Humanoid Robot Market Size, Share & Industry Analysis, By Motion Type (Biped and Wheel Drive), By Component (Hardware and Software), By Application (Industrial, Household, and Services), and Regional Forecast, 2026-2034

Humanoid Robot Market Size

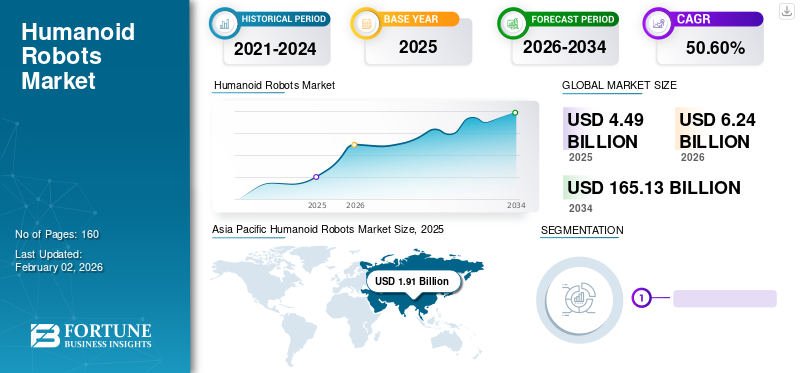

The global humanoid robot market size was valued at USD 4.89 billion in 2025 and is projected to grow from USD 6.24 billion in 2026 to reach USD 165.13 billion by 2034, exhibiting a CAGR of 50.60% during the forecast period. Asia Pacific dominated the humanoid robot market with a market share of 42.60% in 2025.

The Humanoid Robot industry ecosystem includes actuator manufacturers, advanced sensor suppliers, artificial intelligence (AI) software developers, semiconductor providers, system integrators, and end-user enterprises. Hardware currently represents the majority of value capture due to actuator complexity, battery density requirements, and precision control systems. However, software differentiation is increasingly shaping long-term market share distribution.

The market trends indicate strong investor interest but selective enterprise procurement behavior. Organizations are prioritizing measurable productivity gains over experimental deployments. Cost per unit remains a central determinant of adoption velocity, particularly for industrial buyers evaluating the total cost of ownership versus conventional automation systems.

Over the forecast period, the market growth is expected to accelerate as component costs decline, AI training datasets expand, and battery density improves. However, commercialization timelines will vary by application. Industrial and service deployments are likely to precede household adoption, which remains constrained by price sensitivity and safety considerations.

A humanoid robot is a type of robot whose shape resembles a human body. Presently, humanoid robots are in the early stages of development; however, a few have progressed from the research and development stage in the last few years, entering the real world for various applications, such as research, space exploration, personal assistance, caregiving, education, and entertainment, among others.

Building a humanoid robot requires a combination of various engineering disciplines, including electrical engineering, mechanical engineering, and software engineering. The humanoid robot market growth is mainly driven by rapid technological advancements, a reduction in hardware cost, labor shortages in developed countries, and robust government support for robotics. For instance,

- In August 2023, the Beijing Municipal Bureau of Economy and Information Technology announced a USD 1.4 billion robotics fund to advance robotics development in the city. This fund is planned to be used to augment the latest innovations in robotics technology, develop commercial breakthroughs, and finance mergers and acquisition activities within the robotics industry.

- In December 2022, the Government of Canada announced a USD 30 billion investment in Sanctuary Cognitive Systems Corporation, a Vancouver-based company that builds general-purpose humanoid robots.

The COVID-19 pandemic had a positive impact on the global humanoid robot market. The outbreak acted as a catalyst for the robotics industry, further strengthening its widespread adoption and integration across various industries, including the healthcare industry. Various healthcare facilities deployed humanoid robots to monitor patients, sanitize hospitals, and help frontline workers minimize their exposure to the virus. In addition, increased automation due to labor shortages and the need for social distancing further augmented the demand for humanoid robots.

Download Free sample to learn more about this report.

Humanoid Robot MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.89 Billion

- 2026 Market Size: USD 6.24 Billion

- 2034 Forecast Market Size: Size: USD 165.13 Billion

- CAGR: 50.60% from 2026–2034

- Asia Pacific dominated the humanoid robot market with a 42.60% share in 2025.

