Firestopping Sealants Market Size, Share & Industry Analysis, By Chemistry (Acrylic, Silicone, Polyurethane, and Others), By End Use (Commercial Buildings, Residential Buildings, and Industrial & Utility Facilities), and Regional Forecast, 2026-2034

Firestopping Sealants Market Size and Future Outlook

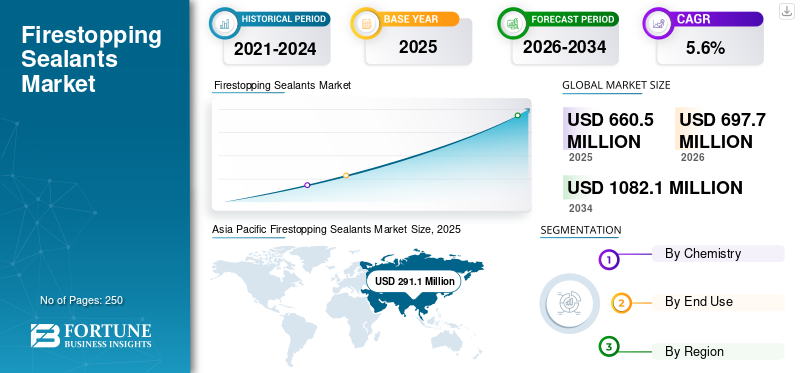

The global firestopping sealants market size was valued at USD 660.5 million in 2025. The market is projected to grow from USD 697.7 million in 2026 to USD 1,082.1 million by 2034, exhibiting a CAGR of 5.6% during the forecast period. Asia Pacific dominated the firestopping sealants market with a market share of 44.07% in 2025.

Firestopping sealants are specialized passive fire-protection materials formulated to seal joints and service penetrations, such as cables, conduits, pipes, ducts, and mixed Mechanical, Electrical, and Plumbing (MEP) systems, in fire-rated walls and floors. These materials maintain compartmentation by limiting the spread of fire, smoke, and hot gases. These sealants are typically designed around acrylic, silicone, or hybrid chemistries. Many systems rely on intumescent behavior, which expands under high temperatures to close voids created by melting substrates or interface movement. These sealants offer strong adhesion to common construction surfaces such as concrete, masonry, gypsum, and metals, but also jobsite-friendly attributes, including tooling, paintability, and movement accommodation. In commercial buildings, industrial facilities, and high-occupancy infrastructure projects, firestopping sealants are deployed at scale across various applications, driving product demand for compliance-driven retrofits.

The global market is shaped by manufacturers that compete on tested-and-listed system breadth, installer productivity, and technical engineering support aligned with UL/ASTM-tested assemblies and local building regulations. Major participants include 3M Company, Dow, Sika, Fischer, RectorSeal, and other fire-protection-material specialists expanding portfolios across sealants, sprays, wraps, putties, and accessories. Ongoing product development is focused on increased joint mobility, improved smoke-seal performance, faster curing times, and cleaner application characteristics.

Download Free sample to learn more about this report.

FIRESTOPPING SEALANTS MARKET TRENDS

Shift Toward Tested-System Standardization to Shape Market Dynamics

A key trend shaping the market is the shift toward standardized, system-based testing and certification, driven by stricter inspections, third-party audits, and increased accountability across construction industry value chains. Specifiers and contractors increasingly favor sealants that are part of clearly documented, UL-, ASTM-, and EN-tested assemblies, reducing installation risk and inspection failures. Alongside regulatory compliance, sustainable building practices are gaining importance. Demand is rising for low-VOC formulations, improved indoor air quality compatibility, and solutions that reduce jobsite waste. Manufacturers are responding by enhancing documentation, developing selection tools for digital systems, and offering environmentally optimized products. This dual focus on compliance certainty and sustainability is reshaping product development and competitive positioning across global markets.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Strict Fire Safety Codes to Drive Market Growth

The global firestopping sealants market is expected to grow primarily due to the tightening of fire safety regulations and the continued growth of high-rise and high-occupancy buildings across both developed and emerging economies. Modern buildings increasingly incorporate dense MEP networks, resulting in a higher volume of increasing the number of service penetrations and joints that require certified firestopping systems to maintain compartmentation. Regulatory bodies are enforcing stricter inspection regimes, particularly in commercial buildings, healthcare facilities, and residential towers, leading to higher adoption of firestop sealant systems. Additionally, government investments in urban infrastructure and public buildings, including hospitals, metros, airports, and affordable housing programs, are reinforcing demand for compliant passive fire protection solutions. Together, stronger regulatory enforcement and sustained vertical construction activity are driving the global firestopping sealants market growth during the forecast period.

