Industry 4.0 in Aerospace and Defense Market Size, Share & Industry Analysis, By Technology (IoT, AI & ML, Digital Twin, Big Data & Advanced Analytics, Robotics & Automation, and Others), By Component (Hardware, Software, and Services), By Application (Manufacturing & Assembly, Predictive Maintenance, Quality Control & Inspection, Supply Chain & Logistics, and Others), and Regional Forecast, 2026-2034

Industry 4.0 in Aerospace and Defense Market Size and Future Outlook

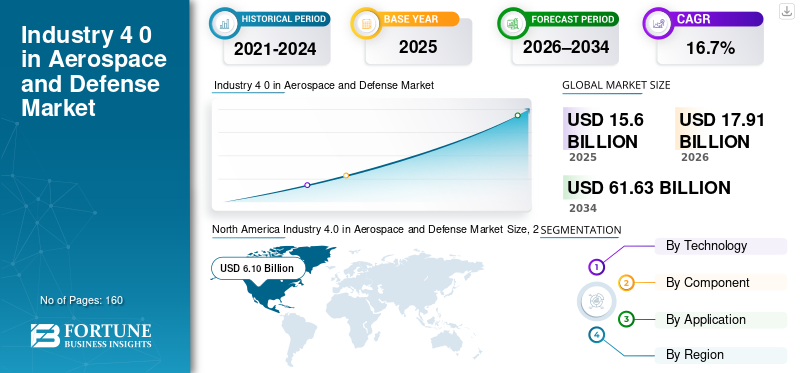

The global Industry 4.0 in aerospace and defense market size was valued at USD 15.60 billion in 2025. The market is projected to grow from USD 17.91 billion in 2026 to USD 61.63 billion by 2034, exhibiting a CAGR of 16.7% during the forecast period. North America dominated the industry 4.0 in aerospace and defense market with a market share of 39.1% in 2025.

The market is gaining traction as organizations pursue digitally transformed operations to achieve improved safety, higher efficiency, and better program execution across complex environments. Industry 4.0 solutions support aircraft design, manufacturing and operating activities by integrating advanced digital technologies such as the Internet of Things, artificial intelligence, and analytics into production processes. These technologies enable real-time insights from data collected across factories and operational assets, supporting optimization of production processes, quality control, and predicting maintenance needs. Adoption is further supported by modernization initiatives led by the Department of Defense, which emphasize digital engineering and lifecycle management across key areas of aerospace and defense operations.

Key players, including Siemens, Dassault Systèmes, Rockwell Automation, and Honeywell, are actively expanding Industry 4.0 platforms and smart manufacturing solutions to support advanced aerospace programs and defense modernization efforts.

Download Free sample to learn more about this report.

INDUSTRY 4.0 IN AEROSPACE AND DEFENSE MARKET Key Takeaways

- 2025 Market Size: USD 15.60 billion

- 2026 Market Size: USD 17.91 billion

- 2034 Forecast Market Size: USD 61.63 billion

- CAGR: 16.7% from 2026–2034

- North America dominated the Industry 4.0 in aerospace and defense market with a market share of 39.1% in 2025.

- In 2025, the IoT segment accounted for the highest Industry 4.0 in aerospace and defense market share.

- In 2025, the hardware segment held the largest market share.

North America

The market reached USD 6.10 billion in 2025, supported by strong defense spending, advanced digital manufacturing, and continued investments in smart factory technologies.

Europe

Europe recorded a market valuation of USD 4.77 billion in 2026, supported by strong aerospace manufacturing capabilities and increasing investments in digital transformation initiatives.

Asia Pacific

Asia Pacific is expected to reach a market valuation of USD 4.37 billion in 2026, emerging as the fastest-growing region in the market.

U.S.

The market is estimated at USD 6.20 billion in 2026, supported by large-scale defense programs, digital engineering initiatives, and widespread Industry 4.0 adoption.