- The biped segment is projected to account for a 70.51% market share in 2026.

- The hardware segment is expected to hold a 69.55% market share in 2026.

North American

North America generated USD 1.31 Billion in 2025, representing 29.30% of the global market, and is projected to reach USD 1.86 Billion in 2026.

Europe

Europe reached USD 0.77 Billion in 2025, capturing 17.10% of global revenue, and is estimated to grow to USD 1.03 Billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 1.91 Billion and 42.60% of the global market in 2025 and is projected to reach USD 2.68 Billion in 2026.

U.S.

The market is projected to reach USD 1.16 Billion in 2026, supported by strong investments in AI, robotics R&D, and enterprise adoption.

Japan

The market is projected to reach USD 0.29 Billion in 2026, driven by robotics expertise, government support, and an aging population.

Read More

Market Dynamics

Market Trends

Global Labor Shortage to Augment the Market Growth

According to the European Commission press release in March 2024, EU member states are struggling to find skilled workers. Around 63% of SMEs in the EU noted that they cannot find the talent they require. In addition, as per the Heidelberger Druckmaschinen AG 2023 report, based on skilled and workforce shortages among German SMEs, 92% of respondents noted that they are affected by the skills and workforce shortage and see digital transformation as a means of reducing staff shortages.

Humanoid robot market trends indicate a shift from research prototypes toward commercially viable minimum performance platforms. Early development emphasized anthropomorphic perfection. Current deployments prioritize task efficiency, balance reliability, and cost optimization over aesthetic realism.

A notable trend involves embodied artificial intelligence integration. Developers are embedding multimodal large language models into robotic control stacks. This enables contextual understanding, adaptive task sequencing, and improved human-robot interaction in enterprise settings. Such capabilities influence long-term market share distribution by differentiating software maturity levels.

Another emerging pattern is modular hardware architecture. Manufacturers are designing interchangeable limbs, actuator units, and battery systems. This reduces maintenance downtime and lowers lifecycle costs. Enterprises increasingly demand serviceability and scalability rather than bespoke hardware configurations. Capital deployment strategies are also evolving. Large technology corporations are investing directly in robotics manufacturing ecosystems rather than relying solely on startup innovation. Vertical integration improves supply security and intellectual property control.

Pilot programs in automotive assembly, warehouse logistics, and electronics manufacturing are expanding. These programs emphasize repetitive handling, inspection, and support tasks rather than complex fine motor assembly.

Labor shortages are a significant driver of the market, influencing demand across various industries. Humanoid robots offer the opportunity to address manual labor shortages by increasing and assisting the prevailing labor force. Manufacturing companies are increasingly opting for robotics solutions to address the labor shortages. For instance,

- In 2024, luxury vehicle automotive companies Mercedes-Benz and BMW announced plans to deploy humanoid robots in their production plants to help with workforce shortages, improve productivity, and control quality.

Download Free sample to learn more about this report.

Market Drivers

Rapid Technological Advancements to Drive the Market Growth

Advanced technologies, such as Artificial intelligence (AI), High-Performance Computing (HPC), Next-generation sensors, and battery technologies are rapidly maturing and converging to accelerate the development of humanoid robot. AI and HPC enable robots to understand and interact in complex and unstructured real-world environments. The use of AI in robotics helps to manage risk better, improve accuracy, and boost productivity. AI-equipped humanoids can pick and pack objects, utilize vision to transport items autonomously around the factory, and perform maintenance tasks in less time compared to human workers.

Labor scarcity across advanced economies represents a primary structural driver of market growth. Manufacturing, logistics, and warehousing sectors face persistent workforce shortages, increasing enterprise willingness to evaluate physical automation alternatives. Unlike fixed industrial robotic arms, humanoid systems can operate within human-designed environments without major infrastructure redesign. Rising wage inflation further strengthens the economic rationale for automation. Enterprises increasingly model long-term total cost of ownership rather than upfront capital expenditure. Where task repetition, injury risk, or shift variability is high, humanoid deployment economics become comparatively attractive.

