Hydrogen Powered Yacht Market Size, Share & Industry Analysis, By Yacht Size (Up to 24 meters, 24-40 meters, 40-70 meters, and Above 70 meters), By Hydrogen Storage Type (Compressed Gaseous Hydrogen (CGH₂), and Liquid Hydrogen (LH₂)), By Build Type (New Build Hydrogen Yachts and Retrofit / Conversion), By Power Output (Below 500 kW, 500 kW - 1 MW, and Above 1 MW) And Regional Forecast, 2026-2034

Hydrogen Powered Yacht Market Size and Future Outlook

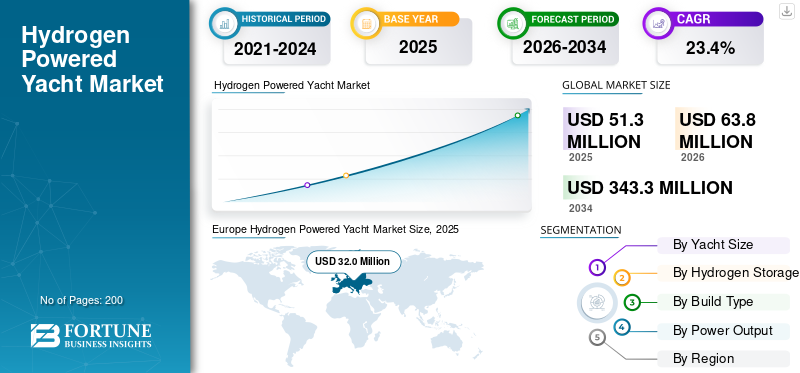

The global hydrogen powered yacht market size was valued at USD 51.3 million in 2025. The market is projected to grow from USD 63.8 million in 2026 to USD 343.3 million by 2034, with a CAGR of 23.4% over the forecast period. Europe dominated the hydrogen powered yacht market with a market share of 62.38% in 2025.

A hydrogen powered yacht is a marine vessel that uses hydrogen as its primary energy source for propulsion and onboard electrical systems. It typically integrates fuel cells that convert hydrogen into electricity, powering electric motors and hotel loads, with water vapor as the only direct emission, enabling low-noise, zero-emission cruising. Key drivers include tightening maritime decarbonization goals, growing demand for sustainable luxury among high net worth individuals, and advancements in marine fuel cell integration and safety standards. Shipyards are leveraging hydrogen to differentiate premium yacht offerings, while evolving classification guidelines and pilot projects reduce technical uncertainty. Expanding refit ecosystems and improving hydrogen storage solutions further accelerate adoption across new builds and conversions.

Leading players include European yacht builders such as Feadship, Lurssen, and Sanlorenzo, as well as technology providers such as Siemens Energy, ABB, and Ballard Power Systems. The trend is toward large-yacht fuel cell integration, hybrid hydrogen-battery architectures, and pilot flagship projects showcasing liquid hydrogen storage. Strategic collaborations between shipyards and fuel cell manufacturers are increasing to accelerate commercialization.

Download Free sample to learn more about this report.

Hydrogen Powered Yacht Market Key Takeaways

- 2025 Market Size: 51.3 million

- 2026 Market Size: USD 63.8 million

- 2034 Forecast Market Size: USD 343.3 million

- CAGR: 23.4% from 2026–2034

- Europe dominated the hydrogen powered yacht market with a 62.38% share in 2025.

- The 24–40 meters yacht size segment held the largest market share in 2025.

- The Below 500 kW power output segment accounted for the largest market share in 2025.

Europe

Europe led the market with USD 32.0 million in 2025.

North America

North America recorded steady growth, supported by clean-marine initiatives.

Asia Pacific

Asia Pacific is expected to witness strong growth during the forecast period.

U.S

The market is projected to reach USD 10.3 million in 2026.

Japan

The market is expected to reach USD 2.3 million in 2026.