Japan

The market is estimated at USD 0.68 billion in 2026, accounting for approximately 3.8% of global revenue, driven by investments in digital production systems and smart aerospace manufacturing.

Read More

INDUSTRY 4.0 IN AEROSPACE AND DEFENSE MARKET TRENDS

Expansion of Smart Factory and Digital Thread Programs is a Key Market Trend

Industry 4.0 adoption in aerospace and defense is increasingly centered on smart factory deployments that connect design, manufacturing, supply chain, and in-service support through a unified digital thread. Companies are scaling connected machines, automation, and data-driven production systems to improve traceability, quality, and throughput across complex build programs. The integration of digital twins, real-time analytics, and connected robotics is enabling higher production consistency and faster issue resolution across aerospace manufacturing environments.

- For instance, Airbus outlines its Industry 4.0 approach around building a smart factory ecosystem with connected equipment, robotics, and AI integrated with shopfloor operations.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Defense Digital Engineering Mandates and Faster Development Cycles are Driving Market Growth

Digital engineering is becoming increasingly important in many aspects of defense acquisition and modernization programs within the aerospace and defense industry. Digital engineering policies are driving programs toward more model-based practices, digital threads, and lifecycle data standards earlier in the acquisition process, which is accelerating demand for connected platforms and analytics-enabled workflows. Concurrently, the increased pressure to shorten development times and reduce cost overruns has intensified the movement toward more digitally enabled manufacturing and validation processes.

- For example, the U.S. DoD’s Digital Engineering instruction issued in December 2023 formalizes guidance for implementing digital engineering capabilities across the program lifecycle.

MARKET RESTRAINTS

Cybersecurity, Data Restrictions, and Legacy System Integration Constraints Limit Adoption

Aerospace and defense organizations face constraints related to security requirements, restricted data environments, and the difficulty of integrating Industry 4.0 technologies with legacy engineering and manufacturing systems. Many deployments remain function-specific rather than enterprise-wide due to technology readiness gaps, interoperability challenges, and the pace of change management in regulated environments. Additionally, concerns around data sovereignty, intellectual property protection, and compliance slow the rollout of cloud-based and connected solutions.

- Industry analysis indicates that broader enterprise-wide Industry 4.0 adoption in A&D has been slow for many organizations due to technology readiness and organizational capability challenges.

MARKET OPPORTUNITIES

Private 5G, Real-Time Visibility, and Predictive Maintenance to Create New Growth Opportunities

Private 5G networks and increasing implementations of predictive maintenance are creating significant opportunities for Industry 4.0 solutions within the aerospace and defense sectors. Higher levels of connectivity will enable factories to capture real-time data more effectively, improve part traceability, provide augmented work instructions, and use predictive maintenance techniques at the asset level, leading to increased production efficiency and higher levels of product quality throughout factory operations. These new capabilities are particularly beneficial in high-mix, low-volume aerospace manufacturing, which frequently contains a significant degree of complexity with regard to compliance.

- For example, in October 2025, Airbus deployed a private 5G network at several of its manufacturing facilities in Canada, while Ericsson has supported Airbus’ digitalization efforts through the implementation of Private LTE networks for the purposes of enabling improved traceability and predictive maintenance.

Segmentation Analysis

By Technology

IoT Segment Held the Largest Share, Driven by its Widespread Use in Connecting Machines

Based on technology, the market is divided into IoT, AI & ML, digital twin, big data & advanced analytics, robotics & automation, and others.

In 2025, the IoT segment accounted for the highest industry 4.0 in aerospace and defense market share. The dominance of IoT is driven by its widespread use in connecting machines, tools, and production assets across aerospace manufacturing environments. IoT enables real-time monitoring of equipment performance, production status, and quality metrics, supporting improved operational visibility and traceability. Aerospace and defense manufacturers increasingly deploy IoT platforms to integrate shopfloor data with enterprise systems, supporting smart factory and digital thread initiatives.

