Firearm Sight Market Size, Share & Industry Analysis, By Magnification Sight Types (Variable, Fixed, & Switchable), By Sight Category (Iron, Non-Magnified Electronic, Holographic, Magnified Optical, and Digital), By Illumination Method, By Focal Plane, By Magnification Type, By Weapon Platform, By Range Band, By Power Source (Tritium-Powered, Replaceable Battery, Rechargeable Battery, Solar-Assisted, and Hybrid Power), By Sensor Type, By Material, By End User (Military, Law Enforcement, Commercial, Private Defense Contractors, and Training Academies), and Regional Forecast 2026-2034

Firearm Sight Market Size and Future Outlook

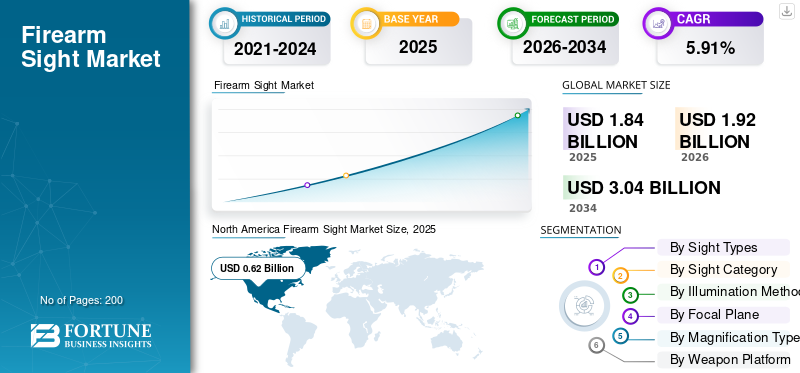

The global firearm sight market size was valued at USD 1.84 billion in 2025. The market is projected to grow from USD 1.92 billion in 2026 to USD 3.04 billion by 2034, exhibiting a CAGR of 5.91% during the forecast period. North America dominated the firearm sight market with a market share of 33.69% in 2025.

The market covers aiming systems mounted on pistols, rifles, shotguns, and crew-served weapons, including iron sights, red-dot/reflex sights, holographic sights, magnifiers, and telescopic/riflescopes. In practice, this is a performance-driven optics market shaped by military, law-enforcement, sport-shooting, and hunting demand, with buyers increasingly favoring faster target acquisition, better low-light performance, and rugged, mission-ready designs over basic sighting systems.

Rising adoption of red-dot and holographic sights for quicker engagement, growing law-enforcement and military modernization, and continued consumer demand from hunting and competitive shooting are driving the growth of the global market.

Among the leading players are Trijicon, EOTECH, Aimpoint, Leupold & Stevens, SIG SAUER, and others. The major players are focusing on driving growth through continuous product refreshes, such as new RMR variants, while staying deeply anchored in military and law-enforcement channels. In addition, they are broadening beyond holographic sights into Vudu/Vudu X riflescopes and adjacent professional optics.

Download Free sample to learn more about this report.

Firearm Sight Market Trends

Growing Demand for Smarter, Integrated, And Versatile Sight Systems Are Driving the Shift Beyond Simple Red Dot Sights

The clearest technology trend is the move from single-function sights to multi-role aiming systems. The U.S. Army’s Next Generation Squad Weapon ecosystem already shows where the market is heading. Army reports on the XM157 Fire Control Systems describe it as a magnified direct-view optic with a laser range finder, environmental sensors, ballistic solver, and digital display overlay. In other words, the industry is moving beyond just putting a dot on glass. The next wave is smarter optics that help the shooter calculate, range, and engage more efficiently. That trend will likely spread from elite military programs into mainstream tactical and professional offerings over time.

For instance, in March 2026, the Army’s xTech|Soldier Fire Finals evaluated emerging fire-control technologies against the XM157, confirming that the government is still actively scouting next-generation optic and fire-control improvements.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Faster Target Acquisition and Force Modernization Are Pushing Buyers Toward Advanced Electro-Optics

The firearm sight market growth is being driven by a basic operational need as shooters want to detect, align, and engage targets faster than they can with legacy iron sights. Military testing is clearly validating this shift. In June 2025, the U.S. Army’s 10th Mountain Division tested the XM152 Mounted Machine Gun Optic for the Mark 19. The Army stated that the optic improves capability through a wide field-of-view holographic reticle for fast close-range acquisition and a 3x magnifier that extends effective range and improves accuracy. That kind of field feedback matters as it shows that customers are not just buying optics for convenience; they are buying them to increase first-round hit probability, battlefield awareness, and engagement flexibility.

