Fast-Charging EV Battery Chemistries Market Size, Share & Industry Analysis, By Battery Chemistry Type (Lithium Iron Phosphate (LFP), Nickel Manganese Cobalt (NMC), Nickel Cobalt Aluminum (NCA), Lithium Titanate (LTO), and Others), By Charging Speed Capability (Standard Fast Charge, High Fast Charge, and Ultra-Fast Charge), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Buses, Trucks, and Others), By Anode Material Type (Graphite, Silicon-Graphite Composite, Lithium Titanate, Lithium Metal, and Others), and Regional Forecast, 2026–2034

Fast-Charging EV Battery Chemistries Market Size and Future Outlook

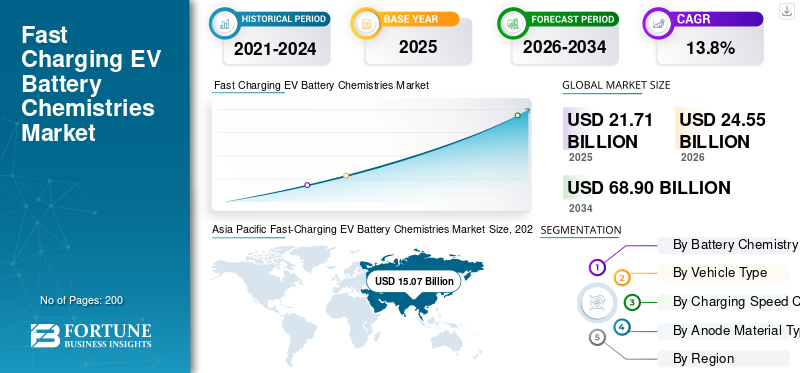

The fast-charging EV battery chemistries market size was valued at USD 21.71 billion in 2025. The market is projected to grow from USD 24.55 billion in 2026 to USD 68.90 billion by 2034, exhibiting a CAGR of 13.8% during the forecast period. Asia Pacific dominated the fast-charging EV battery chemistries market with a market share of 69.41% in 2025.

Fast-charging EV battery chemistries refer to advanced lithium-ion and next-generation battery compositions engineered to support high charging rates, reduced charging time, improved thermal stability, and enhanced energy density for electric vehicles.

Key drivers in the market include rising EV adoption, demand for reduced charging time, expanding fast-charging infrastructure, advancements in battery materials, government incentives, emission regulations, and increasing consumer preference for long-range electric vehicles.

Major players in the market include Contemporary Amperex Technology Co., Limited (CATL), LG Energy Solution Ltd., Panasonic Energy Co., Ltd., and BYD Company Ltd. competing through high C-rate innovation, advanced materials, thermal management technologies, strategic partnerships, and capacity expansion initiatives.

Download Free sample to learn more about this report.

FAST-CHARGING EV BATTERY CHEMISTRIES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 21.71 billion

- 2026 Market Size: USD 24.55 billion

- 2034 Forecast Market Size: USD 68.90 billion

- CAGR: 13.80% from 2026–2034

- Asia Pacific dominated the market with a 69.41% share in 2025.

- The Lithium Iron Phosphate (LFP) segment is expected to lead the market in 2026.

- The Passenger Cars segment is expected to dominate the market in 2026.

Asia Pacific

Dominated the market, driven by strong EV production, battery manufacturing, and expanding fast-charging infrastructure.

Europe

Growing due to battery localization, strict emission regulations, and rising premium EV adoption.

North America

Driven by expanding EV adoption, gigafactory investments, and fast-charging infrastructure development.

U.S.

The market is projected to reach USD 2.06 billion by 2026, supported by federal incentives and domestic battery manufacturing.

Japan

The market is projected to reach USD 0.14 billion by 2026, driven by advanced battery R&D and solid-state battery development.

Read More

FAST-CHARGING EV BATTERY CHEMISTRIES MARKET TRENDS

Advancements in High C-Rate Materials and Silicon Anodes is Emerging Market Trend

Continuous innovation in cathode compositions, silicon-dominant anodes, electrolyte formulations, and cell engineering is shaping key market trends. Manufacturers are focusing on Lithium Iron Phosphate (LFP) optimization, nickel-rich NMC variants, and next-generation solid-state enhancements to improve charging speed without compromising safety. Enhanced thermal management systems and improved battery management algorithms are also gaining traction. These technological developments are redefining performance benchmarks and influencing competitive market share among global battery producers.

