Forklift Rental Market Size, Share & Industry Analysis, By Vehicle Type (Class I, Class II, Class III, Class IV, and Class V), By Lift Capacity (Below 5 Tons, 6–10 Tons, and Above 11 Tons), By Propulsion Type (ICE and EV), By Rental Period (Short-Term Rentals, Medium-Term Rentals, and Long-Term Rentals), By End-Use Industry (Warehousing & Logistics, Construction, Automotive, Food & Beverage, and Others), and Regional Forecast, 2026-2034

Forklift Rental Market Size and Future Outlook

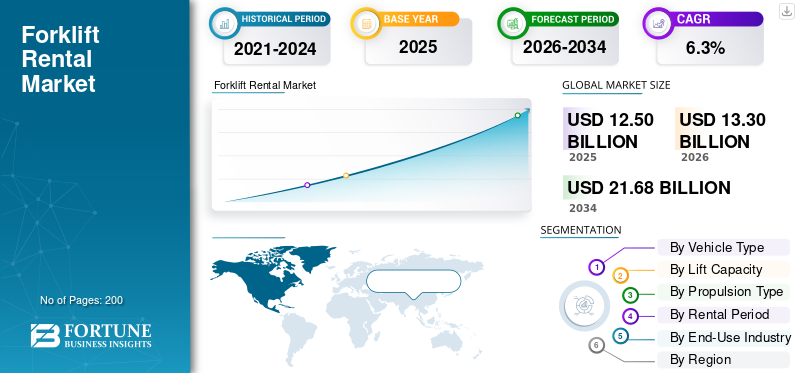

The global forklift rental market size was valued at USD 12.50 billion in 2025. The market is projected to grow from USD 13.30 billion in 2026 to USD 21.68 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the global forklift rental market with a market share of 52.48% in 2025.

The forklift rental market refers to the industry in which businesses and individuals lease forklifts for a specified period rather than purchasing them outright. This market encompasses the short-term, medium-term, and long-term rental of various types of forklifts, including electric forklifts and diesel forklifts, used for material handling in industries such as manufacturing, logistics, construction, warehousing, retail, and ports. The equipment demand is primarily influenced by companies aiming to avoid capital expenditure, manage seasonal fluctuations, and ensure uninterrupted operations without long-term ownership commitments.

The market growth is driven by the rising demand for material handling equipment and pressure on industries to optimize costs, improve equipment utilization, and ensure operational agility. Companies are increasingly opting for equipment rental solutions to avoid high upfront investments, depreciation risks, and complex maintenance responsibilities. The expansion of e-commerce, warehouse automation, and construction activities underscores the need for flexible and scalable equipment access.

Key players in the market focus on expanding fleet diversity, enhancing service responsiveness, and improving contract flexibility to strengthen market position. Leading companies differentiate themselves through large multi-brand inventories, nationwide service networks, and value-added offerings such as operator training, predictive maintenance, and on-site technical support. Competitive advantage increasingly depends on reliability, service speed, and customizable rental solutions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Growing Demand for Cost-Efficient Material Handling Solutions to Drive the Market Growth

A major driver in the market is the increasing emphasis on cost-efficient material handling among manufacturing, logistics, retail, and construction companies. Organizations are under pressure to reduce capital expenditure, avoid long-term asset commitments, and maintain financial flexibility amid fluctuating demand cycles. Renting forklifts enables businesses to access modern equipment without the burden of upfront purchase costs, depreciation, and maintenance-related uncertainties. Many companies are shifting from owning large fleets to adopting rental models that align equipment availability with operational peaks and project-based activities.

- For instance, several warehouse operators have recently transitioned to monthly rental contracts to manage sudden demand surges associated with festive e-commerce seasons, allowing them to scale capacity without incurring major investments.

MARKET RESTRAINTS:

Variability in Equipment Quality across Providers May Limit the Market Growth

Variability in equipment quality among rental providers is a notable constraint for market expansion. Leading companies maintain standardized maintenance schedules and regularly upgrade fleets. In contrast, many small and mid-sized rental firms use older forklifts with inconsistent service histories. This disparity creates uncertainty for end users who depend on predictable performance. The problem is especially relevant in high-throughput settings such as distribution centers and manufacturing plants. Battery degradation, worn-out tires, hydraulic leaks, and outdated safety features can disrupt operations. These issues also increase the risk of workplace incidents. Inconsistency in equipment standards ultimately limits user trust and restrains market expansion.

MARKET OPPORTUNITIES:

Growth of Automated and Smart Warehousing to Create Lucrative Growth Opportunities

The rapid expansion of automated and smart warehousing presents a strong opportunity for the market. As companies adopt high-density storage systems, IoT-based inventory tracking, and data-driven warehouse management platforms, the requirement for advanced, highly maneuverable, and sensor-enabled forklifts is increasing.

