Generative AI in Smart Manufacturing Market Size, Share & Industry Analysis, By Component (Software, Hardware, and Services), By Deployment Mode (Cloud, On-premises, Hybrid, and Edge), By Manufacturing Function (Design & Engineering, Production & Operations, Quality, Maintenance, Supply Chain & Planning, and Others), By Industry Vertical (Automotive & EV, Electronics & Semiconductors, Industrial Machinery, Pharma & Medical Devices, Food & Beverage, and Others), and Regional Forecast, 2026-2034

Generative AI in Smart Manufacturing Market Size and Future Outlook

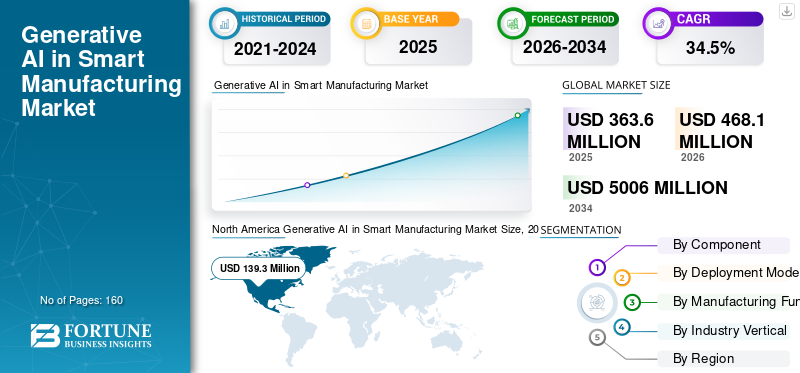

The global generative AI in smart manufacturing market size was valued at USD 363.6 million in 2025. The market is projected to grow from USD 468.1 million in 2026 to USD 5,006.0 million by 2034, exhibiting a CAGR of 34.5% during the forecast period. North America dominated the generative ai in smart manufacturing market with a market share of 38.31% in 2025.

The market is gaining momentum as manufacturers increasingly adopt advanced digital solutions aligned with industry 4.0 initiatives to enhance operational efficiency and competitiveness. Generative AI applications leverage artificial intelligence, machine learning, and sensors data collected from connected equipment to support intelligent decision-making across production environments. These technologies are being applied in areas such as predictive maintenance, advanced vision systems, and process optimization to reduce downtime and improve quality consistency. By enabling data-driven insights and adaptive production workflows, generative AI is playing a growing role in improving productivity and supporting the transition toward more autonomous and resilient smart factories.

Key players such as Siemens, SAP, Microsoft, NVIDIA, and IBM are actively expanding industrial AI platforms, digital twin capabilities, and manufacturing-focused generative AI tools to strengthen market presence and accelerate enterprise deployments.

Download Free sample to learn more about this report.

GENERATIVE AI IN SMART MANUFACTURING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 363.6 million

- 2026 Market Size: USD 468.1 million

- 2034 Forecast Market Size: USD 5,006.0 million

- CAGR: 34.50% from 2026–2034

- North America dominated the market with a 38.31% share in 2025.

- The Production & Operations segment is expected to hold the largest market share in 2025.

- The Software segment is expected to dominate the market in 2025.

North America

The market reached USD 139.3 million in 2025 and is driven by early AI adoption, advanced smart manufacturing infrastructure, and strong industrial software ecosystems.

Asia Pacific

The market is projected to reach USD 140.4 million in 2026, supported by rapid industrialization and growing investments in AI-powered smart factories.

Europe

The market is projected to reach USD 115.5 million in 2026, fueled by digital transformation and increasing adoption of AI across manufacturing industries.

U.S.

The market is projected to reach USD 154.1 million by 2026, driven by strong investments in AI research and smart factory technologies.

Japan

The market is projected to reach USD 26.5 million by 2026, supported by increasing adoption of generative AI for manufacturing optimization.

Read More

GENERATIVE AI IN SMART MANUFACTURING MARKET TRENDS

Rapid Integration of Generative AI with Digital Twins and Smart Factory Platforms is a Key Market Trend

The current market demonstrates a continuing trend toward combining digital twins, industrial IoT platforms, and manufacturing execution systems to create adaptable, data-driven production environments. In addition, the usage of generative models in manufacturing includes an increasing reliance on simulation of production scenarios (e.g., using a generative model to simulate how a certain production setup would work) to produce optimal design variations, as well as to generate synthetic data sets for use in creating high-vision quality systems. Factories are moving from descriptive analytics to prescriptive and/or generative decision-making by making use of these capabilities. This trend can be observed most strongly within advanced manufacturing centers where smart factories are transitioning from implementations at a pilot level, to full deployment across all enterprises.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Demand for Operational Efficiency and Intelligent Automation is Driving Market Growth

Improving productivity and reducing downtime through efficient resource utilization continue to drive market growth. In light of increased pressures from manufacturers (due to difficulty managing complex production environments, needy consumers, and the inability to find qualified personnel) to keep their production operations efficient and profitable, generative AI offers advanced solutions in areas such as automated process optimization, predictive scenario generation and intelligent production planning. These advanced technologies allow for rapid decision-making and improved operational resilience, thus generative AI is positioned as a logical extension of current smart manufacturing initiatives.