- For example, as per industry reports, Airbus implemented IoT-enabled connected factories to enhance production monitoring and operational efficiency across multiple manufacturing sites.

The digital twin segment is anticipated to rise with a CAGR of 17.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Hardware Segment Led Due to the Extensive Deployment of Industrial Sensors

Based on component, the market is segmented into hardware, software, and services.

In 2025, the hardware segment held the largest market share, supported by large-scale deployment of industrial sensors, connected machines, robotics, and automation systems across aerospace and defense facilities. Hardware forms the foundational layer of Industry 4.0 implementations, enabling data collection from production equipment, tools, and assets. Investments in smart machines, automated assembly systems, and industrial networking infrastructure continue to drive hardware demand as manufacturers modernize legacy production lines and expand capacity.

- For instance, companies such as Siemens and Rockwell Automation supply industrial hardware platforms widely used in aerospace smart manufacturing

The software segment is projected to grow at a CAGR of 17.1% over the forecast period.

By Application

Manufacturing and Assembly Segment Dominates due to the incorporation of Industry 4.0 Technologies Improve Production Efficiency

Based on application, the market is segmented into manufacturing & assembly, predictive maintenance, quality control & inspection, supply chain & logistics, and others.

In 2025, the manufacturing and assembly segment accounted for the highest share of the market. Aerospace and defense manufacturers are prioritizing Industry 4.0 technologies to improve production efficiency, reduce defects, and manage complex assembly processes. Digital work instructions, connected tools, robotics, and real-time production analytics are increasingly integrated into assembly lines to enhance throughput and ensure compliance with strict quality standards.

- For example, in March 2025, Boeing adopted digital manufacturing and assembly solutions to improve production accuracy and reduce rework in aircraft assembly programs.

The predictive maintenance segment is projected to grow at a CAGR of 17.5% over the forecast period.

Industry 4.0 in Aerospace and Defense Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Industry 4.0 in Aerospace and Defense Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held a dominant position in the market in 2024 and continued to maintain its leading share in 2025, with a market valuation of USD 6.10 billion. The region’s leadership is supported by early adoption of advanced digital manufacturing processes, strong defense spending, and the presence of major aerospace and defense manufacturers. Companies across the region are investing heavily in smart factories, digital engineering, connected production systems, and predictive maintenance solutions to improve operational efficiency and program execution.

U.S. Industry 4.0 in Aerospace and Defense Market

Based on North America’s strong contribution and the dominance of the U.S. within the region, the U.S. market is analytically estimated at around USD 6.20 billion in 2026. The country’s market is driven by large-scale defense programs, digital engineering mandates, and widespread deployment of Industry 4.0 solutions across aerospace manufacturing and maintenance operations.

Europe

Europe recorded a market valuation of USD 4.77 billion in 2026. The regional market is supported by strong aerospace manufacturing capabilities and increasing investments in digital transformation initiatives. Countries such as Germany, France, and the U.K. are actively deploying smart manufacturing, digital twin, and automation technologies to improve production efficiency and quality controls across aerospace programs.

U.K. Industry 4.0 in Aerospace and Defense Market

The U.K. market in 2026 is estimated at around USD 0.84 billion, representing roughly 4.7% of global revenues.

Germany Industry 4.0 in Aerospace and Defense Market

Germany’s market is projected to reach USD 1.01 billion in 2026, equivalent to around 5.7% of global sales.

Asia Pacific

Asia Pacific is expected to reach a market valuation of USD 4.37 billion in 2026, emerging as the fastest-growing region in the market. Strong growth is driven by expanding aerospace manufacturing capacity, rising defense budgets, and increasing adoption of advanced manufacturing technologies. Countries such as China, India, Japan, and South Korea are investing in digital production systems and smart maintenance solutions to strengthen domestic aerospace and defense capabilities.

