Hydrogen Infrastructure Market Size, Share & Industry Analysis, By Infrastructure Type (Compression & Distribution, Pipelines, Ports & Terminals, Storage, and Refueling), By Application (Energy Storage, Mobility, Industrial, and Others), By End User (Port Authorities & Logistics, Utilities, Transportation, Oil & Gas, Manufacturing, and Others), and Regional Forecast, 2026-2034

Hydrogen Infrastructure Market Size and Future Outlook

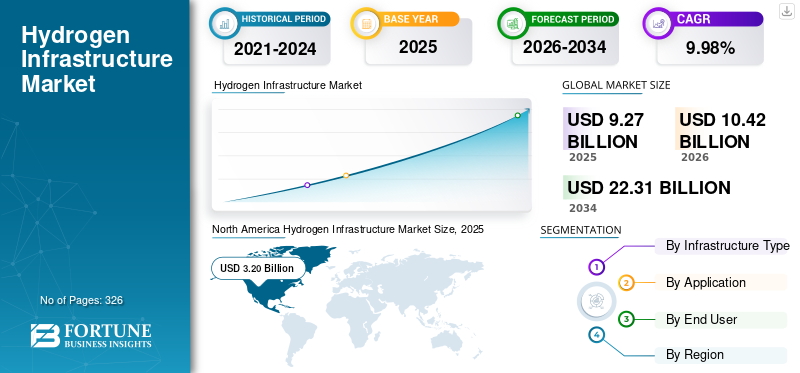

The global hydrogen infrastructure market size was valued at USD 9.27 billion in 2025. The market is projected to grow from USD 10.42 billion in 2026 to USD 22.31 billion by 2034, with a CAGR of 9.98% over the forecast period. North America dominated the hydrogen infrastructure market with a market share of 34.52% in 2025.

Hydrogen infrastructure refers to the network of physical systems and facilities required for the production, transportation, storage, distribution, and utilization of hydrogen as an energy carrier. It includes hydrogen pipelines, storage facilities, refueling stations, compression and liquefaction systems, and import/export terminals used for hydrogen and hydrogen-derived fuels such as ammonia. This infrastructure enables hydrogen delivery across industrial, mobility, power generation, and energy storage applications, supporting decarbonization, renewable energy integration, and the development of a global hydrogen economy.

The growth of the market is primarily driven by increasing global decarbonization targets and the rising adoption of clean energy solutions across industries, transportation, and power generation. Governments worldwide are supporting hydrogen ecosystem development through funding programs, hydrogen strategies, and carbon reduction policies. Expanding investments in green hydrogen & blue hydrogen production, export-import corridors, and hydrogen backbone pipeline networks are further accelerating infrastructure deployment. In addition, growing demand for long-duration energy storage and heavy-duty zero-emission transportation is increasing the need for hydrogen storage, refueling, and distribution infrastructure globally.

Air Liquide, Linde plc, Air Products, Shell, and Snam are among the leading companies in the market. These companies are focused on expanding hydrogen transportation, storage, and distribution networks to support the global energy transition. Most are investing heavily in hydrogen pipelines, liquefaction and compression systems, refueling stations, and import/export terminal infrastructure. They are also forming strategic partnerships with governments, utilities, and industrial players to develop large-scale hydrogen hubs and cross-border hydrogen corridors. Additionally, these firms are leveraging existing gas, industrial, and logistics infrastructure to accelerate commercialization and reduce deployment costs across the hydrogen value chain.

Download Free sample to learn more about this report.

Hydrogen Infrastructure Market Takeaways

- 2025 Market Size: USD 9.27 billion

- 2026 Market Size: USD 10.42 billion

- 2034 Forecast Market Size: USD 22.31 billion

- CAGR: 9.98% from 2026–2034

- North America dominated the hydrogen infrastructure market with a 34.52% share in 2025.

- The pipelines segment held the largest share, accounting for 25.58% of the market in 2025.

- The storage segment is projected to grow at the fastest 11.23% CAGR during the forecast period.

North America

North America led the global market in 2025, reaching USD 3.20 billion and accounting for approximately 34.57% of global revenue.

Europe

Europe accounted for USD 2.28 billion in 2025, representing approximately 24.62% of the global market.

Asia Pacific

Asia Pacific reached USD 2.60 billion in 2025, contributing approximately 28.06% of global market revenues.

U.S.

