In-Vehicle AI Assistants Market Size, Share & Industry Analysis, By Technology Type (Voice Recognition Assistants, NLP-based Assistants, AI-based Personalization Systems, and Hybrid AI Assistants), By Vehicle Type (Passenger Vehicles and Commercial Vehicles), By Level of Integration (Embedded AI Assistants, Cloud-based AI Assistants), By Application (Infotainment & Media Control, Navigation & Traffic Assistance, Vehicle Control, Driver Assistance & Safety Alerts, and Personalization & User Profiling), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026–2034

In-Vehicle AI Assistants Market Size and Future Outlook

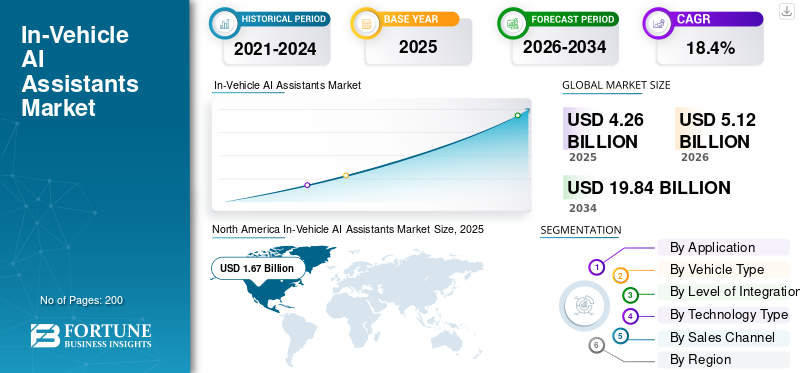

The in-vehicle AI assistants market size was valued at USD 4.26 billion in 2025. The market is projected to grow from USD 5.12 billion in 2026 to USD 19.84 billion by 2034, exhibiting a CAGR of 18.4% during the forecast period. North America dominated the in-vehicle ai assistants market with a market share of 39.2% in 2025.

In-vehicle AI assistants are AI-powered digital systems integrated into connected vehicles, enabling voice interaction, navigation, infotainment control, and driver assistance using speech recognition, natural language processing, and real-time data processing. Market growth is driven by rising demand for connected vehicles, increasing adoption of AI-powered voice assistants, advancements in autonomous vehicles and ADAS, and growing need for enhanced in-car user experience and safety features.

Major players in the market include Amazon.com, Inc., Google LLC, Microsoft Corporation, Cerence Inc., SoundHound AI, Inc., and Apple Inc., competing through AI-powered voice assistants, advanced speech recognition, cloud-based integration, and enhanced in-vehicle user experience solutions.

Download Free sample to learn more about this report.

IN-VEHICLE AI ASSISTANTS MARKET TRENDS

Rising Integration of AI-Powered Voice Interaction in Vehicles is Major Market Trend

One of the market trend is the growing integration of AI powered voice assistants, enabling seamless voice interaction within vehicles. Automakers are focusing on enhancing user experience through hands-free control of navigation, infotainment, and climate systems. Advanced speech recognition and natural language processing technologies are improving accuracy and responsiveness, making in-vehicle AI assistants more intuitive. This trend is further supported by the shift toward connected vehicles and digital ecosystems, where voice-based interfaces are becoming a primary mode of human-machine interaction.

- In July 2025, Mahindra partnered with Cerence Inc. to integrate Cerence Audio AI into its electric-origin SUVs, BE 6 and XEV 9e, enhancing in-car voice interaction through advanced speech signal enhancement, noise cancellation, and AI-driven infotainment systems for improved user experience.

Expansion of Cloud-Based Digital Ecosystems in the Automotive Industry Drives Market Growth

Another significant trend is the increasing adoption of cloud based platforms that support AI-driven functionalities in vehicles. These systems enable real-time data processing, continuous updates, and integration with broader digital ecosystems. Automakers and tech companies are leveraging cloud infrastructure to enhance the personalization and predictive capabilities of artificial intelligence AI assistants. This trend supports scalability and allows seamless integration with external services such as smart homes and mobile devices, strengthening the market growth and positioning AI assistants as central components of next-generation mobility solutions.

- In March 2026, Visteon partnered with NVIDIA to launch an edge-to-cloud AI platform for software-defined vehicles, enabling real-time workload optimization, enhanced data governance, and scalable deployment of AI driven in-vehicle assistants with improved personalization and performance.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Enhanced In-Car User Experience Drives Product Adoption

The growing demand for improved in-car user experience is a major driver of market growth. Consumers increasingly expect personalized, intuitive, and convenient interactions within vehicles, similar to smartphones and smart devices. AI assistants provide features such as contextual recommendations, real-time navigation updates, and voice-enabled controls, enhancing comfort and safety. This shift in consumer expectations is encouraging automakers to integrate AI-driven solutions, thereby accelerating adoption across both passenger cars and commercial vehicles and contributing significantly to in-vehicle AI assistants market growth.