Read More

HYDROGEN POWERED YACHT MARKET TRENDS

Flagship Zero-Emission Superyacht Projects Accelerate Technology Demonstration

Hydrogen powered yachts are increasingly positioned as flagship sustainability statements within the luxury marine sector. Shipyards are using full-scale demonstrator vessels to validate fuel cell integration, onboard hydrogen storage, and hybrid energy management systems. These projects help de-risk future commercialization by working through classification, safety compliance, and real-world performance challenges. As early adopters showcase operational hydrogen yachts, confidence among owners, charter operators, and insurers improves. The trend is particularly visible in Europe, where advanced shipyards are leveraging hydrogen propulsion system to differentiate ultra-luxury offerings. Such demonstrators create technology spillovers into smaller yacht categories over time.

- In May 2024, Feadship launched Project 821, described as the world’s first hydrogen fuel-cell superyacht, showcasing large-scale integration of liquid hydrogen and fuel cell systems.

MARKET DYNAMICS

MARKET DRIVERS

Strengthening Maritime Decarbonization Frameworks to Drive Clean Propulsion Adoption

Global pressure to reduce greenhouse gas emissions in maritime transport is influencing the luxury yacht segment. International Maritime Organization (IMO) strategies targeting net-zero emissions around mid-century are encouraging the development of alternative fuels and eco-friendly, zero-emission propulsion research. Although large yachts represent a niche share of overall marine emissions, regulatory momentum is shaping design expectations, marina policies, and financing criteria. Owners increasingly view hydrogen propulsion as a forward-looking solution that aligns with long-term environmental goals and future-proof compliance. Shipyards are responding by investing in fuel cell integration capabilities and advanced safety systems to meet emerging standards.

- In July 2023, the IMO adopted its revised greenhouse gas strategy, committing to net-zero emissions from international shipping by or around 2050, reinforcing the shift toward alternative marine fuels.

MARKET RESTRAINTS

Limited Hydrogen Bunkering Infrastructure Constrains Widespread Adoption

Despite technological progress, hydrogen-powered yachts face infrastructure constraints that limit rapid market expansion. Dedicated hydrogen bunkering facilities in marinas and coastal hubs remain scarce, and storage, transport, and safety regulations vary across jurisdictions. The absence of a standardized marine hydrogen refueling network increases operational uncertainty for yacht owners planning long-range voyages. High capital expenditure for cryogenic storage and port-side safety compliance further slows deployment. Until coastal hydrogen ecosystems mature, adoption of hydrogen powered yachts is likely to be concentrated near select pilot locations rather than on global cruising routes. Infrastructure readiness remains a decisive gating factor for scaling beyond demonstration projects.

- In February 2021, the European Commission launched its Hydrogen Strategy initiatives, emphasizing infrastructure buildout as a prerequisite for hydrogen uptake across transport sectors, including maritime applications.

MARKET OPPORTUNITIES

Expanding Green Hydrogen Production Creates Long-Term Fuel Cost Potential

Growth in renewable-powered hydrogen production presents a structural opportunity for hydrogen-powered yachts. As electrolyzer capacity expands and renewable energy penetration increases, green hydrogen costs are expected to decline over time. This improves the long-term operating economics of hydrogen yachts relative to conventional fossil fuels, particularly in regions investing heavily in hydrogen value chains. Yacht builders can align with emerging hydrogen hubs to offer vessels optimized for zero-emission cruising in designated green corridors. Falling fuel costs combined with rising environmental awareness among high-net-worth individuals may accelerate premium adoption.

MARKET CHALLENGES

Technical Integration Complexity Challenges Large-Scale Commercialization

Integrating hydrogen fuel cells, cryogenic storage, and marine safety systems into luxury yachts presents significant engineering complexity. Weight distribution, ventilation, fire suppression, and classification approvals require bespoke design solutions, particularly for larger vessels exceeding 1 MW power capacity. System redundancy and onboard safety protocols add further cost and design constraints. Shipyards must coordinate closely with fuel cell manufacturers, classification societies, and regulatory authorities to secure approvals, extending project timelines. Limited field experience compared to conventional marine engines also increases perceived technical risk among buyers. Overcoming these integration challenges is critical for scaling production beyond isolated projects.