The market was valued at USD 2.70 billion in 2025 and is projected to reach USD 3.03 billion by 2026.

Japan

The market was valued at USD 0.33 billion in 2025 and is expected to reach USD 0.37 billion by 2026.

Read More

Hydrogen Infrastructure Market Trends

Expansion of Hydrogen Import/Export Terminal Infrastructure to Amplify Market Growth

One of the most significant trends in the market is the rapid development of hydrogen import/export terminals and port-based hydrogen hubs. Countries with abundant renewable energy resources, such as Australia, Saudi Arabia, the UAE, and Chile, are increasingly investing in ammonia and liquid hydrogen export facilities to supply hydrogen-importing economies, including Japan, South Korea, and Germany. According to the International Energy Agency (IEA), more than 130 ports globally are expected to participate in hydrogen trade by 2030. Large-scale projects such as the NEOM green hydrogen project in Saudi Arabia and the Port of Rotterdam hydrogen import hub demonstrate the growing importance of maritime hydrogen logistics. This trend is accelerating investments in liquefaction systems, storage tanks, marine bunkering infrastructure, and ammonia handling terminals. As global hydrogen trade expands, ports are becoming strategic energy transition hubs, positioning terminal infrastructure as one of the fastest-growing segments within the industry.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Government Decarbonization Policies and Hydrogen Strategies to Favor Market Growth

Government-led decarbonization initiatives are a major driver accelerating the growth globally. Many countries have introduced national hydrogen strategies, subsidies, and carbon reduction targets to support clean hydrogen deployment across industry, transportation, and power sectors. The European Union’s REPowerEU plan, for example, targets the production and import of 20 million tonnes of renewable hydrogen annually by 2030. Similarly, the U.S. Inflation Reduction Act introduced production tax credits of up to USD 3/kg for clean hydrogen, significantly improving project economics. These policies are encouraging investments in hydrogen pipelines, storage facilities, refueling stations, and export terminals. In addition, public funding programs are supporting the creation of hydrogen hubs and industrial corridors. Government support reduces investment risk and accelerates commercialization, particularly for infrastructure projects that require large upfront capital. As countries intensify efforts to achieve net-zero emissions, policy-driven infrastructure expansion is expected to remain a primary market growth catalyst.

Market Restraints

High Capital Cost of Hydrogen Infrastructure Development to Limit Market Growth

The high capital intensity associated with hydrogen infrastructure development remains a major restraint for the hydrogen infrastructure market growth. Building hydrogen pipelines, underground storage systems, liquefaction facilities, and export terminals requires substantial upfront investment compared with conventional energy infrastructure. For example, dedicated hydrogen pipelines can cost between USD 1.5 million and USD 4 million per kilometer, depending on pressure levels and terrain conditions. Similarly, large-scale hydrogen export terminals may require investments exceeding USD 1 billion per facility. In many regions, hydrogen demand remains insufficient to guarantee high infrastructure utilization rates, creating uncertainty around return on investment. In addition, financing challenges are amplified by evolving regulations, long project timelines, and limited commercial-scale deployment experience. While some existing natural gas infrastructure can be repurposed for hydrogen use, extensive retrofitting is often necessary due to hydrogen embrittlement and leakage concerns. These high development costs continue to slow infrastructure deployment, especially in emerging economies with limited funding support.

Market Opportunities

Growing Need for Long-Duration Renewable Energy Storage to Create New Growth Avenues

The increasing need for long-duration renewable energy storage presents a major opportunity for the hydrogen infrastructure market. As renewable power generation from wind and solar expands globally, electricity systems require large-scale storage solutions to manage intermittency and seasonal energy balancing. Hydrogen is emerging as a promising long-duration storage medium as it can store excess renewable electricity for weeks or months through power-to-hydrogen systems. According to the IEA, global renewable energy capacity additions continue to rise rapidly, increasing the importance of flexible storage technologies. This creates significant opportunities for underground hydrogen storage caverns, compression systems, hydrogen pipelines, and hydrogen-to-power infrastructure. Europe is advancing several utility-scale hydrogen storage projects linked to renewable integration and grid balancing initiatives. Hydrogen storage can also strengthen energy security by reducing dependence on imported fossil fuels. As renewable penetration increases globally, demand for hydrogen-based storage infrastructure is expected to grow substantially over the coming years.