Technological progress also supports expansion. Improvements in actuator efficiency, torque density, and sensor fusion capabilities enhance stability and dexterity. Concurrent advances in artificial intelligence models improve object recognition, path planning, and adaptive motion control. These developments reduce operational failure rates and increase enterprise confidence.

Strategic capital investment from technology firms and venture funds accelerates research commercialization. Large language models and reinforcement learning frameworks are being integrated into embodied AI architectures, strengthening task generalization capacity. As training data volumes expand, functional reliability improves. Aging demographics in developed regions create structural demand for service-oriented humanoid solutions. Although near-term adoption remains industrial, demographic pressure supports long-term market size expansion across healthcare and assisted living environments.

In addition, the next-generation sensors, such as 3D/depth cameras, LiDAR, radar, and voice sensors, enable a better understanding of the environment around the robot and allow secure human-robot interaction. These advanced sensors closely imitate the sensory abilities of humans, enabling robots to perform sophisticated tasks. All these factors are anticipated to increase the adoption and drive the market growth during the forecast period.

Market Restraints

Market Acceptance Coupled with Regulatory and Ethical Concerns to Limit the Market Growth

Market acceptance is influenced by a lack of infrastructure and high initial investment, which is expected to limit the growth of the market in the short term. Moreover, negative public perception and ethical concerns also pose significant challenges. As robots become capable of performing complex tasks, they may take over jobs that were once done by humans. This may result in significant job displacement, particularly in the manufacturing industry. According to SEO.ai, around 14% of workers have claimed to have already lost jobs due to robots. Hence, addressing these restraints is crucial to increasing trust in humanoid robots and improving their societal acceptance.

Despite accelerating interest, commercialization remains constrained by cost structure. Current humanoid platforms require high-precision actuators, custom motor assemblies, advanced battery systems, and dense sensor arrays. These components elevate per-unit pricing beyond many enterprise procurement thresholds.

Energy density limitations also restrict operational duration. Battery constraints limit shift-length deployment, reducing cost efficiency relative to stationary robotics. Thermal management complexity further increases maintenance requirements. Safety regulation presents another structural restraint. Humanoid systems operating near human workers must meet stringent safety certification standards. Real-time fail-safe mechanisms, redundancy architectures, and liability frameworks increase engineering and compliance costs.

Software reliability remains under continuous refinement. While artificial intelligence models improve adaptability, edge-case scenarios still require human oversight. Enterprises remain cautious about unsupervised deployment in mission-critical operations. Supply chain concentration adds further uncertainty. Key components, including semiconductors, rare-earth materials, and high-precision gear systems, rely on geographically concentrated production networks. This exposes the Humanoid Robot industry to geopolitical and trade risks.

Market Opportunities

Significant market growth opportunities exist within structured industrial environments. Warehousing and distribution centers present high-potential entry points due to standardized layouts and repetitive workflows. Tasks such as material handling, pallet movement, and inventory transport are conducive to humanoid deployment.

Automotive manufacturing offers another opportunity vector. Humanoid systems can augment human workers in ergonomically challenging roles, reducing injury risk and improving throughput stability. Enterprises evaluating collaborative robotics may view humanoid platforms as flexible alternatives to fixed automation lines.

Defense and hazardous environment applications also represent strategic niches. Inspection, logistics support, and remote operations reduce human exposure to risk. Although volumes remain limited, unit pricing potential is high. Healthcare support services present a longer-term opportunity. Aging populations increase demand for mobility assistance and routine support functions. Regulatory clearance and safety validation will determine commercialization speed.

Market Segmentation Analysis

By Motion Type Analysis

Diverse Business Applications of Biped Humanoid Robots to Fuel the Market Growth

Based on the motion type, the market is segmented into biped and wheel drive.

Biped

The biped segment is predicted to hold the highest share of the humanoid robot market during the forecast period, driven by its wide application across healthcare, entertainment, education, and research, as well as manufacturing and maintenance, accounting for a 70.51% market share in 2026. Robots offer numerous advantages in the healthcare industry as they can help doctors perform various tasks without worrying about their patients during surgery or treatment sessions. Patient care assistants (PCAs) are another typical use case for humanoids. Robots can perform tasks such as taking vital signs and giving medication while also giving emotional support through conversation or touch-based interactions with patients. In the manufacturing industry, a humanoid robot is capable of performing repetitive assembly line work with precision and consistency.