- In June 2022, the IMO issued Interim Guidelines for the Safety of Ships Using Fuel Cell Power Installations, underscoring the specialized regulatory considerations required for marine fuel cell integration.

Download Free sample to learn more about this report.

Segmentation Analysis

By Yacht Size

Expanding Mid-Size Yacht Adoption Strengthens 24-40 Meters Segment Leadership

Based on yacht size, the market is segmented into up to 24 meters, 24-40 meters, 40-70 meters, and above 70 meters.

The 24-40 meters segment dominates due to balanced integration feasibility, mid sized sufficient space for fuel cell systems, and strong demand from environmentally conscious luxury buyers and yachts sport yachts operators. This size category offers practical cruising range while avoiding the extreme engineering complexity of mega yachts. It also aligns well with early hydrogen adoption economics, making it commercially viable for pioneering shipyards.

- In January 2023, Sanlorenzo presented its 50Steel project, integrating fuel cell technology for large yachts, highlighting mid-to-large yacht hydrogen integration momentum.

To know how our report can help streamline your business, Speak to Analyst

The Above 70 meters segment is projected to grow at a CAGR of 27.7% over the forecast period.

By Hydrogen Storage Type

Compressed Gaseous Hydrogen (CGH₂) Segment Gains Traction Due to Integration Simplicity

Based on hydrogen storage type, the market is segmented into Compressed Gaseous Hydrogen (CGH₂) and Liquid Hydrogen (LH₂).

CGH₂ dominates as it offers simpler storage systems, lower cryogenic handling requirements, and easier integration into mid-size yacht designs. Early-stage hydrogen yachts favor compressed systems due to established industrial experience and manageable onboard safety measures. This practicality supports broader pilot deployments and early commercialization.

However, LH₂ is expected to expand significantly as larger yachts require higher energy density and longer cruising ranges. The Liquid Hydrogen (LH₂) segment is projected to grow at a CAGR of 33.7% over the forecast period.

By Build Type

Purpose-Built Hydrogen Yachts Anchor New Build Hydrogen Yachts Segment Dominance

Based on build type, the market is segmented into New Build Hydrogen Yachts and Retrofit/Conversion.

New build hydrogen yachts segment dominates due to design flexibility, optimized tank placement, structural safety compliance, and integrated power management systems. Hydrogen propulsion requires careful planning around weight distribution, ventilation, and certification, which is more efficiently addressed during initial construction rather than retrofitting existing diesel vessels. Shipyards are leveraging new builds to showcase zero-emission innovation and secure premium buyers.

- In May 2024, Feadship delivered its hydrogen fuel-cell-powered superyacht Project 821, demonstrating purpose-built hydrogen integration at scale.

The retrofit/conversion segment is projected to grow at a CAGR of 31.7% over the forecast period.

By Power Output

Below 500 kW Segment Leads Due to Early Deployment Across Compact Yachts

Based on power output, the market is segmented into below 500 kW, 500 kW–1 MW, and Above 1 MW.

The below 500 kW segment dominated with the largest hydrogen powered yacht market share, as hydrogen adoption remains concentrated in smaller and mid-size yachts, where energy requirements are manageable and integration risk is lower. Compact fuel cell systems paired with battery hybrids provide reliable propulsion while maintaining operational efficiency. These systems also reduce upfront capital costs compared to multi-megawatt installations. As hydrogen technology matures, demand for higher-capacity systems is rising in superyachts.

- In October 2023, China’s first hydrogen fuel-cell powered vessel completed a demonstration voyage, validating scalable marine fuel-cell performance.

The Above 1 MW segment is projected to grow at a CAGR of 29.3% over the forecast period.

HYDROGEN POWERED YACHT MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

EUROPE

Europe Hydrogen Powered Yacht Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe dominates the market due to its concentration of high-end shipyards and proactive decarbonization policies. The region is home to leading superyacht builders capable of integrating complex hydrogen fuel-cell systems. Regulatory clarity, strong classification support, and sustainability-focused clientele further strengthen adoption. European shipyards are actively positioning hydrogen yachts as premium zero-emission flagships, reinforcing the region’s leadership. Continuous innovation in marine engineering and collaboration with energy technology firms support scalable long-term growth across multiple yacht size categories.