Market Challenges

Limited Hydrogen Transport and Distribution Network Availability to Limit Market Growth

A major challenge facing the market is the limited availability of dedicated hydrogen transport and distribution networks. Unlike natural gas, hydrogen infrastructure remains highly fragmented and concentrated in a few industrial regions. According to the IEA, only a relatively small portion of the more than 37,000 km of announced hydrogen pipeline projects worldwide has reached final investment decision status. In many countries, hydrogen production sites, industrial users, and refueling locations are not yet connected through integrated transmission systems, increasing transportation costs and limiting scalability. Hydrogen also requires specialized materials and handling systems due to its low volumetric energy density and potential for pipeline embrittlement. As a result, transporting hydrogen through trucks, trailers, or newly built pipelines can be significantly more expensive than existing natural gas logistics. The lack of mature transmission infrastructure slows market development, reduces supply chains' efficiency, and creates uncertainty for investors seeking large-scale commercialization opportunities in the hydrogen economy.

Segmentation Analysis

By Infrastructure Type

Growing Industrial Decarbonization Efforts Led the Pipelines Segment Growth

Based on infrastructure type, the market is segmented into compression & distribution, pipelines, ports & terminals, storage, and refueling.

The pipelines segment accounted for the dominant hydrogen infrastructure market share, holding approximately 25.58% share in 2025. The segment represents one of the most strategically important areas within the market, as pipelines provide large-scale and cost-effective hydrogen transportation between production sites, storage facilities, industrial clusters, and end users. Existing natural gas pipeline networks are increasingly being evaluated for hydrogen repurposing to reduce infrastructure development costs and accelerate deployment timelines. Growing industrial decarbonization efforts and the expansion of hydrogen hubs are increasing the need for interconnected hydrogen transmission systems. Pipeline infrastructure is expected to become increasingly important as hydrogen demand rises across refining, chemicals, steelmaking, power generation, and mobility applications. However, hydrogen transport through pipelines requires specialized materials and engineering solutions, as hydrogen molecules can cause embrittlement and leakage in conventional systems. Despite these technical challenges, pipelines are expected to play a central role in enabling long-term hydrogen market scalability and energy system integration.

Storage is the fastest-growing segment, growing at a CAGR of 11.23% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Increasing Need for Long-Duration Renewable Energy Storage Solutions Boosts the Segment Growth

Based on application, the market is segmented into energy storage, mobility, industrial, and others.

The energy storage segment dominates the market, holding 38.94% of the share due to the increasing need for long-duration renewable energy storage solutions. Hydrogen enables excess electricity generated from renewable sources such as solar and wind to be converted, stored, and later reused for power generation or industrial applications. This segment includes infrastructure related to underground hydrogen storage, compression systems, hydrogen-to-power facilities, and transmission networks supporting energy balancing operations. Growing renewable energy penetration and rising grid instability concerns are increasing the importance of hydrogen-based storage systems for seasonal and utility-scale energy balancing. Hydrogen storage also provides advantages over conventional battery systems for long-duration applications, as it can store energy for weeks or months. As countries accelerate clean energy transitions and strengthen energy security initiatives, investments in hydrogen energy storage infrastructure are expected to increase significantly over the long term.

The mobility is the second-leading segment, growing at a CAGR of 26.09% during the forecast period.

By End User

Rising Investments in Hydrogen Pipelines Propelled the Utilities Segment Growth

Based on end user, the market is segmented into port authorities & logistics, utilities, transportation, oil & gas, manufacturing, and others.

The utilities segment held the largest market share of around 24.18% in 2025, as power companies increasingly integrate hydrogen into energy generation, storage, and transmission systems. This segment includes investments in hydrogen pipelines, underground storage facilities, grid-balancing systems, and hydrogen-to-power infrastructure. Utilities are adopting hydrogen to support renewable energy integration, reduce grid intermittency, and strengthen long-duration energy storage capabilities. Hydrogen is increasingly recognized as a flexible energy carrier capable of storing excess renewable electricity and supplying power during periods of high demand or low renewable generation. Many utility companies are also exploring hydrogen blending within existing natural gas networks and developing hydrogen-ready transmission systems. The segment is expected to experience strong long-term growth as countries accelerate decarbonization efforts and modernize power infrastructure. Utility-led hydrogen infrastructure development is likely to become increasingly important for enabling large-scale renewable integration and improving energy system flexibility.

Manufacturing is the second-leading segment, growing at a CAGR of 9.27% during the forecast period.

