Fish Processing Market Size, Share & Industry Analysis, By Product Type (Frozen Fish, Canned Fish, Fish Meal, and Others), By Species (Fish, Crustaceans, Mollusks, and Others), By Form (Whole, Fillets, Steaks, Chunks, and Others), By Processing Technology (Freezing, Thermal, Drying, and Others), By End-Use (Food Use and Non-Food Use), and Regional Forecast, 2026–2034

(Offer valid till 31st Jul 2026)

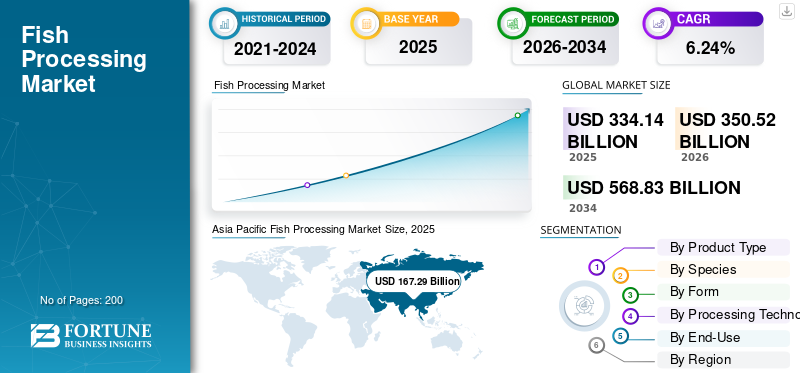

Fish Processing Market Size and Future Outlook

The global fish processing market size was valued at USD 334.14 billion in 2025. The market is projected to grow from USD 350.52 billion in 2026 to USD 568.83 billion by 2034, exhibiting a CAGR of 6.24% during the forecast period. Asia Pacific dominated the fish processing market with a market share of 50.06% in 2025.

Fish processing involves the commercial handling, preservation, and transformation of fish and aquatic organisms from harvest to final delivery to consumers, extending shelf life and adding value. It encompasses activities such as cleaning, gutting, freezing, smoking, and canning, catering to both food consumption and non-food uses, such as fishmeal. Increasing consumption of protein-rich foods, omega-3 fatty acids-based supplements, along with the rising popularity of seafood among millennials and youth consumers, will drive market growth. Stable fish and aquatic animal production, paired with adopted sustainable practices, to produce or capture aquatic animals, promoting industry growth to new heights.

Maruha Nichiro Corporation, Thai Union Group, Nissui Corporation, Mowi ASA, Bolton Group, and others dominate the market.

Download Free sample to learn more about this report.

Fish Processing Market Key Takeaways

- 2025 Market Size: USD 334.14 billion

- 2026 Market Size: USD 350.52 billion

- 2034 Forecast Market Size: USD 568.83 billion

- CAGR: 6.24% from 2026–2034

- Asia Pacific dominated the fish processing market with a 50.06% share in 2025.

- The frozen fish segment dominated the market, reaching USD 137.06 billion in 2025.

- The fish segment held the largest market share, valued at USD 220.11 billion in 2025.

Asia Pacific

Asia Pacific led the global market with a valuation of USD 167.29 billion in 2025 and is the fastest-growing region.

North America

North America generated USD 48.81 billion in 2025 and is projected to grow steadily during the forecast period.

Europe

Europe recorded fish processing product consumption of USD 71.87 billion in 2025.

U.S.

The market was valued at approximately USD 38.03 billion in 2025 and is expected to expand at a CAGR of 5.40%.

Japan

Rising seafood consumption and demand for processed fish products are supporting market growth.

Read More

Fish Processing Market Trends

Rise in Sustainable Fish Capturing to Curate a Newer Market Trend

Sustainability is becoming a defining trend in the fish processing market as regulators, retailers, foodservice operators, and end consumers increasingly prioritize responsibly sourced seafood. Processing companies are under growing pressure to secure raw materials from legal, traceable, and biologically sustainable fisheries, while also reducing post-harvest losses and improving transparency in the chain of custody. This is changing procurement strategies, supplier qualification standards, labeling practices, and investment priorities across the industry. The shift toward sustainable fish capture is also strengthening the long-term positioning of processors that can demonstrate sustainable sourcing and compliance with fishery-management frameworks. In practical terms, this is pushing processors toward better traceability systems, tighter quality control, improved cold-chain handling, and stronger relationships with certified or well-managed fisheries. As sustainability becomes a commercial differentiator rather than only a compliance issue, it is reshaping how fish processors compete in export and premium domestic markets.

