Fresh Food Packaging Market Size, Share & Industry Analysis, By Material (Plastics, Paper & Paperboard, Metal, Glass, and Others), By Packaging Type (Boxes & Cartons, Trays & Clamshells, Jars & Containers, and Others), By Application (Fruits & Vegetables, Ready-to-Eat Meals, Meat, Poultry & Seafood, Dairy Products, Bakery & Confectionery, and Others), and Regional Forecast, 2026-2034

Fresh Food Packaging Market Size and Future Outlook

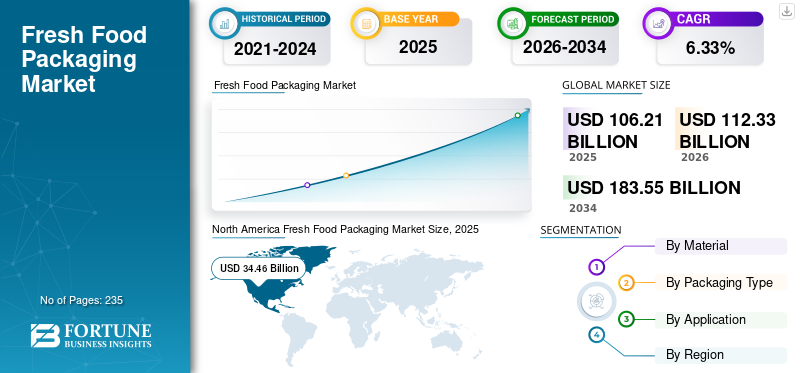

The global fresh food packaging market size was valued at USD 106.21 billion in 2025. The market is projected to grow from USD 112.33 billion in 2026 to USD 183.55 billion by 2034, exhibiting a CAGR of 6.33% during the forecast period. North America dominated the global market with a market share of 32.45% in 2025.

The global market is the sector dedicated to creating and providing packaging solutions that safeguard, preserve, and extend the shelf life of fresh food items, including fruits, vegetables, meat, seafood, and dairy, throughout storage, transportation, and retail distribution. The increasing consumption of fresh and minimally processed foods and a surging demand for extended shelf life, food safety, and convenient retail-ready packaging are driving the growth of the global market across both developed and emerging economies.

Furthermore, many key industry players, such as Amcor Plc, DS Smith, and Mondi, operating in the market, are focusing on developing innovative products and conducting R&D.

Download Free sample to learn more about this report.

Fresh Food Packaging Market KEY TAKEAWAYS

- 2025 Market Size: USD 106.21 billion

- 2026 Market Size: USD 112.33 billion

- 2034 Forecast Market Size: USD 183.55 billion

- CAGR: 6.33% from 2026–2034

- North America dominated the fresh food packaging market with a 32.45% share in 2025.

- The paper and paperboard segment is projected to grow at a CAGR of 6.40% during the forecast period.

- The trays & clamshells segment is projected to grow at a CAGR of 6.19% during the forecast period.

North America

North America held 32.45% share in 2025, valued at USD 34.46 billion.

Europe

Europe market valued at USD 16.64 billion in 2025.

Asia Pacific

Asia Pacific market valued at USD 28.70 billion in 2025.

U.S.

U.S. Market valued at USD 29.89 billion in 2025.

Japan

Japan Market valued at USD 5.52 billion in 2025.

Read More

FRESH FOOD PACKAGING MARKET TRENDS

Growing Adoption of Smart and Active Packaging is a Prominent Trend Observed in the Market

A significant trend influencing the global market is the growing use of smart and active packaging technology. These innovations surpass conventional containment methods by actively engaging with the packaged food or offering real-time insights into product condition. This trend is especially pronounced in premium fresh food sectors and developed markets, although its adoption is slowly spreading globally as costs decrease. With the rise of digitalization across the food supply chain, smart packaging is expected to evolve into a standard value-added feature rather than remain a niche innovation.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Fresh, Safe, and Convenient Food to Propel Market Growth

The global market for fresh food packaging is primarily influenced by evolving consumer lifestyles and surging demand for fresh, minimally processed, and conveniently packaged food items. The rapid pace of urbanization, rising workforce participation, and the increase in dual-income households have greatly increased the consumption of fresh fruits, vegetables, meat, seafood, and dairy products that require protective and hygienic packaging. Innovations in modified atmosphere packaging (MAP) and vacuum packaging further help preserve freshness and minimize food waste.