U.K. HYDROGEN POWERED YACHT MARKET

The U.K. benefits from advanced marine engineering expertise and increasing investment in hydrogen innovation clusters. Strong naval architecture capabilities and sustainability commitments support the gradual hydrogen yacht integration. The U.K. market is likely to reach USD 4.3 million in 2026.

GERMANY HYDROGEN POWERED YACHT MARKET

Germany is set to contribute around 9.3% in 2026 through high-performance marine engineering, fuel-cell technology expertise, and precision manufacturing. Collaboration between energy technology firms and shipyards enhances hydrogen propulsion integration in premium vessels.

NORTH AMERICA

North America hydrogen powered yacht market growth is witnessing a steady rise, supported by a strong refit infrastructure and growing clean-marine innovation initiatives. The region benefits from advanced marina networks, high yacht ownership density, and active decarbonization research programs. Adoption remains moderate compared to Europe, but retrofit-driven hydrogen integration is expanding as safety frameworks mature. Increasing collaboration between technology developers and yacht service yards strengthens the region’s long-term outlook. The U.S. remains central to regional momentum due to its scale and marine engineering capabilities.

U.S. HYDROGEN POWERED YACHT MARKET

The U.S. leads regional adoption due to its large luxury yacht fleet, established refit ecosystem, and marine innovation programs. Hydrogen propulsion trials and maritime decarbonization initiatives are accelerating interest among premium yacht owners. Strong coastal infrastructure and private-sector investment in hydrogen technology enhance commercialization potential, positioning the country as the core North American growth engine. The U.S. market is expected to reach USD 10.3 million in 2026.

ASIA PACIFIC

Asia Pacific is emerging as a fast-growing region, driven by government-backed hydrogen initiatives and expanding shipbuilding capabilities. Demonstration vessels, policy roadmaps, and investments in hydrogen infrastructure are strengthening regional readiness. While initial adoption centers on smaller vessels and pilot programs, the region is gradually moving toward larger yacht integration. Industrial policy alignment and expanding marine technology ecosystems are accelerating momentum, particularly in East Asia. The region is expected to gain share steadily over the forecast period as domestic hydrogen supply chains mature.

CHINA HYDROGEN POWERED YACHT MARKET

China is advancing hydrogen marine applications through state-supported demonstration vessels and expanding clean energy initiatives. Its strong shipbuilding industry and growing hydrogen ecosystem provide scalability advantages in long-term yacht integration. China is anticipated to capture 30.3% share in 2026.

JAPAN HYDROGEN POWERED YACHT MARKET

Japan leverages established fuel-cell expertise and maritime technology innovation. Government-supported hydrogen roadmaps and collaboration with marine manufacturers position the country as a technology-driven contributor. Japan is expected to be valued at USD 2.3 million in 2026.

INDIA HYDROGEN POWERED YACHT MARKET

India is gradually entering the hydrogen marine space through policy-backed pilot deployments and shipyard participation. India is the fastest growing, with a CAGR of 33.9% over the forecast period, and clean energy ambitions and expanding maritime infrastructure are supporting future adoption potential.

REST OF THE WORLD HYDROGEN POWERED YACHT MARKET

The rest of the world, including the Middle East and select emerging marine hubs, indicates gradual but selective growth. Adoption is primarily driven by ultra-luxury yacht demand and sustainability branding rather than large-scale industrial hydrogen ecosystems. While infrastructure limitations remain a constraint, high-net-worth clientele and marina modernization initiatives support niche hydrogen yacht deployment. Growth remains smaller in share compared to Europe and the Asia Pacific, but presents premium project opportunities over the long term.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Fuel Cell Integration, Strategic Shipyard Partnerships, and Green Energy Alliances Define Competitive Positioning

The global hydrogen powered yacht market trends are characterized by technological experimentation, high capital intensity, and collaboration between luxury shipyards and clean-energy technology providers. Leading yacht builders such as Feadship, Lurssen, Sanlorenzo, and Benetti compete by integrating advanced fuel cell systems, hybrid battery architectures, and optimized hydrogen storage solutions into their premium vessels. Technology providers, including Siemens Energy, ABB, Ballard Power Systems, and MAN Energy Solutions, support competitiveness through scalable marine fuel cells, power management systems, and safety engineering expertise. Companies differentiate through purpose-built hydrogen platforms, energy-efficient hull designs, and long-range zero-emission cruising capabilities. Strategic alliances between shipyards, classification societies, and hydrogen infrastructure developers are strengthening commercialization pathways.

