Hydrogen Energy Storage Market Size, Share & Industry Analysis, By Technology (Compressed Gas Storage, Liquid Hydrogen Storage, Material-Based Storage, and Underground Bulk Storage), By Form (Solid, Liquid, and Gas), By End User (Utilities and Grid Operator, Industrial, Transportation, and Others), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

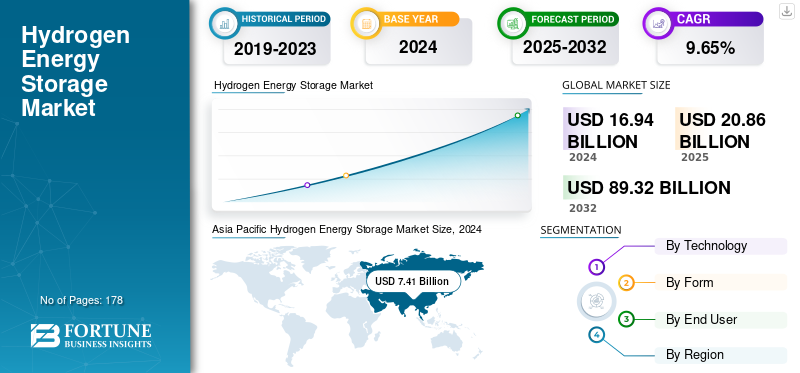

The global hydrogen energy storage market size was valued at USD 16.94 billion in 2024. The market is projected to grow from USD 20.86 billion in 2025 to USD 89.32 billion by 2032, exhibiting a CAGR of 4.58% during the forecast period. Asia Pacific dominated the hydrogen energy storage market with a market share of 43.74% in 2024.

Hydrogen energy storage is a method of storing excess energy by converting it into hydrogen, which can later be used as a clean fuel or to generate electricity. In this system, surplus power, often from renewable sources such as solar or wind, is used to produce hydrogen through processes such as electrolysis. The hydrogen can then be stored in various forms (compressed gas, liquid, or in chemical compounds) and later utilized in fuel cells, combustion engines, or industrial applications when energy demand is higher. This approach helps balance supply and demand in energy systems while supporting the transition to low-carbon energy.

NEL Hydrogen, Linde Plc, Engie, and ITM Power are some of the leading players in the market. Their efforts focus on producing renewable hydrogen through advanced electrolysis technologies and creating reliable, scalable storage systems using high-pressure, cryogenic, and solid-state solutions. These companies invest heavily in integrating hydrogen storage into industrial, mobility, and grid-scale applications, enabling renewable energy balancing and decarbonization of hard-to-abate sectors. Nel ASA plays a pivotal role in the hydrogen energy storage industry as a leading developer of electrolyzer and hydrogen infrastructure technologies. The company focuses on producing green hydrogen through water electrolysis, offering both alkaline and PEM systems that enable large-scale, renewable-based hydrogen generation. Nel also contributes to the storage segment by integrating hydrogen production with modular storage and fueling solutions for industrial, transportation, and energy applications. Its emphasis on efficiency, scalability, and cost reduction supports the broader adoption of hydrogen as an energy carrier.

Download Free sample to learn more about this report.

Hydrogen Energy Storage Market Key Takeaways

- 2024 Market Size: USD 16.94 billion

- 2025 Market Size: USD 20.86 billion

- 2032 Forecast Market Size: USD 89.32 billion

- CAGR: 4.58% from 2025–2032

- Asia Pacific dominated the hydrogen energy storage market with a 43.74% share in 2024.

- The compressed gas storage segment accounted for a 53.46% market share in 2024.

- The industrial segment accounted for a 43.57% market share in 2024.

North America

North America emerged as the second-largest regional market, valued at USD 6.23 billion in 2025.

Asia Pacific

Asia Pacific held a leading market position in 2024, valued at USD 7.41 billion.

Europe

Europe maintained a significant market presence, valued at USD 4.99 billion in 2025.

U.S.

The market valued at USD 5.67 billion in 2025.