- For instance, industrial automation providers and cloud platforms increasingly promote generative AI tools for production optimization and predictive operations as part of broader smart manufacturing initiatives.

MARKET RESTRAINTS

Data Readiness, Security Concerns, and Integration Complexity May Limit Adoption

Despite strong growth potential, adoption of generative AI in smart manufacturing can be constrained by data readiness challenges, cybersecurity concerns, and integration complexity. Manufacturing environments often operate with fragmented data sources, legacy systems, and strict security requirements, which can complicate deployment of generative AI solutions. Concerns related to intellectual property protection, model reliability, and regulatory compliance may also slow adoption, particularly in regulated industries. These factors can delay large-scale implementation beyond pilot projects and hinder generative AI in smart manufacturing market growth.

- Industry discussions frequently highlight the importance of strong data governance and secure system integration to support trusted deployment of generative AI in manufacturing.

MARKET OPPORTUNITIES

Expansion of Generative AI into Core Production and Planning Functions Creates Long-Term Opportunities

The expansion of generative AI beyond design and analytics into core production, maintenance, and supply chain planning functions presents significant growth opportunities. As trust in generative models improves, manufacturers are expected to deploy these solutions for real-time production adjustments, intelligent maintenance recommendations, and scenario-based supply planning. The growing availability of cloud computing, edge AI infrastructure, and manufacturing data platforms further supports scalable deployment across multiple plants. Over the long term, generative AI is expected to become a foundational intelligence layer within smart manufacturing ecosystems.

- For example, cloud service providers continue to expand generative AI capabilities tailored for industrial and manufacturing workloads.

Segmentation Analysis

By Manufacturing Function

Production and Operations Dominate with Focus on Real-Time Optimization

Based on manufacturing function, the market is divided into design & engineering, production & operations, quality, maintenance, supply chain & planning, and others.

In 2025, production & operations accounted for the highest generative AI in smart manufacturing market share. Generative AI is increasingly applied to optimize production scheduling, reduce bottlenecks, and improve equipment utilization. These use cases deliver direct operational benefits, making them a priority for manufacturers scaling generative AI adoption beyond experimentation.

- Manufacturers are increasingly applying AI-driven optimization tools to support adaptive production environments and improve throughput.

The supply chain & planning segment is anticipated to rise with a CAGR of 35.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Software Holds Largest Share Due to Early Adoption of AI Platforms and Applications

Based on component, the market is segmented into software, hardware, and services.

In 2025, the software segment accounted for the highest share of the market. Software platforms form the core of generative AI deployments, enabling model development, simulation, analytics, and integration with existing manufacturing systems. Early adoption has been driven by cloud-based AI platforms and industrial software suites that allow manufacturers to experiment with generative use cases without large upfront hardware investments.

- For example, industrial software providers are embedding generative AI capabilities into manufacturing analytics and digital twin platforms.

The services segment is expected to grow at a CAGR of 35.1% over the forecast period.

By Deployment Mode

Cloud Deployment Leads Due to Scalability and Lower Entry Barriers

Based on deployment mode, the market is segmented into cloud, on-premises, hybrid, and edge.

In 2025, the cloud segment held the highest share of the market. Cloud-based deployment enables scalable computing resources, faster model training, and easier integration with enterprise systems. Manufacturers increasingly rely on cloud platforms to deploy generative AI applications across multiple sites while reducing infrastructure complexity and capital expenditure.

- For instance, leading cloud providers continue to expand AI services specifically designed for manufacturing and industrial workloads.

The edge segment is expected to grow at a CAGR of 36.4% over the forecast period.

By Industry Vertical

Industrial Machinery Leads Adoption Due to Complex and Custom Manufacturing Requirements

Based on industry vertical, the market is segmented into automotive & EV, electronics & semiconductors, industrial machinery, pharma & medical devices, food & beverage, and others.

In 2025, the industrial machinery segment held the highest share. This segment often involves complex, high-mix manufacturing processes that benefit significantly from generative design, simulation, and production optimization. The need to manage customization, engineering complexity, and operational efficiency is driving early and sustained adoption of generative AI solutions.

- Industrial machinery manufacturers increasingly deploy advanced digital tools to optimize design and production workflows.

The electronics & semiconductors segment is expected to grow at a CAGR of 36.8% over the forecast period.

Generative AI in Smart Manufacturing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Generative AI in Smart Manufacturing Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held a dominant position in the market in 2024 and continued to maintain its leading share in 2025, with a market valuation of USD 139.3 million. The region benefits from early adoption of AI technologies, strong presence of industrial software providers, and advanced smart manufacturing infrastructure. Manufacturers across the region are actively integrating generative AI into production, design, and planning workflows to enhance efficiency and competitiveness.

U.S. Generative AI in Smart Manufacturing Market

The U.S. market is estimated at around USD 154.1 million in 2026. The market is supported by strong investment in AI research, advanced manufacturing, and widespread deployment of smart factory technologies across automotive, industrial machinery, and electronics sectors.