Many organizations prefer renting these upgraded models rather than purchasing them, as automation-compatible forklifts involve higher costs, specialized features, and frequent technology upgrades. Smart warehouses often experience fluctuating equipment requirements due to dynamic order volumes, micro-fulfillment operations, and seasonal variations, making flexible rental contracts more suitable than long-term ownership. Additionally, the integration of telematics, safety sensors, and real-time performance monitoring in modern forklifts supports predictive maintenance and operational optimization, which rental providers can offer as value-added services. With companies increasingly moving toward digitalized logistics ecosystems, the rental market is well-positioned to supply technologically advanced machinery without burdening users with capital costs or upgrade responsibilities.

- For instance, in October 2025, Amazon introduced three new technologies that aim to make human employees more efficient while simultaneously reducing the need for human labor. These three AI tools include a sorting robot, an AI management agent, and augmented-reality glasses for drivers.

FORKLIFT RENTAL MARKET TRENDS:

Integration of Telematics and IoT for Fleet Monitoring is one of the Significant Market Trends

A major trend transforming the market is the widespread integration of telematics and IoT systems into rental fleets. Rental providers are increasingly equipping forklifts with sensors and connected technologies that track real-time usage, battery health, fuel consumption, operating hours, and maintenance requirements. This data-driven approach enables companies to optimize fleet performance, minimize downtime, and enhance safety compliance. For rental operators, telematics enhances predictive maintenance capabilities, enabling timely servicing and minimizing costly breakdowns. Customers also benefit from greater transparency, as digital dashboards provide insights into equipment productivity, operator behavior, and cost allocation across tasks or departments. The trend is further accelerating as industries adopt smart warehousing and automated material handling systems, where data synchronization and operational visibility are crucial. This development drives the market growth during the forecast period.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Shortage of Skilled Operators for Advanced Forklifts is a Challenging Factor for the Market

A key challenge for the forklift rentals industry is the shortage of skilled operators for advanced, technology-integrated forklifts. As warehouses and factories adopt electric, sensor-equipped, and semi-automated models, forklift operation becomes more complex/complicate. Many organizations/industries lack operator training and certification and operators are often unfamiliar with digital controls and telematics dashboards. This skill gap slows workflows, increases errors, and raises safety risks. Rental providers offer training programs, but the uptake varies by region due to costs and limited infrastructure. In areas with high labor turnover, companies hesitate to upskill short-term workers, widening the competency gap. As a result, operator shortages limit the use of modern rental fleets and restrict forklift rental market growth.

Segmentation Analysis

By Vehicle Type

Growing Adoption of Lithium-Ion Technologies Reinforces Class I Segment’s Dominance

Based on vehicle type, the market is classified into Class I, Class II, Class III, Class IV, and Class V.

The Class I segment holds the dominating share in the market, driven by the rising shift toward electric, low-emission material-handling solutions across warehouses, manufacturing units, and retail distribution centers. Class I forklifts offer superior energy efficiency, quiet operation, and enhanced maneuverability, making them ideal for indoor environments with strict safety and air-quality requirements. Their lower operating costs, reduced maintenance requirements, and compatibility with smart warehouse layouts further strengthen demand. The growing adoption of lithium-ion batteries, fast-charging capabilities, and telematics integration continues to accelerate rental preferences for Class I models, reinforcing their leadership within the rental ecosystem. These developments are likely to drive the fastest growth of the segment during the forecast period.

By Lift Capacity

High Utilization Rates and Operational Efficiency Drive the Dominance of Below 5 Tons Lift Capacity Forklifts

In terms of lift capacity, the market is categorized into below 5 tons, 6-10 tons, and above 11 tons.

The below 5 tons segment holds the largest forklift rental market share, supported by its use in warehouses, retail facilities, manufacturing plants, and small distribution centers. These forklifts offer optimal maneuverability, lower energy consumption, and cost-efficient operation, making them the preferred choice for daily material-handling. Their compact design suits narrow-aisle storage and high-turnover inventory. E-commerce fulfillment centers and last-mile logistics hubs further boost demand. Rental providers focus on this segment as it enables high utilization rates, quicker fleet turnover, and incurs lower maintenance costs, all of which contribute to the segment’s growth.

To know how our report can help streamline your business, Speak to Analyst

The 6-10 tons segment is poised to grow at a CAGR of 7.2%, showcasing the fastest growth over the analysis period.

By Propulsion Type

Electric Segment Leads with Growing Demand for Clean Material Handling Solutions

Based on propulsion type, the market is segmented into ICE and electric.

