Gas Utility Management Market Size, Share & Industry Analysis, By Component (Software and Services {System Integration & Deployment, Managed Services, Consulting Services, and Others}, By Deployment Mode (Cloud-Based, Hybrid, and On-Premise), By Pipeline Type (Gathering Pipelines, Transmission Pipelines, Distribution Pipelines, and Service Pipelines), and Regional Forecast, 2026-2034

Gas Utility Management Market Size and Future Outlook

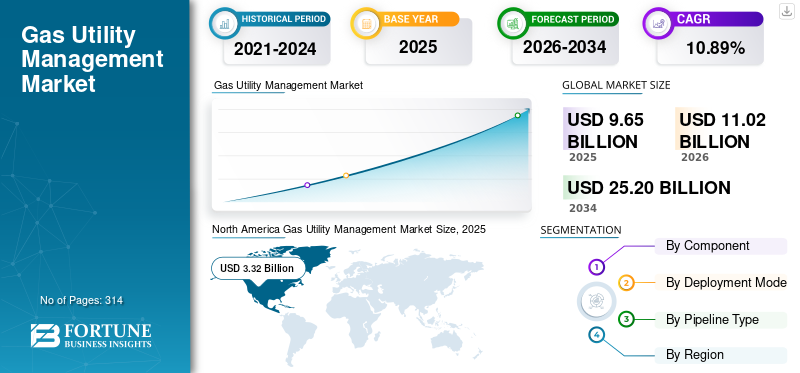

The global gas utility management market size was valued at USD 9.65 billion in 2025. The market is projected to grow from USD 11.02 billion in 2026 to USD 25.20 billion by 2034, exhibiting a CAGR of 10.89% during the forecast period.

Gas utility management refers to the software, platforms, and services used by gas utilities to monitor, operate, maintain, and optimize natural gas transmission and distribution networks. These solutions support critical functions such as asset management, GIS mapping, pipeline integrity management, SCADA monitoring, workforce management, customer billing, and regulatory compliance. The market is driven by increasing investments in pipeline modernization, methane emission monitoring, smart utility technologies, and digital transformation initiatives. Growing emphasis on operational efficiency, infrastructure safety, cybersecurity, and predictive maintenance is further accelerating adoption of advanced gas utility management solutions across global utility networks.

Oracle Corporation, SAP SE, Siemens AG, Hexagon AB, and Schneider Electric SE are among the key market players driving the growth of the market. Their continuous focus on innovation, infrastructure modernization, and integration of smart utility technologies is accelerating the adoption of advanced gas utility management solutions across transmission and distribution networks globally.

Download Free sample to learn more about this report.

Gas Utility Management Market Trends

Increasing Adoption of AI and Predictive Analytics in Gas Utility Operations are Amplifying Market Growth

One of the most significant trends shaping the market is the growing adoption of artificial intelligence (AI), machine learning, and predictive analytics for network monitoring and asset optimization. Gas utilities are increasingly leveraging AI-driven platforms to predict equipment failures, identify potential pipeline leaks, optimize maintenance schedules, and improve workforce productivity. According to the International Energy Agency (IEA), methane emissions from energy operations exceeded 120 million tons globally in 2024, creating greater pressure on utilities to deploy advanced monitoring technologies for leak detection and emissions management. Companies such as Siemens, Schneider Electric, and Hexagon have expanded AI-enabled asset performance management and digital twin solutions to help utilities improve operational visibility and reduce downtime. Predictive maintenance systems can reduce maintenance costs by 10–20% while improving asset reliability, making them increasingly attractive to utility operators. As utilities continue their digital transformation efforts and seek to improve infrastructure resilience, AI and advanced analytics are expected to become integral components of gas utility management strategies globally.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Investments in Pipeline Modernization and Safety Compliance to Push Market Growth

A major driver for the gas utility management market growth is the increasing investment in pipeline modernization and infrastructure safety. Many gas transmission and distribution networks in North America and Europe were built decades ago and require continuous upgrades to meet modern safety standards. According to the American Gas Association (AGA), U.S. natural gas utilities invest more than USD 30 billion annually in infrastructure modernization, safety improvements, and system upgrades. Regulatory agencies are imposing stricter requirements related to pipeline integrity management, leak detection, and methane emission reduction, prompting utilities to invest in GIS, SCADA, asset management, and monitoring solutions. For example, PHMSA in the U.S. has strengthened pipeline safety regulations following several high-profile incidents, increasing the need for real-time monitoring and risk assessment technologies. These investments are accelerating the adoption of advanced utility management systems that enable operators to monitor network conditions, optimize maintenance activities, and ensure regulatory compliance while enhancing overall operational reliability.

