Generation Military Power Supply Market Size, Share & Industry Analysis, By Platforms (Air Platforms, Land Platforms, Naval Platforms, Space & Strategic Platforms, and Fixed Military Infra), By Component (Hardware and Software), By Application (C4ISR & Mission Computing, Radar & Electronic Warfare, Communications & Datalinks, Optronics & Fire Control, Weapon & Missile Systems Electronics, Unmanned & Robotic Systems, and Infrastructure & Support Systems), By Output Power Rating (Low Power, Medium Power, High Power, and Very High Power), By End User, and Regional Forecast, 2026-2034

Generation Military Power Supply Market Size and Future Outlook

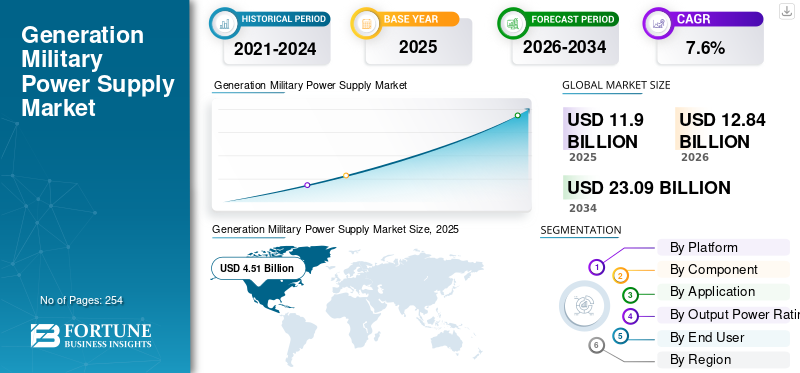

The global generation military power supply market size was valued at USD 11.90 billion in 2025. The market is projected to grow from USD 12.84 billion in 2026 to USD 23.09 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period. North America dominated the global generation military power supply market with a market share of 37.89% in 2025.

Generation military power supplies include the sturdy AC to DC and DC to DC units, VPX/VME and brick converters, inverters, battery, and UPS systems, along with related power-conditioning hardware and software. These systems keep combat platforms, sensors, weapons, and command systems powered reliably in tough military grade environments, whether on aircraft, ships, vehicles, satellites, or fixed sites. This market expansion is driven by armed forces are integrating more electronics into every platform, including sensors, processors, datalinks, electronic warfare, and AI modules. This trend raises the need for greater power density and high efficiency.

Key players in the advanced military power supply market include both specialist power-conversion vendors and large defense contractors. Companies such as TDK-Lambda, Vicor, SynQor, VPT, XP Power, Advanced Conversion Technology, Milpower Source, and Gaia Converter, are some of the major players in the market. This company’s focus on high-reliability AC-DC and DC-DC modules, VPX and VME cards, and custom bricks for tough military environments. Surrounding them are major integrators and defense original equipment manufacturers such as BAE Systems, Thales, Leonardo, RTX, Northrop Grumman, Lockheed Martin, Honeywell, Safran, HENSOLDT, Elbit, and IAI.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Increasing Uses and Additional Integration of Electronics Devices on Military Platforms Driving Market Growth

Every modern combat platforms now contain additional electronics than before. New AESA radars, multi-band EW suites, high-resolution optronics, extra mission computers, datalinks, cyber gear, and AI/ML processors all compete for power and cooling within the same airframe, hull, or vehicle. Legacy 28 Vdc buses and older generation components are not able to use any further with the demands of higher loads, tighter size, weight, and power requirements, and tougher mission profiles. Resulting in manufacturers and defense ministries to upgrade to high-density AC-DC and DC-DC converters, VPX power cards, smart DC-UPS, and digitally managed power rails, driving the market expansion.

In July 2023, SynQor launched a new 3U, three-phase AC-input VPX power supply (VPX-3U-AC115-3-C). This product targets advanced military and aerospace chassis. It meets VITA 62.1 and MIL-STD standards and can deliver efficient 28 Vdc power over 47 to 800 Hz for aircraft and vehicle inputs. This development responds to the demand for denser and more flexible power systems to support increasing electronic payloads.