- In February 2025, Stellantis partnered with Mistral AI to develop an AI-powered in-car assistant using large language models, enabling natural voice interaction, real-time driver support, improved vehicle development, and enhanced customer experience.

Increasing Adoption of Connected and Autonomous Vehicles Fuels Market Growth

The rapid adoption of connected vehicles and advancements in autonomous vehicles are other drivers of the market. These vehicles rely heavily on AI assistants to manage communication, navigation, and system controls. Integration with Advanced Driver Assistance Systems (ADAS) further enhances the role of AI assistants in improving safety and driving efficiency. As automotive technology evolves, the reliance on intelligent, AI-powered interfaces continues to grow, creating sustained demand and driving innovation in in-vehicle assistant technologies globally.

- In October 2025, General Motors announced advancements in conversational AI, eyes-off driving, and a unified software platform, enabling intelligent in-vehicle assistants, enhanced autonomy, real-time personalization, and continuous over-the-air updates for improved driving experience.

MARKET RESTRAINTS

High Development Costs and Integration Complexities Limit Adoption

A major restraint in the market is the high cost associated with developing and integrating advanced AI-powered systems. Implementing accurate voice recognition, multilingual capabilities, and seamless system compatibility requires significant investment in software and hardware. Additionally, integration across diverse vehicle platforms poses technical challenges. These factors can limit adoption, particularly among mid-range vehicle segments, slowing down overall market growth despite increasing demand for advanced AI assistant features.

MARKET OPPORTUNITIES

Rising Demand for Multilingual and Personalized AI Assistants Creates Opportunities

The increasing need for multilingual support and personalized interactions presents a strong opportunity in the market. As vehicles are sold globally, AI assistants must cater to diverse languages and cultural preferences. Advanced speech recognition and natural language processing enable customized responses and adaptive learning based on user behavior. This enhances user experience and expands adoption across emerging markets, especially in regions like the Asia Pacific and the Middle East, where linguistic diversity drives demand for more inclusive AI solutions.

- In April 2026, BYD partnered with Cerence AI to deploy next-generation in-car AI assistants across its global fleet, leveraging an LLM-powered xUI platform to enable conversational voice interaction, multilingual support, and scalable AI-driven user experiences.

Integration with Smart Devices and IoT Ecosystems Unlocks New Growth Avenues

The integration of in-vehicle AI assistants with smart devices and IoT ecosystems offers significant growth opportunities. AI assistants can connect with smartphones, home automation systems, and wearable devices, creating a seamless digital environment. This connectivity enhances convenience through synchronized data and remote vehicle control features. As AI-driven digital ecosystems expand, this integration strengthens the value proposition of in-vehicle assistants, increasing their relevance and supporting long-term market growth and innovation.

- In April 2026, AROBS introduced an AI-ready cockpit domain controller with an integrated automotive AI assistant, enabling context-aware interaction, multimodal inputs, predictive intelligence, and unified control of infotainment and vehicle systems to enhance user experience.

MARKET CHALLENGES

Data Privacy and Cybersecurity Concerns Pose Significant Challenges

One of the primary challenges in the market is addressing data privacy and cybersecurity risks. AI assistants process large volumes of personal and vehicle data, raising concerns about data protection and unauthorized access. Ensuring compliance with global regulations and maintaining secure communication channels is critical. These challenges can impact consumer trust and slow adoption, requiring continuous investment in secure architectures and robust data management practices to sustain product demand and long-term growth.

Segmentation Analysis

By Application

Demand for advanced Infotainment Integration and Voice Interaction Boosts Segment Growth

Based on application, the market is segmented into infotainment & media control, navigation & traffic assistance, vehicle control, driver assistance & safety alerts, and personalization & user profiling.

The infotainment & media control segment dominates the market due to widespread integration of AI-powered voice assistants in connected vehicles. High consumer preference for seamless voice interaction, entertainment streaming, and real-time content access enhances user experience. Automakers prioritize infotainment systems as central digital interfaces, driving strong market demand across passenger vehicles. Continuous upgrades in speech recognition, natural language processing, and cloud-based services further sustain its leading market share globally.

- In December 2025, Pioneer Corporation partnered with Microsoft to develop an AI-powered in-vehicle infotainment agent using cloud and generative AI technologies, enabling natural voice interaction, seamless system integration, and enhanced user experience across vehicle segments.