- In January 2026, Ritar Power highlighted advancements in fast-charging EV batteries, emphasizing high C-rate lithium ion batteries chemistries, improved thermal management systems, and optimized battery management algorithms that enable reduced charging times, enhanced cycle stability, and greater energy efficiency. The report underscored innovations in electrode materials and cooling technologies designed to support rapid energy transfer while minimizing degradation, positioning fast-charging batteries as critical to accelerating electric vehicle and plug in hybrid electric vehicles adoption globally.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising EV Adoption and Charging Time Reduction to Accelerate Market Growth

The rapid increase in global electric vehicle adoption is significantly driving market growth for fast-charging EV battery chemistries. Consumers increasingly demand shorter charging times comparable to refueling conventional vehicles, pushing OEMs to adopt high C-rate capable chemistries. Expanding public fast-charging networks and highway corridor infrastructure further strengthen product demand. Additionally, government incentives and emission reduction targets are accelerating electrification strategies, compelling automakers to integrate advanced batteries chemistry that support ultra-fast charging capabilities.

- According to the IEA, public charging installations across the European Union are set to expand under the Alternative Fuels Infrastructure Regulation (AFIR). The regulation deployed minimum 150 kW fast-charging stations for cars and vans every 60 km along the TEN-T core network in 2025. It requires each site to provide a minimum total capacity of 400 kW, rising to 600 kW by the end of 2027.

MARKET RESTRAINTS

High R&D Costs and Complex Manufacturing Processes to Restrain Market Expansion

The development of fast-charging EV battery chemistries requires substantial investment in research, pilot production, and advanced material sourcing. Manufacturing processes for high C-rate cells demand precision engineering, enhanced quality control, and specialized equipment, increasing capital expenditure. Additionally, scaling innovative chemistries from laboratory to gigafactory level involves technical uncertainties and longer commercialization timelines. These factors can limit smaller players’ participation and slow widespread adoption, particularly in cost-sensitive emerging markets.

MARKET OPPORTUNITIES

Expansion of Megawatt Charging Systems to Unlock New Market Opportunities

The emergence of Megawatt Charging Systems (MCS) for commercial vehicles and heavy-duty fleets presents significant growth opportunities. As logistics, public transport, and long-haul trucking electrify, demand for battery chemistries capable of handling ultra-high power inputs will increase. Fleet operators prioritize minimized downtime and operational efficiency, creating strong market demand for durable, fast-charging battery solutions. Strategic collaborations between battery manufacturers, charging infrastructure providers, and OEMs will further expand revenue potential during the market forecast period.

- In October 2025, Siemens entered the megawatt-class EV charging market with its Sicharge Flex platform, delivering scalable 1 to 3 MW power output, modular infrastructure, and bi-directional grid support. Tailored for heavy EV fleets, the system integrates advanced cooling, high-efficiency power converters, and smart load management to enable rapid charging with reduced grid impact, enhancing uptime for commercial electric vehicles.

MARKET CHALLENGES

Thermal Runaway Risks and Safety Validation to Pose Challenges for Market Development

One of the primary challenges for the market is managing heat generation during rapid energy transfer. High charging rates can accelerate lithium plating, internal resistance buildup, and degradation if not properly controlled. Ensuring safety compliance across diverse climates and charging conditions requires rigorous validation, advanced cooling technologies, and sophisticated battery management systems. Balancing charging speed, lifecycle durability, and safety standards remains a complex engineering hurdle for manufacturers globally.

Segmentation Analysis

By Battery Chemistry Type

Cost Efficiency and Thermal Stability to Strengthen Lithium Iron Phosphate (LFP) Segment Leadership

Based on battery chemistry type, the market is segmented into Lithium Iron Phosphate (LFP), Nickel Manganese Cobalt (NMC), Nickel Cobalt Aluminum (NCA), Lithium Titanate (LTO), and others.

The Lithium Iron Phosphate (LFP) segment dominates the market due to its superior thermal stability, longer lifecycle, and cost advantage compared to nickel-based chemistries. LFP batteries support high charging cycles with lower degradation risks, making them highly suitable for fast-charging applications in mass-market EVs. Strong adoption in China and increasing penetration in Europe further consolidate its market share. Automakers prioritize LFP for entry and mid-range EV models to balance performance, safety, and affordability.

- In February 2026, Škoda launched large-scale EV battery production at its Mladá Boleslav facility, producing 1,122 lithium iron phosphate batteries packs daily for Volkswagen Group MEB-platform EVs. The automated plant processes 234,000 cells and performs 936,000 welds daily, using cell-to-pack architecture and advanced quality monitoring to enhance thermal stability, cost efficiency, and production precision.