Biped humanoid systems represent the most technologically complex segment within the market. These platforms are engineered to replicate human locomotion, enabling compatibility with infrastructure originally designed for human workers. Stairs, narrow corridors, uneven surfaces, and standard tool interfaces can be navigated without environmental redesign. This compatibility is frequently cited as a core strategic rationale by enterprise buyers evaluating long-term automation pathways.

However, biped systems involve significant engineering complexity. High-torque actuators, advanced balance algorithms, inertial measurement units, and real-time motion stabilization systems increase hardware costs. As a result, biped robots currently command premium pricing relative to alternative mobility formats. The capital intensity of production limits immediate large-scale deployment, restraining near-term market share for this segment.

From an adoption standpoint, biped robots are primarily deployed in pilot environments where flexibility outweighs cost sensitivity. Automotive assembly lines, electronics manufacturing, and structured logistics hubs are early testbeds. Enterprises in these sectors value mobility, versatility, and the potential to redeploy systems across multiple task categories. Technological advances in reinforcement learning and simulation-based training have improved gait stability and recovery from perturbations. This has strengthened enterprise confidence in operational reliability. Nevertheless, failure tolerance thresholds remain stringent in industrial settings.

Wheel Drive

The wheel drive segment is expected to grow with the highest CAGR during the forecast period, owing to its enhanced mobility, lower development costs, and user-friendly interaction compared to biped robots. Wheel drive robots are less complex than bipedal ones, resulting in lower maintenance and repair costs. Wheel-drive humanoid configurations provide a pragmatic alternative to full biped locomotion. These systems retain anthropomorphic upper-body manipulation capabilities while substituting complex leg mechanisms with wheeled mobility bases. This approach significantly reduces mechanical complexity, actuator requirements, and energy consumption.

For enterprise buyers focused on return-on-investment validation, wheel-drive platforms often present a lower-risk entry point. Warehousing, indoor logistics, and structured industrial facilities with flat flooring environments are well-suited to this configuration. Stability is inherently higher, and battery efficiency is superior due to reduced dynamic balancing requirements.

Cost efficiency positions wheel-drive systems as early commercial leaders in the market growth cycle. Lower manufacturing costs improve scalability and support broader pilot expansion. In many enterprise evaluations, mobility perfection is less critical than uptime reliability and task repetition consistency. From a market share perspective, wheel-drive units are expected to dominate early revenue capture within B2B deployments. Their predictable operating environment reduces certification hurdles and integration risk.

However, wheel-drive systems face limitations in environments requiring stair climbing or highly irregular terrain navigation. As a result, their long-term addressable market may be narrower than that of biped platforms.

By Component Analysis

Rapid Advancements in Software Technologies to Augment the Segment Growth

Based on the component, the market is divided into hardware and software.

Hardware

The hardware segment is predicted to hold the highest share of the humanoid robots market during the forecast period, as hardware components play a critical role in determining the performance and functionality of humanoid robots, accounting for a 69.55% market share in 2026. The robot needs sensorimotor skills to function in human mode and engage in human-to-human interactions. To regulate its motions, monitor its condition, and prevent collisions with people or objects in its environment, the humanoid robot needs to be equipped with actuators and a variety of sensors.

Hardware represents the dominant value layer within the current market. Core components include actuators, servo motors, gear assemblies, control boards, battery systems, structural frames, and sensor arrays. High torque-to-weight ratios and durability standards significantly influence system cost and performance reliability.

Actuator technology is particularly central. Precision joint control determines balance stability, dexterity, and task adaptability. Enterprises evaluating procurement assess hardware durability under repetitive industrial stress. Component failure rates directly affect the total cost of ownership models.

Battery systems represent another strategic hardware variable. Energy density constrains operational shift length, influencing productivity calculations. Thermal management requirements further shape enclosure design and maintenance intervals. Improvements in lithium-ion chemistry and solid-state battery research may meaningfully impact market growth trajectories.