- In May 2024, Feadship delivered its hydrogen fuel-cell-powered superyacht Project 821, demonstrating large-scale integration of liquid hydrogen storage and fuel cell propulsion, reinforcing competitive momentum toward zero-emission luxury yachting.

LIST OF KEY HYDROGEN POWERED YACHT COMPANIES PROFILED

- Lurssen (Germany)

- Feadship / Royal Van Lent (Netherlands)

- Damen Shipyards Group (Netherlands)

- Sanlorenzo S.p.A. (Italy)

- Ferretti Group (Italy)

- Azimut Benetti Group (Italy)

- Sunreef Yachts (Poland)

- Fincantieri S.p.A. (Italy)

- Heesen Yachts (Netherlands)

- Oceanco (Netherlands)

- Baglietto (Italy)

- Enata Group (UAE)

- Siemens Energy (Germany)

- Ballard Power Systems (Canada)

- PowerCell Sweden AB (Sweden)

KEY INDUSTRY DEVELOPMENTS

- February 2026: VINSSEN and MANA Engineering signed an MoU to jointly develop a hydrogen fuel-cell retrofit solution and pursue Approval in Principle with a classification society. The engineering workflow feasibility study AiP integration mirrors how hydrogen yacht retrofits will likely progress, especially for larger power classes.

- November 2025: Newlight reported completing Factory Acceptance Testing (FAT) with RINA for a hydrogen retrofit package intended for two- and four-stroke marine engines, enabling hydrogen blending to cut emissions. The milestone supports the retrofit/conversion pathway, which is important for yachts where owners prefer upgrades over new builds, by moving retrofit tech closer to vessel installation.

- December 2025: India launched its first indigenous hydrogen fuel-cell passenger vessel into commercial service in Varanasi, built as a national clean-maritime demonstration. While not a yacht, the program expands regional supplier capability in fuel-cell marine systems and safety certification experience, foundational inputs that can later support hydrogen adoption in leisure craft ecosystems.

- October 2025: Hindustan Shipyard Limited signed MoUs with the Indian Ports Association under India’s Green Tug Transition Programme, including the development of hydrogen-powered tugs. Though outside yachting, it signals expanding OEM port collaboration on hydrogen marine propulsion and refueling readiness capabilities that can spill over to marinas and coastal service providers supporting future hydrogen yachts.

- September 2025: Royal Huisman highlighted a new superyacht concept developed in close collaboration with Cor D. Rover Design, Rondal, and Artemis Technologies, combining a wing sail concept with hydrogen fuel-cell technology. Showcased at the Monaco Yacht Show window, it signals broader supplier shipyard teaming to package hydrogen systems with efficiency-first yacht architectures.

REPORT COVERAGE

The global hydrogen powered yacht market analysis provides an in-depth study of the market size and forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, strategic partnerships, mergers, and acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 23.4% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Yacht Size, By Hydrogen Storage Type, By Build Type, By Power Output, and By Region |

| By Yacht Size |

|

| By Hydrogen Storage Type |

|

| By Build Type |

|

| By Power Output |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 51.3 million in 2025 and is projected to reach USD 343.3 million by 2034.

In 2025, the Europe’s market value stood at USD 32.0 million.

The market is expected to grow at a CAGR of 23.4% during the forecast period.

By build type, the new build hydrogen yachts segment led the market.

Strengthening maritime decarbonization frameworks are the key factors driving the market.

Key market players include Feadship, Lurssen, Sanlorenzo, Siemens Energy, ABB, and Ballard Power Systems.

Europe accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us