MARKET RESTRAINTS

Presence of Alternative Fire Barrier Systems May Limit Product Adoption

Despite strong regulatory drivers, the market faces restraints stemming from inconsistent fire safety standards and enforcement levels across regions, particularly in parts of Asia, Latin America, and Africa. In markets with limited inspection rigor, adoption of certified firestopping sealants remains uneven, with some projects relying on lower-cost, non-certified sealing practices. Additionally, alternative fire barrier solutions such as fire-rated boards, wraps, collars, and mortar systems can reduce sealant consumption in certain applications, especially for large penetrations or structural openings. Cost sensitivity in residential and small commercial construction further constrains the uptake of higher-performance sealant systems. These key factors collectively limit penetration in price-driven, lightly regulated construction markets, thereby restraining overall growth potential.

MARKET OPPORTUNITIES

Infrastructure Modernization and Demand for Certified Passive Fire Protection Systems to Create Lucrative Opportunities

Significant opportunities are emerging from infrastructure modernization initiatives and the growing emphasis on certified passive fire protection systems in public and private construction projects. Upgrades to aging commercial buildings, transportation hubs, utilities, and industrial facilities are driving demand for firestopping sealants in retrofit and remediation projects, where non-compliant penetrations must be brought up to current safety standards. Governments across major economies are allocating capital toward smart cities, transportation corridors, healthcare infrastructure, and public housing, all of which require adherence to modern fire-safety standards. In parallel, insurers, developers, and asset owners are prioritizing tested and documented firestop systems to reduce long-term fire risk and liability. These trends are creating attractive opportunities for manufacturers offering certified firestopping solutions.

Segmentation Analysis

By Chemistry

Acrylic Segment Dominated Due to their Cost-Effective and Strong Adhesiveness

Based on chemistry, the market is segmented into acrylic, silicone, polyurethane, and others.

The acrylic segment accounted for the largest global firestopping sealants market share in 2025. Acrylic-based firestop sealants remain the preferred option for high-volume interior applications, such as head-of-wall joints, gypsum-to-concrete interfaces, perimeter gaps, and standard service penetrations, due to their cost advantage, strong adhesion to porous substrates, paintability, and widespread installer familiarity. Acrylic is expected to maintain its dominance, anchored by large-scale commercial and residential fit-out activities that require standardized interior firestop detailing.

The silicone segment is projected to be the fastest-growing chemistry, with an expected CAGR of 6.1%. Growth is supported by increasing adoption in high-movement joints, perimeter fire containment, façade interfaces, and demanding environments where elasticity, weathering resistance, and long-term durability are critical, especially in high-rise, infrastructure, and mission-critical buildings.

By End Use

Commercial Buildings Segment Led Due to Higher Utilization and Inspection-Driven Compliance

By end use, the market is segmented into commercial buildings, residential buildings, and industrial & utility facilities.

The commercial buildings segment accounted for the largest share. The segment’s dominance is driven by high utilization of firestopping sealants in fire-rated walls and floors, and stringent third-party inspection requirements across offices, hospitals, airports, and educational institutions. Commercial developments typically involve frequent service routing changes, increasing reliance on firestop sealants for both initial construction and post-occupancy modifications. Additionally, refurbishment and tenant fit-out cycles generate recurring demand, as penetrations must be resealed to maintain fire compartmentation. The segment’s growth is further supported by sustained commercial construction activity, increasing retrofits of aging building stock, and heightened regulatory enforcement in high-occupancy structures.

To know how our report can help streamline your business, Speak to Analyst

The residential buildings segment is projected to be the fastest-growing end-use category, expanding at a 5.9% CAGR during the study period. Growth is closely linked to rapid urbanization, the expansion of high-rise and multi-family housing, and the tighter enforcement of fire-safety and smoke-containment regulations in residential developments. Modern residential buildings feature higher service density than traditional housing, including centralized HVAC systems, electrical risers, and shared service shafts, all of which require effective firestopping. Additionally, regulatory authorities are placing increased emphasis on compartment integrity between units and common areas, driving greater use of such sealants in walls, floors, and ceiling assemblies.

Firestopping Sealants Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Firestopping Sealants Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global firestopping sealants market in 2025, reaching USD 291.1 million, and is projected to grow to USD 308.2 million by 2026. The region’s leadership is driven by dense MEP installations in modern buildings, increasing enforcement of fire-safety regulations, and large-scale investments in transportation hubs, healthcare facilities, and mixed-use developments. The region also benefits from cost-competitive construction activity, a growing base of international developers, and gradual alignment of local fire codes with global standards, particularly in high-occupancy and commercial projects.

China Firestopping Sealants Market

Given Asia Pacific’s dominant contribution and China’s construction scale, the China market is expected to be valued at USD 157.7 million by 2026, accounting for ~23% of global revenues.

To know how our report can help streamline your business, Speak to Analyst

India Firestopping Sealants Market

The India market is estimated to reach USD 48.3 million by 2026, representing around ~7% of global revenues. Growth is supported by rapid urban development, expansion of commercial office spaces, data centers, metro rail projects, and multi-family housing, where fire compartmentation requirements are gaining regulatory emphasis.