Software

The software segment is expected to grow with the highest CAGR during the forecast period on account of the advancements in software technologies. These advancements enable robots to perform complex tasks and operate remotely. Over the past few years, software development for humanoid robots has produced valuable insights into handling complexity and developing research projects. In a humanoid robot, the layer software plays a crucial role in the processing of massive amounts of data collected from multiple sensors.

Software is emerging as the primary differentiation layer within the Humanoid Robot industry. While hardware enables mobility and manipulation, software determines adaptability, learning efficiency, and enterprise integration capability.

Core software stacks include perception modules, motion planning algorithms, reinforcement learning models, object recognition systems, and fleet management platforms. Advances in multimodal artificial intelligence have strengthened contextual reasoning and task sequencing. This enhances humanoid functionality beyond pre-programmed routines.

Embodied AI architectures allow robots to interpret visual input, linguistic instructions, and environmental constraints simultaneously. Integration of large language models into robotic control systems has improved human-robot collaboration potential. However, enterprise deployment still requires domain-specific fine-tuning.

From a market growth standpoint, recurring revenue models tied to software licensing may become significant. Fleet analytics platforms enable predictive maintenance, performance monitoring, and remote updates. These services increase lifecycle value beyond initial hardware sales.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Advanced Capabilities of Humanoid Robots to Increase Their Adoption in Industrial Settings

Based on the application, the market is divided into industrial, household, and services.

Industrial

The industrial application is predicted to grow with the highest CAGR during the forecast period. These robots are increasingly being adopted into industrial applications owing to their ability to perform complete tasks with precision and efficiency. Robots can be used to inspect products for any irregularities and ensure quality standards as they are equipped with advanced vision systems. They can work continuously without breaks, increasing factory productivity and quality. In addition, a humanoid robot can handle hazardous materials and perform dangerous tasks. Owing to all these capabilities, their use is anticipated to increase over the forecast period.

Industrial deployment represents the most immediate commercial driver of the market growth. Enterprises within the manufacturing, warehousing, and logistics sectors face structural labor shortages and rising wage pressures. These factors strengthen the economic rationale for automation investments that can operate within existing human-centric infrastructure. Humanoid platforms offer flexibility advantages compared to fixed robotic arms. They can navigate factory floors, manipulate tools designed for human operators, and transition between task categories without major layout redesign. This adaptability is central to long-term market size expansion within B2B environments.

Early industrial use cases concentrate on material handling, component transfer, inspection support, and repetitive support functions rather than precision assembly. Enterprises prioritize measurable productivity gains and safety improvements. Injury reduction and ergonomic risk mitigation contribute to return-on-investment justification. Procurement decisions typically involve phased pilot programs followed by incremental scaling. Industrial buyers emphasize uptime reliability, integration compatibility, and maintenance predictability. Total cost of ownership modeling remains rigorous.

Household

Household deployment remains technologically feasible but commercially constrained. Price sensitivity, safety certification requirements, and limited high-value use cases restrict near-term market growth in residential settings.

Unlike industrial buyers, household consumers prioritize affordability, ease of maintenance, and intuitive interaction. Current humanoid platforms remain cost-prohibitive for mainstream residential adoption. Furthermore, safety assurance standards are significantly stricter in domestic environments with children and vulnerable populations.

Functional use cases such as cleaning, lifting assistance, or home maintenance overlap with existing appliance or robotic vacuum solutions. This reduces immediate differentiation value. Consequently, the household segment contributes minimally to the current market size. However, long-term demographic shifts, including aging populations and single-person households, may expand demand for physical assistance systems. If manufacturing scale reduces unit cost substantially, household adoption could represent a future growth layer.

The services segment is predicted to hold the highest share of the humanoid robot market during the forecast period, driven by increasing adoption of humanoid robots in service applications due to their human-like appearance and ability to interact naturally with people, accounting for a 49.52% market share in 2026.

Service-oriented applications occupy a middle ground between industrial and household segments. Potential deployments include hospitality support, retail assistance, healthcare facility logistics, and facility management tasks. Unlike industrial environments, service settings involve dynamic human interaction. This increases complexity in perception, communication, and safety protocols. Nonetheless, labor shortages in hospitality and care sectors strengthen the exploration of humanoid alternatives.

