Feed Additives Market Size, Share & Industry Analysis, By Type (Amino Acids, Vitamins & Minerals, Antioxidants, and Others), By Animal Type (Cattle, Poultry, Swine, and Others), By Form (Dry and Liquid), By Nature (Natural and Synthetic), and Regional Forecast, 2026 - 2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

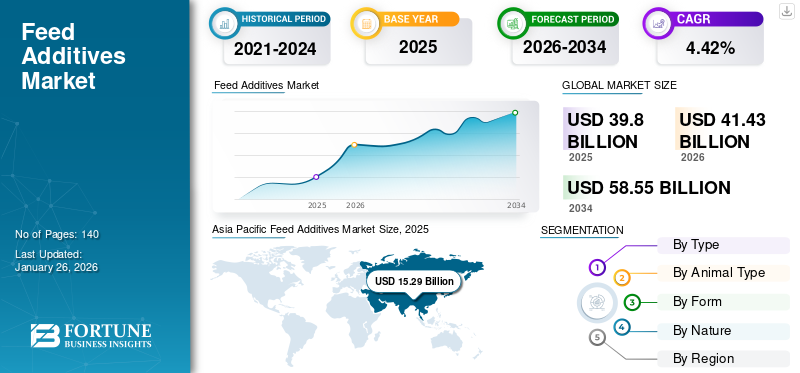

The global feed additives market size was valued at USD 39.80 billion in 2025. The market is projected to grow from USD 41.43 billion in 2026 to USD 58.55 billion by 2034, exhibiting a CAGR of 4.42% during the forecast period. Asia Pacific dominated the feed additives market with a market share of 38.41% in 2025.

Animal feed additives are important ingredients in feed production as they enhance feed utilization efficiency, animal health, and metabolism. These additives are extensively used globally, benefitting various animals and birds, including poultry. They contribute to improved growth performance, increased feed palatability, provide essential nutrients, and optimize feed utilization.

With increasing feed standards, growing consumer awareness, and the demand for healthy animal by-products, feed additive manufacturers are looking for non-residual and more natural alternatives to traditional additives. Some vital additives most commonly used in the feed are prebiotics, probiotics, herbs, and feed enzymes. Herbs, such as cinnamon, cumin, celery, and their botanical extracts, are also used in feed as additives. These botanical herbs possess medicinal properties that help to improve the anti-inflammatory properties of feed and act as an antioxidant, antimicrobial, digestibility booster, and immune stimulant at the same time. Additionally, additives are used to add flavor and color to animal diets.

Download Free sample to learn more about this report.

Feed Additives Market Key Takeaways

- 2025 Market Size: USD 39.80 billion

- 2026 Market Size: USD 41.43 billion

- 2034 Forecast Market Size: USD 58.55 billion

- CAGR: 4.42% from 2026–2034

- Asia Pacific dominated the feed additives market with a market share of 38.41% in 2025.

- The amino acids segment will account for 40.07% market share in 2026 and is expected to retain its dominance over the forecast period.

- The poultry segment is expected to account for 35.99% of the market in 2026 and is expected to retain its dominance over the forecast period.

Asia Pacific

The Asia Pacific region captured 38.41% of the global market in 2025, generating USD 15.29 billion in revenue, and is projected to reach USD 16.03 billion in 2026.

North America

North America contributed approximately USD 10.32 billion to the global market in 2025, accounting for 25.92% share, and is expected to reach USD 10.71 billion in 2026.

Europe

In 2025, the European market stood at USD 7.28 billion, representing 18.30% of global demand, and is projected to grow to USD 7.5 billion in 2026 despite challenges in the poultry sector.

U.S.

The U.S. market is projected to reach USD 8.37 billion by 2026. The country is the second largest animal feed producer in the world with over 5,000 feed manufacturing facilities producing over 200 million tons of finished animal feed yearly.

Japan

The feed additives market is projected to reach USD 0.93 billion by 2026, supported by ongoing modernization of the country's feed industry and steady livestock production.