The electric propulsion segment holds the largest share of the market, driven by the rising demand for clean, energy-efficient, and low-maintenance material-handling solutions. The segment has also emerged as the fastest-growing segment in the market. Electric forklifts are favored across warehouses, logistics hubs, and manufacturing facilities due to their zero-emission operation, reduced noise levels, and suitability for indoor environments. Advances in lithium-ion battery technology, fast-charging systems, and longer operating cycles have further boosted their adoption in rental fleets. Companies are increasingly opting to rent electric models to align with their sustainability targets and avoid high upfront purchase costs. Rental providers also benefit from lower servicing needs, improving fleet uptime and overall profitability. This development drives the market growth during the forecast period.

- For instance, in July 2024, Hyster Company introduced its E80XNL forklift with integrated lithium-ion power. This 8,000-pound capacity cushion tire electric forklift joins four other Hyster models built around a lithium-ion battery pack, offering a more spacious operator compartment and lower center of gravity.

By Rental Period

Short-Term Forklift Rentals Lead the Market Owing to Project-Based and Seasonal Industry Requirements

Based on rental period, the market is segmented into short-term rentals, medium-term rentals, and long-term rentals.

The short-term rentals segment dominates the market, driven by industries seeking flexible, demand-responsive equipment solutions without long-term commitments. Seasonal peaks in e-commerce, project-based construction activities, and periodic warehouse expansions significantly increase demand for short-term forklift use. Companies prefer short-term contracts to handle sudden workload spikes, replace equipment that has broken down, or bridge temporary operational gaps. Key benefits include lower financial risk, faster approval cycles for urgent needs, and rapid scalability of fleets. Rental providers prioritize short-term offerings due to higher turnover rates and stronger profit margins, reinforcing the segment’s leading position across diverse industrial applications.

The long-term rentals segment is anticipated to expand at the fastest rate, depicting a CAGR of 6.9% over the forecast period.

By End-Use Industry

Rapid Growth of Fulfillment Centers and Omnichannel Retailing Boosts Warehousing & Logistics Rental Demand

Based on end-use industry, the market is segmented into warehousing & logistics, construction, automotive, food & beverage, and others.

The warehousing & logistics segment holds the largest share and is the fastest-growing segment in the market. The rapid expansion of e-commerce fulfillment, distribution centers, and last-mile delivery hubs drives growth in this segment. These facilities require continuous, high-throughput material handling. Rental forklifts are essential for managing fluctuating inventory volumes and seasonal demand. Electric and compact forklift models are widely adopted. They are especially suitable for indoor, high-density storage environments. Companies prefer rental solutions to avoid capital expenditure and maintain operational agility. Additionally, the surge in omnichannel retailing and automated warehouse infrastructure continues to strengthen rental demand within this leading segment.

- For instance, in 2025, Amazon launched several new warehouses and plans for expansion in India and the U.S. India saw the opening of new fulfillment centers in locations such as Delhi and Maharashtra and a total investment of USD 20 billion to expand its logistics network.

Forklift Rental Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific dominates the global market, driven by rapid industrial expansion, strong manufacturing output, and the accelerating development of large-scale warehousing and logistics infrastructure across China, India, Japan, and Southeast Asia. Moreover, the region’s booming e-commerce sector, driven by rising consumer demand and rapidly expanding fulfillment networks, has significantly increased the need for flexible material-handling solutions. As a result, companies prefer rental forklifts to manage peak season fluctuations, new facility ramp-ups, and project-specific requirements without incurring heavy capital expenditure. Additionally, the presence of global OEMs, competitive rental pricing, and the expansion of fleets offered by regional providers contribute to the market’s strong momentum.

North America

North America exhibits steady growth in the market, driven by mature warehousing ecosystems, high automation adoption, and an increasing reliance on flexible rental solutions within retail distribution and third-party logistics operations. Companies in the U.S. and Canada are increasingly opting for short-term rentals to offset labor shortages, upgrade their fleets to electric models, and maintain operational continuity during peak delivery cycles.

Europe

Europe remains a strong market, driven by stringent emission regulations, the rapid electrification of material-handling fleets, and the continuous modernization of industrial facilities across Germany, France, the U.K., and the Nordics. The region’s emphasis on sustainability, safety compliance, and telematics-enabled fleet optimization supports the shift toward rented electric forklifts.

Rest of the World

The rest of the world region includes the Middle East, Latin America, and Africa. The regional growth is attributed to the continued expansion of infrastructure development and rapid industrialization, which are driving rental opportunities across these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Rental Providers to Strengthen Market Positions through Portfolio Expansion

The forklift rental market is dominated by established Tier-1 rental companies and global OEM-affiliated service providers, such as Toyota Material Handling, KION Group (comprising Linde & STILL), Jungheinrich AG, Mitsubishi Logisnext, Crown Equipment, and Hyster Yale Group. These leaders are expanding their rental portfolios through the use of advanced electric forklifts, lithium-ion fleets, telematics-enabled units, and flexible on-demand rental models. Strategic collaborations with OEMs, battery manufacturers, and digital fleet management firms are enabling the development of connected rental ecosystems that integrate real-time equipment monitoring, automated fault detection, and maintenance scheduling. Their offerings span a wide range of Class I to V forklifts, telematics hardware, fleet optimization platforms, and value-added service contracts.