Japan

The market valued at USD 1.32 billion in 2025.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Inclination toward Sustainable Energy to Drive the Demand for Hydrogen Energy Storage

The rapid expansion of renewable energy due to the global transition toward sustainable energy is a key driver for hydrogen energy storage. According to the International Energy Agency (IEA), renewable electricity generation is projected to reach 35% of the global total by 2025, led by strong growth in solar and wind capacity. However, these energy sources are inherently intermittent. Solar power only generates electricity during the day, and wind output depends on weather conditions. This mismatch between energy production and demand often results in excess electricity that cannot be used immediately. Hydrogen storage provides a solution by converting surplus renewable electricity into hydrogen through electrolysis. The stored hydrogen can later be converted back to electricity or used directly in various transportation and industrial applications, ensuring that clean energy is not wasted. As more countries commit to ambitious renewable energy targets, the ability of hydrogen storage to balance fluctuating supply and demand is becoming increasingly vital to grid stability and energy security.

Growing Demand for Decarbonization Across Industries to Lead Market Growth

The global shift toward decarbonization is another key driver of hydrogen energy storage. Heavy industries such as steelmaking, cement, and chemicals, along with the transport sector, are among the hardest to decarbonize as they rely heavily on fossil fuels. The International Renewable Energy Agency (IRENA) projects that hydrogen could meet up to 12% of total global energy demand by 2050, highlighting its importance in achieving climate goals. Hydrogen energy storage plays a central role in making this possible by enabling clean hydrogen to be produced at scale and stored for long-term use. For example, hydrogen stored from renewable electricity can power fuel cell trucks, supply industrial furnaces, or serve as feedstock for green ammonia production. This flexibility makes hydrogen storage an indispensable technology for reducing greenhouse gas emissions in sectors where direct electrification is impractical, thereby supporting national and international net-zero targets.

MARKET RESTRAINTS

High Costs of Production and Storage to Constrain Market Growth

One of the biggest challenges for hydrogen energy storage is the high cost of producing and storing hydrogen compared to conventional energy storage methods. Currently, producing green hydrogen through electrolysis remains expensive, mainly as electrolyzers and renewable electricity inputs continue to be costly. According to the International Energy Agency (IEA), the cost of green hydrogen in 2022 ranged between USD 3 to 8 per kilogram, depending on electricity prices and technology used. In contrast, fossil-fuel-based hydrogen (grey hydrogen) costs only around USD 1 to 2 per kilogram, making it much more competitive. Additionally, storage infrastructure such as high-pressure tanks, liquefaction facilities, and underground caverns requires significant investment, further limiting large-scale deployment. Until costs fall through technological innovation and economies of scale, this financial barrier will remain a major hurdle for wider adoption.

MARKET OPPORTUNITIES

Seasonal Energy Storage for Grid Reliability to Offer Lucrative Opportunities for the Market

Hydrogen offers a unique opportunity to provide long-duration and seasonal energy storage, which is difficult to achieve with conventional batteries. While lithium-ion batteries are well-suited for short-term balancing, they typically provide storage for only a few hours. Hydrogen, however, can be stored for weeks or even months in underground caverns or pressurized tanks, making it ideal for bridging seasonal gaps in renewable energy production. For example, Germany is exploring underground salt caverns for hydrogen storage to balance seasonal variations in solar and wind generation. This capability positions hydrogen energy storage as a critical opportunity for countries with high renewable penetration, allowing them to maintain grid reliability while advancing toward their net-zero carbon goals.

MARKET CHALLENGES

Efficiency Losses and Technical Barriers to Restrain Market Growth

Another major challenge is the energy efficiency losses across the hydrogen storage cycle. When renewable electricity is converted into hydrogen through electrolysis, stored, and then reconverted into power using fuel cells or turbines, the round-trip efficiency can drop to as low as 30–40%, compared to 70–90% efficiency in battery storage systems. This makes hydrogen less efficient for short-term energy balancing, limiting its competitiveness in certain applications. Moreover, technical barriers such as hydrogen’s tendency to cause material embrittlement in pipelines and storage vessels add complexity and cost to infrastructure development. These efficiency and safety issues must be addressed through ongoing research and engineering advancements before hydrogen storage can achieve widespread and reliable adoption.

HYDROGEN ENERGY STORAGE MARKET TRENDS

Expansion of Large Scale Hydrogen Projects to Accelerate Market Growth

A notable trend in the hydrogen energy storage market is the rise of large scale hydrogen hubs and increased investments in energy storage solutions projects backed by government and private investors. For instance, the U.S. Department of Energy announced in 2023 that it would invest USD 7 billion to establish regional clean hydrogen hubs under the Bipartisan Infrastructure Law. Similarly, Europe is advancing projects such as the HyStock underground hydrogen energy storage systems in the Netherlands, which aim to demonstrate large-scale seasonal storage. These projects reflect a shift from small pilot programs to utility-scale systems that can stabilize grids and decarbonize entire regions. The increasing focus on scaling up infrastructure highlights a long-term trend in which hydrogen is positioned as a central pillar of future energy systems.