North America

North America remains a significant regional market, reaching USD 145.1 million in 2025. North America’s market is supported by stringent building codes, mature construction practices, and robust enforcement of compliance across commercial and institutional buildings. The region benefits from high retrofit activity, frequent tenant fit-outs, and strong demand from healthcare facilities, data centers, airports, and industrial buildings, all of which require rigorous firestop inspection and documentation.

U.S. Firestopping Sealants Market

The U.S. market in 2026 is valued at USD 136.8 million, accounting for approximately ~20% of global revenues.

Europe

Europe reached a valuation of USD 168.0 million in 2025 and is projected to grow at a CAGR of 5.5% over the coming years. The region represents a mature, compliance-intensive market characterized by strong emphasis on fire safety, building integrity, and standardized construction practices. Demand is supported by commercial buildings, residential developments, and infrastructure upgrades, particularly in Western Europe. The region’s regulatory environment, combined with widespread adoption of third-party inspections, continues to favor consistent use of certified firestopping systems.

Germany Firestopping Sealants Market

The Germany market reached USD 39.9 million in 2026, equivalent to approximately ~6% of global revenues. A strong commercial construction base, extensive industrial facilities, and stringent fire-protection standards support steady demand.

U.K. Firestopping Sealants Market

The U.K. market in 2026 is estimated at USD 29.5 million, accounting for roughly ~4% of global revenues. Growth is supported by heightened focus on fire safety compliance in residential and commercial buildings, particularly following regulatory reforms and increased inspection rigor.

Latin America

Latin America reached a market valuation of USD 31.7 million in 2025. The region represents a developing but steadily expanding market, supported by urban construction, infrastructure investment, and growing awareness of fire-safety requirements in commercial and industrial facilities.

Brazil Firestopping Sealants Market

The Brazil market in 2026 is valued at USD 15.2 million, accounting for approximately ~2% of global revenues. Demand is supported by commercial buildings, industrial facilities, and infrastructure projects, particularly in major urban centers.

Middle East & Africa

The Middle East & Africa’s market stood at USD 24.6 million in 2025. The market remains comparatively smaller but structurally important, supported by large-scale infrastructure development, commercial construction, and industrial projects across the GCC and selected African economies.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focus on Investment to Shape Competitive Dynamics

The global market is characterized by competition among established construction chemicals manufacturers and specialized passive fire-protection providers. Competitive differentiation is driven less by volume scale and more by tested-and-listed system coverage, regulatory compliance, and installer support capabilities. Leading players such as 3M Company, Dow, Sika, Fischer, and RectorSeal maintain strong positions through broad portfolios covering multiple sealant chemistries, penetration types, and joint conditions. Competitive strength is further reinforced by engineering-driven product development, third-party certifications, digital submittal tools, and on-site training programs, which help reduce inspection failures and installation risk. Ongoing investments in high-movement sealants, faster-curing formulations, and low-VOC solutions continue to shape competitive dynamics in regulated construction environments.

LIST OF KEY FIRESTOPPING SEALANTS COMPANIES PROFILED

- 3M Company (U.S.)

- Dow (U.S.)

- Fischer (Germany)

- Promat (Belgium)

- Rectorseal (U.S.)

- Satiate Solutions (India)

- SIKA (Switzerland)

- Tremco Incorporated (U.S.)

- Unitech (India)

- Vijay Systems Engineers (India)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Sika strengthened its passive fire protection offering by further integrating firestopping sealants within its broader joint sealing and building envelope systems. This move supports standardized detailing across fire-rated joints and penetrations in significant commercial and residential developments.

- September 2024: 3M Company expanded its fire protection product line with a new intumescent firestop sealant for high-movement joints in commercial buildings. The product offers enhanced flexibility and improved fire resistance to meet modern construction needs and regulatory requirements.

- June 2024: Promat introduced improvements across its PROMASTOP® and PROMASEAL® firestopping systems, including more adaptable fire collars and sealant solutions for mixed pipe and cable penetrations. The update emphasized installation efficiency and broader system coverage for infrastructure and commercial projects.

REPORT COVERAGE

The global firestopping sealants market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.6% from 2026 to 2034 |

| Unit | Value (USD Million) Volume (Kiloton) |

| Segmentation | By Chemistry, End Use, and Region |

| By Chemistry |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 660.5 million in 2025 and is projected to reach USD 1,082.1 million by 2034.

In 2025, the market value stood at USD 291.1 million.

Recording a CAGR of 5.6%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

The commercial buildings segment led the market in 2025 by end use.

Stricter fire safety codes and increasing high-rise construction are the key factors driving the market.

3M Company, Dow, Sika, Fischer, and RectorSeal are identified as prominent players in the market.

Asia Pacific held the highest market share in 2025.

Infrastructure modernization and growing demand for certified passive fire protection systems are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us