The personalization & user profiling segment is projected to grow at a CAGR of 21.1% during the forecast period. Increasing demand for AI-driven customized experiences, adaptive interfaces, and predictive assistance is accelerating adoption, especially across premium and autonomous vehicles, enhancing long-term market growth.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

High Adoption of Connected Features and AI Integration Drives Passenger Vehicles Segment Demand

Based on vehicle type, the market is segmented into passenger vehicles and commercial vehicles.

The passenger vehicles dominate the market and is also the fastest growing segment, driven by high adoption of AI-powered in-vehicle assistants across premium and mid-range cars. Increasing demand for enhanced user experience, seamless voice interaction, and smart infotainment systems is accelerating integration. The rapid expansion of connected vehicles, electric mobility, and ADAS further strengthens market growth, enabling higher market share across market.

The commercial vehicles segment is projected to grow at a CAGR of 17.3% during the forecast period. Growing fleet digitalization, logistics optimization, and increasing demand for AI-driven navigation and safety solutions are supporting adoption across trucks and buses.

- In January 2024, Ceva expanded its AI ecosystem through partnerships with Visionary.ai and ENOT.ai, enhancing automotive AI assistants with advanced edge processing, real-time vision capabilities, and improved safety features for intelligent driving systems.

By Level of Integration

OEM Integration and Seamless System Control Strengthen Embedded AI Assistants Segment Growth

Based on the level of integration, the market is segmented into embedded (OEM-installed) AI assistants, cloud-based AI assistants, and hybrid (edge + cloud) assistants.

The embedded (OEM-installed) AI assistants segment holds the largest in-vehicle AI assistants market share due to direct integration into vehicle systems, enabling faster response times and reliable voice interaction without connectivity dependency. Automakers prefer embedded solutions for enhanced safety, real-time control, and seamless compatibility with ADAS. Strong adoption across connected vehicles and premium models further supports consistent demand and long-term market growth.

- In August 2025, DTEC expanded its smart mobility ecosystem by collaborating with Mercedes-Benz, Hyundai, Renault, and Ford, deploying AI-powered in-vehicle assistants with multilingual voice interaction, IoT integration, and blockchain-enabled data systems for enhanced user experience.

The hybrid (edge + cloud) assistants segment is projected to grow at a CAGR of 19.8% during the forecast period. Increasing need for real-time processing combined with cloud scalability is driving adoption, enhancing performance, personalization, and continuous updates in AI-powered automotive ecosystems.

By Technology Type

High Demand for Hands-Free Interaction and Safety Enhances Voice Recognition Assistants Development

Based on technology type, the market is segmented into voice recognition assistants, NLP-based assistants, AI-based personalization systems, and hybrid AI assistants.

The voice recognition assistants segment holds the largest market share due to rising demand for seamless voice interaction and hands-free vehicle control. Increasing integration of speech recognition and natural language processing improves command accuracy and enhances user experience. Automakers are prioritizing voice-enabled systems across connected vehicles to support navigation, infotainment, and safety functions, thereby continuous market growth globally.

- In April 2025, Kia launched its generative AI-powered voice assistant across Europe, enabling natural voice interaction, enhanced vehicle control, and continuous over-the-air updates to improve connectivity, functionality, and overall driving user experience.

The hybrid AI assistants segment is projected to grow at a CAGR of 20.0% during the forecast period. Growing adoption of AI-driven multi-functional systems combining voice, NLP, and personalization capabilities is driving demand, enabling smarter and more adaptive in-vehicle assistant experiences.

By Sales Channel

Strong Automaker Integration and Factory-Fitted Systems Drive OEM Demand

Based on sales channel, the market is segmented into OEM and aftermarket.

The OEM segment dominates the market due to the increasing integration of AI-powered in-vehicle assistants directly during vehicle manufacturing. Automakers are embedding advanced voice assistants, speech recognition, natural language processing, and AI-driven features to enhance user experience and differentiate offerings. Factory-installed systems ensure better performance, seamless compatibility with connected vehicles, and integration with advanced driver assistance systems (ADAS), thereby supporting strong market demand, higher market share, and sustained market growth globally.

- In March 2026, Ford launched Ford Pro AI, an embedded AI assistant within its telematics platform, enabling natural language interaction, proactive fleet maintenance insights, and data-driven decision-making to improve operational efficiency and vehicle uptime.

The aftermarket segment is projected to grow at a CAGR of 19.0% during the forecast period. Rising demand for upgrading older vehicles with AI-driven voice interaction and infotainment solutions is driving adoption, especially across emerging markets and existing vehicle fleets.

