Industrial Centrifuges Market Size, Share & Industry Analysis, By Operation Mode (Batch Centrifuges and Continuous Centrifuges), By Product Type (Decanter Centrifuges, Disc Stack Centrifuges, Basket Centrifuges, Tubular Bowl Centrifuges, and Others (Peeler and Pusher Centrifuges)), By Design (Horizontal and Vertical), By End-Use Industry (Chemical, Food & Beverage, Pharmaceutical & Biotechnology, Wastewater Treatment, Oil & Gas, Mining & Metals, Pulp & Paper, and Power Generation), and Regional Forecast, 2026 – 2034

Industrial Centrifuges Market Size and Future Outlook

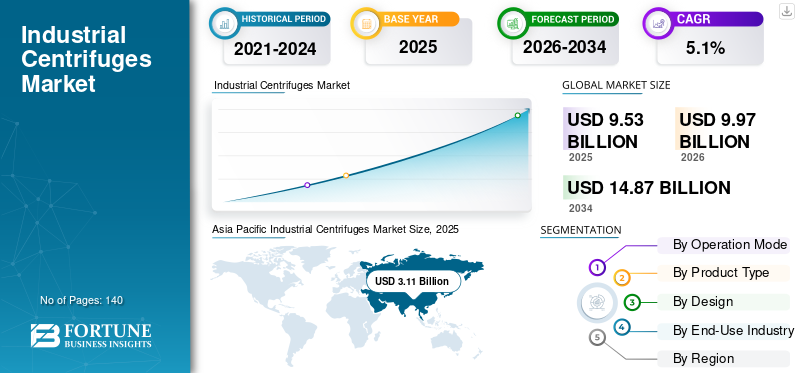

The global industrial centrifuges market size was valued at USD 9.53 billion in 2025. The market is projected to grow from USD 9.97 billion in 2026 to USD 14.87 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period. Asia Pacific dominated the industrial centrifuges market with a market share of 32.63% in 2025.

Industrial centrifuges are increasingly being adopted across process industries to enhance solid-liquid and liquid-liquid separation efficiency in high-volume industrial operations. These systems play a vital role in separating solids from liquids using high speeds, making them essential across applications such as wastewater treatment, chemical processing, food production, and oil refining. The growing need for efficient resource utilization and stricter environmental regulations is intensifying demand for high-performance centrifuge systems, including technologies such as sedimentation centrifuge designs. Industries are focusing on improving process efficiency, reducing waste generation, and enabling recovery of valuable by-products, which is driving the adoption of advanced centrifuge technologies such as decanter and disc stack systems. Increasing investments in industrial automation and continuous processing are accelerating the deployment of centrifuges that can operate with minimal manual intervention while maintaining consistent output quality. The global market is further supported by the expansion of wastewater treatment infrastructure and rising demand across the pharmaceutical and biotechnology industries. Growth trends remain strong across regions, particularly in the North America and Europe markets, where industries are prioritizing operational efficiency, regulatory compliance, and cost optimization.

- For instance, in February 2026, Alfa Laval introduced an upgraded decanter centrifuge platform featuring enhanced energy efficiency and improved solids handling capability, designed to support high-throughput separation processes in wastewater and industrial Designs.

Alfa Laval AB, GEA Group AG, ANDRITZ AG, Flottweg SE, and Mitsubishi Kakoki Kaisha Ltd. are among the key players holding a significant share of the market. Their competitive positioning is strengthened by strong expertise in separation technologies, the ability to deliver high-performance and design-specific centrifuge solutions, extensive global service networks, and continuous innovation in energy-efficient and automated systems to meet evolving industrial processing requirements.

Download Free sample to learn more about this report.

