Hydrogenation Catalyst Market Size, Share & Industry Analysis, By Product Type (Base Metal Based, Precious Metal Based, and Others), By Application (Oil Refining, Petrochemicals & Polymers, Chemicals, Edible Oils & Fats, and Others), and Regional Forecast, 2026-2034

HYDROGENATION CATALYST MARKET SIZE AND FUTURE OUTLOOK

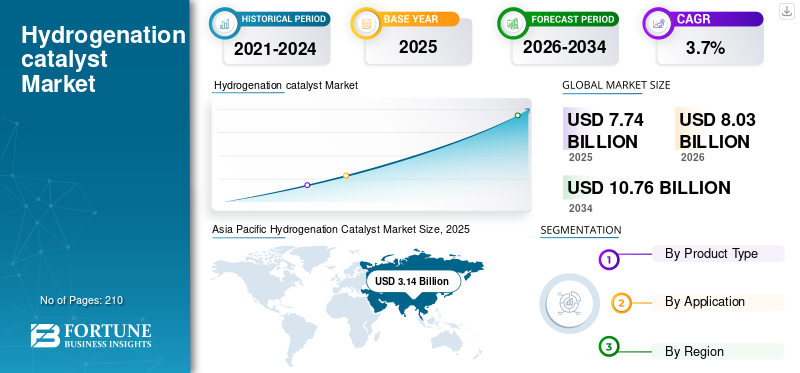

The global hydrogenation catalyst market size was valued at USD 7.74 billion in 2025. The market is projected to grow from USD 8.03 billion in 2026 to USD 10.76 billion by 2034, exhibiting a CAGR of 3.7% during the forecast period. Asia Pacific dominated the hydrogenation catalyst market with a market share of 40.56% in 2025.

A hydrogenation catalyst is a material, typically based on nickel, cobalt-molybdenum, palladium, platinum, or other transition metals, that accelerates the addition of hydrogen to unsaturated chemical bonds under controlled temperature and pressure. It enables the selective saturation of hydrocarbons, aromatics, aldehydes, and other intermediates across refining, petrochemical, chemical, pharmaceutical, and edible oil processes. Major demand drivers comprise tightening global fuel quality and decarbonization standards, which require deeper hydroprocessing, renewable diesel production, and higher selectivity in chemical manufacturing. These structural shifts increase catalyst intensity, upgrade frequency, and performance requirements, supporting steady long-term growth in product consumption worldwide. BASF, Honeywell International Inc., Clariant AG, and Shell are the key players in the market.

Download Free sample to learn more about this report.

HYDROGENATION CATALYST MARKET TRENDS

Energy Transition to Accelerate the Shift toward High-Selectivity and Bio-Feedstock Catalysts

The global push toward decarbonization is reshaping the demand for hydrogenation catalysts, with refiners and chemical producers increasingly adopting high-selectivity systems compatible with renewable feedstocks. Growth in renewable diesel, sustainable aviation fuel (SAF), and bio-based intermediates requires catalysts capable of handling oxygenates, impurities, and variable feedstock quality. This has accelerated innovation in bimetallic and noble-metal catalysts with improved stability and regeneration profiles. Simultaneously, producers are reducing precious metal loadings to manage cost volatility. As a result, the industry is moving from commodity hydroprocessing systems toward more engineered, performance-driven catalyst solutions with higher technical differentiation and lifecycle value.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stricter Fuel Standards and Renewable Fuel Mandates to Boost Product Demand

Tightening global fuel sulfur limits, coupled with renewable diesel and SAF mandates, are significantly increasing hydroprocessing intensity across refineries. To meet ultra-low sulfur specifications and process bio-feedstocks, refiners require advanced selective hydrogenation catalysts with higher activity and longer cycle life. Capacity additions in Asia and the Middle East, along with renewable fuel retrofits in North America and Europe, are structurally lifting catalyst replacement volumes. This regulatory-driven demand provides predictable growth, as compliance is non-discretionary. Consequently, product consumption continues to expand steadily despite modest overall refinery throughput growth, driving hydrogenation catalyst market growth.

MARKET RESTRAINTS

Precious Metal Price Volatility Pressures Margins and Procurement to Restrain Market Growth

Hydrogenation catalysts relying on palladium, platinum, and ruthenium face demand sensitivity due to extreme price volatility in precious metals. Sudden price spikes increase working capital requirements for manufacturers and procurement risk for end-users, often delaying purchases or encouraging regeneration over replacement. While metal pass-through mechanisms partially offset risk, margin compression can occur in competitive contracts. Additionally, increased focus on metal recovery and recycling reduces net fresh catalyst demand growth in specialty applications. This structural exposure to commodity price swings remains a key restraint, particularly in pharmaceuticals and fine chemicals where noble metal intensity is the highest.

