Renewable Energy Integration Market Size, Share & Industry Analysis, By Component (Hardware, Services, and Software), By Grid Level (Microgrid-Level Integration, Behind-the-Meter (BTM) Integration, Distribution-Level Integration, and Transmission-Level Integration), By Application (Commercial & Industrial, Utilities, and Others), and Regional Forecast, 2026-2034

Renewable Energy Integration Market Size and Future Outlook

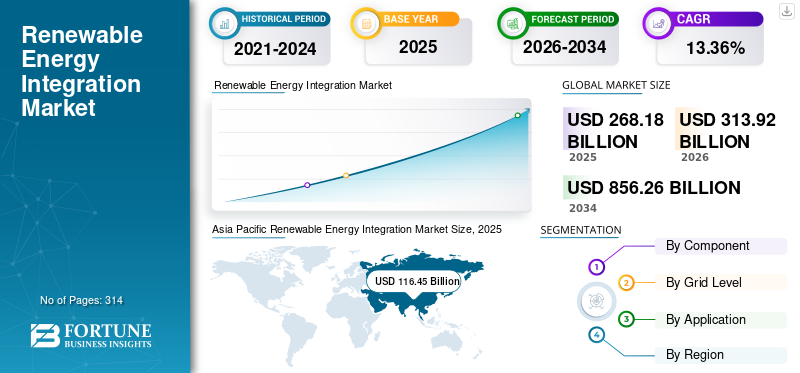

The global renewable energy integration market size was valued at USD 268.18 billion in 2025. The market is projected to grow from USD 313.92 billion in 2026 to USD 856.26 billion by 2034, exhibiting a CAGR of 13.36% during the forecast period. Asia Pacific dominated the renewable energy integration market with a market share of 43.42% in 2025.

Renewable energy integration refers to the process of incorporating renewable energy sources such as solar, wind, hydro, and biomass into existing electricity grids while maintaining grid stability, reliability, and energy efficiency. It involves the deployment of transmission infrastructure, energy storage systems, smart grids, power electronics, and digital energy management solutions to balance variable renewable power generation with electricity demand. Renewable energy integration also includes electric grid modernization, distributed energy resource management, and flexibility solutions that enable seamless operation of renewable-heavy power systems. The increasing adoption of clean energy and electrification is driving significant investments in technologies that support efficient renewable integration across utility-scale, commercial, industrial, and decentralized energy networks.

The growth of the market is primarily driven by the rapid expansion of solar and wind power installations worldwide, which require advanced grid balancing and transmission infrastructure to manage intermittent power generation. Increasing investments in grid modernization, smart grids, and utility-scale energy storage systems are further supporting market growth as utilities seek to improve grid reliability and flexibility. Rising electrification across transportation, industry, and buildings is also increasing electricity demand, accelerating the need for efficient renewable integration solutions. In addition, government decarbonization targets, net-zero commitments, and supportive renewable energy policies are encouraging large-scale investments in transmission networks, distributed energy systems, and digital grid management technologies globally.

Leading companies such as Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, and ABB are actively investing in advanced grid modernization and renewable integration technologies to support the growing penetration of renewable energy worldwide. These companies are focusing on expanding HVDC transmission systems, smart grids, energy storage integration, digital grid management platforms, and grid automation solutions to improve grid stability and flexibility. They are also strengthening their capabilities in distributed energy resource management, offshore wind integration, and battery storage systems to address increasing grid congestion and renewable intermittency challenges. In addition, strategic partnerships with utilities, governments, and renewable developers are enabling these companies to accelerate deployment of large-scale renewable integration infrastructure across major global markets.

Download Free sample to learn more about this report.

Renewable Energy Integration Market Trends

Rapid Expansion of Grid-Scale Energy Storage Systems are Amplifying Market Growth

One of the most significant trends in the market is the rapid deployment of grid-scale Battery Energy Storage Systems (BESS) to support renewable balancing and grid flexibility. As solar and wind penetration increases globally, utilities and grid operators are increasingly investing in storage systems to manage intermittency, stabilize frequency, and reduce renewable curtailment. According to the International Energy Agency (IEA), global battery storage deployment increased by more than 130% in 2023, driven largely by renewable integration requirements in China, the U.S., and Europe. Countries such as Australia and the U.S. are deploying multi-gigawatt storage projects paired with solar power and wind farms to enhance grid reliability. In addition, falling lithium-ion battery prices and growing investments in long-duration energy storage technologies are accelerating adoption. This trend is transforming energy systems from conventional centralized grids toward more flexible, storage-supported renewable power sources globally.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Global Renewable Energy Deployment to Push the Market Growth