Japan Industry 4.0 in Aerospace and Defense Market

The Japanese market in 2026 is estimated at around USD 0.68 billion, accounting for roughly 3.8% of global revenue.

China Industry 4.0 in Aerospace and Defense Market

The Chinese market in 2026 is estimated at around USD 1.48 billion, accounting for roughly 8.3% of the global market.

India Industry 4.0 in Aerospace and Defense Market

The Indian market in 2026 is estimated at around USD 0.91 billion, accounting for roughly 5.1% of the global market.

South America and the Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. South America is projected to reach a market valuation of USD 0.83 billion in 2026. Regional Industry 4.0 in aerospace and defense market growth is supported by the gradual modernization of aerospace manufacturing facilities and increasing interest in digital maintenance and supply chain solutions, particularly in Brazil. The Middle East & Africa market is expected to reach a valuation of USD 0.91 billion in 2026. Investments in defense modernization, aerospace manufacturing, and technology diversification initiatives are supporting the emerging adoption of Industry 4.0 solutions across selected countries, particularly within the GCC.

GCC Industry 4.0 in Aerospace and Defense Market

The GCC market is projected to reach around USD 0.41 billion in 2026, representing roughly 2.3% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Digital Engineering Platforms and Smart Manufacturing Solutions to Strengthen their Market Position

The market is moderately consolidated and contains global technology providers, industrial automation firms, and specialized digital engineering companies. Leading players in the industry, such as Siemens, Dassault Systèmes, Rockwell Automation, and Honeywell have a strong position in the aerospace and defense markets with comprehensive portfolios of digital twins, IoT platforms, advanced analytics, and other automation solutions designed to meet the aerospace and defense industry's needs. These companies also have long-standing relationships with aerospace manufacturers, defense contractors, and government agencies, allowing for deep integration of Industry 4.0 solutions across production, maintenance, and lifecycle management processes. Increasing numbers of market participants are focusing on developing secure digital engineering platforms, deploying smart factories, and implementing predictive maintenance solutions to help address the complex compliance, quality, and security requirements found within the aerospace and defense industry.

LIST OF KEY INDUSTRY 4.0 IN AEROSPACE AND DEFENSE COMPANIES PROFILED

- ABB (Switzerland)

- Dassault Systèmes (France)

- GE Aerospace (U.S.)

- Honeywell (U.S.)

- IBM (U.S.)

- Lockheed Martin (U.S.)

- Microsoft (U.S.)

- PTC (U.S.)

- Rockwell Automation (U.S.)

- Siemens (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Axiscades Technologies formed a strategic partnership with OGMA (Embraer subsidiary) to jointly develop aerospace manufacturing, maintenance, and engineering services for commercial and military aircraft.

- January 2026: Adani Defence & Aerospace and Embraer signed a MoU partnership to develop a regional transport aircraft ecosystem in India, including manufacturing, supply chain, and pilot training collaborations.

- November 2025: Bharat Electronics Limited (BEL) and Safran Electronics & Defence launched an equal-share joint venture to manufacture HAMMER precision-guided weapons domestically, strengthening localized defense production.

- October 2025: Airbus, Thales, and Leonardo agreed to merge their space operations under a new joint initiative aimed at boosting European aerospace competitiveness and innovation.

- July 2025: Defense-tech startup Hadrian raised USD 260 million in investment to build a robot-powered factory for aerospace and defense components, expanding automated manufacturing capacity.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.7% from 2026 t2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology, Component, Application, and Region |

|

By Technology |

|

|

By Component |

|

|

By Application |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 15.60 billion in 2025 and is projected to reach USD 61.63 billion by 2034.

In 2025, the market value stood at USD 6.10 billion.

The market is expected to exhibit a CAGR of 16.7% during the forecast period (2026-2034).

By application, the manufacturing & assembly segment led the market.

Defense digital engineering mandates and faster development cycles are the key factors driving market growth.

Siemens, Dassault Systèmes, Rockwell Automation, and Honeywell are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us