In-Space Manufacturing Market Size, Share & Industry Analysis, By Manufacturing Type (Material Manufacturing, In-Space Fabrication, In-Space Assembly & Construction, and Biomanufacturing), By Operational Platform (International Space Station (ISS), Free-Flying Manufacturing Spacecraft, Commercial Space Stations, and Deep Space & Lunar Platforms), By Technology (Additive Manufacturing, Material Processing Technologies, Robotic Assembly & Automation, and Others), and By End User (Commercial, Government & Space Agencies, and Defense & Security), and Regional Forecast, 2026 – 2034

In-Space Manufacturing Market Size and Future Outlook

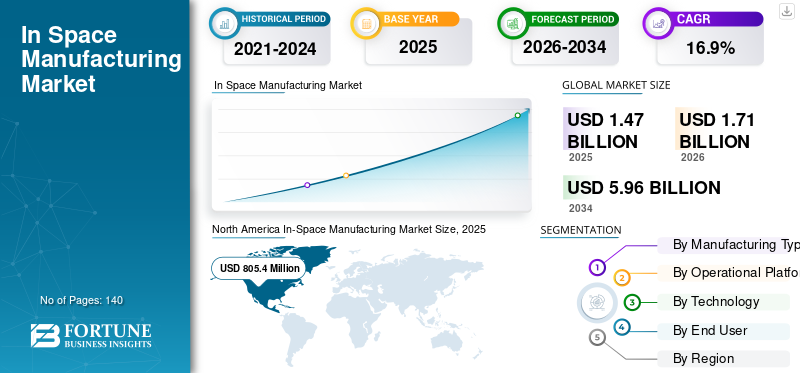

The global in-space manufacturing market size was valued at USD 1,472.8 million in 2025. The market is projected to grow from USD 1,712.9 million in 2026 to USD 5,969.4 million by 2034, exhibiting a CAGR of 16.9% during the forecast period. North America dominated the in space manufacturing market with a market share of 54.68% in 2025.

In-Space Manufacturing (ISM) comprises advanced orbital production capabilities that leverage microgravity conditions to enable the fabrication, processing, and assembly of high-value materials and operational platforms that are difficult or impossible to produce on Earth. These systems integrate specialized hardware such as microgravity-compatible manufacturing modules, automated fabrication units, re-entry capsules, and orbital platforms, along with software-driven mission control, remote operations, and data analytics frameworks to ensure precision, repeatability, and real-time process monitoring. ISM serves as a foundational pillar for the emerging space economy, enabling both earth-return products and in-orbit utilization across a range of industrial and scientific technologies. As governments and private enterprises increasingly invest in commercial space infrastructure and orbital production capabilities, the market is witnessing accelerated growth driven by the need to unlock new material properties, reduce dependency on earth-based supply chains, and support long-term space exploration and habitation. Key regions such as North America and Asia Pacific are at the forefront of adoption, supported by strong institutional funding, commercial innovation ecosystems, and the development of next-generation space stations and autonomous manufacturing platforms. ISM technologies are being deployed across technologies such as advanced fiber optics production, semiconductor and crystal growth, pharmaceutical research, and in-orbit fabrication of satellite Operational Platforms, enabling enhanced performance characteristics, reduced launch mass, and improved system resilience.

- For instance, in February 2025, Varda Space Industries successfully completed its orbital manufacturing mission by producing pharmaceutical compounds in microgravity and returning them to Earth via a re-entry capsule, demonstrating the commercial viability of space-based production and recovery systems.

Redwire Space, Varda Space Industries, Axiom Space, Sierra Space, and Blue Origin are among the key players holding a significant share of the market. Their competitive positioning is reinforced by strong expertise in microgravity manufacturing technologies, vertically integrated space infrastructure capabilities, strategic partnerships with space agencies, and continuous advancements in autonomous manufacturing systems, re-entry logistics, and scalable orbital platforms to support the evolving landscape of commercial space industrialization.

Download Free sample to learn more about this report.

In Space Manufacturing Market Key Takeaways

- 2025 Market Size: USD 1,472.8 million

- 2026 Market Size: USD 1,712.9 million

- 2034 Forecast Market Size: USD 5,969.4 million

- CAGR: 16.9% from 2026–2034

- North America dominated the market with a 54.68% share in 2025.

- Material manufacturing segment held the largest market share in 2025.

- International Space Station (ISS) segment held the largest market share in 2025.

North America

The market reached USD 805.4 million in 2025, driven by strong government funding and commercial space investments.