The rapid expansion of renewable energy capacity worldwide is a major driver for the renewable energy integration market growth. Governments and utilities are aggressively increasing solar and wind installations to meet decarbonization and net-zero emission targets, creating significant demand for transmission upgrades, smart grids, and balancing infrastructure. According to IRENA, global renewable power capacity additions exceeded 470 GW in 2023, with solar accounting for the majority of new installations. As renewable penetration rises, grid operators face increasing challenges related to intermittency, voltage fluctuations, and congestion, driving investments in energy storage systems, grid automation, and advanced forecasting technologies. Large economies such as China, India, the U.S., and Germany are investing heavily in renewable evacuation corridors and HVDC transmission systems to integrate large-scale renewable projects into national grids. This accelerating renewable deployment pipeline continues to create strong long-term demand for renewable integration technologies and infrastructure globally.

Market Restraints

High Capital Investment Requirements for Grid Modernization to Limit the Market Growth

High capital investment requirements associated with grid modernization and transmission infrastructure development remain a major restraint for the market. Integrating large-scale renewable energy into existing power systems requires substantial investments in substations, HVDC transmission lines, smart grid technologies, energy storage systems, and distribution network upgrades. According to the IEA, global grid investments need to exceed USD 600 billion annually by 2030 to align with international climate goals, significantly higher than current investment levels. Many developing economies face financial constraints, aging grid infrastructure, and limited access to funding, slowing renewable integration projects. In addition, long project approval timelines, land acquisition challenges, and regulatory complexities often delay transmission expansion programs. Emerging markets in Africa, Southeast Asia, and Latin America continue to face infrastructure gaps that restrict renewable connectivity and grid flexibility. Further, limiting the pace of renewable integration despite growing renewable energy deployment targets globally.

Market Opportunities

Growth of Distributed Energy Resources and Smart Grids to Create New Growth Avenues

The increasing adoption of Distributed Energy Resources (DERs) and smart grid technologies presents a major growth opportunity for the market. Residential rooftop solar systems, commercial energy storage, electric vehicles, and decentralized renewable generation are transforming traditional electricity networks into more distributed and digitally managed systems. According to the IEA, distributed solar PV is expected to account for nearly half of global solar capacity additions by 2030, creating strong demand for advanced distribution management systems, Virtual Power Plants (VPPs), and smart grid infrastructure. Countries such as Germany, Australia, Japan, and the U.S. are rapidly deploying smart meters, AI-based grid management platforms, and demand response technologies to manage decentralized energy flows efficiently. Utilities are increasingly investing in digital grid automation and DER orchestration platforms to improve grid flexibility and reliability. This shift toward decentralized renewable systems is expected to create significant long-term opportunities for software providers, grid technology companies, and storage system developers globally.

Market Challenges

Grid Congestion and Renewable Curtailment to Limit Market Growth

Grid congestion and renewable energy curtailment remain major challenges for the market as renewable capacity additions continue to outpace transmission infrastructure expansion. Many countries are experiencing increasing interconnection backlogs and transmission bottlenecks, particularly in regions with large-scale solar and wind deployments located far from demand centers. According to the IEA, more than 1,500 GW of renewable energy projects worldwide are currently waiting for grid connections due to inadequate transmission capacity and permitting delays. In countries such as Germany, China, and the U.S., renewable curtailment has increased significantly during periods of peak renewable generation, resulting in financial losses for project developers and grid operators. The challenge is further intensified by aging grid infrastructure, slow permitting processes, and insufficient grid flexibility resources. Addressing congestion requires substantial investments in transmission expansion, energy storage systems, digital grid management, and cross-border interconnections to ensure reliable renewable integration and minimize power curtailment globally.

Segmentation Analysis

By Component

Increasing Investments in Transmission Infrastructures Led to Hardware Segment Growth

Based on component, the market is segmented into hardware, services, and software.