For instance, in April 2025, SIG SAUER announced that the Texas Department of Public Safety is transitioning troopers to the SIG M17 with the ROMEO-M17 red-dot optic. Further, showing how institutional adoption is translating into real procurement momentum.

MARKET RESTRAINTS

Regulation, Export-Control Complexity, And Qualification Standards Can Slow Market Expansion

A major restraint in this market is that firearm sights do not move through a normal consumer-electronics channel when they are sold into defense, law-enforcement, or export markets. Companies must deal with export licensing, item classification, end-use scrutiny, and multiple compliance frameworks. The DDTC states plainly that the ITAR governs commercial defense trade, while the BIS and the Federal Register show that firearms-related export rules were tightened in 2024 and then reversed in 2025. That kind of regulatory swing creates uncertainty for manufacturers, distributors, and foreign channel partners. Even when a sight itself is technologically ready, revenue conversion can slow as compliance timelines, licensing burdens, and jurisdictional issues may delay shipments or narrow addressable markets.

For instance, in September 2025, the BIS announced that it had rescinded the 2024 firearms export rule. The agency explicitly noted that the prior restrictions had been estimated by industry to cost manufacturers hundreds of millions of dollars per year in lost sales.

MARKET OPPORTUNITIES

International Security Demand and Wider Institutional Adoption Are Opening New Growth Paths

The biggest opportunity is the widening customer base beyond traditional civilian sporting use. Military modernization, police sidearm upgrades, allied security assistance, and tactical training programs are all creating room for premium optics. DSCA states that Foreign Military Sales (FMS) remains a core U.S. security-assistance tool, and the Defense Department’s 2025 policy push to improve arms-transfer efficiency signals a broader effort to move defense articles to allies faster. For firearm sight suppliers, that matters as optics increasingly travel with complete weapon systems, upgrade kits, and sustainment packages. As more countries modernize infantry weapons and close-combat capabilities, the sight package becomes a standard line item rather than an optional accessory.

For instance, in September 2025, BIS rescinded the earlier firearms export rule and said the change would allow U.S. manufacturers to compete more effectively in overseas markets, creating hundreds of millions of dollars per year in export opportunities.

MARKET CHALLENGES

Power, Sustainment, Procurement Speed, And Field Usability Remain Difficult Execution Issues

A major challenge for the market is that every technology upgrade creates a sustainment burden. Advanced optics may improve lethality, but they also depend more on batteries, electronics, mounting integrity, software logic, and user training. The Army Battery Team has said the Army is accelerating adoption of advanced batteries to reduce physical, cognitive, and logistical burdens on soldiers. That is a useful signal for this market as it shows that power supply and battery logistics are not side issues anymore; they are part of the deployment equation. If an optic is impressive on paper but creates extra burdens in the field, adoption can slow, especially for large military users managing thousands of systems.

For instance, in June 2025, GAO published its latest weapon-systems annual assessment, again warning that DoD leaders need to structure newer programs for more speed and innovation. For sight makers, the message is simple: winning the technology race is not enough; they also need manufacturability, supportability, and acquisition alignment.

SEGMENTATION ANALYSIS

By Sight Types

Clip-On Add-On Magnification Segment Drives Growth Due to Modular Upgrade Demand Without Replacing Core Optics

The global market by sight types is divided into variable magnification, fixed magnification, switchable magnification, and clip-on add-on magnification.

Clip-on add-on magnification is emerging as the fastest-growing sight type, with the highest CAGR of 7.77% during the forecast period. The growth is driven by its ability to allow users, especially military and law enforcement personnel, to upgrade existing optics without replacing the base system. This modularity reduces procurement cost and simplifies logistics, which is critical for defense buyers managing large inventories of weapon systems. Instead of issuing entirely new optics, forces can extend range capability using clip-on magnifiers, making it a cost-efficient modernization path.

The fixed magnification segment accounted for the largest share of the market in 2025 at 32.65% and is estimated to register a CAGR of 3.75% during the forecast period.

By Sight Category

Smart/Digital/Fire-Control Sights Segment Accelerate Growth Due to Integration of Ballistic Computing and Sensor Fusion

The global market by sight category is divided into iron sights, non-magnified electronic sights, holographic sights, prism sights, magnified optical sights, thermal sights, night vision sights, and smart/digital/fire-control sights.