Market Restraints

High Implementation and Integration Costs to Limit Market Growth

Despite strong growth prospects, the market faces a significant restraint in the form of high implementation and integration costs associated with utility management systems. Large-scale deployments often require integration with existing SCADA systems, GIS platforms, customer information systems, enterprise resource planning software, and legacy operational technology infrastructure. For many municipal and small-scale gas utilities, these projects can involve substantial upfront capital expenditure and long implementation timelines. In addition to software licensing costs, utilities must invest in employee training, data migration, cybersecurity enhancements, and system customization. According to several utility digital transformation programs, implementation projects can take multiple years before delivering measurable returns. Smaller operators, particularly in emerging markets, often lack the financial resources and technical expertise required to deploy sophisticated management platforms. As a result, many continue operating with legacy systems, slowing the overall pace of digital transformation and limiting broader market adoption in cost-sensitive regions.

Market Opportunities

Expansion of Smart Gas Networks and Cloud-Based Utility Platforms to Create New Growth Avenues

The rapid development of smart gas networks presents a significant growth opportunity for the market. Governments and utilities globally are increasingly investing in smart infrastructure to improve operational efficiency, reduce losses, and enhance customer service. For instance, India continues expanding its City Gas Distribution (CGD) network across hundreds of geographical areas, creating substantial demand for digital asset management, GIS, and monitoring platforms. At the same time, cloud-based utility solutions are gaining traction due to their scalability, lower infrastructure requirements, and ability to support advanced analytics. Cloud deployments enable utilities to access real-time operational data, automate reporting, and integrate artificial intelligence capabilities without significant hardware investments. Major technology providers such as Oracle, SAP, and Schneider Electric are expanding cloud-native offerings specifically designed for utility operations. As utilities seek more flexible and cost-effective solutions, the transition toward cloud-enabled smart gas networks is expected to generate substantial opportunities for software providers and service vendors over the coming decade.

Market Challenges

Growing Cybersecurity Risks Across Connected Utility Networks to Challenge Market Growth

One of the most critical challenges facing the market is the increasing threat of cybersecurity attacks targeting utility infrastructure. As gas utilities deploy connected sensors, cloud platforms, smart meters, and remote monitoring systems, the number of potential attack points across operational networks continues to rise. According to the International Energy Agency (IEA), cyberattacks on energy infrastructure have increased significantly over the past decade as critical infrastructure becomes more digitalized. A successful cyberattack on a gas utility can disrupt pipeline operations, compromise sensitive customer data, and create substantial safety risks. Several utilities globally have increased cybersecurity spending in response to ransomware attacks and threats targeting industrial control systems. However, many utilities and industrial users still operate aging infrastructure that was not originally designed with modern cybersecurity requirements. Balancing digital transformation with robust cybersecurity protection remains a major challenge, requiring continuous investments in security monitoring, threat detection, employee training, and regulatory compliance measures.

Segmentation Analysis

By Component

Growing Emphasis on Digital Transformation and Operational Efficiency of Utility Sector Led to Software Segment Dominance

Based on component, the segment covers software and services.

The software segment accounted for dominant gas utility management market share in 2025. The software segment forms the foundation of gas utility management by enabling utilities to efficiently monitor, control, and optimize their transmission and distribution networks. These solutions include asset management, GIS, SCADA, customer information systems, pipeline integrity management, workforce management, and advanced analytics platforms. Growing emphasis on digital transformation, operational efficiency, regulatory compliance, and infrastructure safety is driving the adoption of intelligent software solutions across gas utilities. The integration of technologies such as artificial intelligence, cloud computing, digital twins, and predictive maintenance is further enhancing the capabilities of utility management software, enabling operators to make data-driven decisions, improve asset reliability, and reduce operational risks.

Services is the second-leading segment growing at a CAGR of 10.30% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment Mode

Critical Nature of Utility Operations and Need for Direct Control Over Infrastructure Led to On-Premise Segment Growth

Based on deployment mode, the market is segmented into cloud-based, hybrid, and on-premise.