Asia Pacific

The market reached USD 297.3 million in 2025, driven by expanding space programs.

Europe

The market is driven by strong research capabilities and commercial space initiatives.

U.S.

The market is projected to reach USD 807.0 million by 2026, driven by advanced space infrastructure.

Japan

The market is projected to reach USD 67.0 million by 2026, supported by growing space research investments.

Read More

IN-SPACE MANUFACTURING MARKET TRENDS

Shift toward Autonomous, Modular, and Orbital Production Architectures is Reshaping Market Demand

Demand for in-space manufacturing is increasingly being driven by the need for autonomous operations, scalable production systems, and mission flexibility within orbital environments. As the space industry transitions from government-led experimentation to commercially driven production, organizations are moving away from one-off experimental payloads toward modular, reusable, and continuously operable manufacturing platforms. This shift is enabling the development of standardized in-orbit production units that can be deployed across multiple missions, significantly improving cost efficiency and operational scalability. Unlike traditional space missions that rely heavily on ground-controlled operations, there is a growing emphasis on autonomous and AI-enabled manufacturing systems capable of executing complex production processes with minimal human intervention. These systems integrate onboard data processing, real-time telemetry, and adaptive control mechanisms to optimize manufacturing conditions in microgravity, reduce communication delays, and ensure consistent product quality. The increasing deployment of free-flying manufacturing spacecraft and dedicated orbital factories is further accelerating this transition, allowing companies to conduct manufacturing activities independent of shared infrastructure such as the International Space Station (ISS).

- For instance, in January 2025, Redwire Space expanded its in-orbit manufacturing capabilities by advancing autonomous 3D printing technologies on the international space station, enabling continuous fabrication of operational platforms with minimal crew intervention and demonstrating the feasibility of scalable, automated production systems in microgravity environments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Commercial Space Infrastructure and Demand for High-Value Microgravity Production is Driving Market Growth

The in-space manufacturing market growth is increasingly being driven by the rapid expansion of commercial space infrastructure and the growing demand for high-value products that benefit from microgravity conditions. Unlike traditional earth-based manufacturing, in-space production enables the development of materials and biological structures with enhanced purity, structural integrity, and performance characteristics, creating strong demand across industries such as pharmaceuticals, advanced materials, and semiconductor manufacturing. As private companies and space agencies invest in next-generation orbital platforms, including commercial space stations and free-flying manufacturing spacecraft, the ability to conduct continuous and scalable production in orbit is becoming more viable.

- For instance, in May 2025, Axiom Space advanced the development of its commercial space station modules designed to support continuous in-orbit manufacturing and research activities, enabling scalable production capabilities for both industrial and pharmaceutical Technologies.

MARKET RESTRAINTS

High Mission Costs, Limited Orbital Infrastructure, and Operational Complexity is Constraining Market Scalability

The growth of the market is significantly constrained by the high cost of space missions, limited availability of dedicated manufacturing infrastructure, and the operational complexity associated with conducting production in microgravity environments. Unlike terrestrial manufacturing, in-space production requires specialized hardware, launch services, orbital deployment, and controlled re-entry systems, all of which contribute to significantly higher capital and operational expenditures. The reliance on shared infrastructure such as the International Space Station (ISS) further limits scalability, as access is constrained by mission scheduling, capacity limitations, and regulatory approvals. Additionally, maintaining consistent production quality in microgravity presents technical challenges, including process stability, thermal management, material behavior variability, and limited real-time human intervention. These factors increase the complexity of system design and require advanced automation, redundancy, and remote monitoring capabilities to ensure mission success. The lack of standardized manufacturing protocols and limited flight heritage for many production processes further adds to the uncertainty and risk associated with commercial deployment.

MARKET OPPORTUNITIES

Expansion of Commercial Orbital Platforms and Dedicated Manufacturing Missions are Creating New Growth Avenues

An emerging opportunity in the market lies in the rapid development of commercial orbital platforms and dedicated manufacturing missions, which are transforming ISM from an experimental activity into a scalable industrial capability. As reliance on shared infrastructure such as the International Space Station (ISS) becomes a limiting factor, private companies are investing in commercial space stations, free-flying manufacturing spacecraft, and modular orbital factories designed specifically for continuous production. These platforms enable higher mission frequency, increased payload capacity, and greater operational flexibility, creating a strong foundation for commercial-scale manufacturing.