In-Vehicle AI Assistants Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America and Middle East & Africa.

North America

North America In-Vehicle AI Assistants Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest in-vehicle AI assistants market share, driven by early adoption of AI-powered automotive technologies and the strong presence of leading tech companies. High penetration of connected vehicles, advanced digital ecosystems, and premium vehicle demand support widespread integration of voice assistants and AI-driven systems. Continuous innovation in autonomous vehicles and ADAS further strengthens market growth. Additionally, strong consumer demand for enhanced user experience and cloud-based services sustains long-term market expansion.

- In October 2025, AWS introduced a multi-agent architecture for in-vehicle AI assistants using Strands Agents, enabling voice-driven interaction, real-time diagnostics, predictive maintenance, and seamless integration of vehicle data, enhancing intelligent and personalized driving experiences.

U.S. In-Vehicle AI Assistants Market

The U.S. market in 2026 is estimated at around USD 1.48 billion, accounting for roughly 29.0% of the global market revenues. Strong tech ecosystem, early AI adoption, and high demand for voice assistants drive market leadership.

Europe

Europe accounts for the second largest market share, supported by strong automotive manufacturing capabilities and an increasing focus on intelligent mobility solutions. Rising adoption of AI-driven systems in premium and electric vehicles is driving demand. Regulatory emphasis on vehicle safety and integration of ADAS encourages deployment of in-vehicle AI assistants. Additionally, growing investments in connected vehicles and digital infrastructure, along with demand for enhanced voice interaction and infotainment systems, contribute to steady market growth across major European economies.

- In January 2026, Volvo introduced the EX60 electric vehicle featuring advanced in-vehicle connectivity and AI, enabling natural conversational interaction, enhanced infotainment, and high-performance processing capabilities to deliver a more intelligent and seamless driving experience.

Germany In-Vehicle AI Assistants Market

The Germany market in 2026 is estimated at around USD 0.44 billion, accounting for roughly 8.5% of global market revenues. Strong luxury vehicle segment, ADAS integration, and automotive innovation drive sustained demand.

U.K. In-Vehicle AI Assistants Market

The U.K. in 2026 is estimated at around USD 0.21 billion, accounting for roughly 4.0% of global in-vehicle market sales. Growing EV adoption, digital ecosystems, and connected mobility solutions support steady expansion.

Asia Pacific

Asia Pacific is the third largest market and the fastest growing, projected to expand at a CAGR of 20.1% during the forecast period. Rapid growth in automotive production, especially in countries such as China, India, and Japan, is boosting market demand. Increasing adoption of connected vehicles, rising disposable income, and growing preference for AI-powered infotainment and personalization features are accelerating growth. Expansion of digital ecosystems and strong demand for advanced user experience further position the region as a key growth engine in the global market.

- In April 2026, Volkswagen announced the rollout of AI voice assistants in China-market vehicles, enabling onboard processing with local LLMs, enhancing voice interaction, personalization, and supporting its strategy to regain market share in electric and connected vehicles.

China In-Vehicle AI Assistants Market

The China market in 2026 is estimated at around USD 0.63 billion, accounting for roughly 12.4% of the global market revenues. Strong EV adoption, connected vehicles expansion, and AI-driven infotainment demand accelerate market growth.

Japan In-Vehicle AI Assistants Market

The Japan market in 2026 is predicted to reach at around USD 0.20 billion, accounting for roughly 3.9% of global market revenues. Advanced automotive innovation, premium vehicles, and a strong focus on autonomous technologies support steady growth.

India In-Vehicle AI Assistants Market

The India market in 2026 is projected at around USD 0.16 billion, accounting for roughly 3.1% of market revenues. Rising connected vehicle adoption, growing middle class, and demand for smart infotainment drive the fastest growth.

South America

South America represents the fourth largest market, with growth driven by the gradual adoption of connected vehicles and increasing awareness of AI-enabled automotive technologies. Rising demand for enhanced infotainment and voice assistants in passenger vehicles is supporting market expansion. Although the region is price-sensitive, growing urbanization and improving digital infrastructure are encouraging the adoption of AI-driven systems. Additionally, increasing penetration of smartphones and cloud-based services is helping expand the scope of in-vehicle AI assistants, contributing to moderate but steady market growth.

- In November 2025, ECARX expanded its partnership with Volkswagen Group to supply digital cockpit solutions with Google Automotive Services integration, enhancing voice interaction, infotainment, and user experience across multiple vehicle models in Latin America.