The hardware segment accounted for approximately 48.78% of the renewable energy integration market share in 2025. The segment represents the largest share driven by increasing investments in transmission infrastructure, substations, energy storage systems, smart meters, transformers, and power electronics required to integrate renewable energy into electricity grids. Utilities and grid operators are heavily investing in HVDC transmission systems, grid-forming inverters, Flexible AC Transmission Systems (FACTS), and battery energy storage systems (BESS) to manage the intermittency of solar and wind power. According to the International Energy Agency (IEA), global grid infrastructure investments exceeded USD 330 billion in 2023, with a substantial portion directed toward renewable integration projects. Countries such as China, the U.S., and Germany are expanding renewable evacuation corridors and smart transmission networks to reduce congestion and improve grid reliability. In addition, rapid deployment of utility-scale storage and offshore wind infrastructure is further strengthening demand for renewable integration hardware solutions globally.

Services is the second-leading segment growing at a CAGR of 13.25% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Grid Level

Substantial Infrastructure Required to Connect Utility-Scale Renewable Energy Projects to National Power Grids Led to Transmission-level Integration Segment Growth

Based on grid level, the market is segmented into microgrid-level integration, Behind-the-Meter (BTM) integration, distribution-level integration, and transmission-level integration.

The transmission-level integration segment accounted for approximately 46.45% of the market share. The segment represents the largest share due to the substantial infrastructure required to connect utility-scale renewable energy projects to national power grids. Large solar and wind farms are often located far from major electricity demand centers, creating strong demand for high-voltage transmission lines, HVDC systems, substations, and grid balancing infrastructure. According to the IEA, global transmission investment must expand significantly to support accelerating renewable deployment and prevent grid congestion. Countries such as China, India, the U.S., and Germany are investing heavily in Ultra-High-Voltage (UHV) and HVDC transmission corridors to transport renewable electricity across long distances efficiently. Offshore wind expansion in Europe and Asia is also increasing demand for advanced transmission interconnections and offshore substations.

The microgrid-Level Integration segment is expected to grow at a CAGR of 15.10% during the forecast period.

By Application

Extensive Investments in Transmission Infrastructure and Power Generation Projects to Propel Utilities Segment Growth

Based on application, the market is segmented into commercial & industrial, utilities, and others.

The utilities segment represented the largest market share of around 61.00% in 2025. The segment accounted for more than half of global market revenue due to extensive investments in transmission infrastructure, grid modernization, utility-scale energy storage, and renewable balancing systems. Utilities and grid operators are primarily responsible for integrating large-scale solar and wind projects into national power grids, driving significant demand for HVDC transmission lines, substations, smart grid technologies, and grid stability solutions. According to the International Energy Agency (IEA), global grid investment exceeded USD 330 billion in 2023, with a substantial portion allocated toward renewable integration and transmission expansion projects. Countries such as China, the U.S., Germany, and India are investing heavily in renewable evacuation corridors and utility-scale battery storage systems to address rising grid congestion and renewable intermittency. The utilities segment continues to dominate the market as governments accelerate decarbonization targets and large-scale renewable capacity additions globally.

The commercial & industrial segment is the second-leading segment growing with a CAGR of 12.75% during the forecast period.

Renewable Energy Integration Market Regional Outlook

By region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Renewable Energy Integration Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the dominant region in the market and in 2025 it was valued at USD 116.45 billion, accounting for approximately 43.42% of global revenues. Asia Pacific dominates the market owing to massive renewable energy deployment and large-scale transmission infrastructure investments across China, India, Japan, and Southeast Asia. China remains the largest market globally due to extensive UHV transmission projects, utility-scale solar and wind installations, and rapid battery storage deployment. India is also expanding Green Energy Corridor projects and grid modernization initiatives to support accelerating renewable capacity additions. The region’s strong industrial growth, rising electricity demand, and increasing electrification are driving significant investments in renewable balancing systems, smart grids, and grid expansion projects. In addition, Southeast Asia is emerging as a high-growth market due to expanding renewable adoption and regional grid interconnection initiatives.

China Renewable Energy Integration Market

China remains the dominant contributor in Asia Pacific, valued at USD 58.01 billion in 2025, and is estimated to reach USD 68.68 billion in 2026. China dominates the global market through massive investments in UHV transmission systems, utility-scale renewable projects, and battery storage deployment. The country is rapidly expanding renewable evacuation infrastructure and grid modernization programs to support its accelerating solar and wind capacity additions.