The others segment is projected to grow at a CAGR of 25.7% during the forecast period. Emerging chemistries, including solid state batteries variants and advanced silicon-dominant formulations, are gaining traction due to their ultra-fast charging capability and higher energy density potential.

By Vehicle Type

Mass EV Adoption and Urban Charging Need to Reinforce Passenger Car Segment Dominance

Based on vehicle type, the market is segmented into passenger cars, light commercial vehicles (LCVs), buses, trucks, and others.

The passenger cars segment holds the largest market share, driven by high global EV production volumes and strong consumer demand for reduced charging times. Automakers are increasingly integrating fast-charging battery chemistries to enhance convenience and driving range, particularly in urban and premium vehicle categories. Expanding public fast-charging infrastructure and supportive government incentives further accelerate passenger EV adoption, strengthening this segment’s revenue contribution and overall market position.

- According to the IEA, global electric car sales exceeded 17 million units in 2024, marking a growth of over 25%. The additional 3.5 million units sold in 2024 alone surpassed the total electric car sales recorded worldwide in 2020.

The trucks segment is projected to grow at a CAGR of 17.1% during the market forecast period. Increasing electrification of long-haul and heavy-duty freight transport, combined with megawatt charging deployment, is driving demand for high C-rate, durable battery chemistries capable of supporting rapid turnaround times.

To know how our report can help streamline your business, Speak to Analyst

By Charging Speed Capability

Balanced Performance and Infrastructure Compatibility Leads to Standard Fast Charge Demand

Based on charging speed capability, the market is segmented into standard fast charge, high fast charge, and ultra-fast charge.

The standard fast charge segment dominates the market due to its wide compatibility with existing DC fast-charging infrastructure and optimized balance between charging speed, battery longevity, and cost efficiency. Most mass-market EVs are engineered to support standard fast-charging rates, ensuring strong deployment volumes globally. Automakers prefer this configuration to maintain battery durability while meeting consumer expectations for reduced charging time, thereby sustaining their leading market share.

- In February 2026, EVgo announced the installation of 100 new NACS fast-charging connectors, with an additional 500 planned for 2026, expanding its ultra-fast DC charging network across the U.S. This deployment focuses on high-powered (above 350 kW) NACS ports, enhancing compatibility with next-generation EVs and reducing charge times, while improving grid resiliency and station uptime through smart energy management and service integration.

The ultra-fast charge segment is projected to grow at a CAGR of 17.8% during the market forecast period. Increasing deployment of high-power charging corridors and megawatt charging systems is accelerating demand for battery chemistries capable of handling extreme charging rates with enhanced thermal stability.

By Anode Material Type

Mature Supply Chain and Proven Performance to Anchor Graphite Segment Growth

Based on anode material type, the market is segmented into graphite, silicon-graphite composite, lithium titanate, lithium metal, and others.

The graphite segment holds the largest market share due to its established manufacturing ecosystem, stable electrochemical performance, and cost efficiency. Natural and synthetic graphite anodes offer reliable cycling stability under fast-changing conditions when integrated with advanced battery management systems. Strong supplier networks, scalable processing capacity, and compatibility with LFP and NMC chemistries further reinforce graphite’s leadership across mass-market EV platforms globally.

- In February 2026, Exxon introduced a new form of engineered graphite that enhances EV battery performance by improving anode conductivity and structural stability, which boosts cycle life, increases usable capacity, and extends driving range. The innovation targets reduced lithium plating and enhanced fast-charging tolerance, aiming to improve durability while maintaining thermal safety, potentially lowering overall battery costs and accelerating adoption of higher-efficiency EV cells globally.

The others segment is projected to grow at a CAGR of 23.4% during the market forecast period. Emerging anode innovations, including advanced nanostructured and hybrid materials, are gaining traction for enabling ultra-fast charging, improved energy density, and reduced lithium plating risks.

Fast-Charging EV Battery Chemistries Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

Asia Pacific

Asia Pacific Fast-Charging EV Battery Chemistries Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to its large-scale EV production capacity and strong battery manufacturing ecosystem. China, South Korea, and Japan collectively account for a significant market share, supported by vertically integrated supply chains and aggressive gigafactory expansion. Favorable government policies, subsidies, and domestic raw material processing further strengthen regional leadership. Rapid deployment of public fast-charging infrastructure and high EV penetration rates continue to drive sustained market growth across the region.