MARKET OPPORTUNITIES

Emerging Petrochemical Complexes in Asia and Middle East to Expand the Market

Large-scale integrated refinery and petrochemical projects in Asia Pacific and the Middle East are expanding long-term catalyst demand. New complexes are designed with high hydrocracking severity, petrochemical integration, and export-grade fuel standards, increasing hydrogenation catalyst intensity per barrel processed. These projects create multi-year supply contracts and recurring replacement demand, offering stable revenue visibility for global catalyst suppliers. In parallel, the domestic chemical manufacturing growth in India and Southeast Asia opens new opportunities for base and precious metal hydrogenation systems. The geographical capacity shifts toward emerging markets represent a durable structural growth lever for the market.

MARKET CHALLENGES

Refinery Rationalization in Mature Markets to Cap Structural Volume Growth

While emerging regions are expanding, refinery closures and capacity rationalization in Europe and parts of North America constrain long-term hydrogenation catalyst volume growth in mature markets. Energy transition policies, electrification trends, and flat fuel demand reduce the need for new hydroprocessing capacity. Although renewable diesel retrofits partially offset declines, overall throughput growth remains limited. This creates competitive pressure among catalyst suppliers in OECD markets, intensifying pricing competition and contract renegotiations. Balancing growth in emerging regions with stagnation in mature economies remains a strategic challenge for global manufacturers.

SEGMENTATION ANALYSIS

By Product Type

Rising Selectivity Requirements in Clean Energy Applications to Drive Precious Metal Based Catalyst Demand

Based on product type, the market is segmented into base metal based, precious metal based, and others.

The precious metal based segment is anticipated to hold the dominant global hydrogenation catalyst market share during the forecast period. A major factor driving the demand for precious metal-based catalysts is the increasing need for high selectivity and performance in specialty chemicals, pharmaceuticals, and renewable fuel processing. Palladium, platinum, and ruthenium catalysts enable precise hydrogenation under milder conditions, improving yield and reducing by-products. As bio-feedstocks and complex intermediates become more common, manufacturers require catalysts that handle impurities while maintaining efficiency. This shift toward higher-value, precision-driven production is structurally accelerating the demand for precious metal systems despite their higher cost.

The primary driver for the others segment is the expansion of hydroprocessing capacity in Asia and the Middle East. New refinery and petrochemical complexes are designed to meet ultra-low sulfur fuel standards and process heavier, more challenging crude slates. These requirements increase catalyst intensity and replacement frequency. As emerging economies invest in export-oriented refining infrastructure, the demand for high-activity catalysts continues to rise steadily, making this segment the second-fastest growing globally. The others segment is anticipated to rise with a CAGR of 3.3% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Stricter Fuel Standards and Renewable Fuel Integration to Drive Oil Refining Segment Growth

Based on application, the market is segmented into oil refining, petrochemicals & polymers, chemicals, edible oils & fats, and others.

The oil refining segment is anticipated to hold the dominant market share during the forecast period. A major factor driving product demand in oil refining is the tightening of global fuel quality regulations combined with renewable fuel integration. Ultra-low sulfur mandates and cleaner fuel specifications require deeper hydrotreating and higher hydrocracking severity, increasing catalyst consumption and replacement frequency. Additionally, refiners are retrofitting units to process renewable feedstocks for diesel and sustainable aviation fuel production. These structural shifts elevate hydrogenation intensity per barrel processed, ensuring steady long-term demand despite relatively slower global fuel consumption growth.

The chemicals segment is anticipated to rise with the fastest CAGR of 4.3% over the forecast period. The fastest growth rate is driven by the expanding production of specialty intermediates, performance materials, and fine chemicals. Increasing demand for high-purity alcohols, amines, and functionalized compounds, particularly in pharmaceuticals, agrochemicals, and advanced materials, requires highly selective hydrogenation processes. Manufacturers are prioritizing yield optimization and impurity control, favoring advanced catalyst systems. As chemical value chains shift toward higher complexity and customization, the catalysts play a critical enabling role, accelerating demand growth in this segment globally.

HYDROGENATION CATALYST MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Hydrogenation Catalyst Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region holds the largest market share. The regional product demand is primarily driven by oil refining, supported by large-scale refinery expansions in China and India and increasing hydrocracking severity. The growing domestic fuel consumption and export-oriented refining amplify hydroprocessing requirements. Strong petrochemical integration further supports demand through selective hydrogenation of monomers and intermediates. Additionally, expanding edible oil processing and bulk chemical manufacturing in India and Southeast Asia contribute to the regional demand. The region’s combination of scale, integration, and capacity additions makes it the global growth engine for catalyst consumption.

Japan Hydrogenation Catalyst Market

The Japan market reached approximately USD 0.30 billion in 2025, equivalent to around 3.9% of global sales.

China Hydrogenation Catalyst Market

The China market is projected to be one of the largest worldwide. Its 2025 revenues reached around USD 1.41 billion, representing roughly 18.2% of global sales.

India Hydrogenation Catalyst Market

The India market reached approximately USD 0.49 billion in 2025, equivalent to around 6.3% of global sales.