The Middle East & Africa

The Middle East & Africa market is witnessing emerging growth potential, supported by increasing adoption of premium vehicles and smart mobility solutions. Rising investments in connected vehicles and digital infrastructure are driving market demand for AI-powered assistants. Countries in the Middle East are focusing on advanced technologies and autonomous vehicles, enhancing the adoption of voice interaction and intelligent systems. In Africa, gradual digital transformation and expanding automotive markets are contributing to growth, although at a comparatively slower pace due to economic and infrastructure challenges.

- In November 2025, SelfDrive Mobility launched an AI-powered multilingual car rental assistant, enabling seamless booking, real-time personalization, and enhanced user experience across 40+ languages, transforming mobility interactions through intelligent voice and text-based automation.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Innovation, Voice Interaction, and Digital Ecosystem Expansion Drives Competitive Landscape

The market is moderately fragmented, with global technology giants and specialized AI firms competing for market share. Key players such as Amazon.com, Inc., Google LLC, Microsoft Corporation, Cerence Inc., SoundHound AI, Inc., and Apple Inc. focus on AI-powered voice assistants, speech recognition, natural language processing, and cloud-based integration. Companies are enhancing user experience through personalization, multilingual capabilities, and seamless connectivity. Strategic collaborations with automakers, continuous AI innovation, and expansion of digital ecosystems help strengthen competitive positioning. Increasing investments in AI-driven technologies and partnerships are shaping long-term market competition.

- In May 2024, Cerence collaborated with NVIDIA to develop its CaLLM automotive language model, enabling generative AI-powered in-vehicle assistants that enhance voice interaction, personalization, and overall in-car user experience.

LIST OF KEY IN-VEHICLE AI ASSISTANTS COMPANIES PROFILED

- com, Inc. (U.S.)

- Google LLC (U.S.)

- Microsoft Corporation (U.S.)

- Apple Inc. (U.S.)

- Cerence Inc. (U.S.)

- SoundHound AI, Inc. (U.S.)

- Nuance Communications, Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- Huawei Technologies Co., Ltd. (China)

- Baidu, Inc. (China)

- Alibaba Group Holding Limited (China)

- Tencent Holdings Ltd. (China)

- LG Electronics Inc. (South Korea)

- Panasonic Corporation (Japan)

- Continental AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Toyota and Woven by Toyota unveiled advanced AI technologies, including the AI Vision Engine and Integrated ANZEN System, to enhance mobility, safety, and real-time data integration at Woven City, accelerating AI-driven innovation.

- April 2026: Li Auto launched Amap’s Auto Mobility AI Agent, enabling advanced navigation, multi-turn dialogue, and personalized route planning, enhancing intelligent mobility interaction and transforming in-vehicle AI from passive tools to proactive assistants.

- January 2026: Visteon launched an AI-ADAS compute module powered by NVIDIA, enabling scalable AI-powered cockpit experiences and advanced driver assistance systems, supporting faster deployment of intelligent, software-defined vehicle features.

- January 2026: HERE Technologies launched an AI-powered portfolio for software-defined vehicles, integrating navigation, ADAS, and AI assistants to enhance user experience, accelerate development, and support autonomous and connected vehicle capabilities globally.

- December 2025: Rivian revealed development of an in-house AI assistant integrated with vehicle controls, focusing on an agentic framework and platform-agnostic architecture to enhance in-vehicle intelligence and user experience.

- October 2025: Hyundai Motor Group partnered with NVIDIA to build an AI factory using Blackwell infrastructure, enabling advanced in-vehicle AI, autonomous driving, and smart factory solutions, supported by a USD 3 billion investment.

- January 2024: Volkswagen announced the integration of ChatGPT into its IDA voice assistant via Cerence, enabling advanced voice interaction, infotainment control, and real-time information access across multiple EV and ICE models.

REPORT COVERAGE

The global in-vehicle AI assistants market analysis provides an in-depth study of the market size & forecast by all the market segments included in report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 18.4% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Application, By Vehicle Type, By Level of Integration, By Technology Type, By Sales Channel, and By Region |

| By Application |

|

| By Vehicle Type |

|

| By Level of Integration |

|

| By Technology Type |

|

| By Sales Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.26 billion in 2025 and is projected to reach USD 19.84 billion by 2034.

In 2025, the North America market value stood at USD 1.67 billion.

The market is expected to exhibit a CAGR of 18.4% during the forecast period of 2026-2034.

The passenger vehicles segment leads the market in terms of vehicle type.

Growing demand for enhanced in-car user experience drives market adoption.

Major players in the market include Amazon.com, Inc., Google LLC, Microsoft Corporation, Cerence Inc., SoundHound AI, Inc., and Apple Inc.

North America holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us