India Renewable Energy Integration Market

India was valued at USD 18.42 billion in 2025 and is estimated to reach USD 21.76 billion in 2026. India is one of the fastest-growing markets due to large-scale renewable capacity expansion and ongoing Green Energy Corridor transmission projects. Rising investments in grid modernization, battery storage systems, and renewable balancing infrastructure are supporting the integration of rapidly growing solar and wind installations.

Japan Renewable Energy Integration Market

Japan was valued at USD 11.17 billion in 2025 and is estimated to reach USD 13.25 billion in 2026. Japan’s market is driven by increasing offshore wind development, battery storage deployment, and smart grid investments aimed at improving energy security and grid flexibility. The country is also focusing on distributed energy management systems and renewable balancing technologies to support growing renewable adoption.

North America

North America market was valued at USD 53.43 billion in 2025, accounting for approximately 19.92% of the global market. North America represents a significant share of the market due to strong investments in grid modernization, utility-scale energy storage, and renewable transmission infrastructure across the U.S. and Canada. The region is witnessing rapid deployment of solar and wind projects supported by government incentives such as the U.S. Inflation Reduction Act (IRA), which is accelerating investments in transmission expansion and battery storage systems. Utilities are increasingly adopting smart grid technologies, Virtual Power Plants (VPPs), and AI-based energy management solutions to improve grid flexibility and reliability. In addition, rising electrification, data center expansion, and distributed renewable adoption are driving strong demand for behind-the-meter integration and grid balancing technologies across the region.

U.S. Renewable Energy Integration Market

The U.S. market was valued at USD 46.89 billion in 2025 and is estimated to reach USD 55.61 billion in 2026. The U.S. is one of the largest markets in the region, driven by rapid utility-scale solar and wind deployment, large battery storage projects, and grid modernization initiatives supported by the Inflation Reduction Act (IRA). Increasing investments in transmission expansion, smart grids, and virtual power plants are accelerating renewable integration across major states such as Texas and California.

Europe

Europe accounted for USD 65.80 billion in 2025, representing approximately 24.54% of global revenues. Europe is one of the most advanced markets due to high renewable penetration, aggressive decarbonization targets, and strong investments in smart grids and offshore wind infrastructure. Countries such as Germany, the U.K., Spain, and the Netherlands are investing heavily in grid flexibility, energy storage systems, and offshore transmission networks to support large-scale renewable deployment. The region is also leading in distributed energy integration, virtual power plants, and demand response programs supported by advanced regulatory frameworks. In addition, increasing cross-border interconnections and modernization of aging grid infrastructure are strengthening Europe’s renewable integration capabilities as the region moves toward carbon neutrality goals.

Germany Renewable Energy Integration Market

Germany was valued at USD 15.58 billion in 2025 and is estimated to reach USD 17.93 billion in 2026. Germany is a major market due to high solar and wind penetration, increasing grid congestion, and extensive investments in transmission modernization. The country is focusing on HVDC transmission corridors, smart grids, and energy storage systems to support its energy transition and reduce renewable curtailment.

U.K. Renewable Energy Integration Market

The U.K. market was valued at USD 12.05 billion in 2025 and is estimated to reach USD 14.25 billion in 2026. The U.K. is a leading market for offshore wind integration and grid flexibility solutions, supported by strong decarbonization targets and investments in battery storage systems. The country is actively expanding offshore transmission infrastructure and smart balancing technologies to manage rising renewable penetration and improve grid stability.

Latin America

Latin America accounted for USD 18.15 billion in 2025, accounting for approximately 6.77% of global revenues. Latin America is experiencing growing demand driven by expanding solar and wind capacity, transmission modernization, and hydro-renewable balancing requirements. Brazil dominates the regional market due to its large interconnected grid network, rising renewable investments, and extensive transmission expansion programs. Countries such as Chile and Mexico are also witnessing strong growth in solar-plus-storage projects and renewable grid infrastructure development. The increasing need to connect renewable projects located far from urban demand centers is creating demand for long-distance transmission systems and grid flexibility solutions. In addition, mining electrification and decentralized renewable projects are supporting the adoption of microgrids and energy storage systems across the region.