Hospitals and eldercare facilities may adopt humanoids for non-clinical support tasks such as transport of supplies, sanitation assistance, and mobility support. In retail environments, robots may assist with inventory movement or customer guidance under supervised conditions. From a market trends perspective, service applications will likely scale gradually through structured pilot programs. Regulatory oversight and liability considerations will shape the commercialization pace.

REGIONAL INSIGHTS

Geographically, the humanoid robots market is studied across five major regions, including North America, South America, Europe, the Middle East & Africa, and the Asia Pacific. They are further categorized into countries.

Asia-Pacific Humanoid Robot Market Analysis

Asia Pacific Humanoid Robots Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 42.60% of the global market, reaching a valuation of USD 1.91 billion, and is projected to grow to USD 2.68 billion in 2026, owing to the presence of major players, supportive government initiatives and investments, an aging population, and a robust robotics culture. China, Japan, and South Korea represent the world's leading industrial robotics markets. According to the International Federation of Robotics (IFR), China recorded 290,300 units of annual installations of industrial robots in 2022, with a 52% market share, followed by Japan, which recorded 50,400 units. There is a high number of start-ups working on robotics technologies in these countries. The Indian market is projected to reach USD 0.11 billion by 2026.

Asia-Pacific is positioned as the fastest-scaling region in the market, driven by manufacturing concentration and robotics ecosystem maturity. Labor shortages in developed Asian economies accelerate industrial automation demand. Government-backed innovation programs strengthen funding pipelines. Supply chain integration advantages support cost optimization. Regional manufacturers are likely to capture an increasing global market share.

Japan Humanoid Robot Market

Japan maintains historical leadership in robotics research and humanoid development. Aging demographics create structural incentives for service-oriented applications. Industrial manufacturers evaluate humanoids for flexible automation. Government support enhances research continuity. Although commercialization remains selective, Japan’s expertise in actuator engineering and precision robotics reinforces long-term market growth prospects. The Japanese market is projected to reach USD 0.29 billion by 2026.

China Humanoid Robot Market

China demonstrates aggressive investment in the Humanoid Robot industry aligned with its industrial automation and artificial intelligence strategy. Domestic manufacturers are rapidly scaling hardware production capabilities. Government-backed initiatives accelerate commercialization testing. Cost optimization and supply chain integration may enhance global competitiveness. China’s industrial demand base positions it as a major contributor to the future market size expansion. The Chinese market is projected to reach USD 1.41 billion by 2026.

In 2023, the Government of China set an ambitious goal to develop humanoid robots by 2025, nurturing companies to focus on humanoid robots, strengthen international cooperation on robotics, and develop a reliable industry supply chain. All these factors are anticipated to augment the humanoid robots market growth in this region.

To know how our report can help streamline your business, Speak to Analyst

North America Humanoid Robot Market Analysis

North America accounted for USD 1.31 billion in 2025, representing 29.30% of the global market share, and is projected to reach USD 1.86 billion in 2026. The U.S. leads this region due to the robust academic research and industry innovation. In addition, significant investment in Research & Development (R&D) by government agencies, private companies, and academic institutions further fuels the market growth. The U.S. market is projected to reach USD 1.16 billion by 2026.

North America represents a leading commercialization hub within the market due to strong venture capital inflows and advanced automation adoption across logistics and manufacturing sectors. Labor cost inflation strengthens investment justification. Technology ecosystem maturity supports AI integration and hardware innovation. Enterprise pilots are expanding gradually, reinforcing regional market growth potential despite regulatory scrutiny surrounding safety standards and workforce displacement concerns.

United States Humanoid Robot Market

The United States dominates the regional market size, driven by advanced robotics startups and large technology firms investing in embodied artificial intelligence. Industrial and warehouse pilots are scaling cautiously. Defense and research institutions contribute additional funding support. Adoption remains enterprise-led rather than consumer-driven. Strong semiconductor and AI infrastructure ecosystems enhance competitive positioning within the global Humanoid Robot industry.