- According to the Marine Stewardship Council (MSC), a global nonprofit organization, nearly 20.6% of all wild marine catch worldwide is MSC-certified. Global sales of MSC-certified fish & fish products increased by nearly 8% in 2025.

According to MSC, U.K. and Irish sales of sustainable seafood supplements, such as marine collagen and cod liver oil, doubled last year, reaching USD 17.4 million in 2025.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Increasing Popularity and Consumption of Seafood to Drive Market Development

The global fish processing market growth is being supported by the rising popularity of seafood as a mainstream protein source across both developed and developing economies. Consumers are increasingly shifting toward seafood because of its strong nutritional profile, including high-quality protein, omega-3 fatty acids, vitamins, and minerals. In parallel, urbanization, higher disposable incomes, and broader cold-chain access are making processed fish products more widely available across modern retail, foodservice, and e-commerce channels. As seafood consumption expands, processors benefit from higher demand for frozen, canned, smoked, dried, and other value-added fish products. Thus, the increased consumption-led growth directly supports the seafood processing industries, as a larger share of seafood demand now depends on preservation, portioning, packaging, and value addition rather than on fresh local sales alone. According to the Organisation for Economic Co-operation and Development (OECD), global per capita consumption of aquatic animals is projected to increase, reaching 21.8 kg by 2034, up from 21.1 kg in 2022-2024. Processed formats improve shelf life, transportability, safety, and convenience, allowing seafood to move through wider domestic and international supply chains. As a result, stronger seafood consumption translates into greater demand for freezing, thermal processing, drying, smoking, and secondary processing activities globally.

- According to the European Fishmeal and Fish oil Producers, global fish consumption increased from 188.9 million tonnes in 2023 to 197 million tonnes in 2025, a 4.3% increase during the period. Food consumption volume increased by nearly 3.5% to reach 176 million tonnes in the same period.

Market Restraints

Low Processing Yield Due to Labor Costs and Utilities to Hamper Market Expansion

Low processing yield remains a major restraint for the market, as a significant portion of the raw fish weight is lost at each stage, including gutting, heading, deboning, skinning, trimming, cooking, drying, and others. Depending on processing, end-product type, and species, fish processing generates waste, often comprising 30–70% of the raw material: solid offal (heads, guts, skin, bones, & fins) and liquid effluents. The problem is especially visible in species and product categories where edible recovery is materially lower than live or as-purchased weight. This reduces the saleable output per tonne of raw material and raises the effective input cost per tonne of finished product. As raw fish prices, labor costs, utilities, and compliance expenses increase, low yield can significantly compress processor margins. It will hamper the market growth in the upcoming years.

Market Opportunities

Growing Ready-to-Eat Food Product Demand to Create Better Market Opportunities

The rising demand for ready-to-eat and convenience-oriented food products is creating a strong opportunity for the market. Consumers increasingly prefer products that reduce preparation time while still offering nutrition, taste, and portability. This trend is favoring processed seafood formats such as canned fish, pre-cooked frozen seafood, marinated portions, smoked fish, seafood snacks, and meal-ready packs. In high-income and urban markets, convenience is becoming a key driver of processed seafood. This shift is encouraging processors to move beyond basic preservation and invest in product innovation, packaging, portion control, shelf-life enhancement, and premium convenience formats. As households become smaller and foodservice, quick-service, and retail convenience channels expand, the industry is gaining room to commercialize higher-margin ready-to-eat and ready-to-cook seafood products. This is expected to support both value growth and product diversification in the global fish processing industry.

- According to the People's Network Report on Development Statistics, the prepared food industry has been expanding at a 20% growth rate in recent years. It is expected to exceed one trillion yuan by 2026. Additionally, there are 68,000 players operating in the country, and nearly 11,000 new enterprises have been registered in 2024.

SEGMENTATION ANALYSIS

By Product Type

Broad Consumption Base and Strong Shelf Life to Drive the Frozen Fish Segment Growth

Based on product type, the market is segmented into frozen fish, canned fish, fish meal, and others.