Download Free sample to learn more about this report.

IMPACT OF TARIFF ON THE MARKET

The impact of tariffs on the global hydrogen energy storage market growth is significant, as they directly affect the cost competitiveness of hydrogen technologies and infrastructure. Import duties on key components such as electrolyzers, storage tanks, and fuel cells can raise project costs and slow down adoption, particularly in developing regions where cost sensitivity is high. For example, countries that rely heavily on imported hydrogen equipment from leading suppliers in Europe, Japan, or South Korea may face higher installation expenses due to trade barriers. On the other hand, some governments use tariffs strategically to protect domestic industries and encourage local manufacturing of hydrogen technologies, which can strengthen regional supply chains over time. However, excessive tariff measures risk disrupting global collaboration and slowing the scale-up of hydrogen storage projects needed to meet climate and renewable energy targets. As a result, balancing trade policies to ensure affordability while supporting domestic innovation is crucial for the sustainable growth of the hydrogen energy storage market.

SEGMENTATION ANALYSIS

By Technology

Capacity to Store Hydrogen at Higher Pressures Boosts the Compressed Gas Storage Segment Growth

By technology, the market is segmented into compressed gas storage, liquid hydrogen storage, material-based storage, and underground bulk storage. The compressed gas storage segment dominates the market due to its relative simplicity and maturity, accounting for 53.46% of the market share in 2024. In this approach, hydrogen is stored at high pressures, typically between 350 to 700 bar, in specially designed tanks or underground facilities. It is particularly suitable for applications such as fuel cell vehicles and distributed energy systems, where quick refueling and mobility are essential.

Liquid hydrogen storage is the fastest-growing segment in terms of technology, with a CAGR of 11.29%. It involves cooling hydrogen to cryogenic temperatures of around -253°C, allowing it to be stored in liquid form at a much higher energy density compared to compressed gas. This makes it attractive for applications that require compact storage, such as aerospace, shipping, and large-scale energy transport.

By Form

Gas Segment Dominates the Market Due to its Simple Technology

Based on form, the market is divided into solid, liquid, and gas. Storing hydrogen in gaseous form is the dominant method, accounting for 66.65% share of the market in 2024. Gaseous hydrogen storage relies on high-pressure tanks or underground geological formations such as salt caverns. It is widely deployed in refueling stations and industrial processes due to its straightforward technology and relatively lower costs compared to liquid or solid storage.

Liquid hydrogen storage is the fastest-growing segment, with a CAGR of 11.31%. It involves condensing hydrogen into a liquid state by cooling it to cryogenic levels, enabling a high energy density per unit volume. This makes it an appealing solution for applications where space is limited but energy demand is high, such as aviation, shipping, and cross-border hydrogen transport.

By End User

To know how our report can help streamline your business, Speak to Analyst

Decarbonization Target in the Industrial Sector Boosts the Segment’s Growth in the Market

The market is segmented by end-user into utilities & grid operator, industrial, transportation, and others. Industrial is the dominant segment, holding a 43.57% share in 2024. In this sector, hydrogen energy storage plays a dual role by enabling decarbonization and ensuring a continuous energy supply. Many heavy industries, such as steel, cement, refining, and chemicals, rely on steady high-temperature heat, which is difficult to achieve with intermittent renewables. By storing hydrogen, industries can access on-demand clean fuel that substitutes for coal, natural gas, or oil. For example, the steel industry is actively exploring hydrogen as a feedstock for direct reduced iron (DRI) processes, reducing emissions by replacing coke with hydrogen. According to IRENA, industrial hydrogen demand could exceed 30% of total hydrogen consumption by 2050, making storage solutions critical for balancing production and use. Furthermore, industries with energy-intensive processes benefit from hydrogen’s ability to serve as both a fuel and raw material, reinforcing its role as a cornerstone of industrial decarbonization.