Hydrogen Infrastructure Market Regional Outlook

By geography, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Hydrogen Infrastructure Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025, valued at USD 3.20 billion and accounting for approximately 34.57% of the global market share. The region represents a significant market, driven by strong industrial hydrogen demand, expanding hydrogen hub programs, and increasing investments in clean energy transition projects. The region is witnessing substantial growth in hydrogen pipelines, storage facilities, and refueling infrastructure, supported by government incentives and decarbonization policies. Existing oil & gas infrastructure and large industrial clusters provide favorable conditions for hydrogen transportation and distribution network development. Growing focus on long-duration energy storage and heavy-duty transportation is also accelerating infrastructure deployment across the region.

U.S. Hydrogen Infrastructure Market

The U.S. market stood at USD 2.70 billion in 2025 and is expected to reach USD 3.03 billion by 2026. The U.S. is a leading market, supported by large-scale hydrogen hub investments, strong industrial hydrogen demand, and expanding clean energy policies. Growth is being driven by pipeline development, storage infrastructure, and hydrogen mobility initiatives linked to decarbonization and energy security goals.

Europe

Europe accounted for USD 2.28 billion in 2025, representing approximately 24.62% of global market revenues. Europe is one of the most advanced hydrogen infrastructure markets globally, driven by aggressive climate targets, hydrogen backbone initiatives, and large-scale industrial decarbonization efforts. Investments are increasing in hydrogen pipelines, underground storage systems, import terminals, and integrated hydrogen corridors connecting multiple industrial regions. The region is strongly focused on renewable hydrogen integration and strengthening energy security through diversified clean energy infrastructure. Government policy support and cross-border hydrogen transmission planning continue to accelerate infrastructure development across various applications.

Germany Hydrogen Infrastructure Market

Germany stood at USD 0.58 billion in 2025 and is expected to reach USD 0.65 billion by 2026. Germany is one of the most advanced markets globally due to strong investments in hydrogen backbone pipelines, import terminals, and industrial hydrogen networks. The country is prioritizing renewable hydrogen integration and large-scale infrastructure expansion to support industrial decarbonization and energy security.

U.K. Hydrogen Infrastructure Market

The U.K. market was valued at USD 0.34 billion in 2025 and is expected to reach USD 0.38 billion by 2026. The U.K. market is growing through investments in hydrogen-ready gas networks, industrial decarbonization projects, and hydrogen storage systems. The country is also focusing on hydrogen transport corridors and integrating hydrogen into its broader net-zero energy transition strategy.

Asia Pacific

Asia Pacific market was valued at USD 2.60 billion in 2025, accounting for approximately 28.06% of global revenues. Asia Pacific is a rapidly growing market, supported by strong investments in hydrogen mobility, industrial hydrogen utilization, and hydrogen trade infrastructure. The region is witnessing substantial development of hydrogen refueling stations, import terminals, distribution systems, and export-oriented hydrogen projects. Growing energy demand, industrial expansion, and government-backed hydrogen strategies are supporting infrastructure growth across transportation and industrial sectors. Increasing focus on hydrogen-powered mobility and international hydrogen trade is expected to drive long-term infrastructure expansion throughout the region.

China Hydrogen Infrastructure Marke

China remains the dominant contributor in the Asia Pacific region, standing at USD 1.11 billion in 2025 and is expected to reach USD 1.26 billion by 2026. China is a rapidly expanding market, driven by large-scale hydrogen mobility deployment, industrial hydrogen demand, and government-supported clean transportation initiatives. Significant investments are being made in hydrogen refueling stations, industrial distribution systems, and hydrogen transport infrastructure, which will result in the growth of the market during the forecast period.

India Hydrogen Infrastructure Market

India stood at USD 0.29 billion in 2025 and is expected to reach USD 0.33 billion by 2026. India’s market is growing due to rising investments in green hydrogen production, industrial decarbonization, and export-oriented hydrogen projects. Infrastructure development is focused on hydrogen hubs, storage systems, and port-based logistics networks supporting the national hydrogen mission.

Japan Hydrogen Infrastructure Marke

Japan was valued at USD 0.33 billion in 2025 and is expected to reach USD 0.37 billion by 2026. Japan is heavily focused on developing hydrogen import terminals, liquefied hydrogen logistics systems, and hydrogen mobility infrastructure to strengthen long-term energy security. The country is also advancing hydrogen-based power generation and clean transportation infrastructure development to support the renewable energy transition in the country.