The frozen fish segment dominated the market in 2025, valued at USD 137.06 billion. Frozen fish represent the largest segment due to their wide commercial acceptance, longer shelf life, and suitability across retail, foodservice, and export channels. Frozen fish is one of the most scalable processed seafood formats because it preserves product quality for longer, supports bulk international trade, and meets demand for fillets, whole fish, portions, and other standardized formats. Its strong adoption in supermarkets, restaurants, hotels, and institutional food supply further strengthens its market position. As seafood consumption continues to increase globally, frozen fish remains the most practical and widely traded product type, thereby sustaining its leading share in the fish processing industry.

The fish meal segment is projected to grow at the fastest CAGR of 6.96% during forecast period, due to increasing demand from the aquaculture practices and animal nutrition industries.

By Species

High Availability and Wide Consumption Base to Drive the Fish Segment Growth

Based on species, the market is segmented into fish, crustaceans, mollusks, and others.

The fish segment led the largest global market share in 2025, reaching USD 220.11 billion, due to its abundant availability, widespread consumption, and extensive use across multiple processed product categories. Fish is the most commercially important raw material in the industry because it is processed into frozen, canned, dried, and smoked products, as well as fillets, steaks, chunks, and fish meal. High production volume from both capture fisheries and aquaculture further strengthens supply availability for processors. Owing to its volume advantage, better access to raw materials, and greater product adaptability, the fish segment continues to hold the highest market share.

The crustaceans segment is expected to grow at the fastest CAGR of 7.27% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Form

High Consumer Preference and Broad Stability Led The Fillets Segment's Growth

Based on form, the market is segmented into whole, fillets, steaks, chunks, and others.

The fillets segment held the largest share of the market in 2025, valued at USD 120.85 billion, due to its high consumer preference, ease of use, and broad suitability across retail, foodservice, and industrial applications. Fillets are one of the most commercially preferred processed fish forms as they offer convenience, reduced preparation time, and better portion control compared with whole fish and other traditional formats. Its boneless or low-bone nature makes the product highly acceptable among consumers seeking ready-to-cook, easy-to-handle seafood products. As a result, fillets have gained strong penetration across supermarkets, hypermarkets, restaurants, hotels, and institutional food channels.

The chunks segment is projected to grow at the fastest CAGR of 7.29% during the forecast period. Product demand is increasing due to rising adoption across canned seafood, ready-to-eat meals, ready-to-cook products, and industrial food applications.

By Processing Technology

Longer Shelf-Life and Popularity of Frozen Seafood to Drive the Freezing Segment's Growth

Based on processing technology, the market is segmented into freezing, thermal, drying, and others.

The freezing segment held the largest proportion in the global fish processing market share in 2025, valued at USD 156.32 billion. The segment offers the most effective balance between shelf-life extension, product quality retention, and large-scale commercial distribution. Since fish is highly perishable, processors rely heavily on freezing to slow microbial activity, reduce spoilage risk, and preserve texture, taste, and nutritional value for a longer period. Furthermore, frozen seafood has become the most widely accepted format in retail, foodservice, and export markets, further strengthening the segment's share.

The thermal segment is projected to grow at the fastest CAGR of 7.05% during the forecast period, owing to rising consumer demand for shelf-stable and ready-to-eat seafood products is driving the need for heat-based processing methods.

By End-Use

Strong Demand Across Retail and Foodservice to Drive the Food Use Segment Growth

Based on end use, the market is bifurcated into non-food and food uses.

Food use accounted for the largest share in 2025, valued at USD 290.83 billion. Growing demand for high protein foods, increasing consumer preference for seafood, and the growing availability of processed fish products across supermarkets, hypermarkets, convenience stores, and foodservice outlets are all supporting the dominance of this segment. Frozen fish, canned fish, smoked fish, dried fish, fillets, chunks, and ready-to-cook seafood products are widely consumed across households, restaurants, and institutional channels, driving segment growth in the forecast period.

The non-food segment is projected to witness the fastest CAGR of 5.73% during the forecast period.

Fish Processing Market Regional Outlook

Regionally, the global market analysis spans across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Fish Processing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 48.81 billion in 2025 and is projected to grow at a CAGR of 5.53% during the forecast period. North America remains a major market for fish processing as seafood demand in the region is increasingly tied to convenience, nutrition, and a reliable year-round supply rather than to only fresh local landings. The U.S. Department of Commerce, National Oceanic and Atmospheric Administration (NOAA), Fisheries Office of Science and Technology, publishes estimates of U.S. per capita consumption of seafood products, which increased by 38% and reached 20.8 pounds per person in 2022, compared with 1990.