MARKET RESTRAINTS

Strict Military Standards and Export Controls Restrains Market Growth

Generation military power supply vendors has to deal with a lot of paperwork and qualification processes. To get a power supply unit onto a vehicle, aircraft, ship, or radar, it has to pass various MIL-STD power and EMI tests (1275, 704, 461, 810, VITA-62, and others). It must meet counterfeit parts controls and regularly compliance with ITAR/DFARS export rules. Each new module or redesign adds more test time, documentation, audits, and sometimes full requalification, even for minor component changes, hindering the market growth.

For example, in February 2024, the U.S. Department of Defense issued DoDI 4140.67 on counterfeit prevention. This updated policy emphasizes detecting, fixing, and tracking electronic parts in all weapon and information systems.

MARKET OPPORTUNITIES:

Electrification of Ships, Vehicles, and Bases Is Creating Major Opportunities in Military Power Supply Market

The armed forces are shifting from providing just enough DC power to run electronics to using fully electric or hybrid-electric platforms and microgrids on ships, tactical vehicles, and fixed bases. Integrated electric propulsion on surface combatants, hybrid drives, high-energy sensors, and directed-energy weapons all require much higher, cleaner, and more dynamically managed electrical power than older systems. This change opens up opportunities for new types of high-power converters, solid-state distribution, and microgrid-ready military power systems. On land, tactical microgrids and standardized connections between generators, storage, and loads are becoming essential design features instead of experimental projects.

Additionally, rising investments in the next generation military power supply, along with the gradual integration of renewable energy sources into tactical microgrids and base infrastructure, are creating new opportunities for smart, efficient power-conversion systems.

For instance, the U.S. Navy’s Zumwalt-class destroyers (DDG-1000) are the first surface combatants with full-electric propulsion. They use an Integrated Power System (IPS) that generates and converts high-voltage power for both propulsion and ship systems. This design supports future high-energy sensors and weapons.

GENERATION MILITARY POWER SUPPLY MARKET TRENDS:

Shift toward Digitally Managed, High-density Power Systems is Changing Market

Notable trend is manufacturers are moving away from bulky, simple units to smaller, high-density modules and VPX/VITA-62 power cards that can be monitored and controlled digitally. As manufacturers want more power in a smaller space, full MIL-STD compliance, and the ability to check rail health, and temperature from within the mission computer. This is driving the use of modular military commercial DC-DC families and VPX supplies.

MARKET CHALLENGES:

Fragile Defense Electronics and Microelectronics Supply Chains Are Challenging Market Growth

Demand for new military power systems, building and delivering military power supply solutions on time is becoming more difficult. The supply chain for high-reliability components is fragile and politically sensitive. Rugged PSUs require niche parts, such as radiation-hardened microelectronics, power semiconductors, magnetics, capacitors, and rare-earth materials. Many of these components come from limited global suppliers, and in some cases, they are highly concentrated in a few countries. Export controls, sanctions, trade restrictions, and the wider effort to reduce reliance on China are increasing lead times, costs, and redesign risks.

Impact of Russia-Ukraine War

Russia-Ukraine War is Accelerating but Also Changing Demand in Market

The war has caused the highest defense spending in years, especially in Europe and some parts of the Middle East. This rise boosts demand for power supplies in new radars, GBAD systems, C4ISR nodes, EW suites, and hardened infrastructure. Budgets are moving up, and government’s prioritizing air and missile defense, artillery, ammunition, drones, and electronic warfare devices and platforms. All of these need a lot of power electronics. At the same time, sanctions on Russia, export controls, and the rush to localize ammunition and missile production in Europe are straining component supply, qualification pipelines, and pricing. As a result, OEMs are rushing to increase capacity while dealing with a more complicated regulatory and supply chain environment.

For instance, according Stockholm international peace research institute SIPRI reports 2025 that global military spending reached USD 2.72 trillion in 2024, a 9.4% increase in real terms from the previous year. This marks the steepest rise since the Cold War ended, with particularly rapid growth in Europe and the Middle East following Russia’s full-scale invasion of Ukraine. Meanwhile, the EU adopted the Act in Support of Ammunition Production (ASAP) in July 2023 to increase industrial capacity for artillery shells and missiles.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Air Platforms’ Increasing Radar, EW, and Avionics Integration Driving Growth in Military Power Supplies

In terms of platform, the market is categorized into air platforms, land platforms, naval platforms, space & strategic platforms, and fixed military infra.

