EVTOL Batteries Market Size, Share & Industry Analysis, By Battery Type (Electric, Fuel Cell, and Hybrid), By C Rate (Low C-Rate (<3C), Medium C-Rate (3C–8C), and High C-Rate (>8C)), By Battery Component (Cell, Module, Battery Pack, Battery Management System (BMS), Thermal Management System (TMS), and Others), By Aircraft Type (Air Taxi, UAVs, Cargo Transport, and Others), By Endurance (Short-Endurance (<30 min), Medium-Endurance (30–90 min), and Long-Endurance (>90 min)), By End User (Commercial, Defense, and Others), and Regional Forecast, 2025-2032

EVTOL Batteries Market Size and Future Outlook

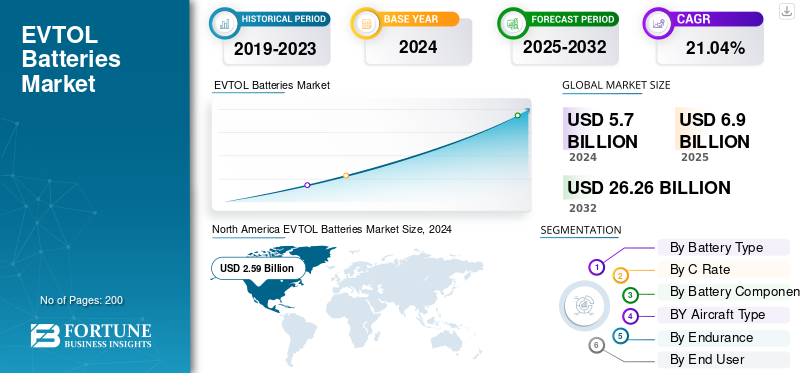

The global EVTOL batteries market size was valued at USD 5.70 billion in 2024. The market is projected to grow from USD 6.90 billion in 2025 to USD 26.26 billion by 2032, exhibiting a CAGR of 21.04% during the forecast period. North America dominated the EVTOL batteries market with a market share of 45.43% in 2024.

Electric Vertical Take-Off and Landing (eVTOL) batteries form the core of the new generation of electric aircraft that aim to make flying within and between cities more efficient and sustainable. These batteries provide the immense burst of power needed for vertical takeoff, then deliver steady energy densities for cruising through the air. An eVTOL battery setup typically includes a combination of cells and modules, managed by systems that keep everything safe and stable. The battery management system (BMS) keeps a close watch on voltage, temperature, and charge levels, while the thermal management system (TMS) helps control heat during intense use and charging. Together, they ensure reliability and enhanced safety in flight.

Globally, several major companies are pushing this technology forward. EHang, Joby Aviation, Archer Aviation, Lilium, and Volocopter are among the leaders, each developing aircraft suited for different uses, from city air taxis to short cargo routes. These firms are also working closely with key aviation regulators such as FAA, EASA, and CAAC to meet the strict certification requirements that will allow electric air mobility to become a regular part of the global transportation system.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rapid Adoption in Various Domains is Primary Cause for Market Growth

The eVTOL battery market is growing quickly as electric aviation shifts from test flights to certified commercial operations. Governments across the world are playing a key role in this transition. In the U.S., NASA’s advanced urban air mobility initiatives envisions thousands of electric aircraft operating in urban areas over the next decade, while the FAA’s Innovate28 and EASA’s Special Condition VTOL initiatives aim to simplify certification by 2028. In Asia, China’s CAAC has already approved the EHang EH216-S, making it the first certified eVTOL aircraft in the world and proving that electric flight is safe and commercially viable. At the same time, city transport agencies and logistics firms are testing short-range air taxis and electric cargo drones to support the demand for urban air mobility (UAM).

MARKET RESTRAINTS

Limited Infrastructure Restrain Market Expansion

According to the U.S. Department of Energy (DOE) and National Renewable Energy Laboratory (NREL), most city power grids aren’t yet equipped to handle the heavy electricity demand needed for vertiport charging, which adds a significant financial burden for early operators. Developing charging infrastructure, maintenance hubs, and battery-swapping systems will require large investments that many cities aren’t ready to make. The shortage of trained aerospace technicians and the concentration of battery materials in Asia also expose supply chains to disruption. Additionally, public hesitation about noise, safety, and the presence of low-flying aircraft slows down route approvals and adoption in urban areas.

MARKET OPPORTUNITIES:

Government Support and Urban Mobility Programs Offer New Opportunities

Strong government funding and national innovation programs are opening major opportunities for eVTOL battery manufacturers. In the U.S., the Air Force’s Agility Prime program is providing financial support to local eVTOL developers, giving early-stage battery suppliers access to both defense and dual-use markets. In Europe, initiatives such as Clean Aviation and SESAR are supporting research in hybrid and electric propulsion systems, encouraging the design of safer, higher-capacity batteries. Meanwhile, Japan’s Osaka Expo 2025 and South Korea’s K-UAM master plan are expected to showcase fully electric air taxis, increasing visibility and local demand for certified battery systems.