INDUSTRIAL CENTRIFUGES MARKET TRENDS

Rising Integration of Automation is Transforming Market Expansion

Demand for the product is increasingly being shaped by the growing need for higher separation efficiency and the ability to handle complex and variable feed compositions across wastewater treatment, chemical processing, food production, and mining industries. Operators are focusing on deploying advanced centrifuge systems equipped with automated control mechanisms, real-time monitoring, and intelligent process optimization features to improve separation performance and operational reliability. This shift is enabling facilities to achieve consistent product quality, reduce downtime, and optimize energy consumption in continuous processing environments. Increasing pressure to comply with stringent environmental regulations and improve resource recovery is driving investments in high-performance centrifuge solutions capable of efficient solids dewatering, liquid clarification, and by-product recovery. Industries are also prioritizing modular and scalable centrifuge systems that can be easily integrated into existing process lines while supporting capacity expansion. These advancements are influencing market dynamics as companies transition toward more automated and digitally connected processing systems that enhance efficiency, reduce manual intervention, and improve overall process control. Equipment manufacturers are responding by developing next-generation industrial centrifuges with enhanced automation capabilities, improved energy efficiency, and seamless integration with digital monitoring platforms, enabling more efficient and optimized separation operations across diverse industrial designs.

- For instance, in June 2025, GEA Group introduced an advanced decanter centrifuge system featuring automated process control and energy-optimized operation, designed to enhance separation efficiency and reduce operational costs in wastewater and industrial processing designs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Efficient Solid-Liquid Separation and Continuous Processing to Drive Market Growth

The industrial centrifuges market is witnessing strong growth as industries increasingly focus on improving separation efficiency and handling large volumes of process streams with greater precision and consistency. Sectors such as wastewater treatment, chemical processing, food and beverage, and mining are prioritizing advanced separation technologies to enhance throughput, reduce processing time, and ensure consistent product quality. The increasing complexity of feed materials, including high-solid-content sludge, variable chemical compositions, and mixed industrial effluents, is driving the need for high-performance centrifuge systems capable of reliable and continuous operation. The growing emphasis on resource recovery and waste minimization is encouraging the adoption of centrifuges that enable efficient solids dewatering, liquid clarification, and recovery of valuable by-products. As industries expand processing capacities and modernize infrastructure, there is a rising demand for systems that can operate under high-load conditions while maintaining operational stability and energy efficiency. Equipment manufacturers are responding by introducing advanced industrial centrifuges with improved separation efficiency, higher throughput capabilities, and enhanced integration with automated control systems, enabling end users to optimize performance and productivity across diverse industrial designs.

- For instance, in October 2023, GEA Group introduced its next-generation decanter centrifuge line with enhanced energy efficiency and optimized bowl design, aimed at improving sludge dewatering performance in municipal and industrial wastewater treatment

MARKET RESTRAINTS

High Capital Costs and Maintenance Requirements to Limit Market Adoption

The adoption of industrial centrifuges is often constrained by the high initial capital investment required for advanced separation equipment, precision-engineered components, and automated control systems. These systems involve complex mechanical designs, high-speed rotating assemblies, and wear-resistant materials, which contribute to elevated equipment costs. Additionally, integrating centrifuges into existing processing lines can be complex, requiring customization based on feed characteristics, operational requirements, and plant layout. The need for regular maintenance, including wear part replacement, balancing, and periodic servicing, further increases operational costs. Industries operating in cost-sensitive environments may face difficulties in justifying the investment, particularly where return on investment depends on processing volumes, efficiency improvements, and resource recovery. Furthermore, variability in input material properties, such as changes in solid concentration or particle size distribution, can affect separation performance and require continuous process optimization. These factors may limit adoption, especially among small and mid-sized operators, and can slow market penetration in emerging regions where technical expertise and infrastructure are still developing.