Air platforms segment dominates the generation military power supplies market. Every fighter, bomber, ISR aircraft, and advanced helicopter is becoming a flying server support. AESA radars, digital EW suites, targeting pods, high-bandwidth datalinks, sensor fusion computers, and increasingly, AI accelerators all require clean, tightly regulated power within a space, weight, and power (SWaP) constrained airframe. This avionics, radar, or EW upgrade often requires a parallel update of the aircraft’s power system. This includes higher-density AC-DC/DC-DC converters, VPX power cards, smarter DC-UPS, and power-distribution hardware, resulting in dominance of the segment.

- For instance, in April 2025, L3Harris’ Viper Shield next-generation electronic warfare suite for F-16 Block 70 aircraft completed its first flight on a Royal Bahraini Air Force jet at Edwards AFB. It is expected to enter service in 2026, adding a digital, high-power EW payload on top of the existing AESA radar and avionics.

Space & strategic platforms segment is fastest growing segment in market expected to grow at a CAGR of 10.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Hardware-Centric Designs Drives Revenue in Military Power Supply Market

On the basis of component, the market is classified into hardware and software.

Hardware holds the largest market share due to every mission system depends on physical power-conversion components. These include rugged AC-DC front ends, DC-DC modules, VPX/VITA-62 cards, inverters, rectifiers, battery chargers, and DC-UPS units. They must withstand shock, vibration, temperature extremes, and strict MIL-STD EMI standards. While software, monitoring, and control are important, the real profit comes from qualified metal boxes and cards that can deliver hundreds to thousands of watts consistently in aircraft, ships, vehicles, and shelters. As platforms add more electronics, defense customers are purchasing higher-density, EMI-filtered, standard-form-factor hardware, segment continues to dominate the market growth.

- For instance, Milpower Source, Vicor, Amphenol Aerospace, NAI, and others companies are consistently introducing new rugged AC-DC and VITA-62 VPX power supplies. These products provide over 600 to 1400 watts with built-in EMI filters and comply with MIL-STD-704/810/461. They are specifically marketed as drop-in hardware for air, land, and naval platforms.

Software segment is fastest growing segment in market expected to grow at a CAGR of 13.5% over the forecast period.

By Application

C4ISR and Mission Computing Modernization Is Driving Growth in Military Power Supply Market

Based on application, the market is segmented into C4ISR & mission computing, radar & electronic warfare, communications & datalinks, optronics & fire control, weapon & missile systems electronics, unmanned & robotic systems, and infrastructure & support systems.

C4ISR and mission computing dominates the generation military power supply market share. C4ISR and mission computing are filled with servers, RF cards, crypto, storage, radios, and AI accelerators that need to operate 24/7 in vehicles, shelters, ships, and fixed locations. To install the network or implement new battle management software requires denser, cleaner, and better-protected power management. This is why C4ISR and mission computing is a leading area in the military power supply solutions.

- For instance, in October 2024, Leidos received a USD 331 million contract to modernize the U.S. Army’s Global Unified Network. This aligns with the Army’s Network Modernization Strategy and Unified Network Plan and aims to deploy a standardized, software-defined structure across multiple sites.

Unmanned & robotic systems segment is fastest growing segment in market at a CAGR of 9.9% growth across the forecast period.

By Output Power Rating

Workhorse Role in C4ISR Racks and VPX Systems, Medium-Power (500 W to 2.50 kW) Segment Dominates Market

Based on output power rating, the market is segmented into low power (< 500 W), medium power (500 W to 2.50 kW), high power (2.50 kW to 10.00 kW), and very high power (> 10.00 kW).

