Drone Defense Systems Market Size, Share & Industry Analysis, By Platform (Fixed / Site-Based, Vehicle-Mounted, and Others), By Component (Hardware, Software, and Services), By Technology (Detection & Tracking, Identification & Classification, and Others), By Threat Type (Small Commercial / Modified Drones, Loitering Munitions, and Others), By Application (Battlefield / Tactical Force Protection, Airbase & Military Installation Protection, and Others), By End User (Military Forces, Critical Infrastructure, Homeland Security & Law Enforcement, and Others), and Regional Forecast, 2026-2034

Drone Defense Systems Market Size and Future Outlook

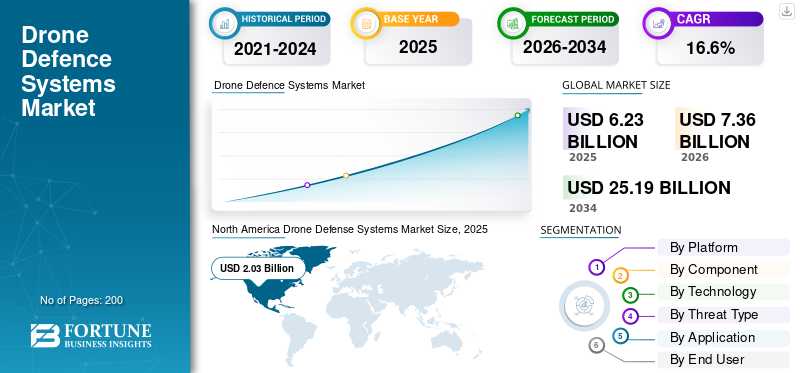

The drone defense systems market size was valued at USD 6.23 billion in 2025. The market is projected to grow from USD 7.36 billion in 2026 to USD 25.19 billion by 2034, exhibiting a CAGR of 16.6% during the forecast period. North America dominated the drone defense systems market with a market share of 32.58% in 2025.

The drone defense systems are used to detect, track, identify, and neutralize hostile unmanned aerial systems across defense, homeland security, critical infrastructure, airports, borders, and maritime sites. The market is growing as drones are now being used for reconnaissance, payload delivery, loitering attacks, infrastructure strikes, and battlefield disruption. This is pushing buyers toward layered counter-UAS systems that combine radar, RF detection, EO/IR sensors, AI-based classification, soft-kill jamming, hard-kill interceptors, and directed-energy weapons.

Key players in the market are RTX/Raytheon, Thales, Leonardo, Rafael Advanced Defense Systems, MBDA, Northrop Grumman, Lockheed Martin, Anduril Industries, D-Fend Solutions, DroneShield, and Hensoldt. These companies are driving the market through integrated detect-and-defeat systems, laser-based interception, AI-enabled command-and-control, and modular solutions for military bases, critical infrastructure, airports, naval assets, and deployed forces.

Download Free sample to learn more about this report.

DRONE DEFENSE SYSTEMS MARKET TRENDS

Shift from Basic Detection-And-Jamming Solutions toward Layered Systems to be a New Market Trend

The market is shifting from basic detection-and-jamming solutions toward layered systems that can physically defeat drones, loitering munitions, and saturation-style attacks. This trend is fueled by the limits of soft-kill systems against autonomous drones, pre-programmed routes, frequency-hopping links, and one-way attack UAVs. As a result, buyers are increasingly prioritizing hard-kill interceptors, high-power lasers, RF effectors, and integrated command-and-control systems that can detect, classify, assign an effector, and neutralize the threat with lower cost per engagement. Moreover, Artificial intelligence is becoming a core technology trend in the market as buyers need faster detection, lower false alarms, and better classification of hostile drones.

In December 2025, Israel’s Ministry of Defense and Rafael delivered the first operational Iron Beam high-power laser system to the IDF after testing against rockets, mortars, and UAVs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Battlefield Drone Attacks are Driving Urgent Drone Defense Systems Procurement

The global drone defense systems market growth is driven by the rapid battlefield use of drones for surveillance, targeting, loitering attacks, and low-cost strike missions. Drone defense is becoming a core layer of air defense and force protection. This is pushing procurement toward integrated counter-UAS systems that combine radar, RF detection, EO/IR tracking, command-and-control, electronic warfare, and kinetic or non-kinetic interceptors for both fixed-site and mobile deployments. AI driven counter-UAS systems are gaining adoption since manual monitoring is no longer enough against fast, small, and low-flying drone threats.