The heightened awareness of food safety, particularly in the wake of the COVID-19 pandemic, has driven the demand for tamper-evident, contamination-resistant packaging solutions. Together, these factors render packaging an essential aspect of the fresh food value chain, propelling fresh food packaging market growth.

MARKET RESTRAINTS

High Cost of Advanced Packaging Solutions May Hamper Market Growth

Despite robust demand, the fresh food packaging sector faces constraints due to the higher costs associated with advanced packaging materials and technologies. Options such as multilayer films, active packaging, biodegradable polymers, and smart packaging systems entail higher costs for raw materials, production, and research and development than traditional plastic packaging. For small- and medium-sized food producers, particularly in developing countries, these expenses can significantly erode profit margins and hinder adoption. Furthermore, the price fluctuations of raw materials such as plastics, paper pulp, and bio-based resins exacerbate cost unpredictability.

MARKET OPPORTUNITIES

Expansion of Sustainable and Eco-Friendly Packaging Provides Potential Growth Opportunities

Sustainability signifies a significant growth opportunity for the global fresh food packaging sector. Increasing consumer environmental awareness, along with more stringent government regulations on plastic use and waste management, is compelling food producers to embrace recyclable, compostable, and biodegradable packaging options.

Furthermore, advancements in lightweighting and material reduction enable manufacturers to decrease their environmental footprint while still ensuring product protection. Companies that proactively invest in scalable, cost-efficient, sustainable packaging technologies are strategically positioned to capitalize on the rising demand from environmentally aware consumers and retailers, establishing sustainability as a crucial catalyst for future market growth.

MARKET CHALLENGES

Maintaining Shelf Life While Reducing Material Use Poses a Critical Challenge to Market Growth

One of the primary challenges in packaging fresh food is balancing shelf-life performance with goals of material reduction and sustainability. Fresh foods are highly perishable and sensitive to factors such as temperature, moisture, oxygen, and microbial activity, requiring high-performance barrier properties. Nevertheless, minimizing plastic usage or transitioning to environmentally friendly materials can jeopardize durability, moisture resistance, and gas control if not properly engineered. Moreover, varying storage conditions and lengthy transportation routes further complicate packaging requirements. Additionally, adherence to regulatory compliance and food safety standards, as well as the need for consistent quality, introduces further layers of complexity.

Segmentation Analysis

By Material

Versatility, Cost Efficiency, and Performance to Drive the Dominance of Plastic Packaging Materials

Based on material, the market is divided into plastics, paper & paperboard, metal, glass, and others.

The plastics segment is expected to account for the largest share of the fresh food packaging market. The segment leads the global market owing to its unparalleled versatility, cost efficiency, and functional effectiveness across various fresh food applications. Plastic materials provide outstanding barrier properties against moisture, oxygen, and contaminants, which are essential for maintaining the freshness, texture, and visual attractiveness of perishable foods. Despite growing concerns about sustainability, continuous advancements in recyclable and mono-material plastics further solidify plastics' dominance in the fresh food packaging sector.

The paper and paperboard segment is expected to grow at a CAGR of 6.40% over the forecast period.

By Packaging Type

Structural Strength and Consumer Convenience Make Boxes & Cartons the Leading Packaging Type

Based on packaging type, the market is segmented into boxes & cartons, trays & clamshells, jars & containers, and others.

In 2025, the boxes & cartons segment dominated the global fresh food packaging market share. The segment leads owing to its ability to combine protection, convenience, and marketing appeal. Cartons, generally made from paperboard or cardboard, offer outstanding structural strength, facilitating the secure transportation and storage of fresh food items such as dairy, baked goods, fruits, and ready-to-eat meals.

Their sturdy design safeguards contents against physical harm, contamination, and external environmental impacts while preserving product freshness. Boxes and cartons offer great versatility, accommodating printing, branding, and labeling, thereby improving shelf visibility and consumer appeal.

The trays & clamshells segment is projected to grow at a CAGR of 6.19% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

High Consumption and Perishability to Drive the Dominance of Fruits & Vegetables Segment

Based on application, the market is segmented into fruits & vegetables, ready-to-eat meals, meat, poultry & seafood, dairy products, bakery & confectionery, and others.