Read More

Feed Additives Market Trends

Growing Popularity for Functional Feed to Boost Product Demand

Feed plays a crucial role in influencing immunity, growth, and the overall performance of animals. Companies operating in the feed industry have developed functional supplements and foods fortified with additives that offer physiological benefits and can improve the immunity of animals. Food additives vary widely in function, such as regulating stress, improving gut health, and enhancing disease resistance.

In forming functional foods, key additives include enzymes, antioxidants, mycotoxin binders, probiotics and prebiotics, plant extracts, and photobiotic compounds. These functional additives are added to feed formulations and incorporated into pellets by various processing methods. Adding these additives to animal feed can improve the overall physiological quality of animals, thereby increasing their market value. With the rapid commercialization of the livestock industry in developing countries, many livestock farms are being set up only to cater to certain market demands. This often necessitates the incorporation of functional additives into animal feed. This trend is expected to be witnessed in emerging countries, supplementing market growth over the forecast period. Asia Pacific witnessed a growth from USD 13.70 Billion in 2023 to USD 14.46 Billion in 2024.

Download Free sample to learn more about this report.

Impact of U.S. Tariff

The U.S. is recognized as one of the most developed countries across the globe, especially for production quantity in the feed and livestock sector. However, it still relies on China for imports of particular additives. Predominantly, around 70% of the amino acids (threonine, lysine, and others) used by the U.S. feed industry are imported from China. This situation worsened when Donald Trump, the American President, announced the news of tariffs imposed on all the end products imported by the country.

According to the new tariff structure, the U.S. will impose a 25% duty on imports of additives from the Chinese market. This high tariff can increase the overall price of the additives, which will make it difficult for consumers as well as animal caretakers to purchase. Although the Tariff Act is on hold till June 2025, it is still anticipated to impact the market substantially.

Market Dynamics

Market Drivers

Thriving Demand for Animal Proteins to Boost Additive Sales

According to the United Nations population projections for 2050, the global population is anticipated to reach more than 9.7 billion, increasing demand for animal protein. The consumption of animal protein has increased significantly in recent years. The animal feed industry is scaling up production efforts to meet this growing demand while ensuring sustainability and reducing the environmental impact of livestock operations. Several factors, such as consumption patterns and daily diets of humans, determine the need for animal protein in the regular diet of humans. The animal-derived protein industry is expected to expand due to the health benefits associated with meat consumption and animal by-products.

Livestock products contribute 30% of the global agricultural value and 19% of the food production value, providing nearly 35% of the protein and 15% of the energy consumed in human food. Meeting consumer demand for milk, meat, eggs, and other animal by-products depends greatly on a steady supply of suitable, cost-effective, safe feed. With a growing demand for quality feed, the need for additives that can provide various functional benefits is also growing. With a promising future outlook for the animal protein industry, the growing need for additives will supplement market growth over the forecast period.

Growing Awareness of Animal Health & Nutrition Propels Industry Growth

The rising awareness of animal nutrition & health is a key driver strengthening the industry's potential. In today’s era, most consumers are concerned about their animal health and are always looking for products that can boost their overall health. This concern fuels the awareness and usage of additives that are known to promote the overall animal's well-being. By seeing such demand, the players in the market are focusing on enhancing their product offerings and are trying to introduce new additives for animals.

Market Restraints

Rising Cost of Feed Raw Materials is Limiting Market Growth for Additives

One of the substantial challenges faced by market players in the feed and nutrition industry is the increasing cost of feed, which accounts for more than 70% of total production costs for some species. In emerging economies, livestock farmers often encounter financial constraints that prevent them from buying expensive feed. Consequently, they use locally-made or self-produced compound feed for their animals, making the meat quality derived from such countries sometimes lower than the average quality. Thus, the surging cost of animal feed restricts the growing momentum of the market.

Market Opportunities

Technological Advancements in Feed Additives Industry Create Growth Opportunities

Technological advancements in the feed additives industry unlock numerous growth opportunities for the market. In today’s era, most consumers are seeking additives that are of improved quality and pose minimal impact on the environment. To cater to this rising demand, the prominent players operating in the global space are adopting advanced technology. For instance, nanotechnology can be used which ensure precise nutrient delivery and minimize environmental impact. Moreover, enterprises adopt automated feeding systems such as robotic feeders, which aid in precise feed mixing and dispensing. Moreover, such advanced technology assures that each animal obtains an appropriate amount of nutrients. As a result, such technology usage enhances growth chances in the market.