In February 2024, the U.S. Army announced a rapid acquisition contract for 600 Coyote 2C counter-UAS interceptors from Raytheon, stating that the award supported a demand increase and the need to expand production capacity.

MARKET RESTRAINTS

Regulatory Frameworks and Spectrum Restrictions Restrain Wider Civil Counter-UAS Deployment

Major restrains is strict regulatory frameworks, airspace constraints, and radio-frequency controls. This is mainly true in civilian areas including airports, stadiums, ports, refineries, and city infrastructure. Many counter-drone systems depend on RF jamming, GNSS disruption, spoofing, or kinetic methods. But, these techniques can disrupt lawful communications, aviation safety, emergency services, and public networks nearby. As a result, non-military buyers limit deployments to detection-only systems, or they require federal or security agency involvement before using active mitigation.

In June 2025, the U.S. Federal Aviation Administration updated its guidance for UAS Detection, Mitigation, and Response at airports. This update mandates that airport operators conduct an aeronautical study before they can deploy UAS detection or mitigation systems on airport premises.

MARKET OPPORTUNITIES

Long-Term Defense Modernization Programs Create a Scalable Counter-UAS Opportunity

An important growth opportunity for the market is the evolution from ad hoc, reactive acquisitions of counter-drone systems to complete defense modernization programmes. Military services are currently interested in flexible solutions capable of evolving with improved sensor capabilities, AI-based classification algorithms, electronic warfare tools, kinetic effectors, directed energy technology, and command and control. This opportunity allow companies to provide modular hardware, open architecture, life cycle sustainment, and local manufacturing capabilities instead of purely stand-alone jamming and detection systems.

MARKET CHALLENGES

Low-Collateral Defeat Remains a Major Deployment Challenge for Counter-UAS Systems

One of the major challenges in the market is neutralizing unauthorized drones without doing any collateral damage. This is complicated in the case of military bases, airports, urban environments, important infrastructure sites, energy facilities, and crowded spaces where jamming can interfere with communication systems, kinetic weapons can generate debris, and powerful systems require stringent safety measures. With drones becoming fast, specially designed, autonomous, and undetectable, customers require counter-UAS solutions that can neutralize drones rapidly without causing any harm to friendly assets, civilians, infrastructure, and adjacent airspace.

Impact of Ongoing Conflicts

Active Conflicts are Accelerating Layered Drone Defense Systems Procurement

The Russia-Ukraine war, Middle East conflicts, Red Sea/Gulf security pressure, and other active conflict zones are directly reshaping the market. These conflicts have proved that low-cost drones, FPV systems, loitering munitions, and one-way attack UAVs can damage airbases, energy sites, naval assets, command posts, vehicles, and frontline positions at very low cost. As a result, defense buyers are moving faster toward layered counter-UAS systems that combine detection, AI-based classification, electronic warfare, hard-kill interceptors, directed energy, and mobile force-protection platforms. The impact is drone defense systems are no longer treated as a niche add-on, it is becoming a standard requirement within air defense, base protection, battlefield mobility, and critical-infrastructure security.

In September 2024, NATO’s Drone Defense Systems Technical Interoperability Exercise included Ukraine for the first time, with more than 450 participants from 19 NATO Allies and three partner countries testing counter-drone interoperability. In September 2025, U.S. CENTCOM and Saudi forces led the Middle East’s largest live-fire counter-UAS exercise under Red Sands, focused on detecting, tracking, and eliminating modern drone threats.

Segmentation Analysis

By Platform

Due to Persistent Protection Needs at Airbases and Strategic Sites, Fixed / Site-Based Systems Dominated Platform Segment

In terms of platform, the market is categorized into fixed / site-based, vehicle-mounted, man-portable, and shipborne.

Fixed / site-based segment dominated the global market in 2025, as most high-value drone defense systems deployment still revolves around permanent or semi-permanent sites. Airbases, military installations, ammunition depots, command centers, radar sites, airports, ports, oil-and-gas assets, and critical infrastructure need continuous surveillance and layered protection, not temporary coverage. These locations usually require integrated radar, RF detection, EO/IR sensors, AI-based classification, jamming, command-and-control, and hard-kill or directed-energy options.