MARKET OPPORTUNITIES

Expansion of Municipal Wastewater Treatment Infrastructure Creating Strong Demand for the Product

An emerging opportunity in the industrial centrifuges market is the rapid expansion of municipal and industrial wastewater treatment infrastructure across both developed and emerging economies. Increasing urbanization, industrial discharge, and stringent environmental regulations are driving investments in advanced sludge management and water reuse systems. Centrifuges play a critical role in sludge dewatering, thickening, and volume reduction, enabling treatment facilities to improve efficiency and reduce disposal costs. Governments and utilities are prioritizing technologies that can handle high sludge volumes while minimizing energy consumption and operational footprint. Additionally, the shift toward water reuse and zero-liquid discharge systems is further increasing the need for reliable and high-performance separation equipment. Manufacturers are focusing on developing centrifuge systems with higher throughput capacity, improved solids capture rates, and enhanced automation to meet the evolving requirements of modern treatment plants. These developments are creating significant growth opportunities, particularly in regions investing heavily in water infrastructure modernization.

- For instance, in January 2024, ANDRITZ AG supplied advanced decanter centrifuge systems for municipal wastewater treatment projects in Europe, aimed at improving sludge dewatering efficiency and reducing overall disposal volumes.

MARKET CHALLENGES

High Energy Consumption and Process Optimization Requirements Impacting Operational Efficiency

A key challenge in the industrial centrifuges market is the relatively high energy consumption associated with continuous high-speed operation, which can significantly impact operating costs in large-scale industrial facilities. Centrifuges require substantial power input to maintain rotational speeds necessary for effective separation, particularly when processing high-density or high-solid-content feed streams. This makes energy efficiency a critical concern for end users, especially in regions with high electricity costs. Additionally, achieving optimal separation performance requires precise control of operational parameters such as feed rate, differential speed, and torque, which can vary depending on feed characteristics. Improper settings can lead to reduced efficiency, higher energy usage, and inconsistent output quality. The need for continuous monitoring and process optimization adds to operational complexity and requires skilled personnel. These challenges can limit efficiency gains and increase the total cost of ownership, particularly for facilities operating under tight cost and performance constraints.

Segmentation Analysis

By Operation Mode

Continuous Centrifuges Segment Led due to their Ability to Operate with Minimal Manual Intervention

By operation mode, the market is segmented into batch centrifuges and continuous centrifuges.

Continuous centrifuges held the largest industrial centrifuges market share as they are extensively deployed across industries such as wastewater treatment, chemical processing, food and beverage, and mining, where uninterrupted and high-volume separation processes are critical. These systems are designed for continuous feed and discharge, enabling efficient handling of large process streams while maintaining consistent separation performance. Their ability to operate with minimal manual intervention and deliver stable output quality makes them highly suitable for large-scale industrial operations. Additionally, continuous centrifuges offer improved operational efficiency, reduced processing time, and better integration with automated process lines, further supporting their widespread adoption. As industries increasingly focus on enhancing throughput and optimizing production efficiency, the demand for continuous centrifuge systems is expected to remain strong, reinforcing their position as the dominant segment within the market.

- For instance, in May 2024, ANDRITZ AG supplied advanced continuous decanter centrifuge systems for industrial wastewater treatment Designs, designed to improve sludge dewatering efficiency and support continuous high-capacity processing operations.

Batch centrifuges are the fastest-growing segment and are projected to expand at a CAGR of 5.8% during the study period. The growth of this segment is driven by increasing demand from industries that require flexible and controlled processing of smaller or variable feed batches, such as pharmaceuticals, specialty chemicals, and food processing. Batch centrifuges offer advantages in terms of operational flexibility, precise control over separation cycles, and suitability for designs involving frequent product changes or sensitive materials.

To know how our report can help streamline your business, Speak to Analyst

By Product Type

Decanter Centrifuges Segment Led, Driven by their Ability to Support High-Throughput Solid-Liquid Separation

By product type, the market is segmented into decanter centrifuges, disc stack centrifuges, basket centrifuges, tubular bowl centrifuges, and others (peeler and pusher centrifuges).