Smart/digital/fire-control sights are estimated to be the fastest-growing segment, with the highest CAGR of 8.17% during the forecast period. The growth is driven by how they fundamentally change the way targeting decisions are made. These systems integrate range finding, environmental sensing, and ballistic computation, allowing users to achieve higher accuracy with less manual adjustment. This shift from “aiming aid” to “decision-support system” is a major leap in value proposition.

The magnified optical sights segment accounted for the largest share of the market in 2025 at 28.41% and is estimated to register a CAGR of 6.62% during the forecast period.

By Illumination Method

IR-Only Emission Illumination Segment Grows Fastest Due to Increasing Demand for Covert and Night Operations

The global market by illumination method is divided into non-illuminated, fiber-optic illuminated, tritium self-luminous, fiber + tritium hybrid, LED battery illuminated, laser projected, and IR-only emission.

IR-only emission systems are projected to be the fastest growing segment, with the highest CAGR of 9.07% during the forecast period. The growth is supported by the increasing demand for covert operations where visibility to the naked eye must be avoided. These systems are essential for military and special forces operating with night vision devices, enabling precise targeting without revealing position. The growth is directly linked to the rising importance of nighttime and low-visibility combat scenarios.

The LED battery illuminated segment accounted for the largest share of the market in 2025 at 33.64% and is estimated to register a CAGR of 6.89% during the forecast period.

By Focal Plane

First Focal Plane Optics Segment Grow Fastest Due to Consistent Reticle Scaling for Precision Shooting

The global market by focal plane is divided into First Focal Plane (FFP), Second Focal Plane (SFP), and dual/hybrid focal configurations.

First focal plane optics are estimated to be the fastest growing segment, with the highest CAGR of 7.17% during the forecast period. This segment is gaining traction as it maintains reticle accuracy across different magnification levels. This is particularly important for long-range and tactical shooting, where range estimation and holdover must remain consistent regardless of zoom. FFP’s adoption is driven by military snipers, designated marksmen, and precision shooters who require reliable ballistic performance.

The second focal plane segment accounted for the largest market share in 2025 at 54.13% and is estimated to register a CAGR of 4.98% during the forecast period.

By Magnification Type

5.1x–8x Magnification Range Segment Expands Fastest Due to Demand for Mid-Range Engagement Versatility

The global market by magnification type is divided into 0x / iron sight, 1x, 1.5x–3x, 3.1x–5x, 5.1x–8x, 8.1x–12x, 12.1x–18x, 18.1x–25x, and above 25x.

The 5.1x–8x magnification is estimated to be the fastest growing segment, with the highest CAGR of 7.47% during the forecast period. In addition, the segment accounted for the largest market share of 19.80% in 2025. The segment offers the best balance between close-range usability and mid-range precision. This range is ideal for modern combat scenarios where engagements often occur between 100–600 meters. Users are moving away from extreme magnification or purely low-power optics toward versatile solutions that can handle multiple engagement distances.

The 1x segment accounted for the second-largest market share of 18.15% in 2025 and is estimated to register a CAGR of 5.63% during the forecast period.

By Weapon Platform

Machine Guns/Crew-Served Small Arms Segment Grow Fastest Due to Modernization of Heavy Weapon Optics

The global market by weapon platform is divided into handguns / pistols, rifles, shotguns, SMGs / PCCs, machine guns / crew-served small arms, crossbows / archery-compatible sight lines, less-lethal launchers, and training / simulation weapons.

The machine guns/crew-served small arms is estimated to be the fastest growing segment, with the highest CAGR of 8.82% during the forecast period. Sights for machine guns and crew-served weapons are expanding quickly as militaries modernize heavy weapon systems. These platforms require more advanced optics to improve accuracy, especially for suppressive fire and long-range engagements.

The rifles segment accounted for the second-largest market share in 2025 at 55.86% and is estimated to register a CAGR of 4.59% during the forecast period.

By Range Band

301–600 M Range Band Segment Grows Fastest Due to Increased Focus On Mid-Range Combat Engagements

The global market by range band is divided into 0–25 m, 26–100 m, 101–300 m, 301–600 m, 601–1,000 m, and above 1,000 m.

The 301–600 m range is estimated to be the fastest-growing segment, with the highest CAGR of 7.71% during the forecast period. The growth reflects the reality of modern combat distances. Many engagements now occur in this mid-range window, especially in semi-urban and open terrain environments. Optics are being optimized specifically for this range, with better magnification options and clearer reticles.

The 101–300 m segment accounted for the second-largest market share in 2025 at 27.82% and is estimated to register a CAGR of 6.34% during the forecast period.