Shipborne segment is expected to grow at a highest CAGR of 22.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Due to Sensor-and-Effector Heavy Procurement, Hardware Dominated Component Segment

On the basis of component, the market is classified into hardware, software, and services.

Hardware segment led the market in 2025, since the market still relies on a robust physical layer before software and services. To build an effective detect-track-defeat chain, buyers need radars, RF detectors, EO/IR cameras, acoustic sensors, jammers, GNSS-disruption equipment, interceptors, launchers, directed-energy systems and mobile or fixed-site kits. Software is growing quickly, but hardware remains the largest component as defense forces and security agencies are still scaling the core equipment base needed to protect airbases, borders, critical infrastructure, naval assets, and deployed forces.

Software segment is expected to show the fastest growth, registering a CAGR of 23.9% over the forecast period.

By Technology

Due to Need for Early Threat Visibility, Detection & Tracking Dominated Technology Segment

On the basis of technology, the market is classified into detection & tracking, identification & classification, soft-kill defeat, and hard-kill defeat.

Detection & tracking segment held the largest global drone defense systems market share in 2025, as every drone defense systems response begins with finding the drone early, tracking its movement, and maintaining path before it reaches the protected asset. Without reliable radar, RF sensing, EO/IR tracking, acoustic detection, and passive surveillance, downstream functions such as identification, jamming, interception, or directed-energy defeat become far less effective. As a result, militaries, airport authorities, and critical-infrastructure operators continue to prioritize the detection layer, mainly around airbases, borders, ports, command sites, energy assets, and defense facilities where short warning times can turn a small drone into a serious operational threat.

Hard-kill defeat segment is expected to show the fastest growth, registering a CAGR of 22.4% over the forecast period.

By Threat Type

Due to Low Cost, Easy Availability, and Rapid Field Modification, Small Commercial / Modified Drones Dominated Threat Type Segment

On the basis of threat type, the market is classified into small commercial / modified drones, loitering munitions / OWA-UAS, and drone swarms.

Small commercial / modified drones dominated the global market in 2025, as they are widely available and frequently encountered drone threat across military, homeland-security, airport, border, and critical-infrastructure environments. These drones are low-cost, easy to buy, simple to modify, and can be adapted for reconnaissance, payload dropping, smuggling, perimeter probing, and short-range attacks. Their operational requirement is upfront, even a low-cost commercial drone can force expensive security responses, disrupt airspace, expose troop positions, or threaten a high-value facility. Loitering munitions and swarm threats are growing faster, but small commercial and modified drones remain the largest current threat category as they appear across both conflict zones and civilian-security settings.

Drone swarms segment is expected to show the fastest growth, registering a CAGR of 22.8% over the forecast period.

By Application

Due to Rising Frontline Drone Attacks, Battlefield / Tactical Force Protection Dominated Application Segment

The market is by application is divided into battlefield / tactical force protection, airbase & military installation protection, critical infrastructure protection, border & homeland security, naval & maritime security, airport security, and others.

Battlefield / tactical force protection dominated the market in 2025, as drone threats pose a daily operational risk for troops, convoys, artillery positions, command posts, logistics nodes, and forward operating bases. Defense forces need counter-UAS systems that can move with deployed units, detect low-flying drones early, classify threats quickly, and neutralize them before they expose positions or deliver payloads. This has pushed the market beyond static base protection toward mobile, layered, and battlefield-ready systems combining radar, RF sensing, EO/IR tracking, electronic warfare, interceptors, and command-and-control integration.

In February 2024, the U.S. Army announced a USD 75.00 million rapid acquisition contract with RTX Corporation for 600 Coyote 2C counter-UAS interceptors in direct support of the U.S. counter-UAS mission.

Naval & maritime security segment is expected to show the fastest market growth, registering a CAGR of 23.0% over the forecast period.

By End User

Due to Frontline Force Protection and Air-Defense Modernization, Military / Defense Forces Dominated End-User Segment

Based on end user, the market is segmented into military / defense forces, critical infrastructure, homeland security & law enforcement, and others.

The military / defense forces segment led the market in 2025, considering the emerging threats to mobility, security, air defense, protection of convoys, naval vessels, and command centres. The military and other defense forces require counter-drone systems for deployment in stationary locations, mobile formations, and even combat zones, thus becoming the largest market segment due to urgency and high priority requirements. As compared to non-military organizations, defense sectors also have more power to adopt more advanced and complex active defeating technologies including electronic warfare.