Latin America

Latin America accounted for USD 0.69 billion in 2025, representing approximately 7.42% of global revenues. Latin America is emerging as an important market due to its strong renewable energy potential and increasing focus on green hydrogen exports. Investments are primarily concentrated in hydrogen export terminals, ammonia logistics infrastructure, and renewable hydrogen production hubs. The region is benefiting from favorable solar and wind resources that support cost-competitive green hydrogen development. As global hydrogen trade expands, infrastructure development related to export logistics, storage, and port systems is expected to increase steadily across Latin America.

Middle East & Africa

The Middle East & Africa region was valued at USD 0.49 billion in 2025. The Middle East & Africa region is becoming a major market, driven by large-scale hydrogen export ambitions and growing investments in ammonia and hydrogen logistics infrastructure. Countries in the region are focusing on export terminals, storage facilities, and integrated hydrogen hubs to leverage abundant renewable energy resources and existing energy trade expertise. Strong participation from national energy companies and sovereign-backed projects is accelerating infrastructure deployment. The region is expected to play a critical role in future global hydrogen trade due to its strategic geographic position and large-scale project pipeline.

GCC Hydrogen Infrastructure Market

The GCC market stood at USD 0.22 billion in 2025 and is expected to reach USD 0.25 billion by 2026. The GCC region is emerging as a major market, driven by large-scale green hydrogen and ammonia export projects. Investments are concentrated in export terminals, hydrogen logistics infrastructure, storage facilities, and integrated hydrogen hubs, supported by strong government and energy-sector participation.

Competitive Landscape

KEY INDUSTRY PLAYERS

Market Players Focus on Distribution Infrastructure to Support Clean Energy Transition Goals

Air Liquide, Linde plc, Air Products, Shell, and Snam are among the leading players in the market. These companies are commonly focused on expanding hydrogen transportation, storage, and distribution infrastructure to support industrial decarbonization and clean energy transition goals. Their efforts include investments in hydrogen pipelines, liquefaction and compression systems, refueling stations, and import/export terminal infrastructure. They are also actively developing large-scale hydrogen hubs and forming partnerships with governments, utilities, and industrial companies to accelerate hydrogen ecosystem development. Additionally, many of these players are leveraging existing gas and energy infrastructure assets to reduce deployment costs and scale hydrogen commercialization globally.

List of Top Hydrogen Infrastructure Companies Profiled

- Air Liquide (France)

- Linde plc (U.K.)

- Air Products (U.S.)

- Plug Power (U.S.)

- Nel ASA (Norway)

- Chart Industries (U.S.)

- Snam (Italy)

- Gasunie (Netherlands)

- Engie (France)

- Shell (U.K.)

- TotalEnergies (France)

- Kawasaki Heavy Industries (Japan)

- Cummins (U.S.)

- Siemens Energy (Germany)

- ADNOC (UAE)

KEY INDUSTRY DEVELOPMENTS

- September 2025: ADNOC entered strategic agreements with international energy and logistics companies to expand hydrogen export terminals, ammonia logistics infrastructure, and integrated hydrogen supply chain capabilities in the UAE.

- March 2025: Snam signed partnership and financing agreements with European infrastructure stakeholders to accelerate development of the Italian H2 Backbone project and cross-border hydrogen pipeline infrastructure across Europe.

- November 2024: Kawasaki Heavy Industries secured contracts and partnership agreements related to liquefied hydrogen shipping infrastructure and hydrogen terminal development to strengthen international hydrogen transportation networks.

- June 2024: Shell and Equinor expanded their strategic cooperation agreement for low-carbon hydrogen and CCS-linked infrastructure projects, focusing on hydrogen transport, storage, and industrial decarbonization systems.

- May 2024: Air Products, ACWA Power, and NEOM continued major investment and project execution agreements for the NEOM Green Hydrogen Project in Saudi Arabia, supporting large-scale hydrogen production, storage, and ammonia export infrastructure development.

REPORT COVERAGE

The hydrogen infrastructure report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.98% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Infrastructure Type

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 9.27 billion in 2025 and is projected to reach USD 22.31 billion by 2034.

In 2025, the market value stood at USD 3.20 billion.

The market is expected to exhibit a CAGR of 9.98% during the forecast period.

By infrastructure type, the pipelines segment led the market.

Government decarbonization policies and hydrogen strategies are the key factors driving market expansion.

Air Liquide, Linde plc, Air Products, Shell, and Snam are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 326

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us