U.S. Fish Processing Market

The U.S. market was valued at approximately USD 38.03 billion in 2025 and is expected to expand at a CAGR of 5.40% during the forecast period. The U.S. dominates the processed fish consumption in the region. Demand is especially strong in frozen, portion-controlled, and convenience-led formats. At the same time, processors also benefit from the country's advanced inspection, traceability, and trade infrastructure. Even as domestic aquaculture expands selectively, the U.S. market remains heavily import-led, which creates sustained demand for secondary processing, cold storage, repacking, and branded seafood products.

Europe

Europe is one of the most important global regions for fish processing. However, the market is now being shaped more by value preservation than by volume expansion. The consumption of fish processing products in the region accounted for USD 71.87 billion in 2025 and is anticipated to grow at a CAGR of 4.89% during the forecast period. Recent market conditions show that processors are operating in a more price-sensitive environment, with consumers reducing fresh-at-home purchases while continuing to spend on seafood overall. This is pushing the industry toward formats with stronger shelf life, clearer convenience benefits, and better value retention, including frozen products, canned seafood, and premium smoked categories. According to the European Commission's 2025 Europe Fish Market report, consumer spending on fishery and aquaculture products rose 4% in 2024 to approximately 67.96 billion. That dynamic is highly supportive of further processing, preservation, and value addition rather than simple fresh volume growth.

Spain Fish Processing Market

Spain accounted for approximately USD 15.96 billion in 2025. Spain is the most strategically important country market within Europe for fish processing because it combines high per-capita seafood consumption with very large import dependence and the region's deepest industrial processing base. Spain plays a dual role in the market: it is both a major consumer market and a major transformation hub for canning, freezing, and prepared seafood. This gives the country an outsized role in European processing of tuna, small pelagics, cephalopods, and shellfish. USDA FAS states that in 2024, Spain was the fourth-largest importer of fish and seafood in the world and that it has the largest fish-processing industry in Europe. That scale, combined with persistent import dependence, keeps Spain central to Europe's processed seafood outlook.

Asia Pacific

Asia Pacific fish processing market reached USD 167.29 billion in 2025 and is the fastest-growing region, with a 7.14% CAGR. Asia Pacific remains the dominant region globally because it combines raw-material availability, large-scale aquaculture practices, export-oriented manufacturing, and high domestic seafood consumption into an integrated regional system. The market is not driven by one single factor: China anchors upstream production and downstream processing, Southeast Asia supports large export-oriented freezing and canning operations, and India continues to strengthen its position in shrimp and marine export processing. The region also benefits from broad species diversity, competitive labor structures, and deep interregional trade flows. OECD-FAO's 2025 outlook states that Asia is expected to account for 75% of global growth in aquatic-animal-food consumption over the outlook period, and that Asia will still account for about 88% of global aquaculture output by 2034. Those structural advantages explain why the Asia Pacific continues to lead the global fish processing industry in both scale and processing depth.

China Fish Processing Market

China was valued at USD 69.11 billion in 2025. China remains the single most important country in the Asia Pacific regional market because it combines the world's largest seafood production base with huge domestic demand and a sophisticated import-processing-export structure. The country's processing industry benefits from aquaculture-led raw material growth, broad species coverage, large freezing and prepared-food capacity, and continued demand for higher-value imported seafood such as salmon, lobster, and shrimp. USDA FAS reports that China remained the world's largest seafood producer in 2024 at 74.1 million metric tons, up 4% from 2023. China is not only a production powerhouse but also a major demand center for internationally traded seafood. That combination keeps China central to global fish processing.

India Fish Processing Market

India reached USD 27.38 billion in 2025. India is emerging as one of the fastest-advancing in the Asia Pacific because its seafood sector is highly export-oriented, strongly linked to frozen shrimp, and increasingly integrated into global cold-chain trade. The industry's growth is being supported by aquaculture expansion, export market diversification, and stronger processing specialization and domestic consumption growth. According to the Government of India, the country exported 1,698,170 metric tons of seafood worth USD 7.45 billion in FY 2024–25, and frozen shrimp remained the major exported item in both quantity and value

South America and the Middle East & Africa

South America accounted for USD 29.93 billion in 2025, growing at a CAGR of 6.34%. South America's processing economics are still heavily influenced by export-oriented primary transformation and industrial reduction. That makes the region especially sensitive to catch cycles, ocean conditions, and international feed markets. OECD-FAO's 2025 outlook also indicates that the Americas will account for 11% of the growth in global aquatic-food consumption over the coming decade, while capture-fishery gains are expected to be more visible in the Americas than in Europe. This keeps South America highly relevant to global fish processing, especially in fishmeal, fish oil, salmon, and frozen shrimp-linked supply chains.