Europe Humanoid Robot Market Analysis

The Europe market was valued at USD 0.77 billion in 2025, capturing 17.10% of global revenue, and is estimated to reach USD 1.03 billion in 2026. The European market is primarily driven by labor shortages, increasing labor costs, rising automation in the manufacturing sector, innovation in robotics hardware, such as sensors, actuators, and materials, supportive government policies, and an aging population. Additionally, strong investments in R&D, integration of AI-enabled robotics, and increasing adoption across healthcare, logistics, and service industries are further supporting market growth in the region.

Europe demonstrates steady market growth supported by advanced manufacturing clusters and structured regulatory frameworks. Automotive and industrial automation sectors represent early adopters. Labor protection regulations influence integration strategies. Research collaboration between universities and robotics firms strengthens innovation pipelines. However, cost sensitivity and conservative enterprise procurement practices moderate rapid market share expansion across several European economies.

Germany Humanoid Robot Market

Germany serves as a strategic industrial testbed within the market due to its automotive manufacturing leadership and engineering specialization. Enterprises evaluate humanoids for ergonomic task support and production flexibility. Integration with Industry 4.0 infrastructure enhances experimentation. Regulatory compliance and worker council involvement shape adoption timelines, influencing gradual but structured market growth. The German market is projected to reach USD 0.2 billion by 2026.

United Kingdom Humanoid Robot Market

The UK market is projected to reach USD 0.08 billion by 2026. The United Kingdom market benefits from strong artificial intelligence research and robotics innovation clusters. Adoption is concentrated in pilot deployments within logistics and research institutions. Venture capital participation supports early-stage platform development. Commercial scaling remains measured due to cost constraints and enterprise risk assessment frameworks. Long-term growth aligns with service-sector automation demand.

Middle East & Africa Humanoid Robot Market Analysis

Middle East & Africa contributed approximately USD 0.27 billion to the global market in 2025, accounting for 6.10% share, and is expected to reach USD 0.37 billion in 2026. In the Middle East & Africa region, the gradual shift towards automation is predicted to offer opportunities for market growth. Government-led smart city initiatives, investments in industrial automation, and growing interest in robotics for healthcare, hospitality, and security applications are expected to influence market expansion positively.

Middle East and Africa markets exhibit selective experimentation within logistics, research institutions, and government innovation initiatives. Adoption remains limited by infrastructure maturity and capital prioritization. However, smart city programs and industrial diversification strategies could support gradual market growth in targeted sectors over the forecast horizon.

Latin America Humanoid Robot Market Analysis

Latin America represents an emerging but limited segment of the market. Adoption remains constrained by capital availability and industrial automation maturity. Pilot experimentation occurs primarily within multinational manufacturing facilities. Price sensitivity influences procurement decisions. Long-term market growth may depend on declining hardware costs and increasing regional investment in advanced manufacturing infrastructure.

South America

In South America, there is a growing awareness regarding robotics and interest from various sectors to increase the adoption. Expanding manufacturing activities, modernization of industrial processes, and rising investments in automation technologies are further contributing to the growth of the humanoid robot market in the region.

The South America market accounted for USD 0.22 billion in 2025, representing 5.00% of the global industry, and is expected to reach USD 0.3 billion in 2026.

Humanoid Robot Industry Competitive Landscape

Key Players Focused on Strengthening Their Market Position with Continuous Developments

The global humanoid robots market is consolidated by leading players such as PAL Robotics, Figure, Agility Robotics, Honda Motor Co., Ltd., Toyota, Boston Dynamics, Hanson Robotics, Sanctuary Cognitive Systems Corporation, NVIDIA Corporation, and Tokyo Robotics Inc., among others. These companies are expanding their operations by adopting strategies such as mergers, acquisitions, product launches, collaborations, and partnerships.

The market remains concentrated among a limited number of technology firms, advanced robotics startups, and diversified industrial automation companies. Competitive positioning is currently shaped less by volume production and more by technological differentiation, capital strength, and ecosystem integration capabilities.

Capital intensity remains a barrier to entry. Scaling humanoid production requires significant investment in precision manufacturing, safety certification, and AI model training infrastructure. As a result, early market share is concentrated among well-funded entities. Strategic partnerships are expanding across semiconductor suppliers, battery technology developers, and enterprise pilot customers. These collaborations accelerate commercialization validation and reduce engineering iteration cycles.