By Power Source

Hybrid Power Systems Segment Grow Fastest Due to Need for Reliability and Extended Operational Endurance

The global market by power sources is divided into no power required, tritium-powered, replaceable battery, rechargeable battery, solar-assisted, external power capable, and hybrid power.

Hybrid power systems are projected to be the fastest-growing segment, with the highest CAGR of 9.23% during the forecast period. The segment is gaining momentum as they combine multiple energy sources, such as batteries and solar assistance, to ensure uninterrupted operation. This is critical in military environments where power reliability can directly impact mission success. The growth is driven by advancements in energy efficiency and power management technologies.

The replaceable battery segment accounted for the second-largest market share in 2025 at 35.04% and is estimated to register a CAGR of 5.94% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Sensor Type

Uncooled Thermal Sensors Segment Grow Fastest Due to Cost-Effective Night and All-Weather Capability

The global market by sensor type is divided into visible only, image intensifier (Gen 2 / 3 / 3+), digital CMOS, uncooled thermal, cooled thermal, and fusion / multispectral.

Uncooled thermal is emerging as the fastest-growing segment, with the highest CAGR of 9.16% during the forecast period. The segment provides thermal detection without the complexity and cost of cooled systems. These sensors enable users to detect targets in complete darkness, smoke, or adverse weather conditions. Technological advancements have significantly improved resolution, sensitivity, and compactness of uncooled sensors.

The visible only segment accounted for the second-largest market share of 57.76% in 2025 and is estimated to register a CAGR of 4.45% during the forecast period.

By Material

Composite Hybrid Housing Segment Grows Fastest Due to Demand for Lightweight and High-Durability Materials

The global market by material is divided into aluminum housing, titanium housing, steel housing, polymer housing, and composite hybrid housing.

Composite hybrid housing is estimated to be the fastest-growing segment, with the highest CAGR of 8.03% during the forecast period. The segment is growing rapidly as it offers the ideal balance between strength and weight reduction. Modern users require optics that can withstand harsh conditions without adding unnecessary load to the weapon system. Material innovation is enabling manufacturers to combine metals and advanced polymers to achieve better shock resistance and durability.

The aluminum housing segment accounted for the second-largest market share in 2025 at 43.60% and is estimated to register a CAGR of 6.34% during the forecast period.

By End User

Training Academies/Ranges Segment Grow Fastest Due to Increased Focus on Simulation and Skill Development

The global market by end user is divided into military, law enforcement, civilian/commercial, security/private defense contractors, and training academies/ranges.

The training academies/ranges is projected to be the fastest-growing segment, with the highest CAGR of 8.41% during the forecast period. The growth is driven by the increasing emphasis on skill development and simulation-based training. Both military and civilian users are investing more in training to improve accuracy and operational readiness. Moreover, the growth is supported by the expansion of professional training programs and recreational shooting activities.

The military segment accounted for the second-largest market share of 46.71% in 2025 and is estimated to register a CAGR of 5.11% during the forecast period.

Firearm Sight Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Firearm Sight Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant global firearm sight market shares in 2025, valued at USD 0.62 billion, and also maintained the leading share in 2026, with USD 0.64 billion. The market is driven by high civilian gun ownership, increasing adoption of advanced optics, and modernization efforts in law enforcement and military. Growing concerns regarding personal safety and security, particularly in the U.S., have significantly boosted the demand for handguns and corresponding accessories such as reflex sights for home defense.

U.S. Firearm Sight Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 0.57 billion in 2025 and is estimated to register a CAGR of 4.56% during the forecast period.

Europe

Europe is projected to grow at the fastest rate, with the highest CAGR of 7.86% during the forecast period. In 2025, the market value stood at USD 0.40 billion. The growth is driven by increased military expenditure, regional security concerns, and a strong hunting culture. The market is driven by technological advancements and the need to modernize existing weapon systems. NATO members are upgrading their infantry weapons to meet collective defense and interoperability standards, driving the demand for advanced, high-tech sights.

U.K. Firearm Sight Market

The U.K. market growth in 2025 was valued at USD 0.08 billion and is estimated to grow at a rate of 6.78% during the forecast period.

Germany Firearm Sight Market

The Germany market growth in 2025 was valued at USD 0.09 billion and is estimated to grow at a rate of 8.43% during the forecast period.

Eastern Europe Firearm Sight Market

The Eastern Europe market growth in 2025 was valued at USD 0.79 billion and is estimated to grow at a rate of 10.32% during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 0.05 billion in 2025 and secured the position of the second-largest region in the market. Rising tensions in hotspots such as the South China Sea and along the China-India border have forced regional powers to upgrade weapon systems, driving demand for advanced laser, thermal and night vision, and thermal imaging sights.