- In January 2026, Amara Raja announced plans to seek new strategic partnerships for lithium-ion cell manufacturing, aiming to strengthen technology access, enhance localized cell production, and support advanced chemistries suited for fast-charging electric vehicle applications in India.

China Fast-Charging EV Battery Chemistries Market

The China market in 2026 is estimated at around USD 15.61 billion, accounting for roughly 63.6% of global revenues. Strong domestic EV production, vertically integrated battery supply chains, and rapid ultra-fast charging deployment reinforce its dominant market share and sustained fast-charging EV battery chemistries market growth.

Japan Fast-Charging EV Battery Chemistries Market

The Japan market in 2026 is estimated at around USD 0.14 billion, accounting for roughly 0.6% of global sales. Growth is supported by advanced battery R&D capabilities, solid-state development initiatives, and strategic OEM partnerships focusing on high-efficiency fast-charging platforms.

India Fast-Charging EV Battery Chemistries Market

The India market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 0.7% of global revenues. Accelerating EV adoption, production-linked incentives, and expanding public charging infrastructure position India as the fastest-growing regional market.

Europe

Europe holds the second-largest fast-charging EV battery chemistries market share, driven by strict carbon emission targets and rapid electrification strategies among automakers. Countries such as Germany, France, and the Nordic region are investing heavily in advanced battery technologies and localized cell production. Growing adoption of premium EVs with higher charging capabilities supports demand for fast-charging chemistries. Additionally, strong policy backing under EU climate frameworks ensures stable market growth and long term industry expansion.

- In January 2026, Verkor inaugurated its first battery cell gigafactory in Dunkirk, France, designed to produce high-performance lithium-ion cells for electric vehicles. The facility integrates advanced electrode manufacturing, automated assembly lines, and low-carbon production processes to support fast-charging capabilities and strengthen Europe’s localized battery supply chain.

Germany Fast-Charging EV Battery Chemistries Market

The Germany market in 2026 is estimated at around USD 0.95 billion, accounting for roughly 3.9% of global revenues. Strong automotive manufacturing presence, EU battery localization strategies, and premium EV demand drive consistent market expansion.

U.K. Fast-Charging EV Battery Chemistries Market

The U.K. market in 2026 is estimated at around USD 0.85 billion, accounting for roughly 3.4% of global sales. Government decarbonization targets, charging corridor investments, and fleet electrification programs support steady market demand growth.

North America

North America represents the third-largest market for fast charging EV battery chemistries, supported by expanding EV adoption in the U.S. and Canada. Federal incentives, state-level zero-emission mandates, and infrastructure funding programs are accelerating fast-charging network deployment. Domestic battery manufacturing investments and strategic collaborations between automakers and cell producers further enhance regional competitiveness. Rising consumer preference for long-range EVs and pickup trucks with rapid charging capability contributes to steady market growth.

- In December 2024, Stellantis and Zeta Energy announced an agreement to develop lithium-sulfur EV batteries, targeting higher energy density, reduced material costs, and improved fast-charging capability, while eliminating nickel, cobalt, and manganese from cathode chemistry.

U.S. Fast-Charging EV Battery Chemistries Market

The U.S. market in 2026 is estimated at around USD 2.06 billion, accounting for roughly 8.4% of global revenues. Federal incentives, domestic gigafactory expansion, and rising electric truck adoption accelerate technological innovation and long-term market growth.

Rest of the World

The Rest of the World region is projected to grow at a CAGR of 17.3% during the market forecast period. Expanding EV initiatives in Latin America, the Middle East, and parts of Africa are driving the gradual adoption of fast charging technologies. Governments are introducing supportive regulations and pilot charging projects to reduce fuel dependency. Increasing urbanization and fleet electrification programs are expected to create new revenue streams and accelerate regional market expansion.

- In February 2026, the UAE inaugurated one of the world’s largest ultra-fast EV charging hubs, featuring multiple above 350 kW DC chargers, high-capacity grid connectivity, smart load management systems, and solar integration to support rapid vehicle turnaround and network stability.

