoption in the U.S. and Canada. Government incentives, investments in charging infrastructure, and rising consumer awareness support market growth. Automakers are focusing on enhancing battery performance and vehicle range, thus increasing demand for advanced thermal management systems. Additionally, the presence of leading technology providers and growing electrification of commercial fleets contribute to steady market expansion in the region.

U.S. EV Thermal Management Systems Market

The U.S. market in 2026 is estimated at around USD 2.02 billion, accounting for a major share of global revenues. Rising EV adoption, expanding charging infrastructure, and increasing focus on battery performance are driving country market growth.

Middle East & Africa

The Middle East & Africa region is witnessing gradual growth in the market, supported by increasing investments in sustainable mobility and clean energy initiatives. Governments in countries such as the UAE and Saudi Arabia are promoting EV adoption through pilot projects and infrastructure development. Although the market is at a nascent stage, rising awareness of electric mobility and diversification efforts away from fossil fuels are expected to drive future demand for thermal management systems.

Latin America

Latin America is experiencing steady growth in the market, driven by emerging EV adoption in countries such as Brazil, Mexico, and Chile. Government initiatives promoting clean transportation and reducing emissions are encouraging the transition toward electric mobility. While infrastructure challenges persist, increasing investments in charging networks and growing participation of global OEMs are expected to support demand for efficient thermal management solutions in the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Positioning of Key Plyers Propels Market Competition

The EV thermal management systems market is characterized by intense competition, with key players focusing on technological innovation, product integration, and strategic partnerships to strengthen their market position. Leading companies such as Denso Corporation, Valeo SA, Hanon Systems, MAHLE GmbH, and BorgWarner Inc. are investing heavily in advanced cooling technologies, including liquid cooling and integrated thermal systems. These players leverage strong relationships with OEMs and global manufacturing capabilities to maintain a competitive edge and expand their geographic presence.

In addition to established players, emerging companies and specialized component manufacturers are intensifying competition by offering cost-effective and customized solutions. Market participants are increasingly focusing on R&D to enhance energy efficiency, reduce system complexity, and support next-generation EV architectures. Collaborations with battery manufacturers and software integration for smart thermal control are becoming key strategies. Furthermore, mergers, acquisitions, and joint ventures are shaping the competitive landscape, enabling companies to diversify portfolios and address evolving OEM requirements.

LIST OF KEY EV THERMAL MANAGEMENT SYSTEMS COMPANIES PROFILED

- Denso Corporation (Japan)

- Valeo SA (France)

- Hanon Systems (South Korea)

- MAHLE GmbH (Germany)

- BorgWarner Inc. (U.S.)

- Modine Manufacturing Company (U.S.)

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Dana Incorporated (U.S.)

- Vitesco Technologies (Germany)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Valeo secured a multi-hundred-million-euro contract with a leading Chinese automaker to supply its Dual Layer HVAC system, improving cabin comfort and delivering up to 25% energy efficiency gains, with production scheduled to begin in 2026.

- August 2025: Hanon Systems partnered with Kia to integrate its fourth-generation EV heat pump technology into the Kia EV3 platform, enhancing battery thermal efficiency and extending vehicle driving range.

- July 2025: BorgWarner announced contracts with two major OEMs to supply 400V and 800V HVCH for plug in hybrid electric vehicle platforms, including pickup trucks, with production starting in 2028

- May 2025: BYD introduced its integrated “16-in-1” EV thermal management system under the e-Platform 3.0 architecture, combining heat pump, battery cooling, and waste heat recovery technologies.

- February 2025: Gentherm announced advancements in battery thermal management and climate comfort technologies to improve passenger comfort and thermal efficiency in electric vehicles.

REPORT COVERAGE

The global EV thermal management systems market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By System Type, By Technology, By Component, ByVehicle Type, By Propulsion Type and By Region |

| By System Type |

|

| By Technology |

|

| By Component |

|

| By Vehicle Type |

|

| By Propulsion Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 22.34 billion in 2025 and is projected to reach USD 84.11 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 15.02 billion.

The market is expected to exhibit a CAGR of 15.3% during the forecast period of 2026-2034.

The passenger car segment led the market by vehicle type.

Rising EV adoption and battery performance needs to drive market growth.

Asia Pacific held the largest market share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us