China Firearm Sight Market

The China market growth in 2025 was valued at USD 0.21 billion and is estimated to grow at a rate of 4.86% during the forecast period.

India Firearm Sight Market

The India market growth in 2025 was valued at USD 0.09 billion and is estimated to grow at a rate of 7.09% during the forecast period.

Japan Firearm Sight Market

The Japan market growth in 2025 was valued at USD 0.06 billion and is estimated to grow at a rate of 9.43% during the forecast period.

Middle East & Africa and Latin America

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market was valued at USD 0.09 billion in 2025. Furthermore, the Middle East & Africa market was valued at USD 0.18 billion in 2025.

Israel Firearm Sight Market

The Israel market growth in 2025 was valued at USD 0.03 billion and is estimated to grow at a rate of 7.77% during the forecast period.

Brazil Firearm Sight Market

The Brazil market growth in 2025 was valued at USD 0.04 billion and is estimated to grow at a rate of 2.52% during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Competition Is Intensifying as Leading OEMs Expand and Innovate Products to Improve Performance Across End Users

The competitive landscape in the firearm sight market is led by established optics specialists such as Trijicon, Aimpoint, EOTECH, Leupold & Stevens, and SIG SAUER, and the market is increasingly being shaped by product refresh cycles rather than basic catalog breadth alone.

These companies are competing on durability, mission-specific performance, continuously innovating and the ability to serve military, law-enforcement, and premium commercial users with proven platforms. At the same time, competition is moving toward broader technology implementation and tighter system integration.

LIST OF KEY FIREARM SIGHT COMPANIES PROFILED

- Trijicon, Inc. (U.S.)

- Aimpoint AB (Sweden)

- EOTECH, LLC (U.S.)

- Steiner-Optik GmbH / Steiner (Germany)

- Meopta s.r.o. (Czech Republic)

- Nightforce Optics, Inc. (U.S.)

- Schmidt & Bender GmbH & Co. KG (Germany)

- SWAROVSKI OPTIK AG & Co KG (Austria)

- Vortex Optics (U.S.)

- Meprolight (Israel)

- Hawke Optics Ltd. (U.K.)

- Leupold & Stevens, Inc. (U.S.)

- Vector Optics (China)

- SIG SAUER, Inc. (U.S.)

- HOLOSUN (U.S.)

KEY INDUSTRY DEVELOPMENT

- April 2026: L3Harris was selected by the U.S. Army to provide its NOVA night-vision goggle system under the Binocular Night Observation Device (BiNOD) program, with a seven-year contract worth up to USD 465 million. This is one of the largest recent awards tied to the advanced sighting and soldier-vision segment.

- February 2026: RTX said its Raytheon ELCAN business received a production contract to supply a customized Specter DR 1-4x weapon sight for the German Armed Forces. The company also noted the tailored configuration integrates an Aimpoint reflex sight for faster close-quarters to mid-range transitions.

- February 2025: RTX announced that Raytheon ELCAN was awarded an additional multi-million-dollar contract by the Danish Defense Armed Forces, through NSPA, for ELCAN Specter DR dual-role sights. The award supports replacement of older C79 fixed 3.4x sights with more versatile optics.

- January 2025: L3Harris received a USD 263 million order from the U.S. Army for continued production of the Enhanced Night Vision Goggle–Binocular (ENVG-B). This was the second order under the full-scale production IDIQ, showing sustained demand for fused night-vision systems linked to targeting and engagement.

- August 2024: Leonardo DRS also received a USD 52 million follow-on production order for Sniper Weapon Sights under the Family of Weapon Sights–Sniper (FWS-S) IDIQ. The company described the system as a clip-on thermal weapon sight used with existing day sniper optics.

REPORT COVERAGE

The global firearm sight market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions as well as key rifles or guns industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.91% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Sight Types

By Sight Category

By Illumination Method

By Focal Plane

By Magnification Type

By Weapon Platform

By Range Band

By Power Source

By Sensor Type

By Material

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.84 billion in 2025 and is projected to reach USD 3.04 billion by 2034.

In 2025, the market value stood at USD 0.40 billion.

The market is expected to exhibit a CAGR of 5.91% during the forecast period.

The training academies / ranges segment is expected to hold the highest CAGR over the forecast period.

Faster target acquisition and force modernization are pushing buyers toward advanced electro-optics.

Trijicon, EOTECH, Aimpoint, Leupold & Stevens, and SIG SAUER are the top key players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us