Market Challenges

Misconception Regarding Use of Additives Impedes Market Potential

Inadequate awareness about the utilization of additives is a considerable challenge faced by producers globally. Most global consumers lack sufficient knowledge and have misconceptions regarding additives, especially the chemically sourced and antibiotic-free additives. Moreover, a few of the additives, particularly antibiotics, pose adverse impacts on animal health. Such factors drift consumers away from additives. Thus, the factors mentioned above create hurdles in the global animal feed additives market growth.

Segmentation Analysis

By Type

Amino Acids Segment Holds Largest Share as It is Crucial for Optimal Animal Performance

Based on type, the market is divided into amino acids, vitamins & minerals, antioxidants, and others.

The amino acids segment will account for 40.07% market share in 2026 and is expected to retain its dominance over the forecast period. The proper balance of amino acids in the regular diet feed is crucial for optimal animal performance. Inadequate levels of these amino acids could result in issues regarding meat production, egg production, and quality. Amino acid additives provide flexibility with feed ingredients, enabling companies to profit more. These amino acids also compensate for certain amino acid deficiencies caused by cheaper alternatives. The amino acids predominantly added to feed are L-methionine, L-valine, L-lysine, L-tryptophan, L-thionine, and L-arginine.

Essential minerals for an animal diet include common salt, calcium, zinc, sulfur, iodine, iron, molybdenum, magnesium, cobalt, and selenium. All farm animals generally need more common salt than their diets contain, and it is routinely provided to them. Among other essential minerals, phosphorus and calcium are the most likely to become deficient as they are in high demand for various functions, such as bone development, milk production, and the formation of eggshells. Good sources of calcium and phosphorus are bone meal, dicalcium phosphate, and defluoridated phosphate. Eggshells are made from almost pure calcium carbonate. Calcium can easily be obtained from crushed limestone, crushed seashells, or marl, all are rich in calcium. Antioxidant additives are expected to grow with a considerable CAGR during the forecast period, mainly due to the growing demand from the Asia Pacific poultry industry.

By Animal Type

Growing Commercialization of Poultry Business Globally Boosted Segment Expansion

Based on animal type, the global feed market is segmented into cattle, poultry, swine, and others. The others segment mainly consists of sheep, goats, and aqua feed.

The poultry segment is expected to account for 35.99% of the market in 2026 and is expected to retain its dominance over the forecast period. The major sub-units in the poultry segment include duck, chicken, turkey, and goose in terms of species. These poultry species are raised for meat and egg production. Among all species, chicken is the major breeding species globally. The poultry sector is one of the fastest-growing agricultural sub-sectors in emerging countries. Factors such as high-income level, high population, and urbanization are expected to contribute to market growth in the future.

Besides the poultry sector, the cattle feed industry also consumes large additives, making it the second largest market. According to the USDA statistics, the global cattle population exceeded one billion in 2022. Cattle primarily consume a diet consisting of legumes, grasses, clover, alfalfa, and hay. To enhance the digestibility of their regular diet, these additives are added during the production process. Moreover, antioxidants are added to the feed to prevent deterioration.

- The cattle segment is expected to hold a 27.81% share in 2024.

- The swine segment is expected to hold a 26.05% share in 2024.

To know how our report can help streamline your business, Speak to Analyst

By Form

Dry Segment Dominated Market Owing to Its Prolonged Shelf Life

Based on form, the global market is distributed into dry and liquid.

Out of both, the dry category led and generated the maximum feed additives market share. Unlike liquid additives, dry additives can be easily handled and stored. The dry segment is anticipated to hold a dominant market share of 70.07% in 2026. Moreover, it has a prolonged shelf life as it is more resistant to moisture and temperature fluctuations. Some dry additives that show high demand include vitamins, minerals, amino acids, and others. It is also economical, primarily due to lower shipping costs. As a result, such advantages bolster its utilization rate globally.

The liquid segment is considered the fastest-growing segment and is anticipated to grow at the same pace in the future. Ease of administration, enhanced uniformity of nutrient delivery, and versatility stimulate the segment’s potential.