The on-premise segment accounted for approximately 48.96% of the market share in 2025. On-premise deployment remains widely utilized across the gas utility sector due to the critical nature of utility operations and the need for direct control over infrastructure and sensitive operational data. Many utilities continue to operate legacy systems that are deeply integrated with pipeline monitoring, network control, and asset management functions. On-premise solutions offer greater customization, data sovereignty, and control over cybersecurity measures, making them suitable for highly regulated environments. Although utilities are gradually adopting cloud technologies, many continue to rely on on-premise deployments for core operational processes where reliability, security, and uninterrupted system performance are paramount.

Cloud-based segment is expected to grow at a CAGR of 11.52% during the forecast period.

By Pipeline Type

Urbanization and Expansion of City Gas Distribution Infrastructure Propelled Distribution Pipelines Segment Growth

Based on pipeline type, the market is segmented into gathering pipelines, transmission pipelines, distribution pipelines, and service pipelines.

The distribution pipelines segment represented the largest market share of 55.55% in 2025. Distribution pipelines represent the largest application area for gas utility management solutions, as they deliver natural gas directly to residential, commercial, and industrial consumers. Utilities utilize GIS, customer information systems, asset management software, leak detection solutions, and workforce management platforms to efficiently operate extensive distribution networks. Urbanization, expansion of city gas distribution infrastructure, and increasing consumer connections are driving significant investments in digital utility management technologies. Utilities are increasingly adopting smart monitoring systems and predictive analytics to improve service reliability, enhance safety, reduce operational costs, and comply with evolving regulatory requirements.

The gathering pipelines is the fastest growing segment with a CAGR of 12.59% during the forecast period.

Gas Utility Management Market Regional Outlook

By region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Gas Utility Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is the dominant region in the market and was valued at USD 3.32 billion in 2025, accounting for approximately 34.43% of global revenues. The growth is driven by its extensive natural gas infrastructure and advanced utility digitalization initiatives. According to the American Gas Association (AGA), more than 79 million U.S. consumers receive natural gas service through over 2.8 million miles of pipeline infrastructure, creating significant demand for asset management, GIS, SCADA, and pipeline integrity solutions. Utilities are increasingly investing in AI-driven predictive maintenance and methane monitoring technologies to comply with stringent PHMSA safety regulations. In Canada, major LNG export projects and pipeline modernization programs are further supporting the adoption of advanced utility management platforms across transmission and distribution networks.

U.S. Gas Utility Management Market

The U.S. market was valued at USD 2.87 billion in 2025 and is estimated to reach USD 3.24 billion in 2026. The U.S. remains the largest market supported by a vast natural gas ecosystem and ongoing infrastructure investments. According to the U.S. Energy Information Administration (EIA), natural gas accounted for approximately 43% of U.S. electricity generation in 2024, highlighting the importance of reliable gas delivery networks. Utilities are increasingly deploying advanced GIS, pipeline integrity management, and real-time monitoring solutions to improve system reliability, reduce operational risks, and support growing energy demand.

Europe

Europe accounted for USD 2.79 billion in 2025, representing approximately 28.89% of global revenues. Europe is a technologically advanced market supported by infrastructure modernization, methane emission reduction programs, and hydrogen integration initiatives. According to ENTSOG, Europe operates more than 200,000 km of high-pressure gas transmission pipelines, requiring sophisticated monitoring and asset management systems. Germany, the U.K., Italy, and France are investing heavily in hydrogen-ready gas networks and digital utility platforms. For example, Italy’s Snam and Germany’s Open Grid Europe are actively developing hydrogen-compatible infrastructure, increasing the need for advanced network management, digital twins, and integrity monitoring solutions. Regulatory focus on decarbonization and operational efficiency continues to accelerate digital transformation across European gas utilities.

Germany Gas Utility Management Market

Germany’s market was valued at USD 0.62 billion in 2025 and is estimated to reach USD 0.72 billion in 2026. Germany represents a key European market due to its extensive gas distribution infrastructure and strong industrial demand. According to BDEW (German Association of Energy and Water Industries), natural gas supplies approximately 50% of Germany's residential heating demand. Utilities are investing in digital monitoring, network optimization, and integrity management systems to enhance operational performance. The country's hydrogen core network initiative is further increasing demand for advanced utility management technologies capable of supporting future gas-hydrogen networks.