EVTOL BATTERIES MARKET TRENDS:

Shift Toward Smarter and Sustainable Battery Ecosystems Defines Market Trends

Download Free sample to learn more about this report.

The eVTOL battery industry is evolving toward smarter, safer, and more sustainable solutions. Manufacturers are focusing on lightweight designs and better energy efficiency to extend flight range and improve safety. Advanced management and thermal control systems are becoming standard, helping batteries perform more consistently over longer lifecycles. Governments and regulators now witness electric aviation as an essential part of future transportation planning, promoting collaboration between aerospace firms, energy companies, and infrastructure providers. Sustainability has become a key theme as well, with a growing push to use recyclable materials and repurpose used batteries to reduce environmental impact.

MARKET CHALLENGES:

High Operating Costs to Hamper Market Growth

Despite rapid innovation, electric aircraft still face high production costs and limited passenger capacity, which makes them more expensive to operate than ground transport. Many cities have yet to establish zoning rules or dedicated airspace policies for vertiports, delaying the rollout of commercial routes. Public concerns about safety, privacy, and noise also slow municipal approvals. On top of that, insurance models and maintenance standards for electric aircraft are still under development, adding uncertainty for investors and operators. Recycling and disposal systems for aviation-grade batteries are another missing piece. Unless regulators, manufacturers, and energy providers work together to solve these cost, infrastructure, and public acceptance issues, global adoption of eVTOL batteries will progress slowly despite their strong long-term potential.

US Tariff Impact

Recent U.S. tariffs on key battery materials such as lithium, nickel, and graphite have affected production costs for domestic eVTOL manufacturers. Since much of the world’s supply still comes from Asia, especially China and South Korea, companies such as Joby Aviation and Archer Aviation are dealing with higher import expenses. These added costs make it harder to scale manufacturing and could delay certification timelines in the near term.

Segmentation Analysis

By Battery Type

High Demand for Zero Emission Platform Electric Segment Contributed to Segmental Growth

On the basis of the segmentation of battery type, the market is classified into electric, fuel cell, and hybrid.

The electric segment accounted for the significant EVTOL batteries market share in 2024. Aviation authorities such as FAA, EASA, and CAAC prioritizing zero-emission platforms, electric battery systems have become the preferred energy source for both prototype and commercial aircraft. The growing demand for zero emission platforms in aviation contributes to this growth.

To know how our report can help streamline your business, Speak to Analyst

By C Rate

Enhanced Balance between Power Delivery and Battery Durability Fuels Growth of Medium C-Rate (3C–8C) Segment

In terms of C rate, the market is categorized into low C-rate (<3C), medium C-rate (3C–8C), and high C-rate (>8C).

The medium C-rate (3C–8C) segment captured the largest share of the market in 2024. In 2025, the segment is anticipated to dominate with 48.25% share. Medium C-rate batteries meet operational needs without excessive heat generation or degradation owing to optimal balance between power delivery and battery longevity.

The high C-rate (>8C) segment is expected to grow at a CAGR of 20.34% over the forecast period.

By Battery Component

Higher Operational Efficiency Supplemented Battery Pack Segment Growth

Based on battery components, the market is segmented into cell, module, battery pack, battery management system (BMS), thermal management system (TMS), and others.

The battery pack segment held the dominating position in 2024. This segment dominated as packs must meet strict aviation safety, thermal, and vibration standards under RTCA DO-311A and EASA CS-VTOL guidelines.

The segment of cell is set to flourish and is growing at a CAGR of 20.99% growth across the forecast period.

By Aircraft Type

As urban mobility programs gain traction Aircraft Type is anticipated forSegment Growth

Based on aircraft type, the market is segmented into air taxi, UAVs, cargo transport, and others.

The air taxi segment held the dominating position in 2024. The air taxi segment leads global demand for eVTOL batteries as urban mobility programs gain traction in major cities. Supported by agencies such as NASA, FAA, and EASA, air taxis are expected to become the first large-scale commercial application of electric aircraft.

The segment of UAVs is set to flourish with a growth rate of 20.65% growth across the forecast period.

By Endurance

Faster Charging Cycles is Anticipated for Short-Endurance (<30 min) Segment Growth

Based on endurance, the market is segmented into short-endurance (<30 min), medium-endurance (30–90 min), and long-endurance (>90 min).

The short-endurance (<30 min) segment held the dominating position in 2024. Short-endurance eVTOLs currently lead the market as most early models are designed for urban routes spanning 20 to 30 kilometers. These shorter missions match the energy capacity of existing batteries and the limits of available charging infrastructure. Shorter flight times also allow for faster recharging and simpler temperature control, making them more practical for early commercial deployment.

The segment of long-endurance (>90 min) is set to flourish with a growth rate of 20.92% CAGR across the forecast period.

By End User

Commercial Segment Set to Dominate Due to Various Wide User Base

Based on end-user, the market is segmented into commercial, defense, and others (private, recreational).

In 2024, the global market was dominated by the commercial segment in terms of end user. The commercial segment accounts for the largest share of eVTOL battery use, driven by passenger transport, logistics, and aerial service operators. Airlines, tourism companies, and air mobility startups are investing heavily in electric fleets to reduce emissions and operating costs.