Key forklift rental players are increasingly adopting IoT analytics, cloud-based fleet dashboards, and AI-enabled utilization tracking to enhance operational efficiency and strengthen customer retention. Partnerships with technology providers such as AWS, Microsoft Azure, and Google Cloud support scalable fleet data management and predictive service solutions. Companies are also pursuing acquisitions, regional warehouse expansions, electrification of rental fleets, and investments in operator training programs to remain competitive amid rising demand for short-term rentals and eco-friendly equipment.

Competitive Benchmarking Table – Forklift Rental Market

|

Company |

Fleet Strength (Electric & IC) |

Geographical Presence |

Technology Adoption (IoT/Telematics) |

Service Model & Value-Added Offerings |

Competitive Positioning |

|

Toyota Material Handling |

Very strong, large electric portfolio, strong Class I–III |

Global - North America, Europe, Asia Pacific |

Advanced telematics (I_Site), strong analytics |

Training, fleet optimization, rapid service |

Market Leader with strong OEM-integrated rental capability |

|

KION Group (Linde & STILL) |

Strong mix of electric & IC trucks |

Strong presence in Europe, Asia Pacific |

Highly advanced (Linde Connected Solutions) |

Energy systems, safety tech, operator-assist |

Technology-Driven Leader in Europe |

|

Jungheinrich AG |

Very strong electric specialization |

Europe-focused with global expansion |

High telematics integration (Fleet Management 4.0) |

Lithium-ion systems, automation support |

Leader in Electric & Warehouse Solutions |

|

Crown Equipment Corporation |

Strong warehouse forklift range |

North America, Europe, Asia Pacific |

Crown INsite telematics |

On-site maintenance, customized rental |

Strong Competitor in Warehouse & Logistics Rentals |

|

Hyster–Yale Group |

Strong IC & heavy-duty electric |

Global - strong North America footprint |

Telematics via Hyster Tracker |

Robust service network, heavy-duty applications |

Strong Player in Construction & Heavy-Load Rentals |

|

Mitsubishi Logisnext |

Wide Electric & IC range |

Asia Pacific, Europe, North America |

Digital fleet tools (Logisnext FleetIQ) |

Flexible short-term rentals, automation-ready units |

Competitive Player with diversified offerings |

LIST OF KEY FORKLIFT RENTAL COMPANIES PROFILED:

- United Rentals, Inc. (U.S.)

- Sunbelt Rentals (U.S.)

- Herc Rentals (U.S.)

- Toyota Industries Corporation (Japan)

- KION Group AG (Germany)

- Jungheinrich AG (Germany)

- Crown Equipment Corporation (U.S.)

- Hyster‑Yale Group (U.S.)

- Mitsubishi Logisnext Co., Ltd. (Japan)

- Manitou Group (France)

KEY INDUSTRY DEVELOPMENTS:

- In July 2025, United Rentals expanded its digital platform by launching Smart Suggestions and augmented-reality equipment fit tools, illustrating increased investment in digital fleet services and rental-user support.

- In July 2025, Mitsubishi Logisnext Co., Ltd. announced an ambitious long-term sustainability roadmap aimed at increasing the electrification rate of its forklift portfolio from approximately 60% to 90% by 2035. The company emphasized that this transition aligns with tightening global emission regulations, the rapid shift toward carbon-neutral supply chains, and rising customer demand for low-emission material-handling solutions.

- In May 2025, Mitsubishi Logisnext Co., Ltd. opened a 73,500 sq ft electrification fabrication facility at its Houston campus to ramp up the production of electric forklifts and counterbalance trucks, aligning with the growing demand for electrified fleets.

- In May 2025, Crown Equipment Corporation unveiled a new dedicated sales and service facility in Chesapeake, Virginia, to bolster its regional support network and enhance uptime for rental and lease fleets in the eastern U.S. market.

- In March 2025, Hyster-Yale Materials Handling, Inc. unveiled a new lineup of high-capacity electric forklifts (J230-400XD series) with integrated lithium-ion batteries, expanding its offerings of heavy-duty electric forklifts.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Vehicle Type

By Lift Capacity

By Rental Period

By Propulsion

By End-Use Industry

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 12.50 billion in 2025 and is projected to reach USD 21.68 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 6.56 billion.

The market is expected to exhibit a CAGR of 6.3% during the forecast period of 2026-2034.

The Class I segment leads the market by vehicle type.

The growing demand for cost-efficient material handling solutions is a major factor driving the market.

Asia Pacific dominates the market with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us