Decanter centrifuges held the largest share of the industrial centrifuges market, driven by their ability to support continuous, high-throughput solid-liquid separation across industries such as wastewater treatment, chemicals, mining, and food processing. These systems are widely adopted due to their capability to handle high solids content, variable feed conditions, and large processing volumes while maintaining consistent separation efficiency. Decanter centrifuges enable continuous operation with automated discharge of solids, making them highly suitable for large-scale industrial designs where operational efficiency and reduced downtime are critical. The demand is particularly strong in wastewater treatment and mining sectors, where effective sludge dewatering and solids handling are essential. Additionally, their robust design, operational reliability, and ease of integration into automated processing lines further support their widespread adoption, reinforcing their position as the leading segment within the industrial centrifuges market.

- For instance, in 2024, Pieralisi Group continued expanding its decanter centrifuge Designs in the food and environmental sectors, particularly in olive oil processing and wastewater treatment solutions.

Tubular bowl centrifuges are the fastest-growing segment and are projected to expand at a CAGR of 6.2%. The growth of this segment is driven by increasing demand for high-precision separation in Designs requiring the removal of very fine particles, such as pharmaceuticals, biotechnology, and specialty chemicals. Tubular centrifuges operate at very high rotational speeds, enabling superior clarification efficiency and separation of low-concentration suspensions that are difficult to process using conventional systems.

By Design

Horizontal Segment Led owing to their Widespread Use In High-Volume Industrial Designs

By design, the market is segmented into horizontal and vertical.

The horizontal segment held the largest industrial centrifuges market share, driven by their widespread use in high-volume industrial designs such as wastewater treatment, mining, chemical processing, and food production. These systems are designed to handle continuous feed with efficient solids discharge, making them highly suitable for processing large volumes of slurry and high-solid-content materials. Horizontal configurations, particularly decanter centrifuges, are widely preferred due to their robust design, operational stability, and ability to manage variable feed conditions while maintaining consistent separation performance. Their capability to operate continuously with minimal manual intervention enhances process efficiency and reduces downtime, further supporting their adoption across large-scale industrial facilities.

Vertical is the fastest-growing segment and is projected to expand at a CAGR of 5.9%. The growth of this segment is driven by increasing demand for compact and high-precision separation systems in industries such as pharmaceuticals, biotechnology, and specialty chemicals. Vertical centrifuges are particularly suitable for designs requiring high clarification efficiency and handling of low-solid or fine-particle suspensions.

By End-Use Industry

Chemical Segment Dominated due to its ability to Maintain Consistent Product Quality In Large-Scale Chemical Production

By end-use industry, the market is segmented into chemical, food & beverage, pharmaceutical & biotechnology, wastewater treatment, oil & gas, mining & metals, pulp & paper, and power generation.

Chemical held the largest share of the market, driven by the extensive use of separation processes across chemical manufacturing operations. Centrifuges are widely utilized for solid-liquid separation, liquid-liquid separation, and product purification in designs such as specialty chemicals, petrochemicals, and polymers. The demand is particularly strong due to the need for continuous processing, high throughput, and consistent product quality in large-scale chemical production.

Pharmaceutical & biotechnology is the fastest-growing segment and is projected to expand at a CAGR of 6.2%. The growth of this segment is driven by increasing demand for high-purity separation processes, particularly in designs such as biologics, vaccines, and active pharmaceutical ingredient (API) production. Industrial centrifuges are widely used for cell separation, clarification, and purification processes where precision and contamination control are critical.

Industrial Centrifuges Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Industrial Centrifuges Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market accounted for over USD 2.20 billion in 2025, supported by strong demand across wastewater treatment, chemical processing, food & beverage, and oil & gas industries in the U.S., Canada, and Mexico. Regional demand is closely linked to increasing investments in wastewater infrastructure, growing emphasis on environmental compliance, and the need for efficient solid-liquid separation across industrial operations. Industries are increasingly deploying advanced centrifuge systems to improve sludge dewatering efficiency, enhance product recovery, and reduce operational costs.