The fruits & vegetables segment is expected to hold a dominant market share over the forecast period. The segment leads the global market, primarily due to the significant perishability of these items and the rising worldwide demand for fresh produce. The growing consumer inclination toward fresh, ready-to-eat, and pre-cut produce has further propelled the implementation of innovative packaging solutions, including clamshells, trays, pouches, and modified atmosphere packaging (MAP).

Moreover, the expansion of modern retail channels, supermarkets, and e-commerce platforms has increased the need for robust, transport-friendly packaging that ensures products arrive at consumers in the best possible condition.

The ready-to-eat meals segment is projected to grow at a CAGR of 6.72% over the forecast period.

Fresh Food Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Fresh Food Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 32.51 billion, and maintained its leading position in 2025, with a value of USD 34.46 billion. The demand for fresh food packaging in North America is propelled by the significant consumption of fresh produce, meat, and ready-to-eat meals, underpinned by a well-established cold chain and organized retail framework. Robust food safety regulations, a focus on extending shelf life, and an increasing preference for sustainable and recyclable packaging materials further enhance market expansion.

Additionally, the rise of e-commerce in grocery shopping and the adoption of technologies such as modified atmosphere and smart packaging are crucial factors driving this growth.

U.S. Fresh Food Packaging Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 29.89 billion in 2025, accounting for roughly 28.14% of global sales.

Asia Pacific

Asia Pacific reached USD 28.70 billion in 2025 and secure the position of the second-largest region in the market. In the region, India and China touched USD 7.57 billion and USD 9.21 billion, respectively, in 2025. In the Asia Pacific region, the market expansion is driven by rapid urbanization, rising disposable incomes, and heightened consumption of fresh produce, including fruits, vegetables, meat, and seafood. The growth of modern retail formats and enhancements in cold chain logistics are further boosting the demand for protective packaging. Additionally, population growth and evolving dietary preferences, coupled with cost-effective flexible packaging solutions, are significant elements influencing regional demand.

Japan Fresh Food Packaging Market

In 2025, the Japanese market reached a value of around USD 5.52 billion, accounting for roughly 5.19% of global revenues. The regional market in Japan is driven by a strong emphasis on food quality, hygiene, and extended shelf life, particularly for seafood and ready-to-eat meals. The aging population and rising demand for portion-controlled packaging are driving the greater adoption of high-precision packaging solutions.

China Fresh Food Packaging Market

The China market is projected to be one of the largest worldwide, with 2025 revenues touching around USD 9.21 billion, representing roughly 8.67% of global sales.

India Fresh Food Packaging Market

In 2025, the India market touched a value of around USD 7.57 billion, accounting for roughly 7.13% of the global revenue.

Europe

Europe is projected to grow at a CAGR of 6.05% over the forecast period, the third-highest among regions, and reached a valuation of USD 16.64 billion in 2025. The regional market is primarily influenced by stringent environmental regulations and sustainability initiatives aimed at reducing plastic waste. A heightened consumer awareness of eco-friendly packaging, along with a growing demand for fresh, locally sourced food, fosters the adoption of paper-based and recyclable alternatives.

Innovative packaging technologies that enhance shelf life and reduce food waste are widely used to align with the EU's circular economy objectives.

U.K. Fresh Food Packaging Market

In 2025, the U.K. market reached USD 3.01 billion, representing approximately 2.83% of global revenues. A significant demand for convenience, transparency, and food safety is driving the U.S. market for fresh food packaging. Strong regulatory standards, sophisticated cold chain systems, and the increasing use of sustainable packaging materials also contribute to market growth.

Germany Fresh Food Packaging Market

The Germany market reached USD 3.53 billion in 2025, equivalent to around 3.32% of the global fresh food packaging sales.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa markets are expected to witness moderate growth during the forecast period. The Latin America market reached a valuation of USD 14.35 billion in 2025. Rising exports of fresh produce and improvements in food distribution infrastructure drive the market for fresh food packaging in Latin America. The growing urban population and the proliferation of supermarket chains drive the demand for standardized, sanitary packaging.

In the Middle East & Africa, South Africa reached USD 3.44 billion in 2025. In the region, the demand is influenced by rising food imports, sustainable packaging solutions, severe climatic conditions, and the need to maintain freshness during extended transportation and storage. The expansion of organized retail, urbanization, and food security initiatives further heightens the dependence on protective packaging solutions.