- For instance, in March 2025, Sierra Space announced progress on its commercial space station development, designed to support scalable in-orbit manufacturing and research operations, enabling continuous production capabilities beyond the constraints of the ISS.

MARKET CHALLENGES

Operational Complexity, Limited Standardization, and Mission Risk Increasing Barriers to Commercialization

A key challenge in the market is the high level of operational complexity and lack of standardized manufacturing frameworks, which increases both technical risk and commercialization barriers. Unlike terrestrial manufacturing environments, ISM operations must function within highly constrained orbital conditions, where factors such as microgravity behavior, thermal fluctuations, radiation exposure, and communication delays can significantly impact production outcomes. Designing systems that can reliably operate under these conditions requires advanced engineering, extensive testing, and high levels of redundancy, increasing development timelines and costs. Another major challenge is the limited standardization of manufacturing processes and quality assurance protocols. Since many ISM technologies are still in early-stage development, there is no universally accepted framework for validating product quality, consistency, or performance, particularly for industries such as pharmaceuticals and advanced materials. This creates uncertainty for end-users and regulators, slowing adoption and commercialization.

Segmentation Analysis

By Manufacturing Type

Material Manufacturing Segment Led as It Represents Most Commercially Viable and Established In-Space Production Activity

By manufacturing type, the market is segmented into material manufacturing, in-space fabrication, in-space assembly & construction, and biomanufacturing.

Material manufacturing segment held the largest in-space manufacturing market share as it represents the most commercially validated and revenue-generating segment within the in-space manufacturing ecosystem. This segment primarily focuses on the production of high-value materials such as advanced optical fibers, semiconductor crystals, and specialty inorganic compounds that benefit significantly from microgravity conditions. The absence of gravity-driven convection and sedimentation enables superior material uniformity, reduced defects, and enhanced performance characteristics, making these products highly valuable for industries such as telecommunications, electronics, and advanced optics.

- For instance, in January 2024, Redwire Corporation announced continued advancements in its in-space manufacturing capabilities aboard the International Space Station, including expanded use of its additive manufacturing facility to produce Operational Platforms in orbit, supporting long-duration mission sustainability.

In-space assembly & construction segment is expected to witness the highest growth rate, with a CAGR of 18.4% over the forecast period, driven by the increasing demand for large-scale space infrastructure and long-duration missions. Unlike material manufacturing, this segment focuses on assembling and constructing systems directly in orbit, including satellite structures, antennas, trusses, and future space habitats.

To know how our report can help streamline your business, Speak to Analyst

By Operational Platform

International Space Station (ISS) Segment Led as It Represents Primary Hub for Current In-Space Manufacturing Activities

By operational platform, the market is segmented into international space station (ISS), free-flying manufacturing spacecraft, commercial space stations, and deep space & lunar platforms.

The International Space Station (ISS) segment held the largest market share as it represents the most established and accessible platform for conducting in-space manufacturing activities. The ISS provides a controlled microgravity environment, existing infrastructure, and proven operational frameworks that enable continuous experimentation and limited-scale production across materials science, biotechnology, and in-orbit fabrication. It serves as the primary testing ground for validating manufacturing processes, system performance, and product quality before transitioning to commercial-scale deployment.

The deep space & lunar platforms segment is expected to register the highest growth, with a CAGR of 20.0% over the forecast period, driven by increasing investments in long-duration space exploration and the development of sustainable off-Earth infrastructure. Unlike low Earth orbit platforms, deep space and lunar environments present unique opportunities for resource utilization, large-scale construction, and autonomous manufacturing systems.

By Technology

Material Processing Technologies Segment Led as It Represents Most Mature and Commercially Proven Approach in In-Space Manufacturing

By technology, the market is segmented into additive manufacturing (3D Printing), material processing technologies, robotic assembly & automation, and biomanufacturing techniques.

Material processing technologies segment held the largest market share as they represent the most commercially validated and widely adopted technological approach within the in-space manufacturing ecosystem. These technologies primarily focus on leveraging microgravity conditions to enhance the production of high-value materials such as optical fibers, semiconductor crystals, and specialty compounds. The absence of gravity-driven convection enables superior material uniformity, reduced defects, and improved structural integrity, making these processes highly attractive for industries requiring precision and performance.

Robotic assembly & automation segment is expected to witness the highest growth, with a CAGR of 18.6% over the forecast period, driven by the increasing need for autonomous operations and scalable in-orbit infrastructure development. This segment focuses on the use of robotic systems, AI-driven control, and automated mechanisms to assemble structures, manufacture Operational Platforms, and perform complex operations in space with minimal human intervention.