U.S. Industrial Centrifuges Market

The U.S. is expected to dominate the market, with an estimated revenue reaching around USD 1.76 billion by 2026, driven by its well-established wastewater treatment infrastructure, large-scale chemical and food processing industries, and increasing adoption of advanced separation technologies. Unlike many regions, U.S.-based operators are focusing on deploying high-efficiency centrifuge systems capable of handling large volumes of industrial and municipal sludge with consistent performance. The country is witnessing significant investments in upgrading wastewater treatment plants and industrial processing facilities to improve separation efficiency and meet stringent environmental standards.

Europe

The European market is driven by a strong focus on sustainability, advanced industrial infrastructure, and increasing adoption of efficient separation technologies across key economies such as Germany, the U.K., France, Italy, and the Netherlands. Demand for the product is closely linked to the region’s well-established wastewater treatment infrastructure, stringent environmental regulations, and growing emphasis on resource efficiency across industries. Organizations are increasingly investing in advanced centrifuge systems to improve sludge dewatering efficiency, enhance product recovery, and comply with evolving regulatory standards related to wastewater discharge and industrial waste management.

U.K. Industrial Centrifuges Market

The U.K. market is estimated to touch USD 0.37 billion by 2026, representing roughly 3.7% of global sales.

Germany Industrial Centrifuges Market

Germany’s market is projected to reach approximately USD 0.66 billion by 2026, equivalent to around 6.6% of global sales.

Asia Pacific

The region remains the fastest-growing regional market, generating revenue of approximately USD 3.11 billion in 2025. Asia Pacific continues to dominate the market, driven by rapid industrialization, increasing wastewater generation, and expanding chemical, food processing, and mining industries across key economies such as China, Japan, South Korea, and India. The region’s growth is primarily supported by rising investments in wastewater treatment infrastructure, growing emphasis on environmental compliance, and the need for efficient solid-liquid separation technologies to handle large and complex industrial process streams. China leads the regional market due to its large-scale industrial base and increasing adoption of advanced centrifuge systems in wastewater treatment and chemical processing sectors, while Japan and South Korea are characterized by high adoption of precision separation technologies and energy-efficient systems. Emerging markets such as India and Southeast Asia are witnessing growing deployment of industrial centrifuges as industries focus on improving process efficiency, reducing operational costs, and meeting evolving environmental and quality standards.

China Industrial Centrifuges Market

China’s market is projected to remain the dominant one in the Asia Pacific region, with revenues estimated to reach around USD 1.37 billion by 2026, representing roughly 13.8% of global sales.

Japan Industrial Centrifuges Market

The Japanese market is estimated to reach around USD 0.49 billion by 2026, accounting for roughly 4.9% of the global sales.

India Industrial Centrifuges Market

The Indian market is estimated at around USD 0.44 billion by 2026, accounting for roughly 4.4% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in wastewater treatment infrastructure, industrial diversification, and growing adoption of advanced separation technologies across key regions such as GCC countries, South Africa, Israel, and North Africa. Demand for industrial centrifuges is closely linked to the region’s efforts to improve water management efficiency, reduce environmental impact, and modernize industrial processing facilities across sectors such as oil & gas, mining, and wastewater treatment. GCC countries are investing heavily in water reuse, desalination, and sludge management projects as part of sustainability and resource optimization initiatives, supporting the deployment of high-performance centrifuge systems. South Africa’s demand is driven by mining and industrial processing activities requiring efficient solid-liquid separation, while North Africa is witnessing increasing investments in wastewater infrastructure. Israel represents a technologically advanced market within the region, with higher adoption of precision separation technologies across industrial and environmental designs.

GCC Industrial Centrifuges Market

The GCC market is projected to reach around USD 0.42 billion by 2026, representing roughly 4.2% of the global sales.