Medium-power supplies play a crucial role in modern defense electronics. They provide enough power for dense C4ISR servers, radar processors, electronic warfare racks, communications gateways, and vehicle or shelter power panels. At the same time, they are compact and efficient, fitting into VPX cards, ATR boxes, and 19" racks without exceeding size, weight, and power or cooling limits. As militaries adopt VPX/OpenVPX and modular mission computers, most new designs fall into the 500 W to 2.5 kW range, typically using a 600 to 1000 W card or a 1 to 2 kW front-end that supplies multiple DC rails and batteries, result in segments dominance.

- For instance, a series of recent VPX and VITA-62 power products from suppliers such as SynQor, Milpower Source, and Amphenol Aerospace cluster around 600 to 1000 W per 3U module. These products specifically target mission-computer, radar, and electronic warfare chassis used in air, land, and naval platforms.

Very High Power (> 10.00 kW) segment is expected to grow at a CAGR of 11.7% growth across the forecast period.

By End User

Central Role in Integrating Power into Every Combat System, Platform & System OEMs Dominate Market

Market is segmented by end-user into ministries of defense, platform & system OEMs, subsystem/payload integrators, and MRO & upgrade providers.

Platform and system OEMs are essential to nearly every defense program. This role puts them in charge of specifying, integrating, and qualifying military power supplies. Whether it's a fighter, frigate, UAV, armored vehicle, radar, or EW suite, the OEM controls the architecture. They ensure that the power system meets MIL-STD requirements, can withstand shock and vibration, stays within thermal limits, and works safely with avionics, processors, and RF loads. As long as defense platforms continue to become more electronically complex, OEMs will stay the key players for adopting high-value power supply units.

Subsystem/payload integrators is set to grow at rate of 8.3% growth across the generation military power supply market forecast period.

Generation Military Power Supply Market Regional Outlook

Sheer Scale of Defense Spending and Electronics-Heavy Modernization, North America Dominates Market

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Generation Military Power Supply Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America next generation military power supply held the dominant share in 2024 valuing at USD 4.24 billion and also took the leading share in 2025 with USD 4.51 billion, led primarily by the United States, which alone contributes over 92.81% share in 2025. The U.S. is the leading player in the military power supply market. It represents the biggest part of global defense spending and manages the most electronics-heavy portfolios of radars, electronic warfare, C4ISR, missile defense, and strategic systems. In 2024, the Americas made up around 40% of global military spending, surpassing Europe at 26% and Asia-Oceania at 23%. The U.S. alone requested about USD 850 billion for the FY2025 DoD budget.

Asia Pacific and Europe

Asia Pacific and Europe are expected to witness significant generation military power supply market growth in the coming years. During the forecast period, the Europe region is projected to have a fastest growth rate of 9.2%. The market in Europe is estimated to be USD 2.95 billion in 2025. The Russia-Ukraine war is a major driver. Countries are rearming, replacing Soviet and Russian equipment, improving air and missile defense, and investing heavily in ISR, secure communications, and artillery command and control. In this region, both the France and Germany are expected to reach USD 0.48 billion and USD 0.62 billion, respectively, in 2026. In Asia Pacific, countries including China, India, Japan, and South Korea rapid growth, China, India, Japan, South Korea, and Australia are also building up their military capabilities in the long term. They are focusing on naval expansion, air power, long-range missiles, and space and ISR. Based on these factors, countries such as China expect to reach a valuation of USD 1.46 billion, and India is set to reach USD 0.44 billion by 2026.

Middle East & Latin America

Meanwhile, the Middle East & Africa, and Latin America are expected to witness significant growth in the forthcoming years. Further, both regions contributes approximately 8.74% and 5.27% respectively in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Specialized Power-Electronics Vendors and Large Defense Contractors Are Battling for Design Wins in an Increasingly Program-Driven, High-Compliance Market

The military power supply market includes a mix of specialized power-conversion companies and large defense OEMs and electronics firms. On one side, there are niche players focused on rugged AC-DC/DC-DC modules, VPX/VITA-62 cards, DC-UPS systems, and filters. They compete on power density, high efficiency, MIL-STD compliance, lead times, and their willingness to customize. The major primes and system integrators, including those in aircraft, ships, vehicles, radar, electronic warfare, and C4ISR. These companies decide which power supply units get designed into their platforms and often maintain preferred vendor lists, long-term agreements, and tightly integrated reference designs.