Utilities & grid operators are the fastest-growing segment in the market with a CAGR of 10.79% as hydrogen energy storage serves as a strategic solution to manage the variability of renewable power sources such as solar and wind. Unlike batteries, which are more suited for short-duration balancing, hydrogen can provide long-term and seasonal storage, ensuring that excess electricity generated during periods of low demand is not wasted. This stored hydrogen can later be reconverted to electricity during peak demand, helping stabilize the grid and prevent blackouts. Countries such as Germany and Japan are piloting large-scale underground hydrogen storage facilities to secure reliable energy reserves. As renewable penetration rises, projected to reach over 60% of global electricity by 2030 according to the IEA, hydrogen storage will become increasingly vital for utilities seeking to enhance energy security, grid flexibility, and carbon-free backup power.

HYDROGEN ENERGY STORAGE MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Hydrogen Energy Storage Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest hydrogen energy storage market share, driven by heavy investments in electrolyzers, refuelling infrastructure, and national hydrogen strategies in China, Japan, South Korea, and Australia. Industry estimates indicate that the Asia Pacific’s share is significantly higher than other regions, accounting for around 38.27% of the market in 2024, valued at approximately USD 7.41 billion in 2024. This reflects the rapid deployment of both hydrogen production and storage capacity. Strong industrial demand from sectors such as steel and chemicals, and government roadmaps to scale green hydrogen supply are key reasons behind the region’s dominance. Leading countries such as China, India, and Japan represent market values of USD 3.82 billion, USD 1.07 billion, and USD 1.32 billion, respectively, in 2025.

North America, led by the U.S. and Canada, is the second leading region in the market, with an estimated revenue of USD 6.23 billion in 2025 and a CAGR of 9.39% during the forecast year. The region’s growth is owing to major policy incentives and funding for hydrogen hubs that stimulate both production and storage projects. The U.S. Department of Energy’s Regional Clean Hydrogen Hubs program, which allocates approximately USD 7 billion for selected hubs, along with the production tax credit for clean hydrogen, underpins a robust project pipeline and attracts private capital. These initiatives strengthen the region’s position in mid- to large-scale storage solutions. The U.S. holds a market of USD 5.67 billion in 2025.

Europe also holds a significant presence in the market, with an estimated revenue of USD 4.99 billion in 2025. Growth in this region is driven by strong regulatory commitments to decarbonize industry and heavy early investment in electrolyzer capacity and underground storage pilots. Recent industry surveys show that Europe leads in installed electrolyzer project capacity about 32% of announced global capacity, reflecting a concentration of supply-chain activity, demand-side incentives, and pilot storage projects, including seasonal and cavern storage demonstrations. Leading countries such as the U.K., Germany, and France hold a market of USD 0.68 billion, USD 1.10 billion, and USD 0.83 billion in 2025.

The Middle East & Africa also holds a notable position in the market and represents a strategically important region for hydrogen storage due to abundant solar and wind resources, large green-hydrogen export projects (e.g., NEOM/ACWA), and a rising number of project announcements. These factors have improved the region’s share in the global hydrogen project pipeline. While local offtake is still growing, think-tank tracking shows MENA project counts surged from a few dozen to over 100 projects by end-2024, many classified as green hydrogen initiatives. This growth positions the Middle East as a rapidly expanding market for hydrogen production and associated storage solutions aimed at export and domestic industry. The Middle East & Africa market is valued at around USD 1.05 billion in 2025, with the GCC countries accounting for USD 0.48 billion in 2025.

Latin America currently holds a smaller share of the global hydrogen storage market compared with Asia Pacific, North America, and Europe. However, the region shows growing potential, led by countries with exceptional renewable resources. Chile, for example, has implemented national strategies to scale electrolyzer capacity, with ambitious targets reported between 2022 and 2024. It is widely recognized as the regional leader, underpinning stronger interest in nearby storage and export infrastructure. This momentum could significantly expand Latin America’s market share as planned projects transition to the construction phase.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Advancement in Product Solutions to Support Efficient Power Systems

ABB, Eaton, Siemens, Schneider Electric, GE, and others are key players operating in the hydrogen energy storage market. ABB has been a pioneer in advancing hydrogen energy storage technology to support the transition toward more flexible and efficient power systems. One of its major milestones is the development of the world's first hybrid high-voltage DC (HVDC) circuit breaker, which combines mechanical and power electronics technologies to interrupt fault currents within milliseconds. This innovation has been crucial for enabling multi-terminal HVDC grids, which are vital for integrating large-scale renewable energy sources such as offshore wind farms. ABB continues to invest heavily in research and development, focusing on improving breaker speed, reducing energy loss, and enhancing compactness. The company is also working on solid-state DC breaker solutions aimed at applications in electric mobility, microgrids, and data centers, helping meet the growing demand for reliable DC protection in both high-voltage transmission and low-voltage industrial sectors.