In addition, defense end users are projected to grow at a CAGR of 21.10% during the study period.

EVTOL Batteries Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America EVTOL Batteries Market Size, 2024 ( USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the dominant share in 2023 valuing at USD 2.01 billion and also took the leading share in 2024 with USD 2.59 billion. Growth in North America is driven by strong government and defense support for electric aviation. The FAA’s Innovate28 plan and NASA’s Advanced Air Mobility (AAM) initiatives are creating regulatory framework clarity and infrastructure for large-scale deployment. In 2025, the U.S. market is estimated to reach USD 2.16 billion.

Europe and Asia Pacific

Other regions such as Europe and Asia Pacific are anticipated to witness a notable EVTOL batteries market growth in the coming years. During the forecast period, the Asia Pacific region is projected to record a growth rate of 21.76%, which is the highest amongst all the regions. Asia-Pacific leads in early commercialization, driven by regulatory flexibility and government backing. Backed by these factors, countries including China anticipate to record the valuation of USD 0.42 billion, Japan to record USD 0.22 billion, and India to record USD 0.31 billion in 2025. After Asia Pacific, the market in Europe is estimated to reach USD 1.23 billion in 2025. In the region, U.K. and Germany both are estimated to reach USD 0.51 billion and 0.38 billion each in 2025.

Middle East & Africa and Latin America

Over the forecast period, the Middle East & Africa and Latin America regions would witness a moderate growth in this marketspace. The Middle East market in 2025 is set to record USD 0.73 billion as its valuation. Latin America is set to attain the value of USD 0.33 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Extensive R&D and Strategic Collaborations Strengthen Competitive Position of Key Players

The global eVTOL battery market has a semi-concentrated structure, with a mix of aerospace OEMs, battery innovators, and component specialists competing for market share. Leading names include EHang, Joby Aviation, Archer Aviation, Lilium, Volocopter, Vertical Aerospace, Beta Technologies, and Eve Air Mobility. They are supported by established battery and energy firms such as CATL, Panasonic Energy, LG Energy Solution, Honeywell, and Saft, which supply certified high-power systems and thermal management solutions for electric aircraft. Most of these players are heavily investing in R&D to enhance energy density, optimize weight, and meet aviation safety standards such as RTCA DO-311A and EASA CS-VTOL, helping push the industry toward certification and large-scale production.

LIST OF KEY EVTOL BATTERIES COMPANIES PROFILED:

- EHang (China)

- Joby Aviation (U.S.)

- Archer Aviation (U.S.)

- Lilium (Germany)

- Volocopter (Germany)

- Beta Technologies (U.S.)

- Eve Air Mobility (Brazil)

- AutoFlight (Germany)

- Vertical Aerospace (U.K.)

- Ampaire (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2025: High-performance lithium-ion battery cells from Gotion High-Tech used by China's EHang, a Nasdaq-listed company that manufactures autonomous aerial vehicles, for its EH216 series air taxis. The business thinks that this step would increase the flying range of its products in preparation for commercial operation.

- April 2025: Enpower Greentech Inc. (EGI), a global supplier of cutting-edge lithium ion battery manufacturing and technology, and Mullen Automotive, a manufacturer of energy technologies and electric vehicles (EVs), have signed a Partnership and Supply Agreement.

- August 2024: An exclusive strategic investment and partnership agreement was established by AutoFlight and CATL to pool their knowledge of battery and eVTOL technologies. The two businesses will concentrate on improving eVTOL batteries' energy density and performance in order to support greater load capacities and longer flight distances while also attaining notable safety and stability gains.

- June 2024: Three major electric vehicle (EV) and two consumer electronic (CE) cell manufacturers in Europe, Asia, and North America have signed five multi-year binding offtake agreements totaling a minimum commitment of over USD 300 million with Group14 Technologies, Inc., the largest global manufacturer and supplier of advanced silicon battery materials.

- June 2023: The first three vendors for Eve Air Mobility's electric vertical take-off and landing (eVTOL) aircraft were revealed. DUC Hélice Propellers will supply the rotors and propellers for the eVTOL, BAE Systems will supply a sophisticated energy storage system, and Nidec Aerospace LLC, a joint venture between Nidec Corporation and Embraer, will supply the electric propulsion system.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Key Segments within the EVTOL Batteries Market

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 21.04% from 2025-2032 |

| Unit | Value (USD Billion ) |

| Segmentation | By Battery Type, C Rate, Battery Component, Aircraft Type, Endurance, End User, and Region |

| By Battery Type |

|

| By C Rate |

|

| By Battery Component |

|

| By Aircraft Type |

|

| By Endurance |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.70 billion in 2024 and is projected to reach USD 26.26 billion by 2032.

In 2024, the market value stood at USD 2.59 billion.

The market is expected to exhibit a CAGR of 21.04% during the forecast period.

The electric segment led the market by battery type.

Rapid adoption of EVTOL batteries in various domains is primary cause for market growth.

EHang, Joby Aviation, Archer Aviation, Lilium, Volocopter, and Beta Technologies are some of the prominent players in the market.

North America dominated the market in 2024.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us