Key players such as TDK-Lambda, Vicor, SynQor, VPT, XP Power, Advanced Conversion Technology, Milpower Source, and Gaia Converter compete to provide reliable bricks, VPX/VITA-62 cards, DC-UPS units, and filters. Across the table are primes and defense electronics companies such as Lockheed Martin, Northrop Grumman, RTX, BAE Systems, Thales, Leonardo, Saab, HENSOLDT, Elbit Systems, and Israel Aerospace Industries (IAI). These companies either use their own qualified power modules or closely partner with these specialists. In practice, most revenue comes from the point where these two groups meet. This occurs when a specialist PSU is integrated into a long-life platform or sensor program owned by a major prime.

LIST OF KEY GENERATION MILITARY POWER SUPPLY COMPANIES PROFILED:

- TDK-Lambda Corporation (Japan)

- Vicor Corporation (U.S.)

- SynQor, Inc. (U.S.)

- VPT, Inc. (U.S.)

- XP Power (Singapore)

- Advanced Conversion Technology (U.S.)

- Milpower Source, Inc. (U.S.)

- Gaia Converter (France)

- North Atlantic Industries (U.S.)

- Advanced Energy / Artesyn Embedded Power (U.S.)

- Behlman Electronics, Inc. (U.S.)

- Crane Aerospace & Electronics (U.S.)

- Eaton Corporation (Ireland)

- Astrodyne TDI (U.S.)

- Powerbox International (Sweden)

- Delta Electronics (Taiwan)

KEY INDUSTRY DEVELOPMENTS:

- August 2024: Aegis Power Systems rolled out a MIL-STD-3071 Tactical Microgrid Interface Module, designed as a drop-in hardware/software node for smart military microgrids, providing grid-stability, safety and cyber-secure control functions.

- March 2024: Vicor continued to promote its VITA 62 MIL-COTS power supplies for 3U and 6U OpenVPX systems, delivering up to 600 W (3U) and 1000 W (6U) from 28 V or 270 V inputs, highlighting how standardized, conduction-cooled VPX power modules are becoming a baseline option across U.S. and allied military electronics racks.

- September 2023: Amphenol Aerospace introduced the M4268 3U VITA 62 VPX DC-DC power supply, a 1000 W multi-output module with internal EMI filters, reverse-battery protection and I²C/VITA 46.11 system management, aimed at airborne, ground and naval OpenVPX systems that need higher power density and smarter management on the VPX backplane.

- September 2023: VPT released the SGRBX configurable 1600 W GaN-based DC-DC converter box for space applications, building on its SGRB series; it integrates an EMI filter, guarantees 100 krad TID and 85 MeV/mg/cm² SEE performance, and reaches up to 96% efficiency, showcasing how state-of-the-art GaN technology is being pushed into high-reliability military and strategic power designs.

- July 2022: SynQor announced its VPX-3U-AC115-3-C three-phase AC-input VPX power supply, delivering around 700 W at 91.5% efficiency, compliant with VITA 62.1 and multiple MIL-STDs, and explicitly targeted at critical military/aerospace VPX power slots a direct response to growing demand for high-density, chassis-standardized PSUs in C4ISR and EW racks.

REPORT COVERAGE

The global generation military power supply market analysis provides an in-depth study of market size; company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technologically advanced, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

| Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.6% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Platform

|

|

By Component

|

|

|

By Application

|

|

|

By Output Power Rating

|

|

|

By End User

|

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 12.84 billion in 2026 and is projected to reach USD 23.09 billion by 2034.

In 2025, the market value stood at USD 4.51 billion.

The market is expected to exhibit a CAGR of 7.6% during the forecast period.

The air platforms segment led the market by platform.

The increasing uses and additional integration of electronics devices on military platforms are the key factors driving the market growth.

TDK-Lambda Corporation (Japan), Vicor Corporation (U.S.), SynQor, Inc. (U.S.), VPT, Inc. (U.S.), XP Power (Singapore), Advanced Conversion Technology (U.S.), Milpower Source, Inc. (U.S.), Gaia Converter (France), and North Atlantic Industries (U.S.), among others are the top companies in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 254

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us