The Middle East & Africa market was valued at USD 16.23 billion in 2025, expanding at a CAGR of 3.83%. The Middle East & Africa market is growing from a smaller base, but its processing outlook is improving as frozen and shelf-stable seafood become more important in food security, modern retail, and cross-border trade. The market is also supported by import-led demand in the Gulf and by rising aquaculture ambitions across parts of Africa. OECD-FAO's 2025 outlook projects that Africa will account for 15% of global growth in aquatic-animal-food consumption over the next decade and that Africa will post the fastest total consumption growth rate, at 24%, even though per-capita availability remains under pressure in Sub-Saharan Africa.

South Africa Fish Processing Market

The South Africa market was valued at approximately USD 4.13 billion in 2025 and is projected to grow at a CAGR of 4.07% during 2026–2034. South Africa is one of the few markets in the region where fisheries governance, harbor infrastructure, and commercial seafood handling are institutionalized enough to support sustained processing activity. Government investment in infrastructure for fish processing to improve landing efficiency, formalize supply chains, and create better conditions for freezing, packing, and value addition, thereby driving market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Base Expansion to Strengthen their Presence will Change the Competitive Landscape

The global market is mederatley consolidated, dominated by a limited number of large global manufacturers and several regional players. Key players such as Maruha Nichiro Corporation, Thai Union Group, Nissui Corporation, Mowi ASA, and Bolton Group are dominating the market. The key players are investing in expanding their production capacity and adopting advanced technologies to reduce waste and achieve sustainable certifications and practices. It will change the competitive landscape in the upcoming years.

Key Players in the Global Market

|

Rank |

Company Name |

|

1 |

Maruha Nichiro Corporation |

|

2 |

Thai Union Group |

|

3 |

Nissui Corporation |

|

4 |

Mowi ASA |

|

5 |

Bolton Group |

List of Key Fish Processing Companies Profiled

- Thai Union Group (Thailand)

- Maruha Nichiro Corporation (Japan)

- Nissui Corporation (Japan)

- Mowi ASA (Norway)

- Dongwon Industries (South Korea)

- Austevoll Seafood (Norway)

- Lerøy Seafood Group (Norway)

- Pesquera Exalmar (Peru)

- Century Pacific Foods Inc. (Philippines)

- Bolton Group (Italy)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Shinkei Systems, the seafood robotics company, purchased a 16,000-square-foot processing plant in Tacoma, Washington, from Fathom Seafood, a well-respected seafood processor in the Seattle area.

- February 2026: The Government of India inaugurated a frozen fish processing center in Nagpur, India. The new plant has a processing capacity of 12,000 tonnes, including 1,200 tonnes of ready-to-cook and 2,400 tonnes of raw frozen fish, annually.

- January 2026: Mowi, one of the leading fish processing company from Norway, opened its first processing plant in Thailand. The company partnered with the country's largest salmon importer and retailer, CP Axtra, to open its production plant in Thailand.

- August 2025: Oleksandr Svishchov, a Ukrainian businessman, philanthropist, and president of the Ukrainian Water Polo Federation, opened a modern fish-processing plant in the Lviv region. The new plant is situated on 6,800 m² and has a capacity of 300 tonnes per month.

- August 2025: Cite Marine, a subsidiary of Nissui Corporation, has acquired a new processing facility in Pontivy, France, from Trétour de Paris. The company aimed to increase its production strength in the country amid rising seafood demand.

REPORT COVERAGE

The market report analyzes the market in depth and highlights key aspects, including market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. In addition, the research report provides insights into the global market and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.24% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Species

|

|

|

By Form

|

|

|

By Processing Technology

|

|

|

By End-Use

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 334.14 billion in 2025 and is anticipated to reach USD 568.83 billion by 2034.

At a CAGR of 6.24%, the global market will exhibit steady growth over the forecast period.

By product type, the frozen fish segment led the market.

Asia Pacific held the largest market share in 2025.

Increasing popularity and consumption of seafood will drive market growth.

Maruha Nichiro Corporation, Thai Union Group, Nissui Corporation, Mowi ASA, Bolton Group, among others, are the leading companies in the market.

Sustainable fish capturing to change the industry outlook.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us