Others segment is expected to show the second fastest market growth, registering a CAGR of 16.0% over the forecast period.

Drone Defense Systems Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Drone Defense Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share for drone defense systems solutions, and is anticipated to grow at a CAGR of 14.5% over the forecast period. North America is supported by the U.S. having the most sophisticated counter-UAS procurement ecosystem covering military bases, deployed forces, border security, homeland facilities, airports, and critical infrastructure. The region benefits from high defense budgets, fast acquisition pathways, mature prime contractors, and a high level of testing of layered detect-track-defeat systems. North America also leads in the integration of radar, RF sensors, EO/IR systems, command-and-control, kinetic interceptors, electronic warfare, and low-collateral defeat options into operational counter-UAS architectures.

In February 2024, the U.S. Army announced a USD 75.00 million rapid acquisition contract with RTX Corporation for 600 Coyote 2C counter-UAS interceptors in support of the U.S. counter-UAS mission.

U.S. Drone Defense Systems Market

Based on the strong contribution of North America to the market and the dominance of U.S. within the region, the U.S. market stood at around USD 1.89 billion in 2025, growing at a CAGR of 14.2% during the forecast period.

Europe

Europe market is anticipated to grow at a second fastest pace with registering a CAGR of 17.5% during the forecast period. Europe market is driven by the Russia-Ukraine war, NATO eastern-flank readiness, mobile force & airbase protection, and critical infrastructure defense. The Europe market demand is no longer limited to fixed military-site protection, it is shifting toward battlefield C-UAS, vehicle-mounted systems, hard-kill defeat, and interoperable NATO architectures. Ukraine has accelerated Europe’s learning curve by exposing how FPV drones, loitering munitions, OWA-UAS, and drone-enabled targeting can reshape battlefield operations. NATO’s September 2024 C-UAS interoperability exercise included Ukraine for the first time and brought together 450 participants from 19 Allied Nations and three partner nations, which supports Europe’s move toward integrated and interoperable counter-drone systems.

France Drone Defense Systems Market

France market reached approximately USD 0.16 billion in 2025, equivalent to around 9.00% of Europe revenues.

Asia Pacific

Asia Pacific is anticipated to grow at a CAGR of 18.8% over the forecast period. Asia Pacific region is led by China, India, Japan, South Korea, Australia, Taiwan, and key maritime states in Southeast Asia. The region’s demand is shaped by airbase hardening, border security, island defense, naval modernization, port security, and protection of critical infrastructure. China leads by scale, while India, Japan, and Australia are becoming more visible procurement-led markets. In April 2026, Australia is set to allocate approx. USD 5.00 billion for counter-drone defense over the next decade.

China Drone Defense Systems Market

The Chinese market revenues stood at around USD 0.45 billion in 2025, representing roughly 33.24% of the global sales.

India Drone Defense Systems Market

The Indian market stood at around USD 0.23 billion in 2025, accounting for roughly 16.86% of Asia Pacific revenues.

Rest of the World

Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a 15.7% CAGR during the forecast period. The Middle East is the strongest demand center due to drone threats against airbases, oil-and-gas assets, ports, naval facilities, borders, and strategic infrastructure. The region is also moving quickly toward active defeat systems, including hard-kill and directed-energy solutions, as soft-kill-only protection is not enough against loitering munitions, OWA-UAS, and coordinated attacks.

Latin America Drone Defense Systems Market

The market in Latin America reached around USD 0.17 billion, accounting for roughly 15.72% of revenues in 2025.

Middle East & Africa Drone Defense Systems Market

Africa market stood at around USD 0.89 billion in 2025 and is expected to reach USD 3.40 billion in 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players are Competing Around Layered, Software-Enabled Counter-UAS Architectures to Expand Market Share

The global market is led by major players such as RTX/Raytheon, Thales, Leonardo, Rafael, MBDA, Northrop Grumman, Lockheed Martin, Hensoldt, and Saab. These companies are moving beyond standalone jammers and sensors toward integrated systems that combine radar, RF detection, EO/IR tracking, C2 software, electronic warfare, interceptors, and directed-energy solutions. RTX/Raytheon’s Coyote interceptor and KuRFS radar reflect this shift toward complete detect-and-defeat architectures for both fixed-site and mobile deployments.