By End User

Government & Space Agencies Segment Led as It Represents Primary Source of Funding and Infrastructure for In-Space Manufacturing Activities

By end user, the market is segmented into commercial, government & space agencies, and defense & security.

The government & space agencies segment held the largest market share as it represents the primary driver of funding, infrastructure development, and mission execution within the in-space manufacturing ecosystem. Space agencies such as NASA, ESA, JAXA, and CNSA play a critical role in enabling ISM activities by providing access to orbital platforms, supporting research programs, and funding technology development initiatives. These organizations are at the forefront of deploying manufacturing experiments on platforms including the International Space Station (ISS) and are actively investing in next-generation space infrastructure to support long-term production capabilities.

The commercial segment is expected to witness the highest growth, with a CAGR of 18.8% over the forecast period, driven by the rapid increase in private sector investment and commercialization of in-space manufacturing activities. Companies are increasingly exploring ISM for high-value functions such as advanced materials, pharmaceuticals, and in-orbit fabrication, aiming to develop scalable business models that leverage microgravity advantages.

In-Space Manufacturing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America In-Space Manufacturing Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 805.4 million in revenue in 2025 and held the largest market share, supported by strong government funding, expanding commercial space infrastructure, and increasing private sector participation across the U.S., Canada, and Mexico. Regional demand is closely linked to the development of orbital manufacturing capabilities, microgravity research programs, and earth-return production systems, particularly in high-value technologies such as advanced materials and pharmaceuticals. The region benefits from the presence of established space agencies, a mature commercial space ecosystem, and continuous investments in Low Earth Orbit (LEO) platforms, autonomous manufacturing systems, and re-entry logistics technologies.

U.S. In-Space Manufacturing Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 807.0 million in 2026, driven by its highly advanced space infrastructure, strong presence of leading ISM companies, and continuous investments from both NASA and private sector players. Unlike many regions, the U.S. is actively transitioning from research-driven missions to commercially scalable manufacturing operations, supported by initiatives such as the commercialization of low Earth orbit and increased private sector access to orbital platforms. The increasing adoption of in-space manufacturing is particularly evident in areas such as microgravity-enabled material production, pharmaceutical research, and in-orbit fabrication, where performance advantages justify high mission costs.

Europe

The European market is driven by a strong focus on scientific research, advanced materials development, and collaborative space programs, along with increasing participation in commercial in-space manufacturing initiatives across Germany, the U.K., France, Italy, and the Netherlands. Demand for ISM is closely linked to the region’s expertise in precision engineering, pharmaceuticals, and specialty materials, where microgravity conditions can provide measurable performance improvements. European space agencies and industry players are prioritizing the development of interoperable and scalable manufacturing platforms, supported by strong regulatory frameworks and international collaborations.

U.K. In-Space Manufacturing Market

The U.K. market is estimated at around USD 56.6 million in 2026, representing roughly 3.3% of global sales.

Germany In-Space Manufacturing Market

Germany’s market is projected to reach approximately USD 62.7 million in 2026, equivalent to around 3.6% of global sales.

Asia Pacific

Asia Pacific remains the significant growing market, with a valuation of USD 297.3 million in 2025 globally. The region’s growth is driven by strong government-led space programs, increasing investments in orbital infrastructure, and rapid expansion of commercial space capabilities across key economies such as China, India, Japan, South Korea, and Southeast Asian countries. Asia Pacific is emerging as a major hub for in-space manufacturing due to its focus on independent space station development, microgravity research, and long-term space exploration strategies.

China In-Space Manufacturing Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 123.1 million, representing roughly 7.2% of global sales.

Japan In-Space Manufacturing Market

The Japanese market is estimated at around USD 67.0 million in 2026, accounting for roughly 3.9% of the global sales.

India In-Space Manufacturing Market

The Indian market is estimated at around USD 44.7 million in 2026, accounting for roughly 2.6% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in space programs, strategic diversification initiatives, and the gradual development of advanced technological capabilities across GCC countries, Israel, South Africa, and North Africa. Demand for in-space manufacturing in the region is closely linked to government-led space initiatives, scientific research programs, and emerging interest in high-value manufacturing technologies, particularly in areas such as advanced materials and satellite technologies. GCC countries, especially the UAE and Saudi Arabia, are actively investing in space exploration, satellite development, and long-term space economy strategies, aiming to reduce dependence on traditional energy sectors and position themselves in high-technology domains.