U.K. Gas Utility Management Market

The U.K. market was valued at USD 0.50 billion in 2025 and is estimated to reach USD 0.57 billion in 2026. The U.K. market is driven by modernization of gas networks and increasing investments in net-zero transition initiatives and clean energy. According to Ofgem, Britain's gas distribution networks deliver gas to approximately 23 million homes and businesses. Utilities are investing in digital asset management, leak detection technologies, and predictive maintenance platforms to improve operational efficiency and support future hydrogen blending projects. The country's focus on decarbonizing gas infrastructure continues to accelerate digital transformation efforts.

Asia Pacific

Asia Pacific’s market was valued at USD 2.65 billion in 2025, accounting for approximately 27.43% of the global market. Asia Pacific is the fastest-growing market due to rapid urbanization, expanding gas distribution infrastructure, and increasing natural gas consumption. China operates one of the world’s largest gas pipeline networks, exceeding 120,000 km of long-distance pipelines, while India continues expanding its City Gas Distribution (CGD) network across hundreds of geographical areas under government-led initiatives. These developments are driving investments in GIS, customer information systems, remote monitoring, and pipeline management solutions. In addition, growing LNG infrastructure investments across China, India, Japan, and Southeast Asia are creating strong demand for digital utility platforms that enhance operational efficiency and network reliability.

China Gas Utility Management Market

China remains the dominant contributor in Asia Pacific, valued at USD 1.11 billion in 2025, and is estimated to reach USD 1.28 billion in 2026. The dominance is supported by rapid gas infrastructure expansion and urban gas adoption. According to the National Bureau of Statistics of China, the country's natural gas consumption exceeded 420 billion cubic meters (bcm) in 2024. Large-scale investments in city gas distribution systems and long-distance transmission pipelines are driving demand for SCADA, GIS, customer information systems, and predictive maintenance platforms. Smart city developments are further accelerating utility digitalization across urban centers.

India Gas Utility Management Market

India’s market was valued at USD 0.39 billion in 2025 and is estimated to reach USD 0.45 billion in 2026. India is emerging as a high-growth market due to expanding gas access and pipeline development. According to the Petroleum and Natural Gas Regulatory Board (PNGRB), the country's authorized City Gas Distribution network now covers over 70% of India's population and nearly 90% of its geographical area. This rapid network expansion is creating substantial demand for digital asset management, billing systems, GIS mapping, and remote monitoring solutions to efficiently manage growing infrastructure assets.

Japan Gas Utility Management Market

Japan’s market was valued at USD 0.42 billion in 2025 and is estimated to reach USD 0.48 billion in 2026. Japan is a technologically mature market with strong emphasis on operational reliability and safety. According to the Ministry of Economy, Trade and Industry (METI), Japan has installed more than 20 million smart gas meters, making it one of the world's most advanced gas metering markets. Utilities are leveraging advanced analytics, IoT-enabled monitoring, and cybersecurity solutions to enhance network performance, improve customer service, and strengthen resilience against natural disasters.

Latin America

Latin America accounted for USD 0.50 billion in 2025, accounting for approximately 5.22% of global revenues. Latin America is witnessing gradual growth in gas utility management adoption, supported by pipeline expansion projects and modernization of utility operations. Brazil has been expanding its natural gas market through initiatives such as the New Gas Market Program, which aims to increase competition and infrastructure development. Mexico continues to strengthen its gas transportation network through cross-border pipeline connections with the U.S., supporting greater demand for monitoring and asset management systems. Utilities throughout the region are increasingly implementing digital billing, GIS, and network monitoring solutions to improve operational performance, reduce losses, and enhance customer service capabilities.

Middle East & Africa

The Middle East & Africa was valued at USD 0.39 billion in 2025. The region is benefiting from significant investments in natural gas infrastructure, LNG projects, and smart utility development. Qatar, Saudi Arabia, and the UAE are expanding gas production and transmission capacities to support industrial growth and energy diversification. For example, Saudi Aramco Digital is developing industrial communication networks to support IoT-enabled monitoring and operational intelligence across critical infrastructure assets. In Africa, countries such as Egypt and Nigeria are investing in pipeline expansion and gas distribution projects to increase domestic gas utilization. These developments are driving demand for advanced asset management, SCADA, cybersecurity, and pipeline monitoring solutions to improve operational efficiency and network reliability.