By Nature

Synthetic Segment Led Global Market Due to Its Cost-Effectiveness

Based on nature, the market is bifurcated into natural and synthetic.

In 2026, the synthetic segment is projected to lead the market with a 66.16% share. Compared to the natural category, synthetic additives are cost-effective and strengthen nutrient absorption in animals. These ingredients can be tailored to a particular animal’s condition or needs, which further improves the animal’s performance. Additionally, incorporating such ingredients in the daily diet of animals can minimize the risk of foodborne illnesses. Thus, the factors above can facilitate the sales of synthetic additives.

The natural sector emerged as the fastest-growing segment and is predicted to maintain the same pace in the coming years. The increasing awareness of natural additives and improved feed efficiency of natural additives fuels growth.

FEED ADDITIVES MARKET REGIONAL OUTLOOK

The global study of the market considers various regions: North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Feed Additives Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 38.41% of the global market in 2025, generating USD 15.29 billion in revenue, and is projected to reach USD 16.03 billion in 2026. Asia Pacific held the largest market share in 2025 due to the presence of China and India, among the top 5 animal feed-producing countries globally. The growth in this region can be attributed to the ongoing consolidation and modernization of the feed industry in China, India, Vietnam, and Japan. In this region, the poultry segment held the largest market share of the animal type. It is mainly driven by the presence of numerous small-scale farmholders and competitiveness among large commercial enterprises operating in the poultry sector, all vying to expand in new geographies. The Japan market is projected to reach USD 0.93 billion by 2026, the China market is projected to reach USD 8.63 billion by 2026, and the India market is projected to reach USD 2.49 billion by 2026.

Additionally, other factors that are predominantly expanding the industry growth in Asia Pacific include the ever-increasing livestock population, untapped potential in emerging markets, flourishing end-user industries, and the growing consumption of domestic animal products. Furthermore, the changing purchasing power of the population and favorable demographics of the region are contributing to supplementing the animal feed industry in the region.

- In Asia Pacific, the poultry segment is estimated to hold a 38.93% market share in 2024.

- In Asia Pacific, the swine segment is estimated to hold a 28.22% market share in 2024.

To know how our report can help streamline your business, Speak to Analyst

North America

North America contributed approximately USD 10.32 billion to the global market in 2025, accounting for 25.92% share, and is expected to reach USD 10.71 billion in 2026. Reasons behind the growth include surging demand for proteinaceous products and rising focus on animal welfare and health. Moreover, the region is witnessing a strong inclination toward organic and natural animal-based items, which further propels the usage of additives.

Amongst North America, the U.S. dominated and is the second largest animal feed producer in the world. The U.S. comprises over 5,000 feed manufacturing facilities, producing over 200 million tons of finished animal feed yearly. The top three consumers of animal feed in the U.S. are beef cattle, pigs, and broilers. According to AFIA (American Feed Industry Association), North Carolina, Iowa, California, Texas, and Minnesota topped the list for animal feed consumption. Along with this, Mexico is also one of the world's top five animal feed producers. The U.S. market is projected to reach USD 8.37 billion by 2026.

Europe

In 2025, the Europe market stood at USD 7.28 billion, representing 18.30% of global demand, and is projected to grow to USD 7.5 billion in 2026. According to a report by Alltech, European laying hen feed production was 30.9 million tons in 2021 but dipped by 1% in 2022 to 30.6 million tons. In 2022, avian influenza, other diseases, and high raw material costs affected the laying hen industry in many European markets. The region saw a tight poultry market with high prices. Poultry production is expected to decline, keeping prices high due to continued pressure from avian flu and high input costs. For U.K. poultry, self-sufficiency declined in 2023, with imports increasing slightly from the Netherlands, Poland, and Thailand. The UK market is projected to reach USD 0.75 billion by 2026, while the Germany market is projected to reach USD 1.56 billion by 2026.