Saudi Arabia Fresh Food Packaging Market

The Saudi Arabian market reached approximately USD 3.88 billion in 2025, accounting for roughly 3.66% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players’ Focus on Expanding Product Launch and Acquisitions to Propel Market Progress

The global market has a semi-consolidated structure, with prominent players including Amcor Plc, DS Smith, and Mondi. The significant market share of these packaging companies is due to numerous strategic initiatives, including collaborations among operating entities to advance research.

- For instance, in February 2024, Amcor partnered with Stonyfield Organic, the nation's foremost organic yogurt producer, and Cheer Pack North America, a prominent manufacturer of spouted pouch packaging, to introduce the inaugural all-polyethylene (PE) spouted pouch. This collaboration unites three sustainability pioneers to create a groundbreaking solution that offers an eco-friendlier packaging option without sacrificing performance.

Other notable players in the global market include Coveris, Sealed Air, and International Paper. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY FRESH FOOD PACKAGING COMPANIES PROFILED

- Amcor Plc (Switzerland)

- DS Smith (U.K.)

- Mondi (U.K.)

- Coveris (Austria)

- Sealed Air (U.S.)

- International Paper (U.S.)

- Huhtamaki (Finland)

- Transcontinental Inc. (Switzerland)

- Sonoco Products Company (U.S.)

- ProAmpac (U.S.)

- Genpak, LLC (U.S.)

- Winpak Ltd. (Canada)

- Flair Flexible Packaging Corporation (Canada)

- PPC Flexible Packaging LLC (U.S.)

- Amerplast (Finland)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Coveris integrated freshness and sustainability by introducing a new monomaterial packaging solution for refrigerated products. In alignment with its continuous No Waste initiative, Coveris launched a resealable monomaterial tray specifically designed for refrigerated food uses. This groundbreaking MonoFlexBP tray serves as a replacement for non-recyclable, mixed-material packaging, all while providing enhanced shelf life and convenience for consumers.

- July 2025: Huhtamaki, a global frontrunner in sustainable food packaging solutions, announced the launch of its latest ice cream cups that combine product innovation with strong consumer appeal. These cups are designed to be both home- and industrial-compostable and recyclable, providing a novel, sustainable packaging option for the ice cream sector.

- April 2025: DS Smith collaborated with Priméale, a branch of Agrial, to create an eco-friendly alternative to plastic trays. The collaboration is centered on developing a recyclable fiber-based punnet for the Priméale Vegetable Kit collection. This effort seeks to substitute plastic packaging with a more sustainable choice in the fresh produce sector.

- April 2025: Amcor partnered with Riverside Natural Foods, a prominent certified organic snack manufacturer, to introduce MadeGood Trail Mix bars in AmFiber paper-based packaging. This exclusive launch, coinciding with Earth Month, represents a pioneering solution in the category that offers curbside recyclability within the paper stream while maintaining package performance without compromise.

- January 2024: In its ongoing efforts to create packaging materials aligned with its clients' sustainability objectives, the global packaging solutions provider SEE introduced the first bio-based, industrially compostable tray for protein packaging, which has been effectively tested to meet the requirements of current food processing machinery. SEE's innovative CRYOVAC brand compostable overwrap tray is constructed from a bio-based, food-contact-grade resin that has received USDA certification for containing 54% bio-based content, chemically sourced from renewable wood cellulose.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.33% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Packaging Type, Application, and Region |

|

By Material |

· Plastics · Paper & Paperboard · Metal · Glass · Others |

|

By Packaging Type |

· Boxes & Cartons · Trays & Clamshells · Jars & Containers · Others |

|

By Application |

· Fruits & Vegetables · Ready-to-Eat Meals · Meat, Poultry & Seafood · Dairy Products · Bakery & Confectionery · Others |

|

By Region |

· North America (By Material, Packaging Type, Application, and Country) o U.S. o Canada · Europe (By Material, Packaging Type, Application, and Country/Sub-region) o Germany o U.K. o France o Italy o Spain o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Packaging Type, Application, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Packaging Type, Application, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Packaging Type, Application, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 106.21 billion in 2025 and is projected to reach USD 183.55 billion by 2034.

In 2025, the North America market value stood at USD 34.46 billion.

The market is expected to grow at a CAGR of 6.33% over the forecast period of 2026-2034.

By material, the plastics segment is expected to lead the market.

The rising demand for fresh, safe, and convenient food is a key factor propelling market growth.

Amcor Plc, DS Smith, and Mondi are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 235

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us