GCC In-Space Manufacturing Market

The GCC market is projected to reach around USD 20.6 million in 2026, representing roughly 1.2% of the global sales.

South America

The South America market is driven by growing participation in space research initiatives, increasing government interest in technological advancement, and expanding collaboration with international space agencies across key economies such as Brazil, Argentina, and Chile. Demand for in-space manufacturing in the region is primarily linked to scientific research, satellite development programs, and early-stage exploration of microgravity technologies, rather than large-scale commercial manufacturing activities. Brazil and Argentina represent the leading contributors within the region, supported by their involvement in space research programs and partnerships with global space agencies. These countries are gradually building capabilities in materials science, satellite technologies, and aerospace engineering, which form the foundation for future participation in in-space manufacturing activities.

Brazil In-Space Manufacturing Market

The Brazil market is projected to reach around USD 19.9 million in 2026, representing roughly 1.2% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by Orbital Infrastructure, Microgravity Manufacturing Capabilities, and End-to-End Space Logistics Integration

The in-space manufacturing market is moderately consolidated and rapidly evolving, with competitive positioning driven by access to orbital platforms, proprietary manufacturing technologies, and the ability to integrate end-to-end mission capabilities, including launch, in-orbit production, and re-entry logistics. Leading players such as Redwire Space, Varda Space Industries, Axiom Space, Sierra Space, and Blue Origin maintain strong positions by developing integrated in-space manufacturing ecosystems that combine hardware, software, and operational expertise to enable scalable and repeatable production in microgravity environments.

Competitive differentiation is increasingly shaped by the ability to transition from experimental missions to commercially viable production cycles. Companies are investing in autonomous manufacturing systems, modular orbital platforms, and dedicated re-entry vehicles to improve production efficiency, reduce mission costs, and enable high-frequency manufacturing operations. Unlike traditional space activities, success in this market depends on the ability to control the entire value chain, from raw material deployment to product recovery and commercialization.

- For instance, in December 2023, Thales Alenia Space continued its contribution to ISS infrastructure and next-generation space habitat modules, supporting long-term capabilities for in-orbit manufacturing and research.

LIST OF KEY IN-SPACE MANUFACTURING COMPANIES PROFILED IN REPORT

- Redwire Space (U.S.)

- Varda Space Industries (U.S.)

- Axiom Space (U.S.)

- Sierra Space (U.S.)

- Blue Origin (U.S.)

- Northrop Grumman Corporation (U.S.)

- Space Forge Ltd. (U.K.)

- Airbus SE (Europe)

- Thales Alenia Space (Europe)

- Le Verre Fluoré (France)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Redwire Corporation launched additional colloids experiments to the International Space Station (ISS) aboard a commercial resupply mission, supporting its Colloidal Solids Instrument (COLIS) platform to advance research in material science, drug development, and microgravity-enabled manufacturing processes.

- April 2026: Redwire Corporation, announced a multi-year marketing partnership with the Washington Commanders to support U.S. service members, veterans and their families.

- February 2026: Axiom Space secured USD 350 million in financing to accelerate the development of its commercial space station, aimed at supporting scalable in-orbit manufacturing, research, and industrial activities beyond the ISS.

- January 2026: Varda Space Industries announced the successful reentry of its W-5 capsule, reinforcing its capabilities in orbital pharmaceutical processing and controlled Earth-return logistics for in-space manufactured products.

- January 2026: Sierra Space announced the completion of the first nine satellite structures under the Space Development Agency’s Tranche 2 Tracking Layer program, demonstrating its expanding capabilities in space-based manufacturing and structural production systems.

REPORT COVERAGE

The global in-space manufacturing market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.9% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Manufacturing Type, Operational Platform, Technology, End User, and Region |

| By Manufacturing Type |

|

| By Operational Platform |

|

| By Technology |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value is expected to stand at USD 1,712.9 million in 2026 and is projected to reach USD 5,969.4 million by 2034.

In 2025, the North America’s market value stood at USD 805.4 million.

The market is expected to exhibit a CAGR of 16.9% during the forecast period (2026-2034).

By end user, the government & space agencies segment led the market.

Commercial space infrastructure growth, microgravity materials demand, autonomous manufacturing, lower launch costs, and in-orbit production capabilities are driving market growth.

Redwire Space, Varda Space Industries, Axiom Space, Sierra Space, Blue Origin, Airbus, and Thales Alenia Space are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us