Europe

Europe to record a market valuation of USD 115.5 million in 2026. Europe market growth is driven by strong industrial bases and ongoing digital transformation initiatives. Countries such as Germany, France, and Italy are increasingly adopting generative AI to enhance production efficiency, support sustainability goals, and improve manufacturing flexibility.

U.K. Generative AI in Smart Manufacturing Market

The U.K. market is estimated at around USD 16.3 million in 2026, representing roughly 3.5% of global revenues.

Germany Generative AI in Smart Manufacturing Market

Germany’s market is projected to reach USD 30.1 million in 2026, equivalent to around 6.4% of global sales.

Asia Pacific

Asia Pacific to record a market valuation of USD 140.4 million in 2026. Regional market supported by rapid industrialization, expansion of smart factories, and increasing adoption of AI across manufacturing industry. China, Japan, South Korea, and India are investing in generative AI to support large-scale manufacturing optimization and advanced production planning.

Japan Generative AI in Smart Manufacturing Market

The Japan market is estimated at around USD 26.5 million in 2026, accounting for roughly 5.7% of global revenue.

China Generative AI in Smart Manufacturing Market

The China market is estimated at around USD 49.2 million in 2026, accounting for roughly 10.5% of global revenue.

India Generative AI in Smart Manufacturing Market

The Indian market is estimated at around USD 16.5 million in 2026, accounting for roughly 5.7% of global market.

South America and Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. South America is projected to reach a market valuation of USD 20.9 million in 2026. Growth in the region is driven by gradual modernization of manufacturing facilities and increasing awareness of AI-enabled production optimization, particularly in Brazil and other emerging industrial markets.

The Middle East & Africa market is expected to reach a valuation of USD 11.7 million in 2026. Investments in industrial diversification, digital transformation, and smart manufacturing initiatives are supporting gradual adoption of generative AI solutions across selected manufacturing hubs.

GCC Generative AI in Smart Manufacturing Market

The GCC market is projected to reach around USD 4.9 million in 2026, representing roughly 1.0% of global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Industrial AI Platforms, Digital Twins, and Scalable Deployment to Strengthen Market Position

Emerging generative AI technologies are gaining momentum & becoming increasingly competitive in smart manufacturing, with participants from the industrial software, cloud hyperscaler & AI technology industries. Industry leaders including Siemens, SAP, Microsoft, NVIDIA, and IBM are well-positioned due to their ability to combine their experience in combining existing industrial software, using cloud infrastructure to extend generative AI capabilities; as well as their expertise within the manufacturing domain. Manufacturers building on the use of generative AI are leveraging existing digital twin platforms, manufacturing execution systems, and industrial analytics tools to improve design optimization, production planning (or quality of production) & improve maintenance decision making. Strategically, partnerships between industrial automation companies & cloud or AI specialists will help accelerate the commercialization & scaling of generative AI solutions throughout the entire manufacturing environment. As generative AI is becoming more widely adopted and transitioned out of pilot status into production environments, emphasis on data security, model governance and enterprise level deployment will become increasingly important for differentiation.

LIST OF KEY GENERATIVE AI IN SMART MANUFACTURING COMPANIES PROFILED IN REPORT

- Siemens AG (Germany)

- SAP SE (Germany)

- Microsoft Corporation (U.S.)

- IBM Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Dassault Systèmes SE (France)

- PTC Inc. (U.S.)

- Oracle Corporation (U.S.)

- Accenture plc (Ireland)

- Rockwell Automation, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2024: IBM highlighted new generative AI use cases for industrial clients focused on predictive operations, maintenance recommendations, and production optimization within smart manufacturing environments.

- February 2024: SAP announced enhancements to its AI and generative AI roadmap aimed at embedding intelligent assistants and decision-support capabilities into manufacturing and supply chain applications.

- January 2024: Microsoft expanded Azure OpenAI Service availability for enterprise and industrial customers, supporting integration of generative AI into manufacturing analytics and operations workflows.

- November 2023: NVIDIA introduced new generative AI tools and frameworks for industrial digital twins, enabling manufacturers to simulate and optimize factory operations using AI-generated scenarios.

- October 2023: Siemens announced the expansion of generative AI capabilities within its industrial software portfolio to support design optimization, engineering productivity, and manufacturing simulation use cases.

REPORT COVERAGE

The global generative AI in smart manufacturing market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details strategic partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 34.5% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Component, Deployment Mode, Manufacturing Function, Industry Vertical, and Region |

| By Component |

|

| By Deployment Mode |

|

| By Manufacturing Function |

|

| By Industry Vertical |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 363.6 million in 2025 and is projected to reach USD 5,006.0 million by 2034.

In 2025, the North Americas market value stood at USD 139.3 million.

The market is expected to exhibit a CAGR of 34.5% during the forecast period of 2026-2034.

By manufacturing function, the production & operations segment is expected to lead the market.

The market is being driven by manufacturers’ need to boost operational efficiency, reduce downtime, and manage complex production challenges through intelligent automation powered by generative AI.

Siemens, SAP, Microsoft, NVIDIA, and IBM are the major players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us