Middle East & Africa

The Middle East & Africa was valued at USD 14.35 billion in 2025. The region is emerging as a high-growth market due to large-scale solar projects, grid modernization programs, and green hydrogen developments. GCC countries, particularly Saudi Arabia and the UAE, are investing heavily in renewable megaprojects, battery storage systems, and smart transmission infrastructure to diversify their energy mix and reduce dependence on fossil fuels. South Africa is also accelerating renewable integration investments to address grid reliability challenges and support renewable power expansion. Across Africa, increasing electrification initiatives and remote energy access programs are driving demand for microgrids and decentralized renewable systems. The region’s ongoing investments in greenfield grid infrastructure and cross-border interconnections are expected to create strong long-term growth opportunities.

GCC Renewable Energy Integration Market

The GCC market which was valued at USD 8.00 billion in 2025 and is estimated to reach USD 9.05 billion in 2026. The GCC region is emerging as a high-growth market driven by giga-scale solar projects, green hydrogen developments, and smart grid investments across Saudi Arabia and the UAE. Increasing deployment of utility-scale battery storage and transmission infrastructure is supporting the transition toward renewable-heavy power systems in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Investment in Grid Modernization and Energy Storage Integration by Key Players are Booming Market Share

Leading companies such as Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, and ABB are playing a critical role in advancing the renewable energy integration market through large-scale investments in grid modernization, smart grid technologies, energy storage integration, and transmission infrastructure. These companies are actively developing HVDC systems, grid automation platforms, battery energy storage solutions, and digital energy management technologies to improve grid flexibility and support increasing renewable penetration globally. They are also partnering with utilities, governments, and renewable developers to deploy offshore wind transmission networks, renewable evacuation corridors, and distributed energy management systems across major markets. In addition, these companies are strengthening their focus on AI-based grid optimization, virtual power plants, and decentralized energy integration solutions to address rising grid congestion, renewable intermittency, and electrification demand worldwide.

List of Key Renewable Energy Integration Companies Profiled

- Hitachi Energy (Switzerland)

- Siemens Energy (Germany)

- GE Vernova (U.S.)

- Schneider Electric (France)

- ABB (Switzerland)

- Eaton (Ireland)

- Honeywell (U.S.)

- Mitsubishi Electric (Japan)

- Toshiba Energy Systems & Solutions (Japan)

- NextEra Energy (U.S.)

- Fluence Energy (U.S.)

- Tesla Energy (U.S.)

- Wärtsilä Energy (Finland)

- Sungrow Power Supply (China)

- Huawei Digital Power (China)

KEY INDUSTRY DEVELOPMENTS

- May 2026: The All India DISCOMs Association (AIDA) partnered with the U.S.-based Energy Systems Integration Group (ESIG) through an MoU to support India’s power distribution sector with global technical expertise. The collaboration focuses on renewable energy integration, grid modernization, system planning, and improving grid flexibility. Both organizations will promote knowledge sharing, technical workshops, and collaboration between Indian and international power sector experts to strengthen the operational capabilities of DISCOMs.

- May 2026: ADB plans to invest USD 70 billion in energy and digital infrastructure across Asia Pacific by 2035, including USD 50 billion for the Pan-Asia Power Grid Initiative. The program aims to strengthen cross-border renewable energy trade through transmission expansion, grid integration, storage, and digitalization, while improving energy access and reducing regional power-sector emissions.

- February 2026: Siemens and Mescada are deploying one of Australia’s largest AI-enabled cloud-based SCADA systems for Global Power Generation Australia (GPGA). The system will connect eight renewable energy and storage assets across Australia, enabling centralized real-time monitoring, control, and future integration with the Australian Energy Market Operator (AEMO) for grid-responsive operations.

- November 2025: ABB has been chosen by ContourGlobal to upgrade the solar field control systems at four CSP plants in Spain using ABB Ability Symphony Plus SCADA solutions. The modernization will improve renewable power integration, system reliability, scalability, and cybersecurity for long-term grid operations.

- June 2025: Hitachi Energy started supplying a substation for Jordan’s 52.5 MW Shams Ma’an solar project, one of the largest photovoltaic plants in the Middle East. The project uses more than 680,000 solar panels and is expected to generate 160 GWh annually, supporting Jordan’s renewable energy targets and reducing dependence on imported fuels.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.36% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Grid Level

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 268.18 billion in 2025 and is projected to reach USD 856.26 billion by 2034.

In 2025, the market value stood at USD 116.45 billion.

The market is expected to exhibit a CAGR of 13.36% during the forecast period.

By component, the hardware segment is expected to lead the market.

The rising global renewable energy deployment are driving market expansion.

Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, and ABB are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 314

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us