North America

In North America, the product demand is primarily driven by oil refining, particularly the rapid expansion of renewable diesel and sustainable aviation fuel capacity in the U.S. Refinery retrofits and hydroprocessing upgrades to meet ultra-low sulfur standards increase catalyst intensity and replacement frequency. The supporting demand comes from chemicals and petrochemicals, where selective hydrogenation is critical for monomer purification and specialty intermediates.

U.S. Hydrogenation Catalyst Market

The U.S. market reached approximately USD 1.61 billion in 2025, accounting for roughly 20.8% of global sales.

Europe

In Europe, a key driver of product demand is the chemicals sector, supported by the region’s strong specialty chemical and pharmaceutical manufacturing base. Increasing focus on high-purity intermediates and sustainable production pathways requires advanced precious metal catalysts. While oil refining remains significant, capacity rationalization limits growth, though renewable fuel retrofits provide partial support. Petrochemical hydrogenation and selective processing further supports demand. Overall, Europe’s market growth is quality-driven, with catalyst intensity rising due to stringent environmental regulations and product purity standards.

U.K. Hydrogenation Catalyst Market

The U.K. market reached approximately USD 0.16 billion in 2025, equivalent to around 2.1% of global sales.

Germany Hydrogenation Catalyst Market

The Germany market reached approximately USD 0.34 billion in 2025, equivalent to around 4.4% of global sales.

Latin America

In Latin America, the product demand is mainly driven by oil refining, particularly refinery modernization programs in Brazil and Mexico aimed at improving fuel quality and processing heavier crude slates. Upgrades in hydrotreating and hydrocracking increase catalyst replacement volumes. Supporting demand arises from edible oils and basic chemicals, especially in Brazil’s soybean processing industry. However, limited petrochemical expansion and modest specialty chemical capacity affect overall growth. The region remains refinery-centric, with demand tied closely to infrastructure upgrades rather than new capacity additions.

Brazil Hydrogenation Catalyst Market

The Brazil market reached approximately USD 0.21 billion in 2025, equivalent to around 2.7% of global sales.

Middle East & Africa

In the Middle East & Africa, the product demand is predominantly driven by oil refining, particularly the commissioning of large, integrated refinery and petrochemical complexes in Saudi Arabia, the UAE, and Nigeria. These facilities are designed for high hydrocracking severity and export-grade clean fuels, significantly increasing catalyst intensity. Supporting demand comes from growing petrochemical integration, where selective hydrogenation protects downstream polymer production. Limited specialty chemical and edible oil processing activity keeps the demand refinery-focused, positioning the region as the fastest-growing market globally.

Saudi Arabia Hydrogenation Catalyst Market

The Saudi Arabia market reached approximately USD 0.33 billion in 2025, equivalent to around 4.3% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Long-Term Refinery Contracts and R&D Capabilities to Drive the Leadership of Global Catalyst Producers

The global market is moderately consolidated, dominated by multinational catalyst specialists with strong R&D capabilities, proprietary formulations, and long-term refinery and petrochemical contracts. High technical barriers, metal recovery infrastructure, and application-specific customization create significant switching costs, favoring established suppliers. Competition centers on high performance catalysts, lifecycle optimization, and precious metal management rather than price alone. Key players in the market include BASF, Honeywell International Inc., Clariant AG, and Shell. Regional manufacturers operate in Asia but technology depth and global service networks differentiate the leading players.

LIST OF KEY HYDROGENATION CATALYST COMPANIES PROFILED

- BASF (Germany)

- Clariant (Switzerland)

- Shell (U.K.)

- Evonik (Germany)

- R. Grace & Co. (U.S.)

- Umicore (Belgium)

- Honeywell International Inc. (U.S.)

- China Petrochemical Corporation (China)

- Applied Catalysts (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2025 – Honeywell agreed to acquire Johnson Matthey’s Catalyst Technologies business, expanding its UOP portfolio across refining, petrochemicals, and renewable fuels. The deal enhances Honeywell’s capabilities in sustainable fuels, hydrogen, and ammonia, adds significant installed base scale, and is expected to be accretive in the first year, with closing anticipated in the first half of 2026.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Volume (Kiloton); Value (USD Billion) |

| Growth Rate | CAGR of 3.7% during 2026-2034 |

| Segmentation | By Product Type, By Application, and By Geography |

| By Product Type |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 7.74 billion in 2025 and is projected to record a valuation of USD 10.76 billion by 2034.

In 2025, Asia Pacific market stood at USD 3.14 billion.

The market will exhibit steady growth at a CAGR of 3.7% during the forecast period of 2026-2034.

The oil refining segment is expected to lead the market during the forecast period.

Stricter fuel standards and renewable fuel mandates is a key factor driving market growth.

BASF, Honeywell International Inc., Clariant AG, and Shell are the major players operating in the market.

Asia Pacific dominates the market in terms of share.

Petrochemical complexes in emerging economies are likely to drive product adoption.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us