GCC Gas Utility Management Market

The GCC market which was valued at USD 0.22 billion in 2025 and is estimated to reach USD 0.26 billion in 2026. The GCC market is expanding rapidly due to rising natural gas utilization and infrastructure investments. According to the Gas Exporting Countries Forum (GECF), the Middle East accounts for approximately 38% of global proven natural gas reserves, with GCC countries continuing to expand domestic gas transmission and processing capacity. Major national energy companies are deploying advanced asset management, SCADA, and digital monitoring systems to improve operational efficiency, support industrial growth, and optimize large-scale gas infrastructure networks.

COMPETITIVE LANDSCAPE

Key Industry Players

Extensive Technology Portfolios and Long-Standing Relationships with Utility Operators by Key Players are Booming Market Share for Companies

The gas utility management market is led by companies such as Oracle Corporation, SAP SE, Siemens AG, Schneider Electric SE, and Hexagon AB, which have established strong positions through their extensive technology portfolios and long-standing relationships with utility operators globally. These companies provide integrated solutions covering asset management, network monitoring, GIS, analytics, automation, customer management, and operational optimization, enabling utilities to improve efficiency, reliability, and regulatory compliance. Their continued investments in cloud computing, artificial intelligence, digital twins, IoT, cybersecurity, and predictive maintenance technologies are accelerating the digital transformation of gas utilities. Additionally, their global presence, strong research and development capabilities, and ability to support large-scale utility modernization projects have made them preferred partners for gas transmission and distribution operators, contributing significantly to the overall growth and advancement of the market.

List of Key Gas Utility Management Companies Profiled in Report

- Oracle Corporation (U.S.)

- SAP SE (Germany)

- IBM Corporation (U.S.)

- Hexagon AB (Sweden)

- Esri Inc. (U.S.)

- Schneider Electric SE (France)

- Siemens AG (Germany)

- AVEVA Group plc (U.K.)

- Hitachi Energy Ltd. (Switzerland)

- Bentley Systems, Inc. (U.S.)

- GE Vernova (U.S.)

- Trimble Inc. (U.S.)

- Hansen Technologies Ltd. (Australia)

- IFS AB (Sweden)

- Wipro Limited (India)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Schneider Electric announced a strategic collaboration with NVIDIA to develop AI-ready infrastructure and industrial digitalization solutions. The partnership focuses on integrating advanced AI capabilities into energy management, automation, and industrial operations platforms. This initiative is expected to enhance real-time analytics, predictive maintenance, and operational efficiency for utilities and critical infrastructure operators, including gas network operators.

- March 2025: Siemens completed the acquisition of Altair Engineering for USD 10 billion, significantly expanding its industrial software, simulation, and digital twin capabilities. The acquisition strengthens Siemens' position in infrastructure digitalization and asset lifecycle management. The enhanced portfolio will enable utilities to optimize network planning, improve operational reliability, and accelerate digital transformation across energy and utility assets.

- December 2024: Hitachi Energy announced an investment of more than USD 250 million to expand its global manufacturing footprint and digital grid technologies. The investment supports growing demand for energy infrastructure modernization, grid resilience, and digital asset management solutions. The expansion will also strengthen the company's ability to deliver advanced monitoring, automation, and operational intelligence solutions to utility operators globally.

- September 2024: Oracle enhanced its Oracle Utilities Network Management System with advanced AI-powered outage prediction and operational analytics capabilities. The upgrade enables utility operators to improve asset visibility, reduce downtime, and accelerate incident response. By leveraging machine learning and cloud-based analytics, Oracle aims to help utilities make more informed operational decisions while improving network reliability and customer service performance.

- June 2024: AVEVA introduced new industrial intelligence and AI-driven operational capabilities within its CONNECT platform. The enhancements enable utility operators to unify operational and engineering data, improve predictive maintenance, and optimize asset performance. The platform supports real-time decision-making and helps infrastructure operators increase efficiency, reduce operational risks, and accelerate their digital transformation initiatives.

REPORT COVERAGE

The gas utility management market report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.89% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Deployment Mode

|

|

|

By Pipeline Type

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 9.65 billion in 2025 and is projected to reach USD 25.20 billion by 2034.

In 2025, the North Americas market value stood at USD 3.32 billion.

The market is expected to exhibit a CAGR of 10.89% during the forecast period.

By component, the software segment led the market.

Rising investments in pipeline modernization and safety compliance are driving market expansion.

Oracle Corporation, SAP SE, Siemens AG, Hexagon AB, and Schneider Electric SE are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 314

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us