Pricing strategy remains fluid. Few companies have achieved mass production scale; therefore, per-unit costs remain elevated. Over time, component standardization and production learning curves may reshape the market share distribution toward firms capable of industrial-scale manufacturing.

List of Top Humanoid Robots Companies:

- PAL Robotics (Spain)

- Figure (U.S.)

- Agility Robotics (U.S.)

- Honda Motor Co., Ltd. (Japan)

- Toyota (Japan)

- Boston Dynamics (U.S.)

- Hanson Robotics (China)

- Sanctuary Cognitive Systems Corporation (Canada)

- NVIDIA Corporation (U.S.)

- Tokyo Robotics Inc. (Japan)

KEY INDUSTRY DEVELOPMENTS IN THE HUMANOID ROBOT MARKET:

- February 2025: Apptronik Inc. initiated industrial collaboration programs targeting manufacturing assembly augmentation. The purpose was to refine ergonomic task automation and increase uptime reliability in factory environments. Technologies incorporated included modular actuator systems, advanced torque sensors, and adaptive manipulation algorithms.

- May 2025: Unitree Robotics Co. Ltd. introduced upgraded humanoid prototypes emphasizing cost-efficient actuator assemblies and improved mobility control. The initiative sought to lower hardware entry barriers and accelerate pilot expansion in emerging markets. Capabilities highlighted included high-torque electric motors, integrated sensor fusion systems, and AI-based gait optimization software.

- June 2024: Elon Musk, CEO of Tesla Motors, confirmed that Tesla could sell its humanoid robot “Optimus” by the end of 2025 and predicted that it could drive Tesla’s valuation to USD 25 trillion.

- June 2024: The Institute of Electrical and Electronics Engineers (IEEE), a technical professional organization, announced the launch of a study group to explore the current humanoid landscape and develop robot standards that organizations can follow. This group is open to others across academia, government agencies, and industry.

- April 2024: Boston Dynamics, an American robotics design company, unveiled the latest version of the Atlas humanoid robot in a new video. This robot is fully electric, stronger, and agile compared to its retired predecessor.

- April 2024: Sanctuary Cognitive Systems Corporation, a humanoid robot developer, and Magna International, a mobility technology firm, announced a partnership to advance the development of humanoid robots for automotive manufacturing. This partnership includes a thorough review aimed at enhancing the cost and scalability of humanoid robots using Magna's automotive product portfolio, engineering, and manufacturing capabilities.

- March 2024: Figure, a humanoid robot maker, partnered with OpenAI, an AI research and deployment organization, to integrate OpenAI’s AI systems into humanoid robots developed by Figure.

REPORT COVERAGE

The report offers qualitative and quantitative insights into the market and a detailed analysis of the size & growth rate for all possible segments in the market. It also provides an elaborate analysis of market dynamics, emerging trends, and the competitive landscape. The report offers key insights, such as the implementation of automation in specific market segments, recent industry developments, such as partnerships, mergers, funding, acquisitions, consolidated SWOT analysis of key players, business strategies of leading market players, macro & micro economic indicators, and major industry trends. This detailed analysis provides a comprehensive view of the market and its potential for growth and development.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021– 2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026– 2034 |

|

Historical Period |

2021 – 2024 |

|

Growth Rate |

CAGR of 50.60% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Motion Type

By Component

By Application

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market is predicted to reach USD 165.13 billion by 2034.

In 2025, the market value stood at USD 4.49 billion.

The market is projected to record a CAGR of 50.60% during the forecast period.

The biped is the expected to hold the leading motion type segment in the market.

The rapid technological advancements, labor shortages, aging population, and increasing automation to drive the market growth.

Some of the top players in the market are PAL Robotics, Agility Robotics, Honda Motor Co., Ltd., Toyota, Boston Dynamics, Hanson Robotics, NVIDIA Corporation, and others.

Asia Pacific dominated the humanoid robot market with a market share of 42.60% in 2025.

By component, the software segment is expected to show the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us