COMPETITIVE LANDSCAPE

Key Industry Players

Gigafactory Expansion, Advanced Materials Innovation, and Strategic Alliances Define Market Competition

The market is moderately consolidated, led by global battery manufacturers with strong vertically integrated supply chains and large-scale gigafactory capacities. Key players such as Contemporary Amperex Technology Co., Limited (CATL), LG Energy Solution Ltd., Panasonic Energy Co., Ltd., and BYD Company Ltd. compete through high C-rate cell innovation, advanced cathode-anode engineering, and thermal management technologies. Companies focus on strategic OEM partnerships, raw material sourcing agreements, and regional capacity expansion to strengthen market share. Investments in silicon anodes, solid-state research, and faster charging validation further intensify competitive differentiation.

- In June 2024, CATL unveiled its Tianheng energy storage system featuring zero degradation in the first five years, ultra-high energy density, and advanced thermal management. The system integrates long-life LFP cells, optimized pack design, and intelligent battery management to enhance safety, operational efficiency, and lifecycle performance for large-scale renewable and grid-support applications.

LIST OF KEY FAST-CHARGING EV BATTERY CHEMISTRIES COMPANIES PROFILED

- Contemporary Amperex Technology Co., Limited (CATL) (China)

- BYD Company Ltd. (China)

- LG Energy Solution Ltd. (South Korea)

- Samsung SDI Co., Ltd. (South Korea)

- SK On Co., Ltd. (South Korea)

- Panasonic Energy Co., Ltd. (Japan)

- CALB (China Aviation Lithium Battery) (China)

- EVE Energy Co., Ltd. (China)

- Gotion High-Tech Co., Ltd. (China)

- Sunwoda Electronic Co., Ltd. (China)

- Farasis Energy, Inc. (China)

- Svolt Energy Technology Co., Ltd. (China)

- Northvolt AB (Sweden)

- AESC Group Ltd. (Envision AESC) (Japan)

- StoreDot Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Donut Lab released solid-state EV battery test results demonstrating ultra-fast charging from 10% to 80% in approximately 8 minutes, while maintaining high energy density and improved thermal stability. The prototype cells showed enhanced cycle life and reduced degradation under high C-rate charging conditions, highlighting solid-state electrolyte advantages in minimizing lithium dendrite formation and improving safety performance.

- October 2025: General Motors revealed a next-generation EV battery charging technology designed to significantly reduce charging times through optimized cell architecture and enhanced battery management software. The system improves high C-rate tolerance, thermal regulation, and charging efficiency, supporting faster energy replenishment while maintaining long-term battery durability and performance across GM’s Ultium-based electric vehicle platforms.

- April 2025: CATL launched its second-generation fast-charging battery featuring 4C charging capability, delivering approximately 600 km range in 10 minutes, enhanced low-temperature performance, and improved lithium plating control through advanced electrolyte and electrode optimization.

- August 2024: Zeekr unveiled what it claims is the world’s fastest-charging EV battery, capable of 10% to 80% charging in around 10.5 minutes using advanced lithium iron phosphate (LFP) chemistry, upgraded battery management systems, and enhanced thermal control to support high C-rate charging while maintaining safety and cycle stability.

- July 2024: BYD and CATL announced plans to release next-generation EV batteries supporting 6C fast-charging, enabling charging from 10% to 80% in under 10 minutes, utilizing advanced electrode design, optimized electrolytes, and enhanced thermal management systems.

- June 2024: Nyobolt unveiled an EV sports car prototype demonstrating ultra-fast charging from 10% to 80% in under 5 minutes using high-power lithium-ion cells with advanced anode materials, optimized thermal management, and enhanced cycle stability for real-world road performance.

- April 2024: CATL introduced its Shenxing Plus battery, delivering over 1,000 km CLTC range and supporting 4C superfast charging, enabling approximately 600 km driving range from a 10-minute charge through optimized LFP chemistry, advanced cell design, and enhanced energy density improvements.

REPORT COVERAGE

The global fast-charging EV battery chemistries market analysis provides an in-depth study of the market size & forecast by all the market segments included in the vehicle security components market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Battery Chemistry Type, By Vehicle Type, By Charging Speed Capability, By Anode Material Type, and By Region |

| By Battery Chemistry Type |

|

| By Vehicle Type |

|

| By Charging Speed Capability |

|

| By Anode Material Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 21.71 billion in 2025 and is projected to reach USD 68.90 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 15.07 billion.

The market is expected to exhibit a CAGR of 13.8% during the forecast period of 2026-2034.

The passenger cars segment leads the market in terms of vehicle type.

Rising EV adoption and charging time reduction to accelerate market growth.

Major players in the market include Contemporary Amperex Technology Co., Limited (CATL), LG Energy Solution Ltd., Panasonic Energy Co., Ltd., and BYD Company Ltd., among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us