In 2022, Europe, which reported declines in most feed categories by volume, saw the largest drop in cow feed compared to the previous year. According to a report by Alltech, beef feed production in Europe was 17.5 million tons in 2021, which decreased in 2022 to reach 15.7 million tons. According to the report, although some countries in the region reported significant increases, total animal feed production decreased by more than 10%. Due to low prices, Bulgaria reported a slight shift from milk to beef production. In many cases, drought and rising beef prices have prompted dietary supplementation.

South America

The Brazilian feed industry is the third largest industry in the world, mainly due to its large raw material production capacity and the country’s considerable size, combined with its high meat consumption. Brazil's agricultural output has grown rapidly over the past decade, spurred by rising global demand and technological progress. The surge in Brazil's export demand for protein further propels the feed industry, which is striving to expand production to meet this heightened demand.

The growing livestock, poultry, and aquaculture sectors make Brazil well-suited to niche markets such as additives and ingredients. Rising prices for corn and soybean meal continue to rise, exerting pressure on the feed industry. Feed additives and ingredients are important in alleviating financial pressures and uncertainties, ensuring that animals receive adequate nutritional food. With Brazil and other South American countries being popular destinations for investment in the feed industry, the South American region is expected to grow with the highest CAGR during the analysis period.

Latin America and Middle East & Africa

In 2025, Middle East & Africa generated USD 1 billion, contributing 2.50% to global market revenue, and is projected to grow to USD 1.02 billion in 2026. The Middle East & Africa region is at its nascent stage and is anticipated to grow at the same pace in the coming years. The increasing number of livestock and the augmented number of animal meat players in the region propel the growth.

Latin America recorded a market size of USD 5.92 billion in 2025, capturing 14.86% of the global market share, and is projected to reach USD 6.17 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Mergers & Acquisitions and Partnerships to Gain a Competitive Edge

Various regional and international key players are consistently developing advanced strategies to take a competitive advantage over other competitors. Many companies are forming mergers, acquisitions, partnerships, and deploying collaborative strategies to enable market growth. For instance, in January 2023, Animal health and nutrition company Novus International, Inc. acquired biotech company Agrivida Inc. Through this acquisition, Novus would take ownership of the proprietary INTERIUS technology developed by Agrivida to embed additives inside the grain.

List of Key Feed Additive Companies Profiled

- Cargill, Incorporated (U.S.)

- ADM (U.S.)

- Ajinomoto Co., Inc. (Japan)

- Evonik Industries (Germany)

- DuPont (U.S.)

- Novozymes (Denmark)

- DSM (Netherlands)

- Adisseo (China)

- Hansen Holding (Denmark)

- Kemin Industries, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2024: Volac, a U.K.-based additives company, released its latest website for the additives division. This launch highlights the technical support services of the firm and evidence-based items that enhance the sustainability and efficiency of livestock production systems globally.

- August 2023 – Adisseo, a Chinese conglomerate operating in the animal nutrition industry, shared plans to expand its footprint by constructing a new powder methionine plant in Fujian province in China. The company invested nearly USD 680 million in this facility, which is expected to be operational by 2027.

- February 2021 – Global animal nutrition conglomerate DLG Group, in collaboration with Alltech, acquired Finland-based company Karki-Agri. This move would enhance their ability to provide field-proven and innovative animal nutrition solutions, strengthening their market position.

- February 2021 – Investment Partners, through its IK IX Fund, acquired the majority of shares from the founders of Innovad. Innovad is a supplier of animal health and nutrition solutions.

- November 2020 –Evonik acquired the Porocel Group for USD 210 million. Revenues from the newly acquired entity would be included in Evonik’s sales and earnings for 2020. The company, with its employees and the corresponding production facilities, was integrated into the Smart Materials division of Evonik.

REPORT COVERAGE

The feed additives market industry report provides a detailed analysis of the market and focuses on key aspects such as leading companies, animal types, and leading types of products. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.42% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Animal Type

|

|

|

By Form

|

|

|

By Nature

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size stood at USD 41.43 billion in 2026.

The market is likely to grow at a CAGR of 4.42% over the forecast period (2026-2034).

Based on type, the amino acids segment led the market.

Thriving demand for animal proteins is expected to drive market growth.

Some of the top players in the market are Cargill, Kemin Industries, and Evonik.

Asia Pacific dominated the feed additives market with a market share of 38.41% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us