List of the Key Hydrogen Energy Storage Companies Profiled

- Linde plc (Ireland)

- Air Liquide (France)

- Air Products & Chemicals, Inc. (U.S.)

- ENGIE (France)

- Plug Power Inc (U.S.)

- ITM Power (U.K.)

- Nel Hydrogen (Norway)

- Iwatani Corporation (Japan)

- Chart Industries (U.S.)

- Worthington Industries Inc (U.S.)

- Luxfer Holdings plc (U.K.)

- Hexagon Composites ASA (Norway)

- INOXCVA (India)

- Steelhead Composites Inc (U.S.)

- FuelCell Energy, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, CPS Energy agreed to purchase four natural gas power plants from ProEnergy in the ERCOT market for USD 1.387 billion. With a combined capacity of 1.632 GW, these modern peaking facilities are located in Harris, Brazoria, and Galveston Counties. The assets are dual-fuel capable, giving CPS Energy the flexibility to transition to hydrogen blends in the future to cut carbon emissions.

- In August 2025, Energy Vault secured approval to participate in California’s wholesale power market with its 293MWh Calistoga Resiliency Centre in Napa Valley. Cleared by the CPUC, the project combines hydrogen fuel cells with a lithium-ion battery system to provide backup power during wildfire-related outages and other disruptions. Along with a newly signed interconnection agreement, the approval confirms the facility’s readiness to deliver grid services once distribution upgrades are complete.

- In July 2025, Masdar signed an MoU with Germany’s EnBW to collaborate on energy storage, offshore wind, and green hydrogen production projects across Europe. The agreement, signed in Berlin during the first UAE-Germany Business Council meeting, outlines cooperation on battery storage in Germany and the U.K., offshore wind developments in the North and Baltic Seas, and potential green hydrogen ventures. The partnership aims to drive clean energy innovation, support decarbonisation in hard-to-abate sectors, and enhance Europe’s energy security while also considering other renewable technologies.

- In January 2025, HELION Hydrogen Power, part of the Alstom Group, partnered with M Reformer to test the compatibility of its high-power fuel cells with hydrogen derived from methanol. As part of the project, HELION will supply a 100kW fuel cell to be integrated with M Reformer's E-NOMAD system at the company’s site near Barcelona. The demonstration aims to showcase the potential of liquid hydrogen carriers such as methanol for boosting on-site energy storage. As per HELION, the collaboration supports its strategy to develop multi-vector hydrogen solutions and address storage limitations for clients.

- In December 2024, Mitsubishi Power Americas, through its subsidiary MHI Hydrogen Infrastructure, signed a subrecipient agreement with the Pacific Northwest Hydrogen Association for its Boardman Hydrogen Hub project. The deal supports PNWH2’s role as one of the seven U.S. regional hydrogen hubs under the DOE’s H2Hubs Program, which is currently in Phase 1. This milestone strengthens project development, secures access to federal funding, and advances clean hydrogen deployment in the region. MHI H2I would apply Mitsubishi’s hydrogen technologies to help meet the DOE’s clean energy goals and contribute to building a national hydrogen network.

REPORT COVERAGE

The report delivers a detailed insight into the market and focuses on key aspects, such as leading companies. Besides, it offers insights into the market trends & technologies and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors and challenges that have contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 9.65% from 2025 to 2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology

|

|

By Form

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 19.37 billion in 2024.

The market is likely to record a CAGR of 9.65% over the forecast period (2025-2032).

By end user, the industrial segment is leading the market.

The Asia Pacific market size was valued at USD 7.41 billion in 2024.

Rising renewable energy deployment is the key factor driving the market’s growth.

Some of the key players in the market are NEL Hydrogen, Linde Plc, Engie, ITM Power, and others.

The global market size is expected to reach a valuation of USD 41.50 billion by 2032.

- 2019-2032

- 2024

- 2019-2023

- 178

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us