Specialist companies such as Anduril Industries, D-Fend Solutions, DroneShield, Dedrone by Axon, Sentrycs, CERBAIR, and Fortem Technologies are strengthening competition with faster innovation in autonomy, AI-based classification, RF cyber takeover, passive detection, and modular deployment. Rafael’s DRONE DOME, Thales-CS GROUP’s PARADE, and Anduril’s Counter-UAS family show that market leadership now depends on integration depth, software upgradeability, low-collateral defeat, and the ability to support battlefield, fixed-site, vehicle-mounted, and shipborne operations.

LIST OF KEY DRONE DEFENSE SYSTEMS COMPANIES PROFILED IN REPORT

- RTX Corporation / Raytheon (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

- MBDA (France)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Israel Aerospace Industries Ltd. (Israel)

- HENSOLDT AG (Germany)

- Saab AB (Sweden)

- Rheinmetall AG (Germany)

- Anduril Industries, Inc. (U.S.)

- DroneShield Limited (Australia)

- D-Fend Solutions AD Ltd. (Israel)

- Dedrone by Axon Enterprise, Inc. (U.S.)

- Fortem Technologies, Inc. (U.S.)

- Sentrycs Ltd. (Israel)

- CERBAIR SAS (France)

- QinetiQ Group plc (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: The Australian Government announced that it would allocate approximately USD 4.85 billion, for counter-drone defense under the Integrated Investment Program over the next decade. The investment aims to strengthen the Australian Defense Force’s ability to counter UAV threats at home and abroad.

- January 2026: Kongsberg Defense & Aerospace won a contract worth approximately USD 1.66 billion, to deliver 18 SAN CUAS counter-UAS batteries to Poland. The systems include multiple effectors such as guns, missiles, interceptor drones, and other means to counter aerial threats.

- December 2025: The Israel Ministry of Defense and Rafael Advanced Defense Systems delivered the first operational Iron Beam high-power laser system to the IDF. The system is designed to counter aerial threats including UAVs, rockets, and mortars.

- November 2025: The U.K. Ministry of Defense awarded MBDA a contract worth approximately USD 416.80 million, to deliver DragonFire laser systems to the Royal Navy from 2027.

- June 2025: India’s Ministry of Defense concluded emergency procurement contracts worth approximately USD 230.65 million. The package included Integrated Drone Detection and Interdiction Systems, low-level lightweight radars, VSHORADS, RPAVs, loitering munitions, and other mission-critical systems for the Indian Army.

- July 2024: South Korea’s Defense Acquisition Program Administration started mass production of the Laser-Based Anti-Aircraft Weapon Block-I after signing a production contract with Hanwha Aerospace in June 2024. The contract value was approximately USD 72.00 million.

- January 2024: The U.S. Army awarded RTX Corporation a USD 75.00 million rapid acquisition contract for the production of 600 Coyote 2C counter-UAS interceptors. The contract supported the U.S. counter-unmanned aircraft systems mission and strengthened fixed-site and mobile drone defeat capability.

- April 2022: The French defense procurement agency DGA notified the Thales and CS GROUP consortium for the PARADE drone countermeasures programme. The programme worth approximately USD 35.74 million, a total programme budget of approximately USD 379.07 million, over 11 years.

REPORT COVERAGE

The global drone defense systems market analysis provides an in-depth study of market size, market segmentation, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry expert’s developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.6% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

By Segmentation |

By Platform

|

|

By Component

|

|

|

By Technology

|

|

|

By Threat Type

|

|

|

By Application

|

|

|

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value is expected to stand at USD 7.36 billion in 2026 and is projected to reach USD 25.19 billion by 2034.

In 2025, the North America’s market value stood at USD 2.03 billion.

The market is expected to exhibit a CAGR of 16.6% during the forecast period.

Fixed / site-based segment led the market by platform.

Rising battlefield drone attacks are driving urgent drone defense systems procurement.

Key players in the market include RTX Corporation / Raytheon, Lockheed Martin Corporation, Northrop Grumman Corporation, Thales Group, Leonardo S.p.A., Rafael Advanced Defense Systems Ltd., Israel Aerospace Industries Ltd., HENSOLDT AG, Saab AB, Rheinmetall AG, Anduril Industries, DroneShield Limited, D-Fend Solutions, Dedrone by Axon, and Fortem Technologies.

North America held the largest share in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us