South America

The South American market is driven by growing industrial activities, increasing focus on resource efficiency, and gradual adoption of advanced separation technologies across key economies such as Brazil, Argentina, and Chile. Demand for industrial centrifuges is primarily supported by expanding wastewater treatment infrastructure, rising food processing activities, and strong mining operations across the region. Industries are increasingly deploying centrifuge systems to improve solid-liquid separation efficiency, optimize resource recovery, and reduce operational costs.

Brazil Industrial Centrifuges Market

The Brazilian market is projected to reach around USD 0.35 billion by 2026, representing roughly 3.5% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Technological Capabilities to Deliver High-performance Separation Solutions Across Diverse Industries

The industrial centrifuges market is moderately consolidated, with competitive positioning driven by technological capabilities, design-specific expertise, and the ability to deliver high-performance separation solutions across diverse industries such as wastewater treatment, chemical processing, food & beverage, and mining. Leading players such as Alfa Laval AB, GEA Group AG, ANDRITZ AG, Flottweg SE, and Mitsubishi Kakoki Kaisha Ltd. maintain strong market positions by offering advanced centrifuge systems capable of efficient solid-liquid and liquid-liquid separation under high-throughput industrial conditions.

Competitive differentiation is increasingly shaped by the ability to develop energy-efficient centrifuge systems with enhanced separation performance, improved wear resistance, and optimized operational reliability. As industries focus on improving process efficiency, reducing waste generation, and maximizing resource recovery, market players are investing in next-generation centrifuge technologies with advanced control systems, automated operation, and digital monitoring capabilities.

- For instance, in March 2024, Mitsubishi Kakoki Kaisha highlighted its industrial centrifuge systems for chemical and environmental designs, focusing on high-efficiency solid-liquid separation and stable continuous operation in large-scale processing facilities.

LIST OF KEY INDUSTRIAL CENTRIFUGES COMPANIES PROFILED

- Alfa Laval AB (Sweden)

- GEA Group AG (Germany)

- ANDRITZ AG (Austria)

- Flottweg SE (Germany)

- Mitsubishi Kakoki Kaisha Ltd. (Japan)

- Hiller GmbH (Germany)

- Pieralisi Group (Italy)

- SIEBTECHNIK TEMA (Germany)

- SPX FLOW, Inc. (U.S.)

- FLSmidth & Co. A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Pieralisi Group strengthened its industrial centrifuge applications in olive oil and food processing industries, focusing on improving extraction efficiency and product quality in continuous processing environments.

- October 2025: Hiller GmbH advanced its decanter centrifuge solutions for municipal and industrial sludge treatment, emphasizing improved dewatering performance and reduced operating costs.

- September 2025: SPX FLOW, Inc. highlighted its separation technologies, including centrifuge systems, for dairy and beverage processing Designs, aimed at enhancing product consistency and processing efficiency.

- August 2025: FLSmidth & Co. A/S focused on expanding its separation solutions for mining operations, with centrifuge-based technologies designed to support tailings management and water recovery processes.

- July 2025: SIEBTECHNIK TEMA emphasized its centrifuge systems for mining and chemical industries, designed to improve solids handling performance in abrasive and high-load processing environments.

REPORT COVERAGE

The global industrial centrifuges market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Operation Mode, Product Type, Design, End-Use Industry, and Region |

| By Operation Mode |

|

| By Product Type |

|

| By Design |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market stood at USD 9.53 billion in 2025 and is projected to reach USD 14.87 billion by 2034.

In 2025, North America’s market value stood at USD 2.20 billion.

The market is expected to exhibit a CAGR of 5.1% during the forecast period (2026-2034).

By end-use industry, the chemical segment led the market.

Rising demand for efficient solid-liquid separation and continuous processing is a key factor driving market growth.

Alfa Laval AB, GEA Group AG, ANDRITZ AG, Flottweg SE, and Mitsubishi Kakoki Kaisha Ltd. are the top players in the market.

Asia Pacific holds the largest market share.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us